2024 banking and capital markets outlook

Banks' strategic choices will be tested as they contend with multiple fundamental challenges to their business models. They must demonstrate conviction and agility to thrive.

Key messages

- A slowing global economy, coupled with a divergent economic landscape, will challenge the banking industry in 2024. Banks’ ability to generate income and manage costs will be tested in new ways.

- Multiple disruptive forces are reshaping the foundational architecture of the banking and capital markets industry. Higher interest rates, reduced money supply, more assertive regulations, climate change, and geopolitical tensions are key drivers behind this transformation.

Learn more

- The exponential pace of new technologies, and the confluence of multiple trends, are influencing how banks operate and serve customer needs. The impact of generative AI, industry convergence, embedded finance, open data, digitization of money, decarbonization, digital identity, and fraud will grow in 2024.

- Banks, in general, are on sound footing, but revenue models will be tested. Organic growth will be modest, forcing institutions to pursue new sources of value in a capital-scarce environment.

- Investment banking and sales and trading businesses will need to adapt to new competitive dynamics. Forces like the growth of private capital will challenge this sector to offer more value to both corporate and buy-side clients.

- Early 2023 shocks to global banking have galvanized the industry to reassess their strategies. While bank leaders focus on proposed regulatory changes to capital, liquidity, and risk management for US banks, there is much to be done to evolve business models.

{kind=link}

These challenges will result in divergent and sporadic economic growth. Some economies will face a brighter future, while others will still be fighting stickier inflation and low growth.

How will the macroeconomic environment in 2024 impact the banking industry?

Banks globally will face a unique mix of challenges in 2024. Each of these hurdles will impact banks’ ability to generate income and manage costs (both interest costs and operational expenses).

Deposit costs are here to stay—for now

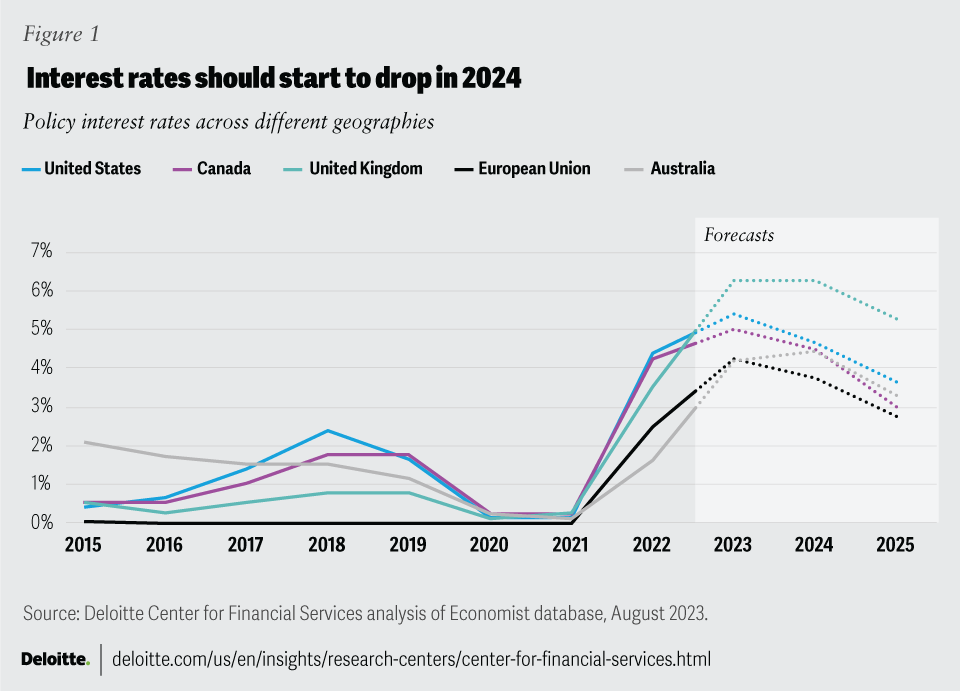

Higher interest rates have been a boon to the banking industry. In 2022, net interest income increased significantly in many jurisdictions, with American and Canadian banks posting a rise of 18% year over year (YoY), followed by their European peers at 11%.11

However, elevated rates will continue to push funding costs higher and squeeze margins. The pace and steepness of the current rate cycles have dramatically boosted the cost of interest-bearing deposits for US banks. But these costs have risen more sharply for regional and midsize banks. For instance, deposit costs for the largest banks stood at 2.2% in Q2 2023, compared to 2.5% for the smaller banks.12 This is a similar pattern in other countries that have experienced rate hikes.

Going forward, the global banking industry may be hard-pressed to bring down high deposit costs (and lower deposit betas) even as interest rates drop. Customer expectations of higher rates, coupled with increased market competition, will force many banks to offer higher deposit rates to retain customers and shore up liquidity. The situation will vary by region, though. European banks may be able to decrease deposit costs more rapidly, for instance. The European banking industry has not faced as much competition from money market funds, unlike in the United States. During the banking turmoil in March 2023, inflows into Europe’s money market funds totaled US$19.3 billion, dwarfing in comparison to US$367 billion into the US money market funds.13,14 Similarly, Asian banks, in India, for instance, may sustain higher rates in the wake of stronger economic growth. In fact, banks in the Asia-Pacific (APAC) region are expected to outpace global peers in generating stronger net interest income.

Loans growth will be modest, at best

In terms of loan growth, we expect demand to be modest given the macroeconomic conditions and high borrowing costs. Banks will also likely continue their restrictive credit lending policies. According to the recent bank lending surveys conducted by the Federal Reserve and the ECB, many banks have already tightened credit standards across all product categories. They anticipate further tightening due to a less favorable economic outlook and likely deterioration in collateral values and credit quality.15,16

However, the impact of the macroeconomic environment will be disparate across loan categories. Consumer spending has remained robust in major economies, but as consumer savings deplete, demand for credit card and auto loans should remain strong. At the same time, across the United States and Europe, bank loan demand from firms has decreased significantly. Bank loans to corporates may weaken in the short term but could pick up later in 2024. (See sidebar, “Real estate jitters” for commentary on commercial real estate loans.)

Real estate jitters

Residential mortgage origination in the United States may see a robust increase in contrast to other advanced economies such as the United Kingdom, Germany, and Australia. However, the commercial real estate (CRE) sector in the United States will continue to be stressed, and this will particularly affect regional and midsize banks that may be overexposed to office space. In light of higher uncertainty, inflated property prices, and concerns about debt repayments, banks will be more selective in their new CRE originations and refinancing. Banks could also be forced to realize losses on certain loan portfolios if there are fire sales or foreclosures at a large scale. CRE loan delinquencies are already rising. The delinquency rate (90+ days past due) in the United States has increased, from 1.84% in Q4 2022 to 3.3% in Q1 2023.17

The European CRE market appears to be more resilient than the US market. European CRE loans are largely concentrated among the larger banks that are well-capitalized.18 The APAC region is also expected to follow a smoother trajectory; demand from the hospitality sector should support growth in CRE loans, while multifamily residential mortgages will likely see a continued uptick.

Climate change should also play an important role in loan demand and credit availability. According to a recent EU Bank survey,19 over the next 12 months, banks expect a stronger credit tightening due to climate risks on credit standards for loans to “brown” firms, while a net easing impact is expected for green firms and firms transitioning to decarbonization. Firm-specific climate-related transition risks and physical risks should have a much larger role in credit disbursements going forward.20

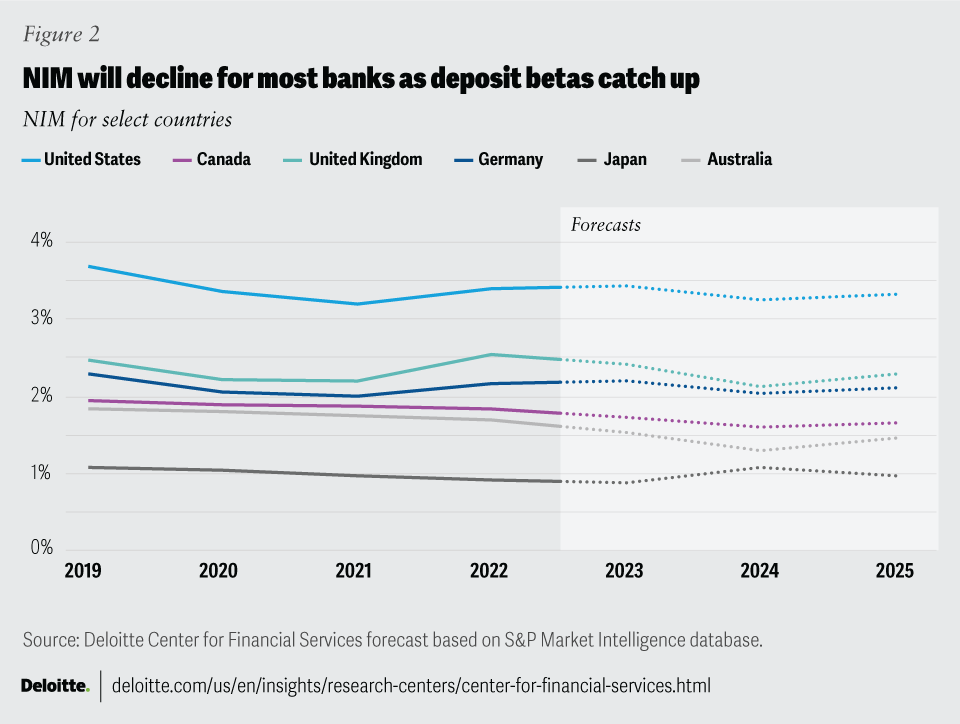

The combination of higher deposit costs, lower policy rates, and somewhat constrained loan potential can adversely impact banks’ ability to generate strong net interest margin (NIM) in 2024. In fact, banks’ NIMs may already have peaked, as suggested by recent bank earnings. US and European banks should experience a decline in net interest margins in 2024 (figure 2). APAC banks are more likely to enjoy stronger net interest income next year with a higher—and possibly rising—rate environment in many developing countries. These new factors will likely force banks to reassess the true cost of deposits and how they may be deployed.

{kind=link}

More noninterest income sources will be sought out

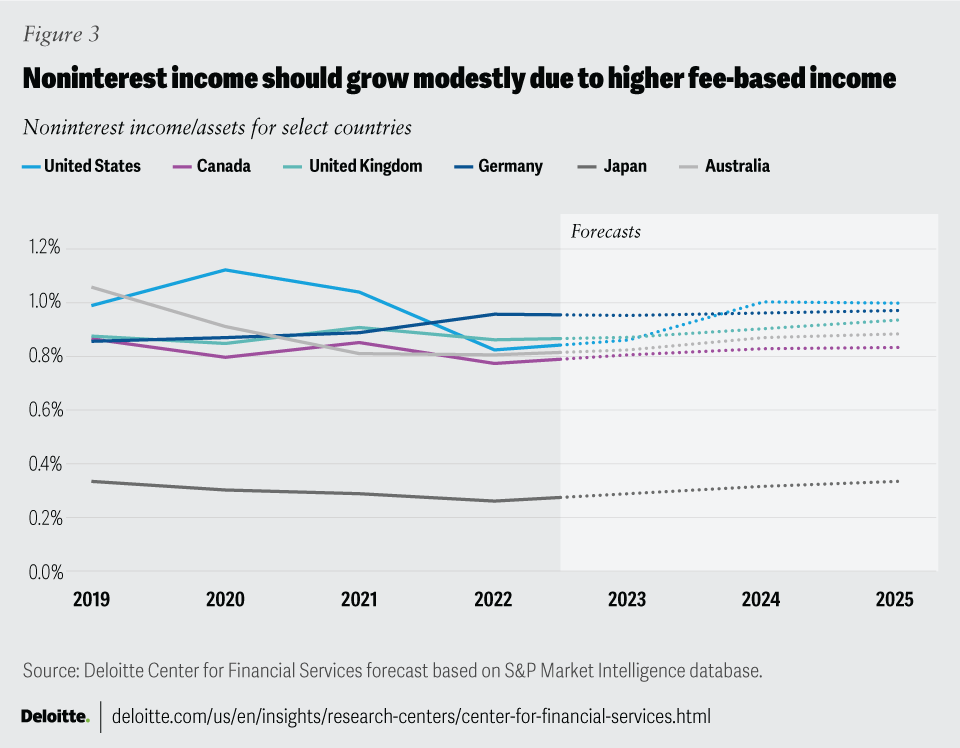

Banks should prioritize noninterest income in 2024 to make up for the shortfall in net interest income. Noninterest income is expected to grow meaningfully in the next few years (figure 3). Most banks will seek to raise fee income through a variety of channels, but they may face some constraints in doing so. Consumer-focused fees, such as overdraft fees, nonsufficient funds fees, and credit card late fees, could attract regulatory scrutiny.

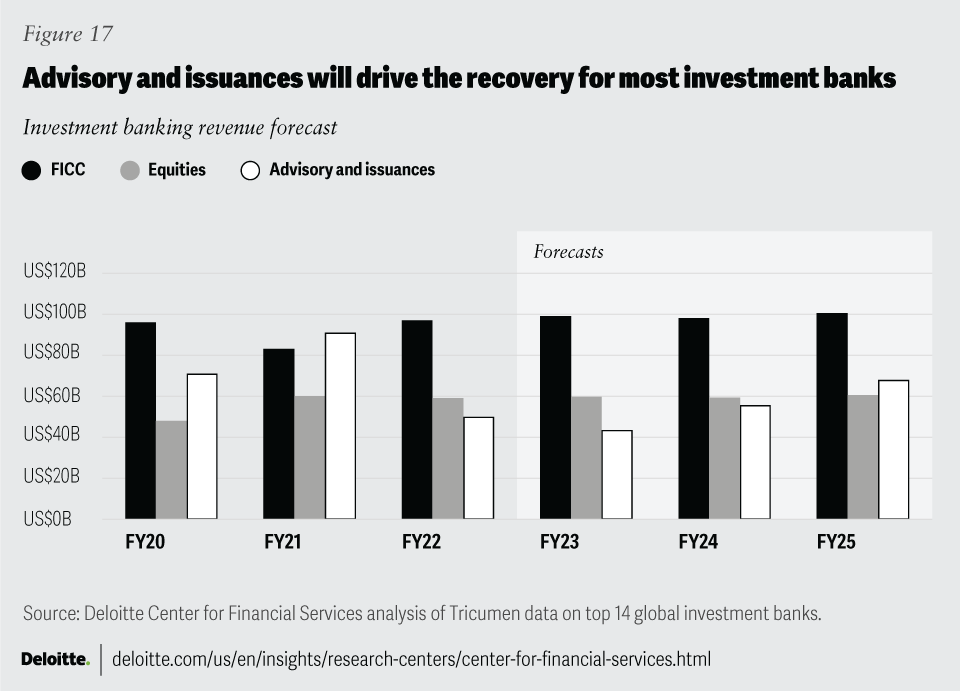

However, banks with stronger advisory, underwriting, and corporate banking franchises should have more room to grow their fee income. Clearer valuations and a backlog of deals should lead to higher M&A and issuance activities in the United States, boosting fees. However, reduced volatility across different products will crimp revenue growth in both equities and FICC (fixed income, commodities, and currencies) trading.

{kind=link}

Sharpening the cost discipline

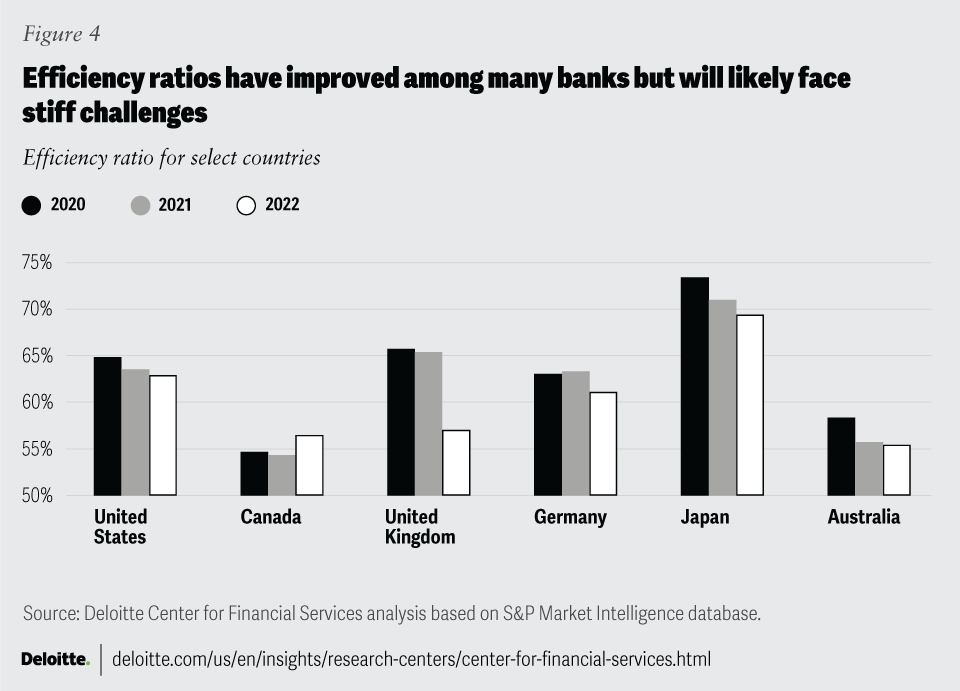

With the rising pressure on revenue generation, cost discipline will become even more of a priority, and possibly a competitive differentiator for banks. Efficiency ratio has been improving in the last few years globally (Figure 4), but it is expected to inch higher in 2024, due to sluggish revenue growth and high operating and compensation expenses. Many banks will also continue to invest in technology to remain competitive. Attracting talent in specialized areas such as artificial intelligence, cloud, data science, and cybersecurity should bump up compensation expenses, even as banks rationalize in other areas. In addition, tight labor markets and accelerated wage growth in traditional offshore locations should add to the industry’s cost pressures.

{kind=link}

Guarding against loan losses

In the first half of 2023, many banks raised their provisions for future credit losses, anticipating elevated loan defaults from a pandemic-era low. For instance, in Q2 2023, cumulative provisions for the top 10 US banks rose by 26% quarter over quarter (QoQ).21 Credit quality is expected to deteriorate as customers' ability to pay off loan diminishes, and the full impact of inflation and monetary tightening is felt by businesses and consumers. There is already evidence of rising delinquencies in certain loan categories, such as credit cards and CRE.22,23 Similarly, corporate default rates in the speculative grade may also increase.

While credit quality is decreasing and showing stress in specific segments, credit quality as a whole appears to be normalizing to prepandemic levels. Banks are continuing to build reserves to restore reduced balances over the last few years. Most large banks, globally, seem to have adequate liquidity and strong capital buffers to withstand a severe downturn, as evidenced by recent stress test results by the Federal Reserve, the ECB, and the Bank of England.24,25

US Basel III endgame implications

The US federal banking regulators recently released a notice of proposed rulemaking (NPR) on Basel III final reforms. The proposed changes are aimed at improving the “strength and resiliency” of the US banking system and will impact the regulatory capital frameworks for banks above US$100 billion in assets (about 36 banks). Smaller banks with significant trading activity will also be subject to the new risk framework. These changes are estimated to result in a 16% increase to CET1 (common equity tier 1) capital levels and a 20% increase to RWA (risk-weighted assets) for large bank-holding companies.26

Higher capital requirements are likely to disadvantage global banks domiciled in the United States and constrain lending, capital markets, and trading activities of all banks, possibly benefitting nonbanks and smaller institutions. These expansive changes, including the application of AOCI, G-SIB surcharge, and dual-RWA requirements, will lead to higher operational burdens, requiring significant investment in risk management, data, controls, compliance, and validation infrastructure.

The impact on banks with large recurring and fee-based businesses, such as credit card fees and investment banking fees, as per the Federal Reserve will be “exacerbated by the use of an internal loss multiplier that may result in an excessive overall capital charge for operational risk.”27 The new provisions will reduce fee margins for securities underwriting and could materially reduce the depth of banks’ products. This could further increase transfer of services and associated risks to nonbanks/unregulated sectors.

The new rules will also require banks to factor in unrealized gains and losses in capital ratios to comply with the supplementary leverage ratio requirement and the countercyclical capital buffer. In the short term, some banks may look at diminished buybacks. They could also impact investments in technology and market expansion strategies.

The Basel III NPR allows a transition period of three years, starting July 1, 2025.28 The proposed rules will undoubtedly evolve in the future, but it will be important for banks to assess existing internal infrastructure and potential strategic implications, and engage in continuous conversations with regulators.29

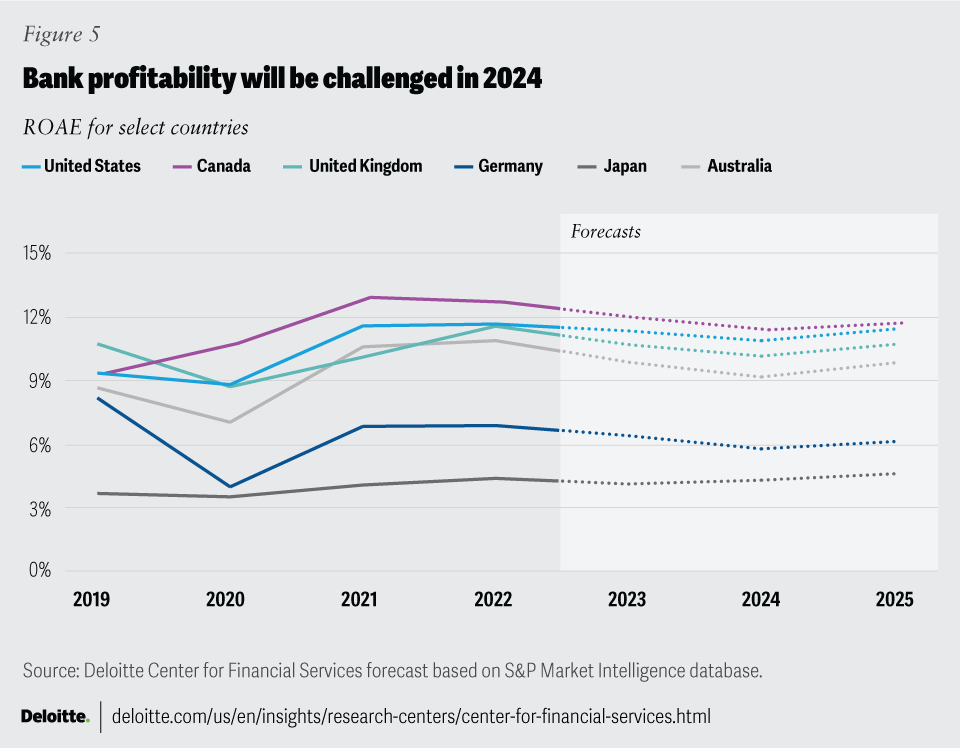

Bank profitability in many regions will be tested in 2024 due to higher funding costs and sluggish revenue growth (figure 5). However, banks with more diversified revenue streams and a strong cost discipline should be able to boost their profitability, and possibly their market valuation, more than most.

{kind=link}

The tilt toward Asia

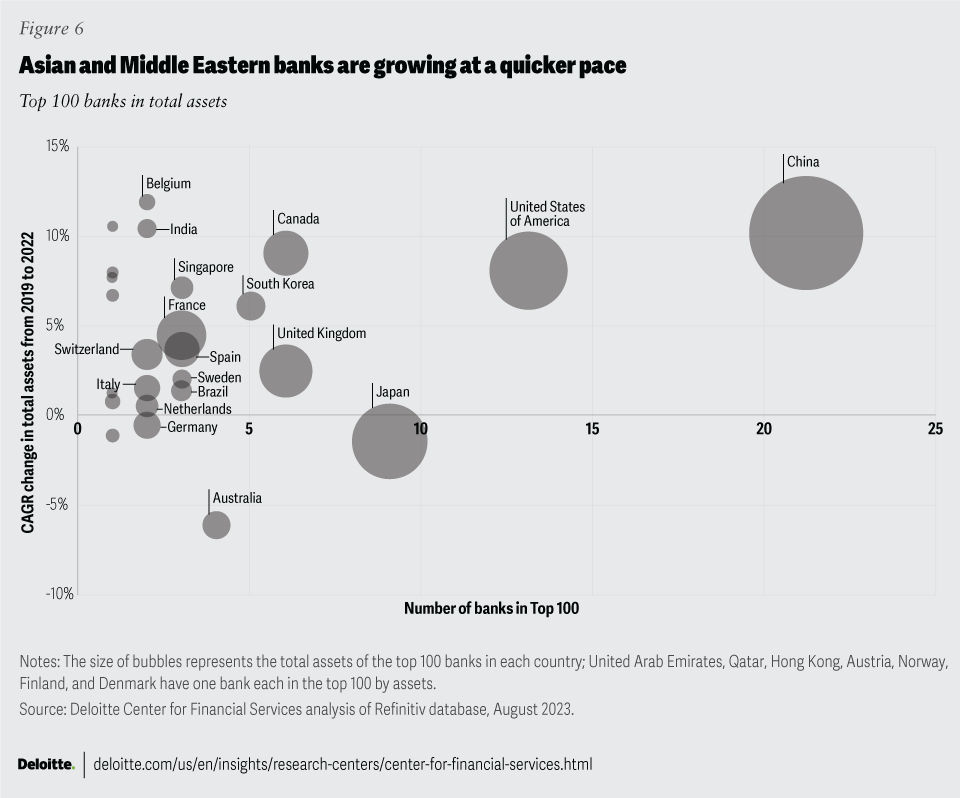

Going forward, the size and scope of global banking will change even more. The global banking industry has already seen fundamental shifts with Chinese and American banks dominating the global rankings. Figure 6 shows the changes in size (as measured by assets) and the number of banks from each country in the top global 100 banks. Over the next decade, more banks from India and the Middle East are expected to join the ranks of the top 100, tilting the balance toward Asia and the Middle East. Indian banks will grow their balance sheets as the economy grows and huge investments are made in domestic infrastructure, but they may struggle to break outside their domestic markets. Meanwhile, sovereign wealth funds in the Middle East will likely exert strong influence on global money flows.

{kind=link}

Forces shaping the future of the B&CM industry

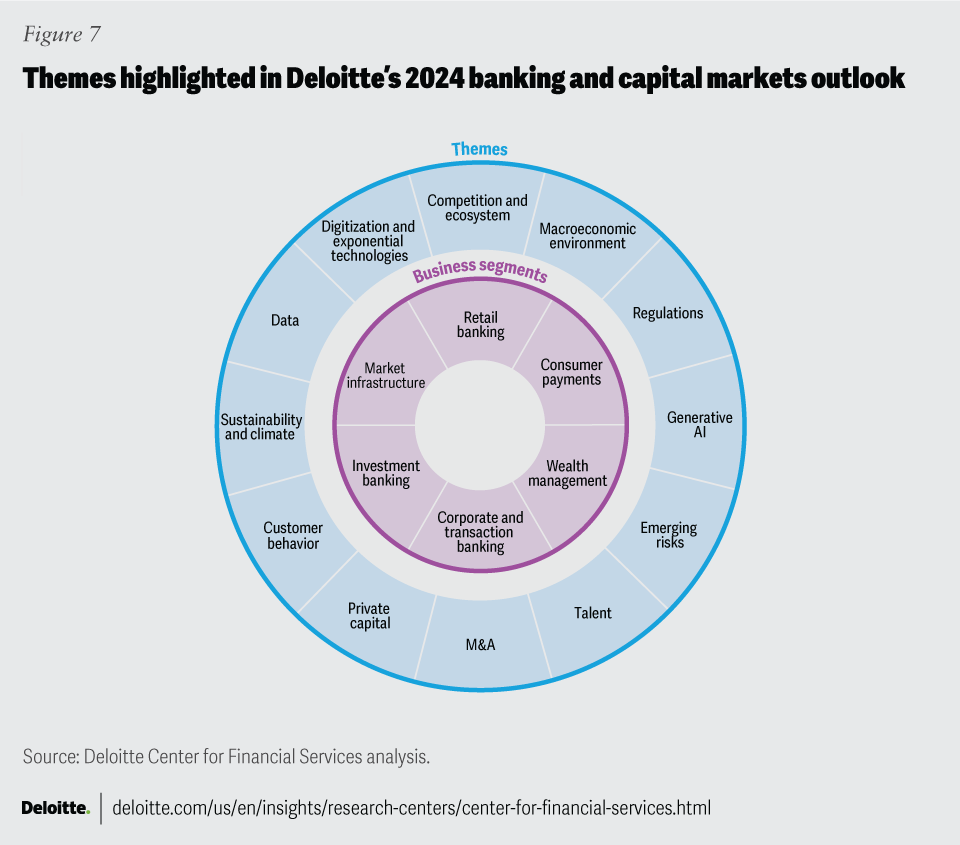

In addition to the macroeconomic factors highlighted in the previous chapter, the banking and capital markets industry must contend with various fundamental and disruptive forces challenging incumbent institutions’ business models in 2024 (figure 7).

{kind=link}

Not only are competitive dynamics shifting, but the pace and intensity with which rivals are challenging banks is unprecedented. Banks are now more intensely pitted against traditional and new rivals as more customers become open to having their needs met by nonfinancial institutions.

Deposits, for example, have become a ferocious battleground. Retail banks are competing with digital banks offering higher deposit costs. And in the payments arena, digital wallets and account-to-account payments are fast becoming the de facto payment options in many countries, while buy now, pay later (BNPL) is more widely accepted as a mainstream offering and alternative to credit card financing.

Capital markets and investment banking businesses are not immune to new competitive forces, either. Scale has helped bulge-bracket investment banks in the United States grow market share; however, a resurgence among European banks might be underway as they focus on specialized services, and boutique firms increasingly participate in bigger deals. Meanwhile, private capital could pose a greater threat for credit provisioning and talent. Hedge funds are also increasingly penetrating more of investment banks’ value chain. In market infrastructure, traditional exchanges see increasing competition from niche exchanges and the growth of trading venues in emerging markets.

At the same time, the relationships between banks, fintechs, and bigtechs are evolving rapidly. Fintechs are largely no longer seen as adversaries; collaboration with incumbents is now commonplace. With increasing industry convergence, strategic partnerships of banks with franchised brands in technology and other nonfinancial industries is becoming the norm for customer acquisition and retention.

Concurrently, customers are becoming more vocal about their evolving expectations. They want their banks to balance digital-first experiences without compromising the personal touch. Information is also becoming democratized, with technology and social media empowering customers in ways not seen before. Banks should heed these new demands as retail customers are spoiled for choice and many will be willing to switch accounts and diversify their relationships across multiple platforms with a tap on their smartphones. Younger consumers, in particular, are clamoring for a superior experience that some technology firms and fintech platforms offer. Wealth management clients are increasingly vocalizing their desire for omnichannel experiences at lower costs. And corporate and institutional customers, for their part, seem more intent than ever to broaden the number of banking relationships to diversify risk.

On the regulatory front, we continue to observe a divergence in laws and policies, with some jurisdictions typically charting a more assertive path, as in the EU’s new AI Act.30 As a result, there is still a lack of a coordinated, global approach to crypto, digital assets, data privacy, artificial intelligence, and even climate risk. But regulatory scrutiny is on the rise, with governments increasingly focusing on consumer protection, industry resilience, and open competition. More regulators and policymakers around the world are now probing banks’ lending practices and calling on them to do more to help consumers.

In addition, banks, particularly in the United States, could face stricter capital requirements under a proposed overhaul to capital rules as part of Basel III “endgame” starting July 2025.31 These rules could impact banks’ ability to support some capital markets activities, such as prop trading. They could also impede retail banks’ ability to lend in the residential mortgage space.

Regulatory pressures will be particularly acute for regional and small banks, especially those that are concentrated in their investment and lending portfolio and deposit mix. Many banks will spend the bulk of 2024 trying to tighten lending standards and diversify their balance sheets away from risky assets such as CRE loans and even safe assets such as long-term treasuries.

Meanwhile, open banking regulations in the United Kingdom, Europe, Australia, Saudi Arabia, Brazil, and Mexico are reducing the barriers for data sharing and offering customers more choice for financial products and services. The US Consumer Financial Protection Bureau (CFPB) is mulling similar rules.32 US consumer watchdogs are also sounding the alarm on the proliferation of artificial intelligence (AI)-driven chatbots in banking.

Scale and diversification, greater regulatory oversight, and the desire to shed low-yielding assets should drive further consolidation and M&A in the banking industry.

In the technology arena, it is hard not to get caught up in the excitement surrounding the incredible potential of generative AI. By all accounts, it can be a hugely transformative force. But more broadly, AI and automation are not new to banking. In fact, machine learning/deep learning algorithms and natural language processing (NLP) techniques have been widely used for years to help automate trading, modernize risk management, and conduct investment research. However, despite the billions of dollars spent on automating the various functions across the transaction life cycle, there are still a fair number of tasks that are conducted using precious human capital. But large language models (LLMs) could help automate many tasks, from generating marketing products to coding. Generative AI can not only save money, but also improve worker productivity. It could also free up resources to spark innovation and enable employees to focus more on productively interacting with clients.

Scaling generative AI will take time. In the short term, one of the biggest challenges in 2024 will be to determine the focus. In assessing the many potential use cases, leaders should choose the ones that will be the most impactful. The benefits of LLMs may not be uniform. They should also consider the potential ease of execution and any associated risks.

But for any of these technologies to have maximal impact, having the right data—and making sure it can be accessed and shared across the enterprise—will be key. While banks have been building out data capabilities for years, the pressure to derive insights to gain a more holistic view of customers has never been greater. There is a growing appetite among customers for real-time data about their payments, cash positions, trading, and valuations. In addition, advances in open banking globally are gradually eroding what was once traditional banks’ competitive edge. It is becoming increasingly important for banks to meaningfully harness both traditional and alternative datasets, as well as forge new partnerships with third parties, to create new value in the form of personalized insights, tailored product offerings, and enhanced customer experiences.

The proliferation of new technologies is opening banks to risks they may have never had to grapple with before. Open banking and the increase in partnerships with technology partners, for example, can expose banks’ infrastructure to new vulnerabilities and cyberattacks. Fourth-party risks are also becoming more of a threat as banks engage in more partnerships with service providers that have their own vendors. The speed with which these threats take shape is also accelerating. Generative AI has gained the sophistication needed to create “deepfakes,” which makes it more challenging for financial institutions to differentiate human customers from digital media imitating their likenesses. Collectively, this fast-moving risk environment is proving to be a huge obstacle to maintaining customer trust.

And, of course, one cannot ignore what climate change is already doing to our planet—the multiple heat waves, floods, and wildfires in the first half of 2023 are a precursor to what is likely to be the norm in the future. Banks, as key financial intermediaries, play an important role in bending the arc of climate change. But looking beyond, banks have a unique opportunity to support climate innovation through green finance and carbon markets. Not only can they provide early-stage financing to startups piloting carbon capture and storage and carbon dioxide removal technologies, but they can also help direct more capital to carbon project developers in emerging economies.

Finally, how well banks manage their talent will one of the most critical success factors in 2024 and beyond. The war for talent in technology remains a pressure point for many banks. Banks may have to pay dearly to hire specialized tech talent from outside businesses or train their own employees to become more tech savvy, especially as innovations from and within AI expand. Bankers should be empowered with the knowledge and resources they’ll need to adequately advise clients amid market uncertainties. As with other industries, banks may also have to instill a culture that reconnects employees with their corporate identity and creates a sense of belonging that can be a conveyed in a hybrid work environment.

To effectively deal with the forces outlined above, banks will likely have to make agility a fundamental attribute. Executives should be bold, decisive, and creative, yet remain true to their identity as financial intermediaries.

In the following chapters, we highlight how these themes will impact specific segments within banking and capital markets, including retail banking, consumer payments, wealth management, corporate and transaction banking, investment banking, and market infrastructure.

Retail banking: Fortifying customer relationships and owning a greater share of wallet

Priorities for retail banks in 2024 and beyond

Retail banking businesses will not only grapple with higher funding costs and slower loan growth, but they must also contend with declining loyalty and increasing customer defections. While deposit flows should stabilize, it will likely remain challenging to contain deposit costs even as policy rates decline. Banks should also expect new rules and regulations in the form of higher capital and liquidity requirements, as well as heightened scrutiny of risk modeling. In addition, weakening household finances will continue to pressure banks’ loan books, prompting further credit tightening.

Retail banks should find new ways to forge deeper customer relationships and instill a greater sense of financial empowerment. Personalization will be key to demonstrating lifetime value. But banks will likely struggle to customize products and services due to legacy systems and their inability to curate tailored experiences using customer data. They should strive to adopt advanced modeling tools that generate predictive insights and enable the delivery of real-time financial advice. Banks should also look at how emerging technologies can improve risk, compliance, and operations tasks in addition to enhancing the customer experience. For example, they can consider how generative AI may accelerate credit risk assessments, instantly alert mortgage applicants to missing or incomplete documents, and boost the productivity of customer-facing teams.

Retail banks are grappling with a confluence of pressures, including higher funding costs, growing competition from digital banks, and surging demand for increasingly personalized services, even as they explore how best to deploy generative AI and strengthen their data analytic capabilities. Many of these challenges will be exacerbated by the fact that retail customers are spoiled for choice, and it has become easier for them to switch accounts and diversify deposits across multiple platforms. In addition, the growth of embedded finance and open banking are changing the face of retail banking as customers know it.

While deposit outflows largely stabilized after a turbulent first half of 2023, many challenges persist. On the lending side, higher rates continue to lower borrowers’ appetite, leading to slower pace of growth for new loans and refinancing. Retail customers are running behind on payments, causing more auto, credit card, and consumer loans to head into delinquency. Banks around the world are increasing their buffers to prepare for a higher rate of defaults. Canada’s five biggest lenders, for example, boosted their YoY loan loss provisions 13-fold in the first three months of 2023.33 Banks will likely tighten credit further heading into 2024 and may even look to sell subprime auto loans and riskier home equity loans to strengthen their balance sheets.

These mounting challenges will have disparate impacts on retail banks in 2024. Which banks will be strained the most, and how can they reposition their business models to deliver more value to their customers? What other opportunities may be available for banks to recapture customer loyalty and serve customers beyond the point of transaction?

The fight for deposits will continue

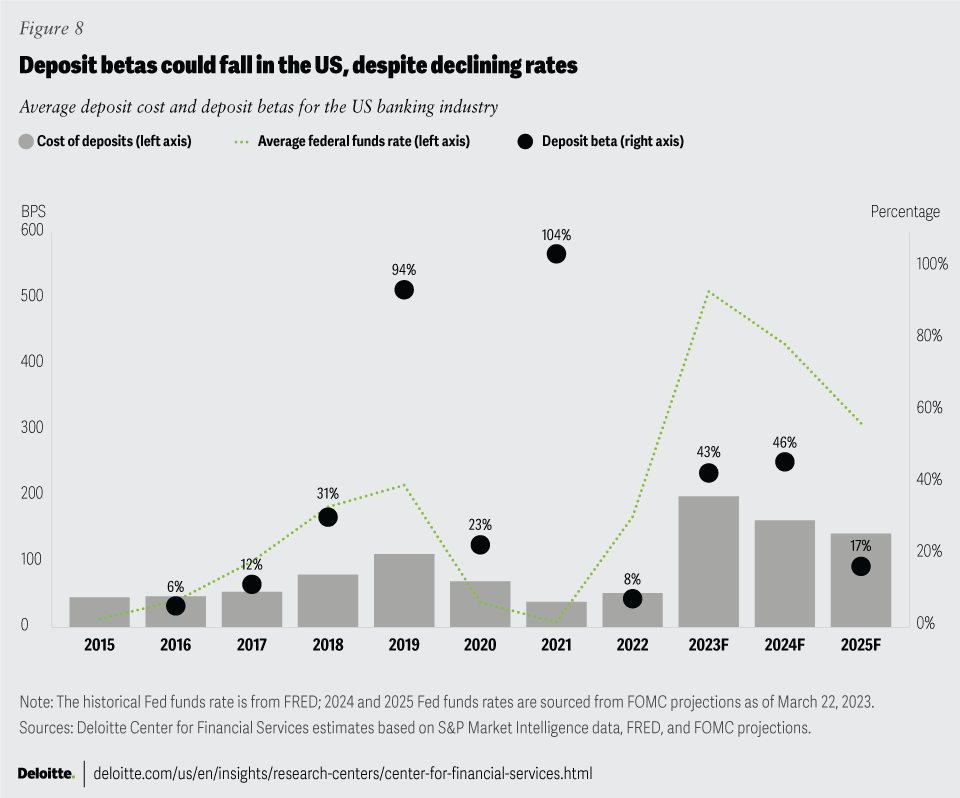

Although deposit flows stabilized in Q2 2023, banks will incur increasingly higher costs to retain deposits. For instance, the cost of interest-bearing deposits (including certificates of deposit, money market deposit accounts, and savings deposits) in the United States rose by 192 basis points to 2.1% by the end of 1H 2023, up from 0.2% a year ago.34 This trend accelerated in the wake of bank failures, when the goal of retaining deposits became even more paramount. Going forward, the industry should be hard-pressed to bring down their deposit costs even as the policy rate declines (figure 8).

{kind=link}

Retail customers are demanding higher rates on their deposits, and many have already switched their cash into higher-yielding time deposits.35 Some US brokerages are beginning to chase “held-away cash” at retail banks with new services through higher yields.36 Digital banking is also contributing to this phenomenon. Digital-only banks, for instance, will likely continue to offer higher CD rates; they are also offering variations on typical features such as a CD with no early withdrawal penalty. Several online banks, such as Ally Financial and Goldman Sachs’ Marcus, bucked the deposit exodus trend experienced by some regional and midsize banks and grew their deposit base during the first half of 2023.37 These digital-only banks and fintechs backed by traditional banks joined large traditional banks as the winners of March 2023’s flight to safety.38 Choice Financial Group, which sponsors the fintech Mercury, saw 17% deposit growth that quarter. SoFi and Varo Bank each had 37% and 43% quarterly deposit growth, respectively.39

Similarly, European car manufacturers are increasingly looking for alternative sources of funding for auto loans, given the soaring costs of corporate bonds and asset-backed securities. As a result, they are also emerging as rivals to traditional banks.40 These automobile companies are luring depositors with higher interest rates for deposits and money in savings accounts.41

European customers are also increasingly withdrawing money from banks in search of better terms due to some lenders’ reluctancy to pay more to retain deposits they believe they can do without. Most of Europe's largest banks reported net deposit outflows year over year for the first quarter of 2023.42 Money market funds are also popular with European savers seeking a higher return on their cash in the face of persistently high levels of inflation.

New rules and regulations will also pressure retail banks. In particular, higher capital and liquidity requirements, a reevaluation of assumptions about deposit stickiness by supervisors, and closer scrutiny of how capital and deposit dynamics should factor into banks’ risk modeling will be priorities on the regulatory agenda. Recent events have also reiterated the importance of scale and stability. Some banks may not have the appetite to remain below certain asset thresholds. As a result, more M&A activity within the banking industry is likely. Entities with sticky deposits that lack strong lending platforms may be particularly attractive targets during any upcoming wave of consolidation.43 Some midsize and regional banks could also seek mergers that will bring in enough outside capital to enable the sale of low-yielding assets.44

Banks should take steps to remind customers of the value they provide beyond deposits by broadening the conversation to include additional avenues of support, such as wealth management and insurance services. They should also use data analytics to identify at-risk account holders and create custom product and pricing solutions that may be preferable for their unique circumstances.45

Lending pressures will continue to weigh on banks

Higher rates, persistent inflation, and weakening household finances will continue to pressure banks’ loan books. While many banks have been buoyed by net interest income, potential rising delinquencies and loan loss reserves should start to impact profitability more. The return of student debt payments in the United States will also add more financial stress and impede spending at a time when many consumers are struggling with the higher cost of living. As a result, it will be increasingly important for banks to actively engage with customers and pivot to an advice-based model to help these customers manage their debt.

US banks should also anticipate slower growth and prepare for a rise in consumer loan defaults. Some banks have started to reduce their exposure to home lending as mortgage originations fell to their lowest point in 20 years, dropping 56% between the first quarters of 2022 and 2023.46 In addition, large lenders could soon face stricter capital requirements under a proposed overhaul to bank capital rules by US banking regulators.47 These changes may impact banks’ ability to lend to first-time and underrepresented homebuyers.48

Demand for mortgages and consumer loans in Europe are also expected to falter, while tightening credit standards could constrain spending and growth.49 Meanwhile, APAC is also struggling with anemic loan demand, prompting many banks to consider new sources of revenue. Banks in Mainland China, for example, are trying to spur demand for mortgages by offering relay loans for elderly borrowers that are inherited by children if they cannot pay, as well as joint loans for unmarried couples.50 Australia’s major lenders are also beginning to divert resources away from residential mortgages and are weighing moves into other businesses, such as commercial loans.51

Regulators and policymakers around the world are also increasingly scrutinizing banks’ lending practices and calling on the sector to do more to help consumers. The Consumer Financial Protection Bureau is focusing on banking “junk fees” and working to make mortgage servicing and auto lending less risky for borrowers.52 Meanwhile, a new UK regulation will bring more transparency to mortgage lending,53 and South Korea has made it easier for new entrants to compete with large lenders.54

Banks should also take steps to help improve their credit risk models by making them more inclusive with the addition of more alternative data. Rent payment history, gig economy income, and utility bill payments may help credit invisibles: consumers with limited information to demonstrate creditworthiness. In addition, they can develop more embedded finance tools in lending processes, such as adding technologies that enable instant loan approvals at an auto dealership.

Empowering customers and reimagining loyalty

Global banks can’t solely rely on brand recognition to grow their customer base. They should take greater steps to redefine what customer loyalty looks like and forge deeper relationships by supporting and empowering customers.

Banks should strive to be the go-to hub for most of consumers’ financial needs, especially as economic uncertainties weigh on customers more heavily over the coming year. Only 21% of customers surveyed say they’ve received guidance or advice from their primary bank between January 2022 and January 2023, even though the financial health of many Americans dropped markedly in that period.55 Customers who received advice and felt it met their needs were more likely to reward the bank accordingly: About half opened a new account with that institution.56

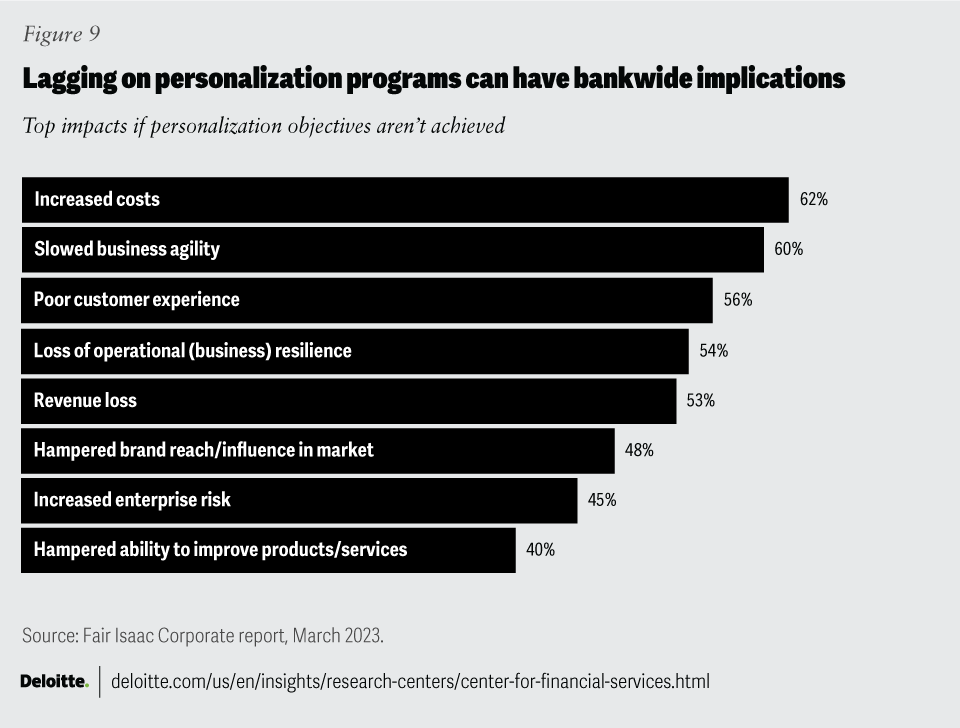

Banks should look for where they can use customer data to personalize experiences and deepen customer lifetime value. This has been a priority for global banking leaders for some time, but personalization efforts have been hampered by legacy systems, data privacy concerns, lack of data, and the inability to harness data fully to curate tailored experiences. As a result, two out of three banks report they are unable to assess the context of a customer’s situation outside of a single moment in time.57 This inability is not only detrimental to the customer experience; it can also hinder financial performance and fraud detection (figure 9).

{kind=link}

Banks should increasingly invest in advanced modeling tools that can parse through transaction data and deliver predictive insights at multiple customer touchpoints. They can also use emerging AI capabilities to provide richer and more targeted advisory services. Over time, banks should seek to advance hyperpersonalization to the point that customers feel they are a segment of one.58 For example, if a bank sees that an aspiring borrower abandoned a mortgage application to check out other lending platforms, it may dispatch an advisor to contact the applicant with a more competitive rate and offer of personalized support.59

Banks should also shift away from a product-focused business model to become a consumer-centric organization. As industry lines blur, and customer expectations are influenced by experiences in other domains, customers are increasingly expecting banks to replicate the services they get elsewhere. Some are also becoming more comfortable having their needs met by nonfinancial institutions. Bank leaders can learn from customer interactions with entities outside of banking and consider new opportunities to serve them in a more unique or holistic way. Northwestern Mutual, for example, took a page out of a dating app playbook to design a matchmaking algorithm that pairs customers with financial advisors that are best suited for their needs.60

Strategic partnerships with franchised brands can also be a powerful tool for customer acquisition and retention, especially if the bank works with third-party institutions to deliver custom rewards. For example, hundreds of music fans shared plans on social media to apply for a Capital One card to gain access to presale tickets for a popular 2023 concert tour.61 These nontraditional, nonbanking perks are beginning to play a greater role in customers’ choice of a primary financial services provider. However, such brand sponsorships could also come with some risks.

Forging ahead with tech advances and innovation

Banks should also seize opportunities to use emerging technologies to reduce risk, streamline operations, and build trust with customers by offering new safeguards from fraud. For example, open banking initiatives that give customers more control of their finances are gaining steam in many parts of the world. Regulators and central banks continue lowering the barriers for data sharing in the United Kingdom, Europe, Australia, Saudi Arabia, Brazil, and Mexico. The US market may also usher in a wave of open banking soon, as the CFPB mulls a new rule to give customers more rights over their personal data. The rule could open the door for third-party firms to seek consent for access to customer data through application programming interfaces (APIs), and provide more tailored services such as budgeting, financial management, and lending. This could also help large banks obtain data from other institutions, such as community banks and credit unions, which may be useful for growing their own business lines.62

Banks can also develop new methods for issuing and authenticating digital identity, especially as more deepfakes emerge that take on the likeness of real or fabricated humans. Greater adoption of digital wallets is also heightening the need for safeguards. In the Nordics and Canada, many financial institutions garnered a great deal of goodwill and trust by advancing BankID and Interac Verified systems,63 demonstrating their role as credibility agents in the digital economy. Biometrics, including behavioral biometrics that analyze a consumer’s touchscreen behavior, mobile app navigation, and typing habits, will also become more and more pivotal in the fight against fraud.

In addition, in the near term, generative AI will have many benefits for risk, compliance, and operations functions. For instance, banks are evaluating how the technology can improve mortgage applications by performing faster and more accurate underwriting processes and enabling conversational AI tools to instantly alert borrowers to missing or incomplete documents.

Some banks are launching pilots to learn how they can better assist customers with the nascent technology. ABN Amro in the Netherlands, for example, is using generative AI with 200 employees to summarize their conversations with customers. It is also testing how it can gather customer data to resolve issues in real time.64 Sweden’s Klarna Bank has equipped every employee with access to generative AI language models and asked them to experiment with the technology.65 JPMorgan Chase estimates that these tools will generate an additional US$1.5 billion in value by the end of 2023.66 Its retail bank has found success in using AI to extend customized offerings, such as credit card upgrades.67

Financial institutions are still reluctant to embed AI into customer applications since it can bring about new exposures to ethical and security risks. In the United States, the CFPB warned that banks using generative AI may not be providing “timely, straightforward" answers to user questions, and expressed concern about the tools’ ability to comply with consumer protection laws.68 But as banks learn to use generative AI safely, they can make chatbots more sophisticated and easier to understand, deliver personalized marketing campaigns customized to each target’s content consumption habits, and reduce wait times for processes such as mortgage lending.

Consumer payments: Grabbing a bigger slice of the revenue pie in a fast-evolving ecosystem

Priorities for payments institutions in 2024 and beyond

2024 will see an acceleration of several trends shaping the future of the consumer payments industry. Consumer spending will increasingly shift from cash to digital payments. However, growth in digital and real-time payments, along with the proliferation of artificial intelligence, will also make fraud and cyber threats more challenging to prevent and detect.

Governments, especially in developing economies, will play a more prominent role in consumer payments by expanding financial inclusion, reducing inefficiencies, and fostering competition. The trio of regulatory, market, and competitive forces will further challenge the economics of the volume-focused business models. Many incumbent institutions recognize they need to deliver new value beyond transaction execution to remain relevant, as the traditional boundaries in the payment ecosystem blur.

Use of proprietary and alternative data and more robust analytical models should enable institutions to better understand consumers’ needs and offer more personalized insights. They should engage collaboratively with the ecosystem but choose the right third-party providers (TPPs) that consumers trust to lessen concerns around security and privacy. Investing in technology talent and using sophisticated AI and biometrics technologies could help incumbents strengthen fraud detection models and protect consumer payments and data from malicious actors.

The world of global consumer payments is evolving rapidly, driven by a multitude of factors. Digital wallets and faster payment rails are pushing traditional payment methods further into the background. However, use of credit cards has stayed resilient and BNPL has further democratized access to credit at the point of sale, both in-store and digitally. Governments are actively pushing the bar on financial inclusion with digital faster payments, such as Instant Payment Platform in the United Arab Emirates and Unified Payments Interface (UPI) in India.69

However, the shift from cash to digital payment methods shows a divergence in maturity levels across countries and regions. Countries, such as Norway and the Netherlands, have been trailblazers in the use of digital payments in the developed world for some years now. Joining them are China, India, and Brazil, leading the digital payments revolution from developing economies. Meanwhile, many countries in Europe and Asia-Pacific, despite their sizable economies, are a bit behind in the use of cashless payments.70

Despite these differences, the resilience in consumer spending, especially in travel, has translated well for card issuers and payment networks. JPMorgan Chase reported a 7% increase in credit and debit card transactions and an 18% rise in card loans in Q2 2023, largely attributed to its US volumes.71 Similarly, Mastercard reported a 12% YoY growth in global gross dollar value of transactions to US$2.3 trillion in Q2 2023, attributed largely to international travel and cross-border spending.72

However, consumers are acquiring more debt, thus increasing the credit risk for issuers. Credit cards remain the dominant payment method for American consumers, encompassing 31% of payments in 2022.73 US consumer credit card debt surpassed US$1 trillion in Q2 2023, reaching a new peak since 2003.74 In the same quarter, the 30+ day credit card delinquency rate climbed to 7.2%, a level last seen more than a decade ago in 2012.75 The moratorium on US student loans ending in September 2023 could further deplete consumers’ savings and constrain their ability to pay their credit card dues on time.

Concurrently, institutions in the card value chain must also grapple with the changing economics of their business models. For instance, regulators in the United States plan to reduce card swipe fees. Meanwhile, national governments are building sovereign card rails and forging bilateral deals to bring more efficiencies to domestic and cross-border payment flows. Debit volumes are under pressure with a rise of account-to-account–based real-time payments networks. Meanwhile, software players are bringing payments in-house, eating into the revenue of merchant acquirers.

Given these mixed dynamics, what should payments institutions do to increase their share of the revenue pie in 2024 and beyond? How can they reimagine value creation and delivery to remain relevant to consumers and bolster their competitiveness?

Economics of card swipe fees face a new threat

Card networks have faced pressure from retailers to lower card swipe fees for some years now, but this issue is finding a new voice in lawmakers’ reform agendas across different jurisdictions.

In the United States, the Credit Card Competition Act (CCCA), reintroduced in Congress in June 2023, proposes more network choices for merchants to further reduce swipe fees.76 Some retailers are passing on part of this cost to consumers by imposing a surcharge on credit card transactions. Lawmakers are hoping that additional competition will result in lower cost to retailers, and ultimately, to consumers in the form of lower prices.

But if this law is passed, it could hamper the ability of incumbent payments networks and card issuers to offer attractive rewards to consumers, which are largely financed by swipe fees. The restriction on swipe fees could also reduce issuers’ incentives to issue cards to consumers with inadequate access to credit.

It is also not clear how much retailers’ savings would ultimately be passed on to consumers, if at all. But increased price competition would put an additional strain on issuers and networks’ transaction revenues and the card products they offer to consumers.

Swipe fees are not a burning issue in Europe, but in other countries, such as India, there is a renewed focus on expanding competition. For instance, the Indian central bank has mandated that card issuers must issue their cards on more than one network beginning in October 2023.77 The move will end exclusive issuance arrangements between card networks and leading issuers.

Government-backed payments systems cause further fragmentation

After building their sovereign card rails to reduce dominance on the international payment plans, national governments are exploring modernizing consumer payments to make them more convenient and cost-effective for their citizens. More than 70 countries have adopted real-time payments (RTP) rails, with many solutions having government endorsement and support. Public-sector involvement is equally important in addressing inefficiencies in the ~US$650 billion global remittance market.78 According to the World Bank, the global average cost of sending US$200 in remittance across borders was as steep as 6.25% of value in Q1 2023, falling disproportionately on the poor.79 The average cost of remittance remains more than twice the United Nations Sustainable Development Goals target of 3%, which is to be reached by 2030.80

While hopes for a ubiquitous and efficient cross-border remittance solution are still alive, national governments are initiating bilateral arrangements to make their domestic RTP systems interoperable across borders one country at a time. India and Singapore have linked UPI and PayNow, their respective faster payment rails, to enable quick and low-cost fund transfers.81 More recently, India signed a deal with the UAE’s Mashreq Bank to use UPI to facilitate foreign remittances from the India diaspora in the region.82

Europe also plans to create a unified instant payments solution with its European Payments Initiative, a new payment standard for European consumers and merchants for all types of transactions, including in-store, online, cash withdrawal, and peer-to-peer (P2P).83 Set to launch in Belgium, France, and Germany in 2024, this initiative aims to offer a pan-European bank card, digital wallet, and P2P payments solution to consumers for lower friction in cross-border payments.

An increase in such bilateral deals and regional initiatives would make the global payments landscape more fragmented and create different regional payment blocs. Yet, encouragingly, we are inching closer to a more efficient cross-border payments system, one payment bloc at a time.

The blurring of product lines and competition for customers’ wallets

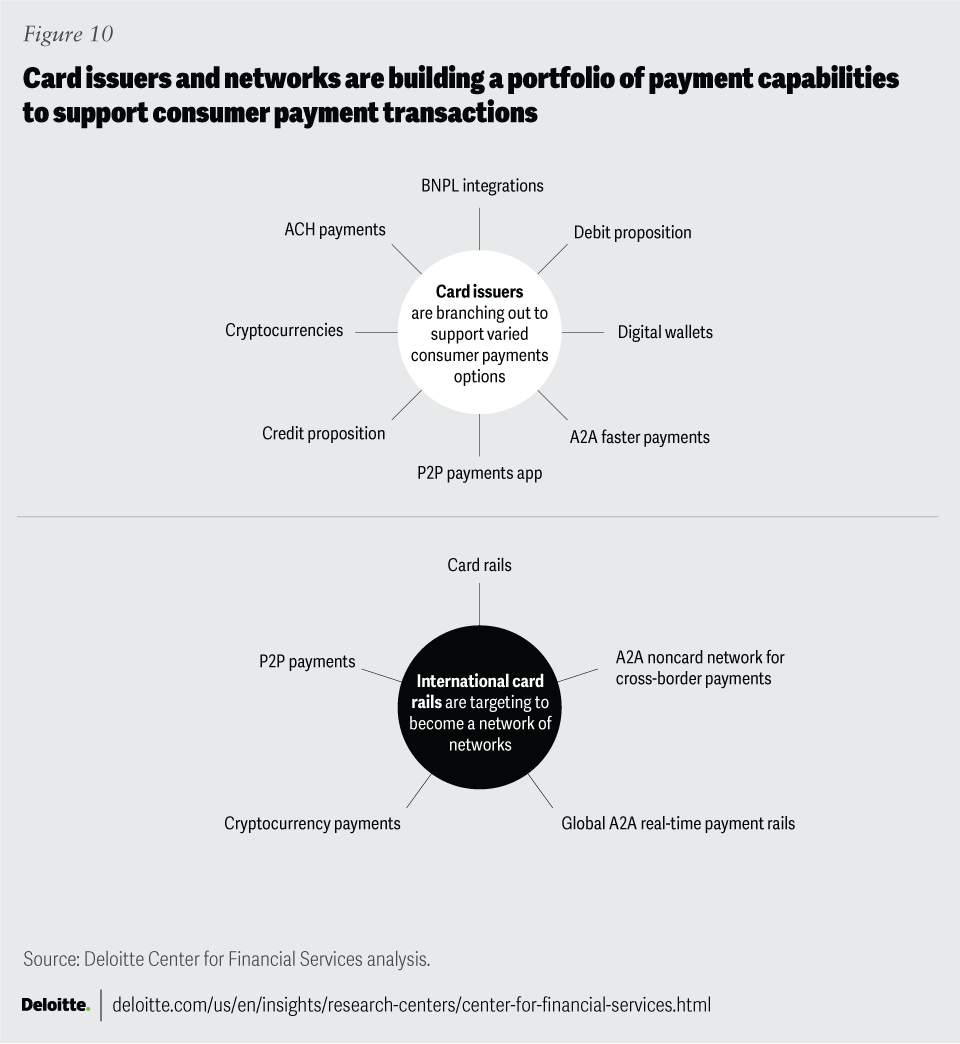

Traditionally, payments institutions stuck to their respective product lanes, but now they are encroaching into each other’s businesses to grow revenues. For instance, card issuers are trying to grab a greater share of account-to-account (A2A) consumer payments, as domestic RTP offerings expand. In the United States, both large and small banks have signed up as early adopters of FedNow,84 the Federal Reserve’s real-time A2A payments rail. Even global card networks are excited about A2A payments and building multi-rail (e.g., cards, P2P, A2A, and crypto) value propositions (figure 10).

{kind=link}

Blockchain-based and fiat currency-backed stablecoins are also entering the world of consumer payments. In some instances, they are further disintermediating the role of traditional payments institutions by facilitating the exchange of money in cross-border remittances, P2P payments, and even customer-to-business retail payments.

Concurrently, digital wallet and BNPL providers have launched card offerings; card issuers, in return, are launching their own digital wallets85 and integrating BNPL offerings into their portfolios. Issuers are also working with merchants to offer embedded payments, allowing nonfinancial companies to offer integrated payment solutions to their consumers.

These efforts to expand beyond their core offerings suggest card issuers and networks recognize that this interconnected web of payments, products, and rails will only get more complex as we enter 2024. The innovations and competitive actions threaten their transaction revenues, and risk diminishing visibility and ownership of consumer data.

Additionally, open banking around the world is gradually eroding what once was payments incumbents’ competitive edge. With open banking, third-party providers, including fintechs, bigtechs, and other software providers, can access customer data in payment providers’ systems via APIs, embed payments, and help consumers pay seamlessly within their shopping journeys. This may be the beginning of open data encompassing nonfinancial interactions as well, such as with telecom and utility players. At the same time, ensuring privacy and security of data will be critical. With this in mind, the EU is considering new regulations for the use and access of open data.86

Going forward, card issuers should continue to deliver value beyond payment transactions to remain competitive. Much of this may boil down to how well they know their customers and their ability to analyze customers’ proprietary transactional and alternative datasets to offer more personalized advice, such as spending controls, budgeting advice, and tailored rewards.

Meanwhile, data can be leveraged to help enable value creation, new business models, and new partnerships. Choosing the right TPPs that consumers trust would allow payments incumbents to alleviate consumers’ concerns around security and privacy while also elevating their experience with innovative offerings. This growing role of trust in a world where physical and virtual realities are increasingly converging would solidify the push toward digital identity, making it easier for institutions to authenticate senders and recipients of money across all interactions.

Responsible BNPL credit to elevate consumers’ financial well-being

The proliferation of BNPL in consumer payments has encouraged traditional credit card issuers to include BNPL in their portfolios. An inflationary environment further heightened the financial and operational benefits of BNPL over traditional credit products, driving lending volumes.

While BNPL products have helped many consumers access credit, multiple studies suggest that these consumers may be overspending beyond their means. In a recent Pymnts survey of BNPL users, 70% of respondents admitted they spent more than they would have, had they paid upfront.87 Also, according to the CFPB, “[BNPL] firms have created their own gateways and digital, app-driven marketplaces, powered by personalized behavioral data, to lure their users into buying more products.”88

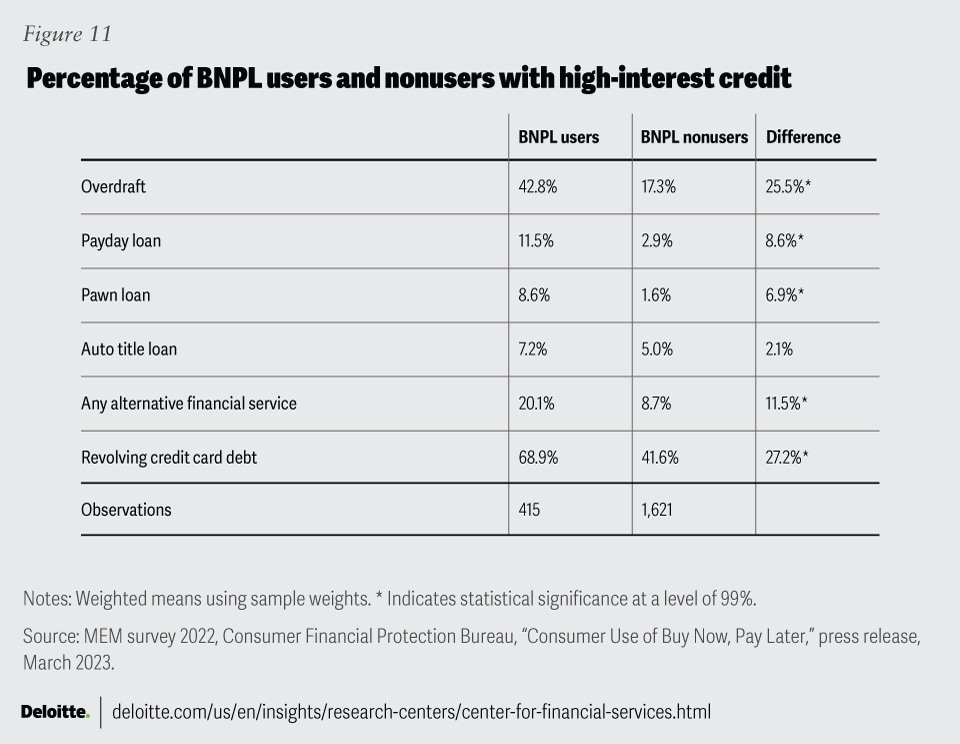

Another concern is how BNPL balances seem to be disproportionately accumulated by those heavily dependent on credit for their living. For instance, BNPL users were more likely to be highly indebted and rely on many other high-interest credit products compared to BNPL nonusers, according to a CFPB analysis (figure 11). While these credit products are intended to help consumers in distress, are they eventually putting them in more distress?

{kind=link}

The US regulator’s findings also indicate other issues with the BNPL space: inadequate dispute protections compared to credit cards, bigtech-style data surveillance, and slow progress among reporting agencies to develop mature reporting protocols when it comes to BNPL credit.

As a result, regulators globally plan to supervise this industry to bolster consumer protection. In May 2023, Australia announced reforms that recognize BNPL as a credit product under the Credit Act, and mandate that firms comply with responsible lending obligations and hardship requirements.89

These regulations, along with institutions’ enhanced risk management, reporting to traditional credit bureaus, and emphasis on the short term, small-ticket size credit, could usher in the next wave of BNPL maturity. Card issuers and pure-play BNPL providers can play a significant role to elevate consumers’ financial well-being by providing advice and responsible credit. For instance, Klarna launched a credit opt-out feature that offers consumers a choice to opt out of using credit to stay within their budget.90

Moreover, by providing cash flow tools to consolidate multiple payment schedules, delivering insights on budgeting, and supporting customers in achieving financial goals, issuers and BNPL providers in the space can encourage customers to save and spend more effectively.91 In fact, responsible BNPL credit can help the unserved and underserved consumers build or rebuild credit.92

Traditional acquirers face growing competition from software players and modern acquirers

Merchant acquiring and payments processing providers, which are increasingly operating in a commoditized business, recognize the opportunity with small and midsize businesses (SMBs). A 2022 Credit Suisse study indicated that the US SMB segment comprised under 20% of payment flows but accounted for about 55% of potential revenues for acquirers.93

Competition is closely following the money. Software providers, especially working with SMBs, continue to bring payment elements in-house (becoming a “payfac”) to own a larger share of the merchant acquiring value chain.94 Additionally, modern acquirers are scaling both domestically and internationally, and expanding beyond payments to offer embedded finance products to deepen wallet share. For instance, Adyen began offering business checking accounts and business lending options for platforms and marketplaces in Europe and the United States in late 2022.95

Caught between competition from software providers and modern acquirers, the incumbent merchant acquirers should step up their defense. Some acquirers may choose to partner with or even acquire software firms that cater to merchants to retain a greater share of the value chain. Meanwhile, competing with modern acquirers would demand superior digital and service capabilities. Incumbent acquirers should not only offer international presence and omnichannel payments acceptance, but also provide a single (or few) integration(s) to businesses to access local processing platforms and payment methods and to acquire support, among other local services.

Fighting synthetic fraud when fake is as good as real

Payment firms are in a global arms race with malicious threat actors, as scams become more sophisticated. Synthetic fraud is one such example that is notoriously difficult to detect.96 Many fraudsters concoct entire personas using a mix of real and fabricated information, which are often pinned to social security numbers.

The proliferation of generative AI is only expected to accelerate the pace at which fraudsters fabricate such synthetic identities to trick consumers and businesses to send payments to their impersonated accounts, commonly referred to as authorized push payments (APP) fraud. In the United Kingdom, Faster Payments service has experienced a 6% YoY increase in APP fraud cases97 on personal accounts, with losses amounting to US$600.1 million in 2022.98

To combat these risks, regulators are stepping in with measures to bolster consumer protection. The UK Payments System Regulator issued new reimbursement requirements in which both the payer and payee’s institutions need to fully compensate consumers who are victims of APP fraud within Faster Payments.99

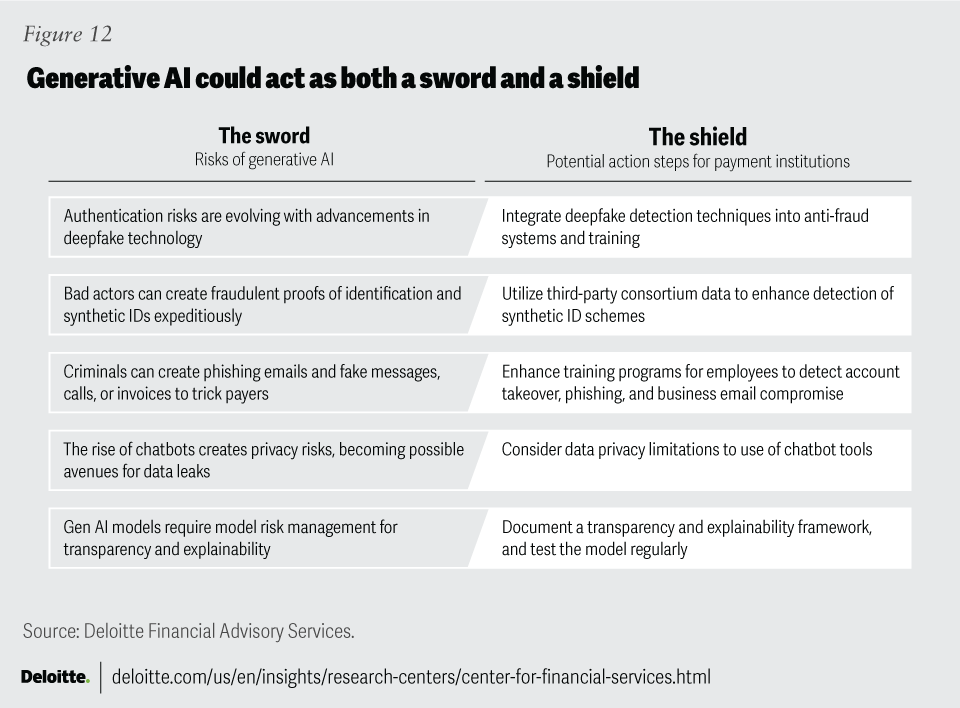

The stakes are high for payment institutions; they should strengthen their risk-based approaches to minimize or eliminate fraudulent payment requests. They should supercharge their anti-fraud skillsets with generative AI technologies and third-party data to train their authentication and fraud detection models to predict criminals’ next moves and circumvent their advances (figure 12).

Banks should also work more closely with startups and established technology firms to develop multimodal biometric security that evaluates several indicators at once, such as fingerprints, natural speech patterns, and word choice, to increase fraud-detection outcomes and reduce false positives. Collaborating with nonfinancial institutions, such as telecoms, mobile network providers, and regulators, would also add allies that could analyze consumers’ nonfinancial data to prevent unauthorized use of identity.

{kind=link}

Wealth management: Revamping the advice engine for the future of wealth

Priorities for wealth management institutions in 2024 and beyond

Wealth management business is at the cusp of change. While global wealth continues to build and diversify across regions, recent market volatility has challenged assets under management (AUM) growth. This is prompting wealth managers to redouble their efforts to provide a richer advice experience, which they can then combine with innovative new products. Technology continues to play an important role for wealth firms, especially as institutions come to grips with the need to develop expertise in, and promote the use of, artificial intelligence to drive greater personalization. Many wealth managers will also look to automate routine tasks through generative AI and advanced data analytics. The push to bring about greater efficiencies and broaden product offerings by acquiring or partnering with third parties will continue to be of interest, although deals may be struck at a slower pace than in previous years.

Intergenerational wealth transfer continues to gather momentum as well. This shift will require advisors to develop even more holistic advice capabilities.Many members of Gen X and other generations are worried about whether their parents will be able to attain a comfortable retirement, while those holding the assets are clamoring for broader coaching and advice. Some of these new concerns are driven by greater longevity. Succession planning is also becoming more urgent as the advisor population ages in many parts of the world. The next investor generation will want to sit across the table—physical or virtual—from someone who looks like them and has the same lived experiences they have. Acquiring and developing younger and more diverse talent could challenge growth, however.

Macroeconomic, geopolitical, and regulatory uncertainties have exacerbated costs and margin pressures for global wealth managers, but they remain resilient. Global wealth is likely to surpass US$500 trillion in 2024, nearly five times the global GDP.100 From a regional perspective, the biggest portion of this wealth is now in Asia-Pacific (~40%), with China accounting for nearly 20%. North America has about 33% of that total, with Europe at 23%.101 Assets under management should grow at an annual pace of around 8% over the next five years,102 more than double the expected growth in global GDP.103 And net financial wealth held by the mass retail market could almost double to US$22 trillion by 2030.104

Even with these positive expectations, wealth managers should continue to evaluate their competitive strengths and operating models to support the agility needed in the future. What changes should they consider in their operating models to capitalize on the growth prospects in 2024 and beyond? How can they differentiate themselves to create a winning franchise?

Honing the advice experience

With client needs and markets shifting, wealth managers cannot rely on bull markets for increased assets under management. In the previous decade, more than 70% of the growth in AUM was the result of market performance, with only the remaining 30% coming from organic growth.105 Investor satisfaction is a function of returns. For instance, US investor satisfaction with full-service investment advisors tumbled 17 points in 2022, coinciding with a 20% drop in the S&P 500 in the same period.106 But wealth managers have little control over market performance, so they should focus on improving customer satisfaction through other means. These include offering advice beyond investments and supporting clients through their life journey. Unfortunately, only 11% of advisors currently take these additional steps.107

Further, the shift from accumulation to decumulation among those holding the greatest share of assets continues. With more baby boomers retiring every day, the boundaries of advice continue to not only expand across retirement income, but also include health insurance, longevity, and even dementia care planning. For good reason: A recent survey showed that 80% of Americans aged 50 and older were concerned about funding their own health care costs in retirement.108 The most impactful advice propositions will likely emerge around moments that matter, by integrating both financial and nonfinancial assets and liabilities.

Moreover, a recent Deloitte survey of 300 affluent Swiss banking clients revealed that they want it all: superior, omnichannel wealth management experiences at lower costs.109 Self-service platforms remain a popular approach to serve not just the affluent, but also young, first-time investors with lower investable assets. Even so, the ability for wealth managers to support moments that impact their clients’ life and wealth journeys can be a differentiator. A good place to start is by using data and analytics to create hyperpersonalization based on an efficient segmentation strategy.

To best serve these younger generations, firms should hire more young talent. Unfortunately, about 37% of advisors plan to retire during the next decade, but 72% of newcomers (those with three or fewer years of advisory experience) fail to stay in the industry.110 Wealth managers should adjust their recruitment policies to focus on diversity and provide sufficient growth opportunities to budding advisors to maximize success. UBS, for example, is diversifying its advisor pool in terms of age and race to better mirror younger generations.111

Retooling platforms with a focus on cost takeout and deepening client relationships

Wealth managers continue to invest in technology, but with a greater focus on cost rationalization than before. Indeed, 68% of wealth managers surveyed consider optimizing cost-to-income ratio and aiding regulatory compliance as their top, near-term business challenges.112 Consequently, there’s a greater inclination to look to third parties: In a recent survey of global wealth management and private banking clients, 72% of respondents said they plan to collaborate with fintechs, broker-dealers, and custodians to modernize their technology infrastructure and free up internal resources and time to focus on strategically important products and services that enhance client experience.113

Firms will invest in forming clear data management strategies to better use new forms of data and artificial intelligence. This will help them generate richer insights while creating agile and scalable operations to keep pace with future advice models. The spend on cloud services for wealth management platforms, including more wealth management-specific industry cloud solutions, could grow by more than US$10 billion over the next 10 years.114 Firms can start today by undertaking small-scale transformation to help create quick wins that can build confidence and trust on the way to enabling faster time to market and operational efficiency. Perpetual know your customer (KYC), for instance, can help provide a more complete, real-time risk picture, but its success depends on the unification and quality of firmwide data.115 But security concerns (e.g., cybersecurity, data privacy, deepfakes, and hallucinations) loom, making it vital to instill an AI trust framework.116 Regulators are also becoming increasingly focused on conflicts of interest. In July, the Securities and Exchange Commission (SEC) proposed new rules requiring firms to keep investors’ best interests in mind when using AI.117

Next, firms are providing advisors with integrated omnichannel solutions that support new on-demand conversations. Engagement and collaboration tools like live chat, secure messenger, and cobrowsing can free them up to focus on higher-value activities and even increase the number of clients served.

Generative AI is starting to be used in fraud detection, anti-money laundering (AML), client communication and marketing, product fit assessment, memo writing, and report generation based on research.118 Deutsche Bank is deploying deep learning to analyze client portfolios for concentration risk and match individual clients with suitable funds, bonds, or shares.119 Meanwhile, JPMorgan has recently applied to trademark IndexGPT, which can analyze and select securities based on client preferences.120

Bridging the offerings gap

While exchange-traded funds remain the preferred investment vehicle for clients of all sizes, with more than US$600 billion in net flows in 2022, direct indexing and alternative investments continue to gain momentum. In fact, alternative investments could increase from 11% of consumer household investable assets to 20% by 2026 and generate an additional US$11 trillion in incremental net flows for wealth management firms.121 Ultra-high-net-worth investors expect to be overweighted on private equity, the largest percentage of any of the alternative asset classes, followed by hedge funds, venture capital, and private debt.122 Meanwhile, extreme price volatility and the recent turmoil in crypto markets seem to have cooled demand for digital assets.

With private assets becoming more mainstream as regulations ease, wealth managers could offer products to clients who are lower on the asset spectrum. For example, Luxembourg’s parliament recently passed a bill that lowers the minimum investment threshold for alternative funds by about US$27,000 to US$108,500.123 The United States is also relaxing rules that govern “accredited investor” definitions to allow for broader retail participation in alternative products.124 Wealth managers are looking to acquire these capabilities. Recently, MUFG announced its intention to buy alternative asset firms to meet client demand.125 Training advisors is crucial since advisors typically do not recommend products with which they are not familiar.126

Meanwhile, just 17% of advisors surveyed in the United States are citing ESG factors as a consideration in their clients’ investment processes, the lowest in five years.127 This could be a function of profit-taking, portfolio rebalancing, underperformance, or, perhaps, a lack of trust. In a Deloitte survey of about 1,000 retail investors in the United Kingdom, 69% said they have or would refrain from investing in a financial asset if they did not trust the ESG investment framework used by their provider.128

Industry estimates suggest ESG assets could reach US$50 trillion by 2025.129 Firms should, therefore, continue to support advisors with tools that aid client conversations around values-based investing. New regulations, such as the European Commission’s proposed Green Claims Directive, which would require companies to back environmental claims with a comprehensive assessment,130 along with the SEC’s new rules for company disclosures on ESG policies,131 would require firms to put guardrails in place to avert the perception of greenwashing. These may include third-party certifications and compliance checks.

Wealth management M&A to slow down

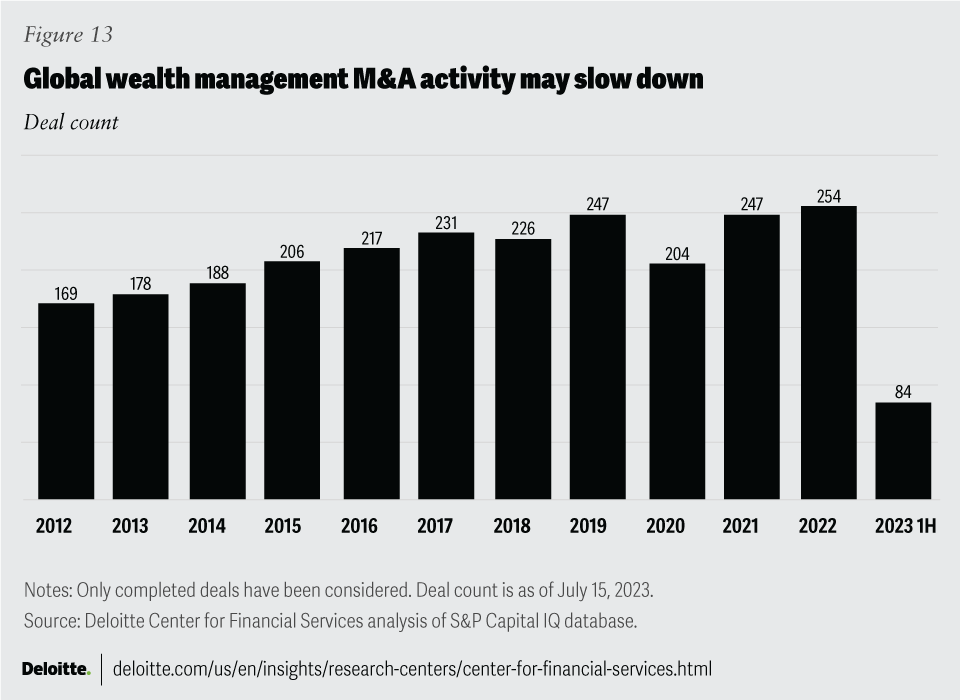

Owing to the attractiveness of the segment, insurance companies, hedge funds, and others continue to consider acquisitions in this space.132 Globally, wealth managers closed 254 deals last year (figure 13), the highest in a decade, with North America accounting for 70% of the deals, followed by Europe (21%) and Asia-Pacific (6%). Driven by a buy-and-build strategy, private equity-backed firms Mercer Global Advisors and Wealth Enhancement Group, acquired 18 and 11 companies, respectively, last year.133, 134 The primary drivers for M&A activity are economies of scale, cost reduction, new services, and talent acquisition. However, the number of deals are down by 26% YoY to 84 in the first half of 2023. This slower pace may continue even in 2024 as macroeconomic conditions weigh on buyer sentiment.

{kind=link}

Corporate and transaction banking: Enabling efficient money flows through digitization

Priorities for corporate and transaction banks in 2024 and beyond

Corporate and transaction banking businesses are looking at a confluence of priorities.135 While commercial loan growth held steady for most of last year and the start of 2023, banks are looking at a more muted outlook for the next several quarters along with tightening lending standards and the increasing risk of CRE loan portfolios. De-risking is also on the minds of many corporate clients, who seek more optionality with respect to their banking relationships.

There is enormous pressure for banks to pick up the pace of digitization to elevate customer experience and strengthen relationships, while also managing costs. Digital solutions in loan origination and underwriting, cash management, B2B payments, trade finance, and asset servicing should help institutions unlock new efficiencies and address customers’ pain points.

Growth opportunities are emerging, however. From digital asset custody to green transition strategy advice, corporate bankers should remain agile to support their clients’ more complex needs. They should work constructively with borrowers and champion an advice-based model to strengthen the personal touch, while also empowering clients with a self-service model to address their direct, simple needs.

The current state of lending to corporates and SMBs has shown strength globally despite the economic challenges in the past year. US banks’ outstanding exposure of C&I loans rose 6% YoY to US$2.8 trillion in May 2023.136 At the same time, their outstanding exposure to total CRE loans rose 11% YoY to US$2.9 trillion,137 much of it held by banks with less than US$100 billion in assets.

Bank lending to corporates in the Eurozone grew 3% YoY to US$6.4 trillion in June 2023.138,139 European banks’ NIMs have also benefited from lower deposit costs, and institutions continue to demonstrate cost discipline.140

However, a less favorable economic outlook, lower risk tolerance, and the desire to shore up liquidity positions have prompted many banks to tighten their credit to corporate borrowers. In Q2 2023, 68% and 51% of surveyed US banks reported tighter standards for CRE and C&I loans, respectively.141 Meanwhile, only 30% of European banks reported tighter credit standards for commercial real estate in H1 2023, compared to 25% in H2 2022.142

The office CRE debt market continues to show signs of weakness due to declining values and rising vacancy rates, particularly in the United States.143 Of the total US office property loans maturing in 2024 that are held by banks and with investors as commercial mortgage-backed securities (CMBS), 17.4% are classified as “troubled” or “potentially troubled/watchlist” as of August 2023. This figure stands at 10.5% for retail property loans and 8.5% for multifamily property loans.144

As a result, regulatory scrutiny is expected to increase for banks with high exposure to the CRE market, especially small banks with assets under US$10 billion. A Federal Reserve analysis indicated that small banks’ CRE loans as a percentage of risk-based capital stood at 357% in Q1 2023, compared to 131% for the overall banking industry and 300% regulatory threshold.145 SMBs with heavy CRE exposure could become M&A targets in 2024 as they seek to shore up their balance sheets. Meanwhile, regulators have already encouraged banks to work “constructively” with CRE borrowers by offering loan accommodations and extending repayment arrangements.146

On the deposits side, corporate clients are reducing their bank concentration and diversifying their deposits across multiple banks. Banks’ funding costs have increased since they are paying higher rates to corporate depositors.

With this backdrop, what should corporate banks do to maintain profitable lending margins in 2024 and beyond? Given the constraints on NIM growth, how can they strengthen customer relationships to drive fee-based business with corporate and institutional clients?

Balancing risk, efficiency, and relationships in a cautious lending environment

Corporate banks will face a unique set of challenges going into 2024. With the global economy recovering at a divergent pace and the ongoing uncertainties around interest rate trajectories, revenue growth is likely to be challenged, especially in the United States. In Europe, the mounting political pressure to offer higher deposit rates to customers is beginning to disincentivize investors.147

In such a macroeconomic environment, banks should strengthen their risk management with alternative data (such as trading data, bank transaction data and repayment history, customer ratings and reviews on different digital platforms, accounts receivable, and cash-balance data) in real time. Refining customer segmentation models around structural archetypes (e.g., capital-intensive businesses, transaction-heavy businesses, and cash flow businesses, among others) should allow for more tailored credit approval processes and risk monitoring.

Concurrently, there is enormous pressure for banks to pick up the pace of digitization while managing costs. In particular, many banks are working to determine how best to use AI/machine learning (ML) and APIs to improve risk selection and achieve operating efficiencies in the loan value chain, especially in the SMB loan portfolio. For instance, many UK banks have emerged as trailblazers in SMB lending by fully automating loans up to US$100,000.148

Banks are also looking at how to use embedded finance as a distribution channel to increase access, especially to more SMB customers. Embedding real-time payments, deposit accounts, and capital loans into corporate customers’ existing ERP and accounting systems makes it more efficient for businesses to access financial services in a unified ecosystem without needing to directly interact with banks.

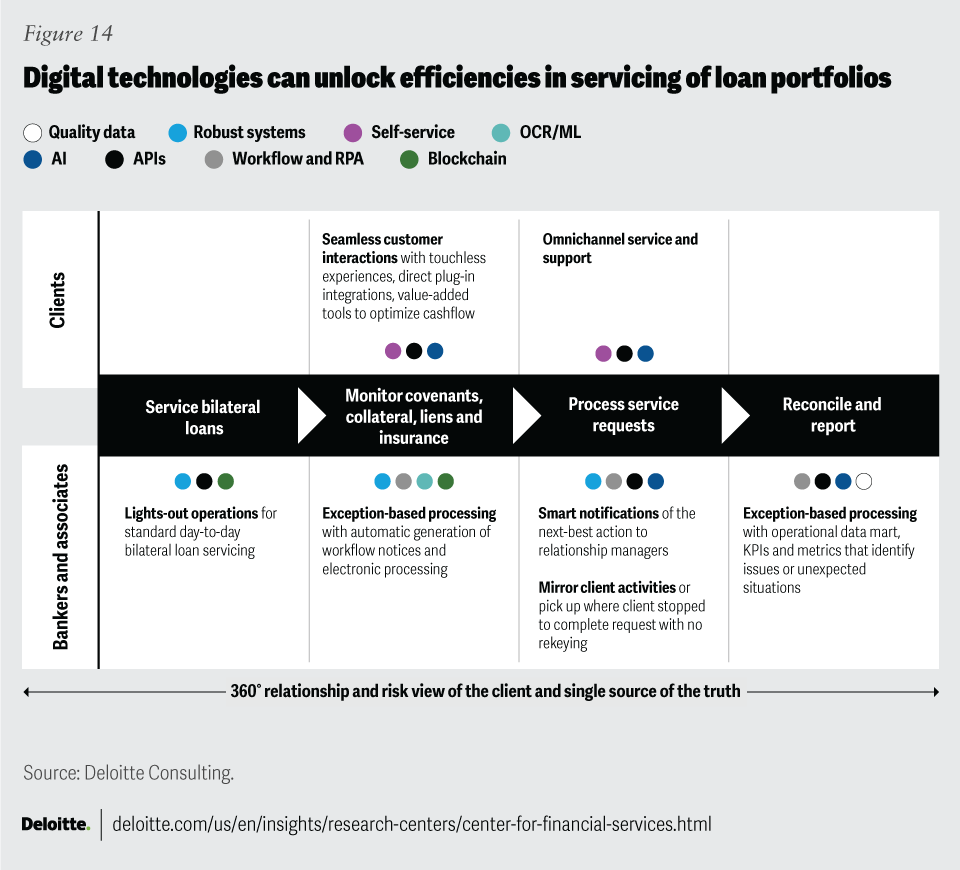

While product and loan origination has seen a lot of digital action, these technologies have not yet unlocked efficiencies in loan servicing (figure 14). Standard, day-to-day loan servicing could be automated, providing a seamless customer experience and an omnichannel support. Digital systems can also autogenerate workflow notices on actions required by corporate clients. This would free up relationship bankers to focus on sales, customer service, managing risks, and handling true exceptions.

Doing so will also elevate relationship bankers’ role; they can focus more time addressing the needs of the clients and reinforcing the personal touch. Adopting a solution mindset and honing industry specialization should empower relationship bankers to champion an advice-based model. Bankers who complement their industry specialization with tech proficiency and cross-industry fluency are likely to forge stronger client relationships.

Corporate banking units should aim to build agile staffing models to support customers’ pain points, for instance, by becoming trusted advisors in their climate transition strategy. In addition to upskilling existing talent pools on honing solution mindset and industry specialization, banks will need to rejigger their workforce and elevate commercial bankers’ profiles to make it more attractive for young talent to participate in and champion this cultural change.

{kind=link}

Empowering corporate treasurers with new tools to better manage finances

Events leading up to the US bank failures in early 2023 put many corporate treasurers, especially clients of US regional banks, under extreme stress. Fearing contagion, treasurers worried if their deposits were safe, and how their payroll processing and payments would be negatively impacted. Corporate treasurers in Europe were also on high alert as the collapse of Credit Suisse unfolded.

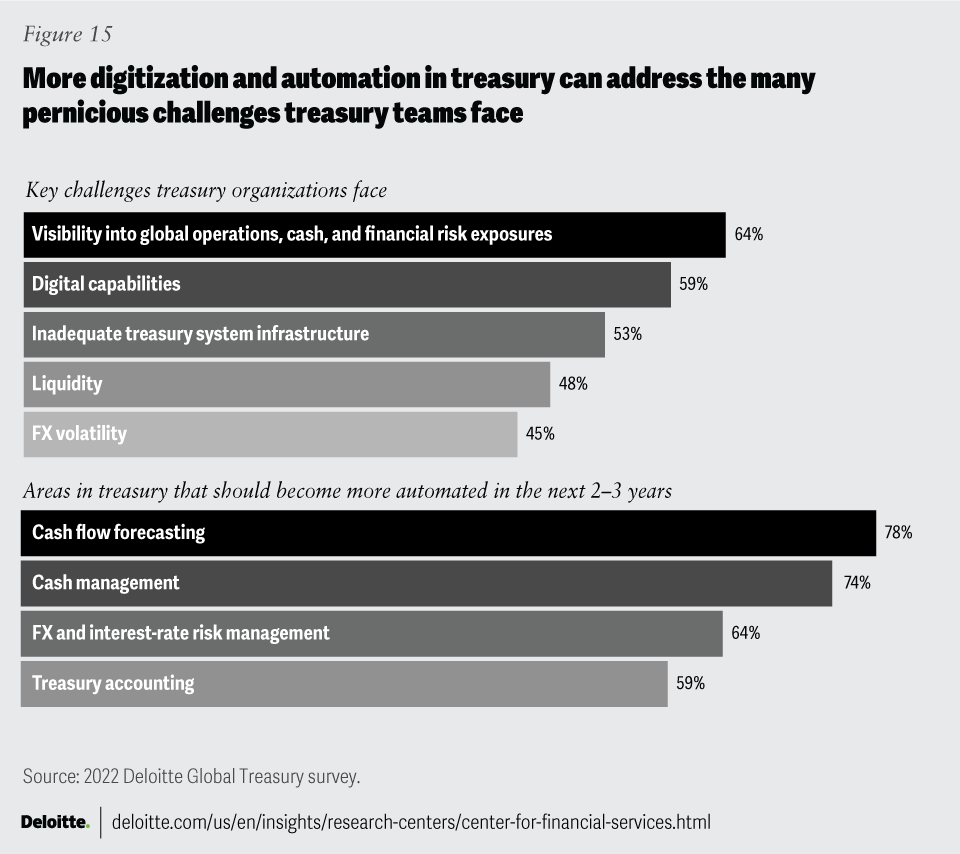

This experience only reinforced the importance of capital preservation. Boards of directors also recognize the importance. According to Deloitte’s 2022 Global Treasury survey of corporate executives, 96% of respondents say their boards or chief financial officers view enhancing liquidity risk management as a critical or important mandate.149

There is also anecdotal evidence of “de-risking” by corporate clients, who seem quite intent on broadening the number of banking relationships. It is not uncommon, especially for large corporates, to have 10 or more banking relationships.150 This may be true for SMBs as well.