Perspectives

The Deloitte Research Monthly Report

Issue X - Special Report: 2016 Outlook

18 December 2015

Economics

What to watch for in 2016: GDP growth rate and RMB exchange rate

GDP growth rate and RMB exchange rate are the key issues for 2016. The two are closely linked. We continue to take the position that a more flexible RMB exchange rate (meaning a weaker RMB against a strong USD, but not necessarily against most major trading currencies) is important from the standpoint of 1) reflation; 2) cushioning the pains of economic restructuring.

The official GDP growth target for 2016 is set at 6.5% with the rationale of doubling the size of economy by 2020. In order to achieve the economic growth target, policy responses will have be more pro-growth (but without resorting to fiscal stimulus measures such as in late 2008). Premier Li Keqiang has ruled out the possibilities of a “strong stimulus” for the next few years. Meanwhile, the twin objectives of “stabilization of economic growth & adjustment of economic structure” will have economic growth take precedence over structural adjustment. In addition, certain supply-side reforms (streamlining administrative approvals and selective closures of loss-making SOEs) are likely to be introduced with the overarching goal of reducing excess capacities in several sectors such as steel and ship-building. However, there is a price to be paid (or several) for sustaining a relatively high GDP growth rate – one of them is leverage.

If overall leverage continues to rise (total debt/GDP reached about 260% in 2015), it would be important for the Government to rein in leverage with local governments and firms. So the policy implications are clear – first of all, central government is expected to take on certain liabilities from local governments. This means debt swaps and maturity extensions as in 2015. For the corporate sector, it means a greater reliance on direct financing through capital markets and the exit of certain zombie companies. In the wake of the stock market interventions of summer 2015, one of the chief lessons learnt is that financial market supervision, which has significantly trailed market development, must be more coordinated. So it is not surprising that the PBOC takes the lead in terms of mitigating financial sector risk undertaking financial liberalization.

2015 saw much progress in interest rate liberalization with the removal of the ceiling for deposit rates. Heated competition in the banking sector has resulted in shrinking interest rate differentials which in turn has eroded bank profits at a time when asset quality is worsening due to slower economic growth. We have been advocating a weaker RMB exchange rate for reasons other than those based on the conventional argument of restoring competitiveness. Actually, PBOC’s reluctance to depreciate the RMB significantly following the initial downward adjustment on August 11 showed that China does not view a weaker exchange rate as an effective tool when external demand is weak. But this is perhaps somewhat short-sighted as it does not take into account other factors.

Despite a benign inflationary outlook, China does not have much room for cutting interest rates (banks can’t afford it) and therefore a cheaper RMB is a logical tool for enhancing monetary policy’s effectiveness. A cheaper RMB, for foreign investors, could be a key trigger for restoring confidence in the stock market which has been in the doldrums for years.

Structural adjustment for China really boils down to reducing corporate leverage – the main source of financial risk. If more foreign capital could return to Chinese equities which have been under-weighed for years, China’s task of economic rebalancing would be easier. On a deeper level, tolerating greater flexibility on RMB exchange rate (PBOC’s hint on targeting a basket of currencies prior to December FOMC meeting indicated that RMB won’t be loosely pegged to the dollar in future) would prevent exchange rate misalignment.

In conclusion, 2016 won’t be an easy year but an economic `hard landing’ is unlikely. We forecast GDP growth at 6.4% and USD/RMB exchange rate at 6.8 in 2016.

Energy

Low level of oil prices, greater adjustment of oil sector and steady increase in natural gas production and consumption

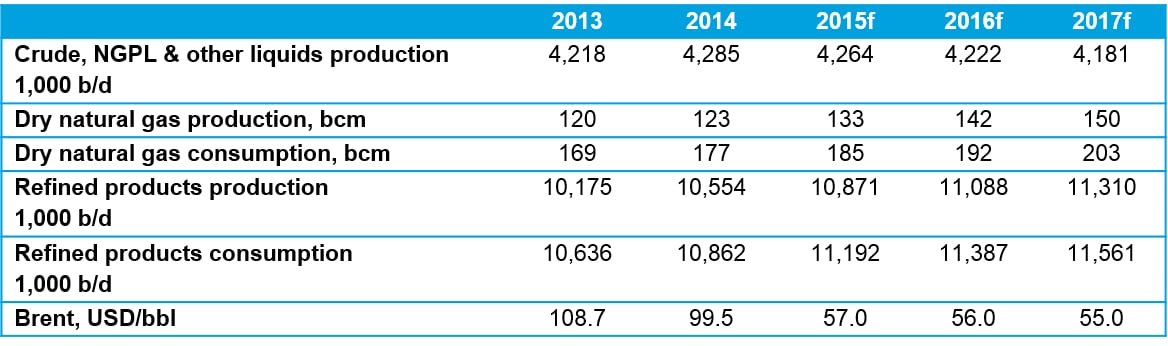

A persistent oversupply will reinforce the bearish outlook for oil prices in 2016. OPEC will maintain its current 30mn b/d production target and may raise the target in June 2016 by 500,000 b/d to accommodate Iran's return to market.

China's crude oil production is expected to fall as lower prices will lead to production cuts by the country's largest oil producers, namely CNPC and Sinopec. In addition, an inevitable decline of production from existing oil fields will also weigh on output. On the other hand, crude oil imports will remain strong, largely driven by continued stockpiling activities that bear no relation to current macroeconomic trends.

Sluggish economic growth, a slowdown in industrial activity and a structural shift away from oil-based fuel consumption will see China's consumption of refined fuels drastically slow. The growth rate is expected to be about 1.5%, quite a change from the 6.0% growth rate experienced over the 2003-2013 period. Although some 1.7mn b/d of new refining capacity is scheduled to come online over the next five years, a subdued domestic demand has dampened growth in the demand for refined fuels. This, coupled with severe under-utilization of the existing refining capacity, could see a greater consolidation in the country's refining sector.

While LNG imports will outstrip pipeline gas imports over the next four years as a result of lower import cost and the start of several long-term contracts with large Australian export ventures, pipeline gas' dominance will be restored from 2020 with the anticipated completion of a fourth line at the Central Asia-China Gas Pipeline. This will pave the way for a large ramp-up in imports from Turkmenistan.

Click to enlarge image

Retail

Increased support of domestic demand and greater consumption of middle to high end goods will pave the way for growth in retail and consumer markets in 2016

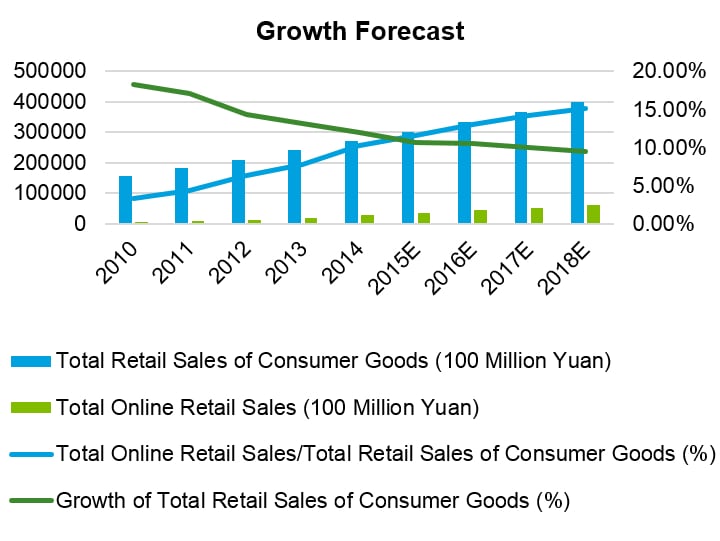

In 2015 the GDP growth rate fell below 7% as the traditional manufacturing industry continued to weaken. November’s PMI fell to 49.6, the lowest level since 2012. On the hand, the consumer sector and the retail sector recorded a steady growth in 2015, becoming the torchbearers of China's `new economy’. The "13th Five-year Plan" has made provisions for supply side reform and boosting domestic demand. The new policy initiatives and economic reforms will ensure that the consumer and retail markets are likely to grow in a stable manner.

The consumer and retail markets will become more globalized, digitized and diversified in 2016. The omnipresence of Internet and Mobile phone technologies have changed the lifestyle of consumers. According to the latest available data, online retail accounts for more than 10% of total retail sales of consumer goods and mobile transactions account for more than 50% of total online retail. In 2016 the trend will continue as both online and mobile transactions continue to grow.

Thanks to a strong and steady growth in consumer demand (fueled by China's growing middle class), the cross-border E-commerce industry has been growing rapidly over the past several years. Since 2011, annual growth of the industry has been over 20% while businesses at import companies have grown at over 40% annually. According to Alipay's data, 2015’s volume of sales on Black Friday and Cyber Monday increased 30 times over last year, indicating that in 2016 the cross-border E-commerce industry will continue to grow but competition will probably intensify.

On the other hand, compared to online retailers, brick-and-mortar retailers are having a bad time. The growth of total sales of the top 100 retailers stayed around 1% in 2015, though in September it fell below 0. After several years' underperformance, in 2015 major retailers attempted to migrate to an Omni-channel Retailing model. At present, about 82% of China's top 100 chain enterprises have started e-commerce businesses, amongst which 54% have built their own e-commerce platforms. In 2016 brick-and-mortar retailers will expand their investments in Omni-channel development and actively employ big data technologies as well as Internet technologies to improve consumer experience.

Click to enlarge images

Life Science & Healthcare

Drug innovation and new business models are the focus in the upcoming transition

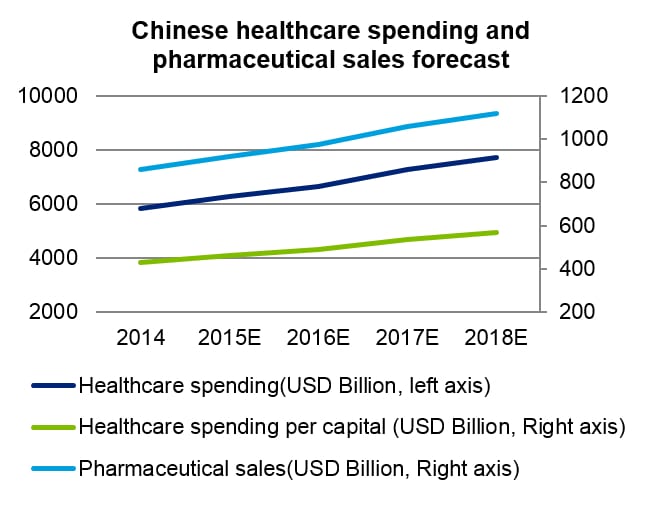

In the context of tighter control of medical insurance costs and drug revenue margins, the pharmaceutical industry finds itself under pressure. This will force pharmaceutical companies to seek high growth by way of introducing new drugs or venturing into new markets. The introduction of new drug approval policies that favor innovative drugs and high-quality generics is going to prompt these companies to upgrade their overall R&D strength to enhance market competitiveness. In addition, domestic companies are looking into the overseas market and moving into the preparation export business and searching for merger and acquisition opportunities.

There is huge potential demand for advanced medical services, and private hospitals remain the hot spot for investment. With the rapid rise in household income, consumption of self-pay based advanced medical services is likely to continue to rise, especially while commercial insurance also continues to gain momentum, all of which will be a boon to private hospitals. The promise held by this rapidly widening market coupled with the government’s policy to encourage private investment in the medical sector makes private hospitals very attractive to private capital. But reimbursement restrictions and a shortage of physicians are the big obstacles that may hinder the development of this market.

The rise of new Internet+ oriented business models are transforming and reshaping the LSHC industry, giving rise to opportunities for unprecedented growth. Internet and mobile technology is re-constructing online and offline medical resources to provide care in a more efficient manner. With more data capable of being recorded, stored and consolidated, medical informatization is gaining popularity as big data is more likely to be meaningfully utilized in patient care, drug innovation and marketing. However, e-Pharmacy is still in a state of limbo as it is waiting for the policy allowing online sales of prescription drugs.

Click to enlarge images

Automotive

Auto sales are set to recover yet market outlook remains clouded

Auto sales rebound in 2016 with SUVs taking the lead

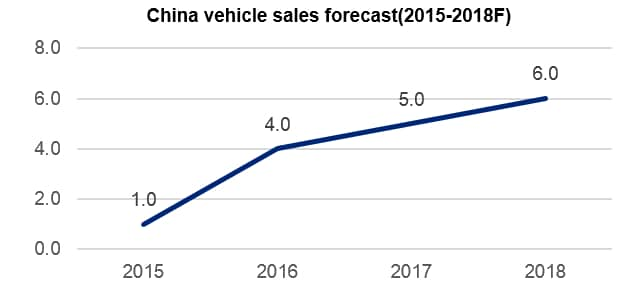

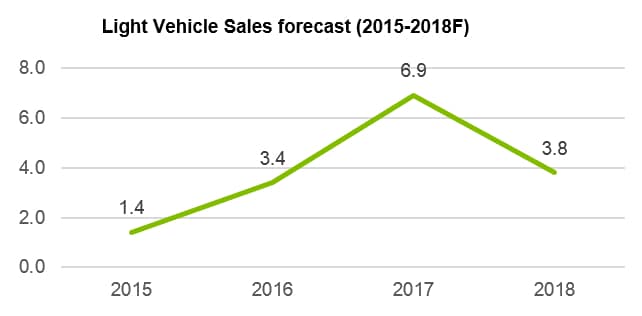

Auto sales in China are expected to recover slightly in 2016 with an estimated 4% growth for the whole year, falling behind GDP growth rate. SUVs will remain the fastest growing segment in the automotive sector, maintaining a double-digit growth rate in 2016. Motor vehicles have become a necessary upgrade target for most households especially since China relaxed its one-child policy. The sedan segment will face a second straight year of weaker growth in 2016. However, cars with engines smaller than 1.6 liters will continue to show resilience and make up a larger portion of PV sales, influenced by the purchase tax reduction policy which is less likely to jump-start vehicle sales, much as the same policy initiative did in 2009.

(See Chart C & D)

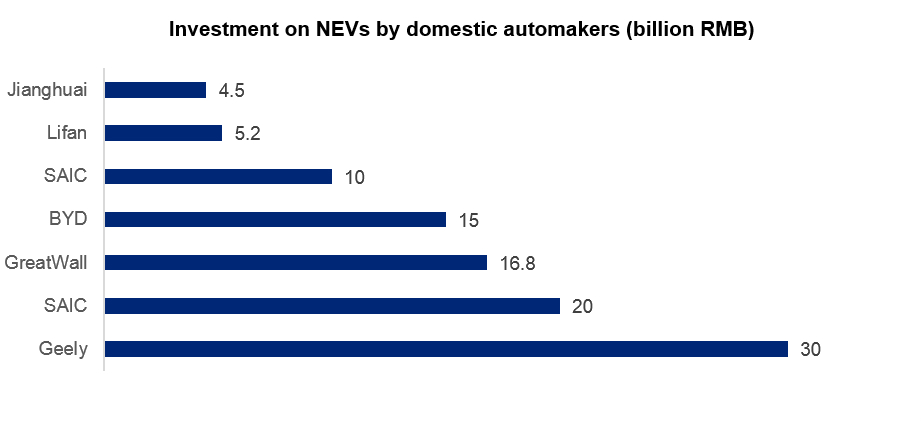

Explosive growth in the New-Energy Vehicle market

The Chinese government has designated new-energy vehicles as an `emerging strategic industry’ under the “Made in China 2025” and 13th Five-year Plan initiatives. The government has rolled out a set of policies to support R&D, manufacturing and consumption of new-energy vehicles as well as the expansion of charging facilities. On the other hand, Phase IV fuel consumption standards for passenger vehicles will take effect on January 1 2016 and all manufacturers across the board are required to meet an average fuel consumption (CAFC) target of 5.0 L/100km by 2020. Several automakers have already ramped up investment and expanded capacity on energy saving and new energy vehicles. We expect that production and sales of new-energy vehicles will continue to grow rapidly in 2016. It is worth noting though that at no more than 2% of the overall market sales, NEVs are at the moment incapable of leading the transformation of Chinese auto industry.

(See Chart E)

Independent aftermarket to flourish in the wake of new antitrust regulations

In the wake of new antitrust regulations, auto parts sales and routine maintenance will gradually be replaced by independent aftermarket (IAM). More than 20,000 4S stores nationwide will be forced to transform their business models.

As an independent aftermarket is still in its infancy in China, service providers have little bargaining power and profitability is minimal. A six-ministry joint regulation that requires auto manufacturers to disclose their maintenance and repair technology information will take effect on January 1 2016 while another regulation has affirmed equal status for “spare parts of equivalent quality”. The new regulations mandate full and non-discriminatory access to all spare parts, repair and maintenance information, and the relevant diagnostic tools, along with free distribution of spare parts. Taken together, these new regulations represent the first step towards levelling the playing field for IAM channels.

Click to enlarge images

Telecommunication

4G+ era, operator breakthrough, China Tower IPO and MVNO shakeup

"Trend followers" and "necessity buyers" the next wave in 4G and the rise of 4G+

Recent Deloitte China research reveals that most of the "Early adopters" and "Early Considerers" have already subscribed to 4G services and that the market will gradually reach a saturation point and competition will continue to be heated in the future. 4G service subscription still has enough room to grow with regard to "Trend followers" and "Necessity buyers". Nevertheless, operators need to be careful with these market segments, and offer product portfolios or bundles with competitive prices so as to attract users who are sensitive to prices and conservative with new techs. Recent construction and rollout of 4G+ will speed up and bring innovation to telecommunication's business models, making it possible for subscribers to communicate with one another at anytime and anywhere with faster speed and higher quality.

(see Chart F)

Operators’ breakthrough will meet challenges

Operators are under pressures from two fronts; the market competition and squeeze of OTT application and service providers from the outside, and the “business tax reform VAT” and the operation costs compression from the inside. Although the overall business volume and business income continue to increase, the growth rate has been declining. Three obstacles need to be tackled:

- Contradiction between traditional operation and new competition environment

- Contradiction between static operation strategy and dynamic market change

- Contradiction between self-oriented and customer-oriented

China Tower set to go public while exploring mixed ownership system

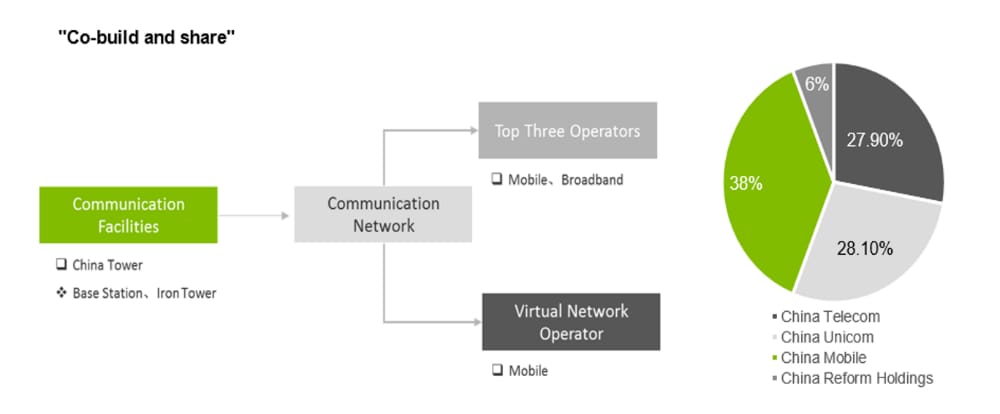

By the end of 2015, most of operators' towers will have been handed over to China Tower, indicating that China Tower will soon complete the second stage of its "three-step" strategy, that is, operating and maintaining more than 1.5 million towers worth¥231.4billion in assets. China Tower's most important current plan is to go public and develop a mixed ownership system. To promote the listing and restructuring, China Tower has adopted the shareholder ownership system of the top three operators and China Reform Holdings Corporation. This is an important step that aims to deepen reform of the telecommunication system and promotes the principle of “co-build and share” with regard to communication facilities. By the same token, it is also regarded as an effort to actively explore new ways of state-owned enterprise restructuring and mixed ownership economic system.

(see Chart G)

MVNO's trial ending soon, market positioning is key to winning

By the end of 2015, the two-year trial for MVNO services will soon come to the end. The MVNO users have grown to about 13 million. The Ministry of Industry and Information Technology will review the operating results at the end of year and issue license to the qualified MVNO. After getting their licenses, MVNO operators will have to make key decisions on strategy and operations to keep them competitive in the market. At current stage, there are three problems MVNOs ought to resolve:

- Simple resale business mode should be changed.

- Effective synergistic effect has not been formed.

- Resource cost is quite high.

Click to enlarge images