Perspectives

The Deloitte Research Monthly Report

Issue XXIV

17 March 2017

Economics

A cautious retreat from GDP target

The overall tone is for growth and stability

The annual National Party Congress is about setting the tone for economic management in the coming year and this year is no exception. Again, like the previous four years, the critical issue is the trade-off between economic growth and reform. This trade-off becomes more fraught with danger as time goes on because of the continued buildup of leverage. (In spite of the sober messages on “L-shaped economic trajectory” from the authoritative figure -- please refer to his press interview last May). This year, the policy bias is towards economic growth, mainly because of the emphasis on stability in the run up to the 19th Party Congress (October 2017). Despite the strong policy bias towards growth, the Government has made some admirable attempts to move away from an overly ambitious GDP growth target. For one thing, it has repeatedly said that there will not be any “potent stimulus” given to the economy.

Another significant change lies in the language that the top leaders are using. “About 6.5%”, coming from top leaders’, is a significant change from “6.5% to 7%” - which is what they were saying in 2016. But even a GDP growth rate of about 6.5% would require a relatively expansionary fiscal policy assuming that monetary policy will in fact be turning neutral in 2017 as the growth of money supply is limited to 12% yoy (as compared to 13% yoy in 2016). Indeed, as the Fed moves closer to tightening interest rates (1st rate hike in March, then followed by another 2-3 times in 2017), the dollar could get pushed higher. Another short-term bullish factor for the dollar is the long-speculated border adjustment tax which has been touted by President Trump. At this juncture, there are scant details on the mechanism of such a tax, but if the main motivation of introducing this tax is making American products more competitive, then intuitively one can predict that such a tax would make exports cheaper and imports dearer. If the US trade deficit actually does go down thanks to such a border adjustment tax (the likelihood of implementing the tax is probably 30%), the dollar could get an additional boost, over and above the widening interest rate differentials which favor the greenback. Furthermore, if there are no meaningful changes in the savings rate in the US, the dollar needs to strengthen further in order to slow down the economy which is exhibiting signs of overheating.

As almost 20% of China’s exports go to the US, the external environment in 2017 is much more challenging than in 2016. The best policy response we see is to quickly shift to the lower limit/bound of “about 6.5%” (for example, policymakers could implicitly state that 5% GDP growth is perfectly ok) so that fiscal policy could be less expansionary. If fiscal policy is too loose, China could face the risk of missing the inflation target (set at 3% in 2017), and in turn undermining the stable RMB exchange rate.

Gauging right growth rate

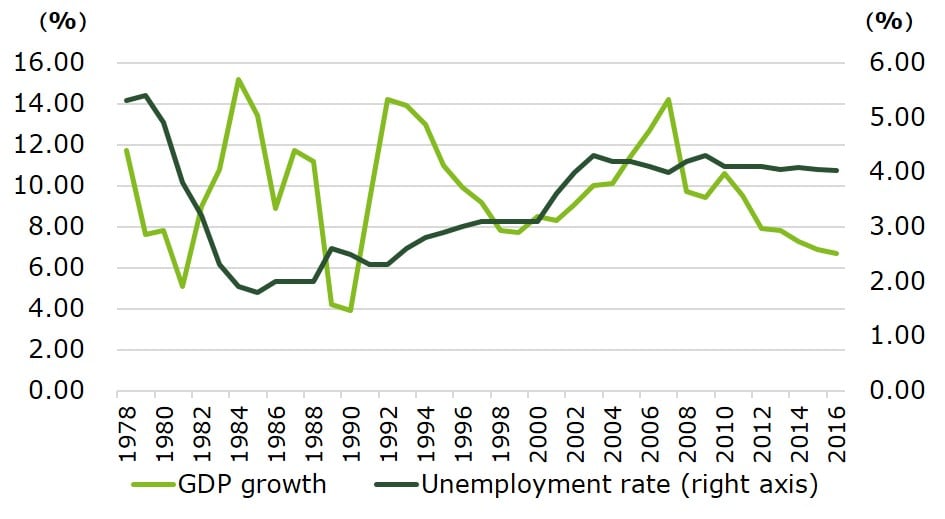

The notion of “About 6.5%” has two purposes – 1) to provide policymakers leeway in case GDP growth falls short of the target; 2) 6.5% is the necessary pace for China to achieve the goal of a “moderately affluent” society by 2020. On the job creation front, the goal in 2017 is to generate 11 million jobs, compared to 10 million in 2015 (which was comfortably exceeded). As the Chinese economy is undergoing its transformation, the inverse relationship between GDP growth and the unemployment rate (the so-called Okun’s law) may not apply. For example, during the height of the Asian Financial Crisis in 1998, the government’s back-of-the-envelope calculation suggested that 1% of GDP growth would be translated into 2 million jobs. Based on this calculation, the government initially pledged 8% of GDP at the time. This 8% GDP growth target and no-devaluation commitment boosted China’s prestige when the region was beset by deep recession and capital outflows. Since then, 8% has become a magic figure – symbolizing confidence and stability - for the last 20 years. It is widely agreed in policy circles today that the RMB4trn (actually more, thanks to the actions of over-zealous banks), despite a short term spike in GDP growth between 2009 and 2010, actually resulted in an overall depletion of asset quality due to less efficient allocation of capital. This is why, in the last two years, top leaders have been adamant about not engaging in any more “potent and powerful stimulus” packages. According to Premier Li Keqiang, capacity reduction of steel and coal will be 50m tons and 150m tons respectively in 2017. However, enforcing a shutdown of steel mills and coal mines when commodities are rising on a global cyclical upswing is a tricky matter. As Mr Chang Zhenming, chairman of CITIC, put it: as capacity reduction will be more challenging in 2017, the main vehicle for restructuring debt-ridden SOEs will be debt-equity swaps. A higher GDP target will be a huge deterrent to local governments’ cleansing of zombie companies.

A less evident side-effect of a powerful stimulus is actually the drag on job creation. In order to understand this counter-intuitive hypothesis, we must understand that the Chinese economy is also a dichotomy of a rising New Economy and a struggling Old Economy. The typical stimulus, which tends to target infrastructure because it has immediate impact on headline GDP growth, will benefit the Old Economy more and take away financial resources from the New Economy. This will impact job creation.

Chart: A lower GDP growth rate unlikely to cause a rising unemployment rate

Avoiding a currency war

Thanks to the tough measures taken to control capital outflows, February’s forex reserves rose to $3.01trn for the 1st time since June 2016. The question is not whether such measures are sustainable but rather, what is the cost of a stable RMB exchange rate to the economy? As we have been arguing all long, for a very open economy like China’s, the administrative cost of implementing capital controls can be very high. Due to loops in external account, it is simply impossible to verify and monitor all trade transactions. In addition, because the line between the current account (good and services) and the capital account (portfolio investment and real estate) has become somewhat blurred in today’s world, authenticating trade transactions can become a mind-boggling exercise. In practice, this means a more lengthy approval process of transactions at both local and central levels. As a result, the RMB is effectively devalued as many transactions which were previously considered normal can only be executed at a higher cost. There can be no doubt that the existing exchange rate has made the real economy bleed. But at the same time, dollar hoarding behavior has been curtailed as the general public has regained confidence in the stability of the RMB exchange rate. We have been of the view that the RMB exchange rate is not uncompetitive per se, but the desire of firms and consumers to diversify their assets will weigh on the RMB. A stable RMB exchange is also a gesture of goodwill to the Trump administration who is pressuring major surplus countries (China and Germany are on the top of the list which contains countries running large trade surplus). In the medium term, we do think economic calculations will trump political arguments and if it comes down to economic growth or a stable RMB exchange rate, policymakers will favor the former.

Supply-side reform

There has been much debate and discussion on the unique features of China’s supply-side reforms as it flies in the face of conventional wisdom, i.e. tax cuts and deregulation. The main thrust of China’s supply-side reform, in my view, is to bring down excess capacity in certain sectors, but at a gradual pace. Apart from the concrete targets set by the Premier Minister Li Keqiang on coal and steel, Xiao Yaqing, the Head of State-owned Assets Supervision and Administration Commission (SASAC), whose main responsibilities are to supervise large SOEs, has warned large SOEs not to get into reckless investment. This is significant as de-leveraging is more about belt-tightening and restructuring of SOEs than simply reducing excess capacity. The appointment of Guo Shuqing, as chairman of China Banking & Regulatory Commission (CBRC), is a signal that greater emphasis will be placed on banking asset quality. If de-leveraging focuses on SOEs, then other actors of the economy must pick up the slack. The Government has indicated that foreign companies will be allowed to raise capital in the domestic debt market. Should the domestic debt market be opened to foreign companies, the current policy of tight control over capital outflows might be eased as confidence slowly returns to the RMB. At the closing day press conference, Premier Li announced that there will be a debt market link between the mainland and Hong Kong, similar to the schemes that link Hong Kong stock exchanges with bourses in Shanghai and Shenzhen which have proven to be very successful. The purpose of these measures is to integrate China's financial markets with the global market in a controlled fashion.

In conclusion, NPC has produced few surprises. The most important lesson we can take away from it is that policymakers are aware of the harmful side-effects of fiscal stimulus packages and will gradually guide GDP growth lower as long as the job market remains healthy. Therefore, we see no reason to change our 2017 GDP growth forecast of 6.2% and USD/CNY of RMB 7.3 to the dollar.

Retail

E-retailers aim at dominating traditional platforms

National Bureau of Statistics has reported that total retail sales of consumer goods registered a year-on-year increase of 9.5%, a 10-year low, to reach RMB 5.80 trillion in the first 2 months of 2017. According to the agency, such sluggish growth was due to dramatic decline in car sales growth (certain tax benefits were phased out last year) and lack of growth drivers (as cars in 2016). However, online retail sales have reached RMB0.86 trillion, a whopping 31.9% year-on-year increase. The ratio of online retail sales of goods to total retail sales of consumer goods increased 1.6% to 11.1% (9.5% in the first 2 months of 2016) and the penetration rate kept rising.

New Retail has now become a key word in China's retail market and will continue to be the main theme in years to come. Faced with the slowdown of China's online retail market (the year-on-year growth of China's online retail sales fell from 33.3% in 2015 to 26.2% in 2016 ), E-commerce giants began searching for new avenues to grow their businesses. Cash rich, they are now leading the industry restructuring and making sure that they are at the centre of the chain. The integration of the offline resources of traditional retailers and the technologies and innovative thinking of internet companies is what drives the New Retail movement. But leading traditional retailers may also come up with their own approach to New Retail through in-house innovation and resource consolidation. As such, the field is wide open and full of possibilities.

In essence, New Retail involves the restructuring of traditional retail business to include the integration of online and offline resources. It also involves a complete rethinking of the production process itself, the relationship between retailers and consumers, the consumer experience and so on. In this restructuring, technologies such as Big Data, the Internet of Things, Artificial Intelligence and the like, will be used for satisfying or even pre-empting consumers' demands and maximizing the consumer experience will become the objective. At the recent national “two sessions” conference, Xiaomi’s founder Lei Jun shared his understanding of the New Retail movement which, in his opinion, is all about the integration of online and offline resources and the adoption of technologies and innovative thinking to help retailers improve consumer experiences and promote efficiency.

Of late there have been some significant developments in this line. In February 2017 Alibaba signed a strategic partnership agreement with Shanghai Bailian Group (one of the largest retailers in China, ranked 121st by Deloitte in its `Global Power of Retailing 2017 Top 250 Retailers’ study), another huge move after Alibaba's investments in Sanjiang Shopping Club. Since 2016, Alibaba has increased its alliances with traditional retailers through equity investments and strategic cooperation to increase its presence in offline retail.

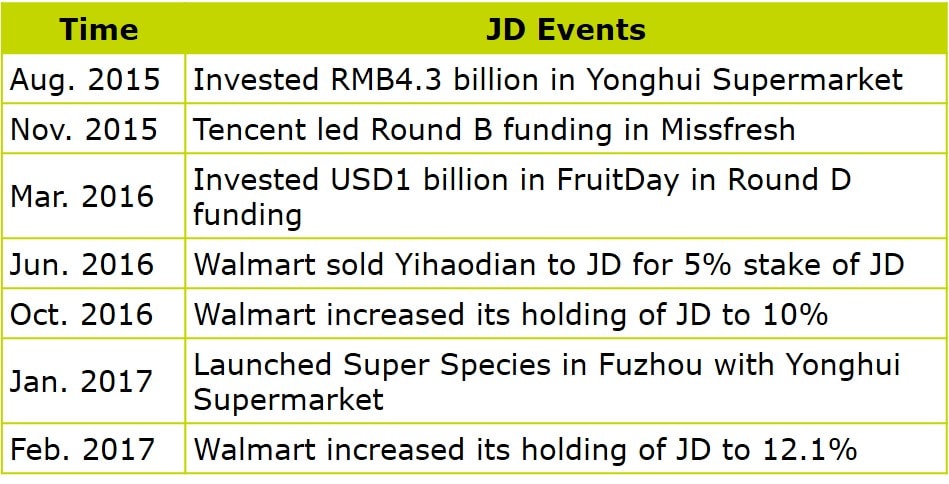

Another Chinese internet behemoth JD is also speeding up its negotiations with offline resources and multi-businesses. Walmart, which increased its JD holdings to 12.1% in February 2017, has made JD its most important partner in China. In January 2017 JD and Yonghui Supermarket launched a new experience store dubbed Super Species, a store similar to Alibaba’s Hema. Both Hema and Super Species are regarded as important pilot projects in the vanguard of the `New Retail’ movement because of their espousal of new thinking and new technologies.

Technology

Machine learning at your fingertips

Recent breakthroughs in computational capability and machine learning, coupled with the accumulation of big data, has set the stage for the proliferation of Artificial Intelligence (AI). The Chinese government is looking seriously at AI. During the recent "two sessions" conference. Premier Li Keqiang spoke about AI in his report on government work for the first time, which sent a strong signal that China would boost AI development. Last year, AI was also incorporated into the 13th Five-Year Plan for National Science and Technology Innovation.

For some time now, machine learning has been at the core of AI. It is designed to simulate every aspect of the human brain’s structure and function with elements representing neurons and their interconnections via computer models.

In essence, machine learning is a way of using cloud data to create algorithms which allow the computer to learn from and make predictions on data. But this approach has two major limitations, one of which is the dependency on the transmission of data. If the network connection is down, mobile devices then cannot complete tasks independently, which will create safety issues in domains such as healthcare, autonomous vehicles and unmanned drones. Further limitations include the huge amount of electricity that large cloud server clusters consume to help realize machine learning.

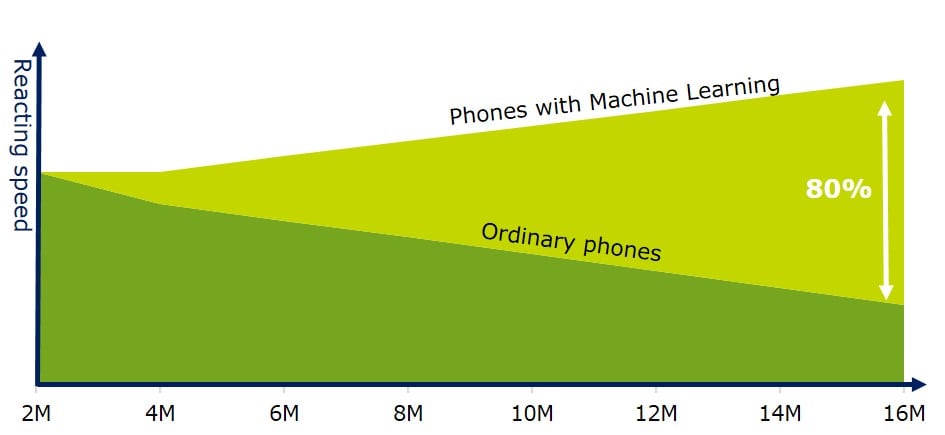

Fortunately, AI chips and neural network algorithms adapted to mobile devices are expected to make significant progress in 2017. This will make it possible for machine learning to be executed on mobile devices independent of cloud data. It allows mobile devices to perform machine learning tasks even when not connected to a network, such as indoor navigation, image recognition, augmented reality, voice-recognition and language translation. Some smartphones are already equipped with machine learning capability to allocate performance resources after analysing user usage behaviour, which means that the system will increase its response time and speed as users spend longer amounts of time on their devices.

Chart: Reaction Speed Ordinary Phones vs Phones with Machine Learning

Machine learning on mobile devices can be used in education, healthcare, smart home, Internet of Things (IoT) and many other areas. For example, making specialized study plans in the terms of student’s individual learning curve to analyse the pattern and progress of his/her knowledge acquisition; wearable medical equipment that can track and analyse patient’s health in real time, warn and react when unusual conditions are identified, and even diagnose and treat some types of diseases; smart home systems which will manage household equipment based on the interaction between the owner and devices after learning user’s living habits. Meanwhile, IoT devices will be equipped with self-detection systems to diagnose and fix malfunctions.

Thus as machine learning goes mobile, aided by AI chips and compact neural network algorithm, will allow for optimal experience at user's fingertip in the future. As Apple CEO Tim Cook put it “AI will make this product [the iPhone] even more essential to you [the customer].

Life Science & Healthcare

Medical insurance reform weighs on drug prices

On February 21, China announced the revised National Reimbursement Drug List (NRDL) which is the group of drugs covered by the basic medical insurance. The much-anticipated list of reimbursable drugs includes 2,535 chemical and traditional Chinese drugs, 339 more than the current list last updated in 2009. In addition, a mechanism has been established to include medicines on the NRDL after the national price has been negotiated.

Innovative domestically produced drugs are encouraged

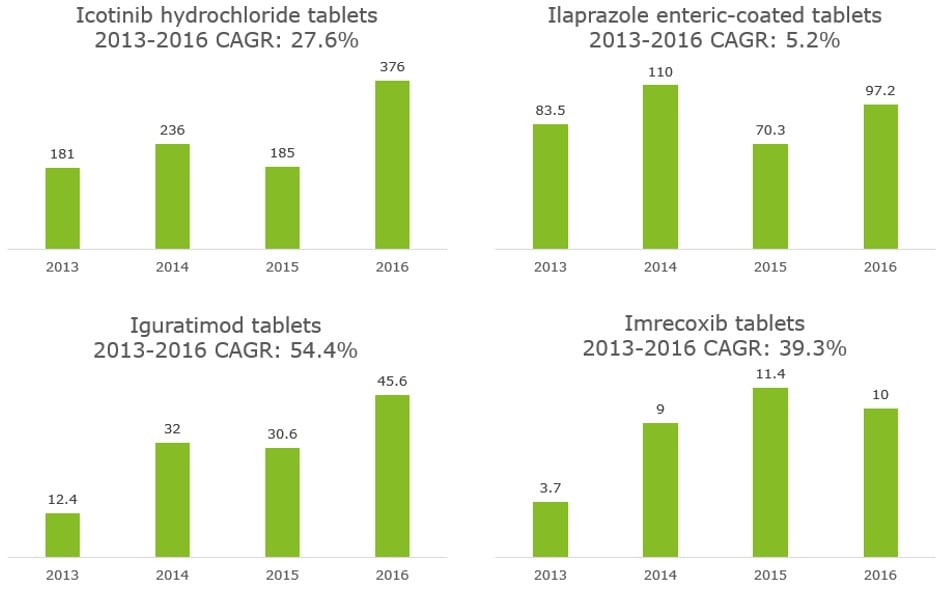

The latest NRDL reflects the direction of policy support for innovative domestically produced drugs. It has shifted the emphasis onto review of the new domestic drugs approved for sale after the last update in 2009. Several innovative domestic drugs have been added this time, including Icotinib, Ilaprazole, Iguratimod and Imrecoxib. As domestically produced drugs are more cost effective than imported ones, the government encourages the use of such drugs to help reduce healthcare expenditure. This policy shift will not only improve patient’s access to innovative new drugs, but also boost the domestic market and motivate enterprises to invest more in R&D.

Chart: Sales of innovative drugs newly added to NRDL (RMB, million)

A tradeoff between price and market share is an essential part of the national negotiation on drug prices

The latest update also covers 45 patented drugs with excellent clinical value but high asking prices that will be slated for the second round of national drug price negotiation after which they will probably be added onto the NRDL. As inclusion on the NRDL is likely to lead to massive sales growth (for example, the sales of Icotinib whose price has been cut by 54% in the first national price negotiation, have doubled in 2016), many pharmaceutical firms have been inclined to reduce prices during the negotiation in order to gain greater market share. However, it is worth noting that since most domestically patented drugs are still in the process of recouping R&D spending, enterprises would be better off to strike a balance between the benefit of a bigger market share and loss of revenue from price reduction. (All the drugs in the first national negotiation have undergone a price reduction of over 50%.)

Medical insurance payment system reform makes cost effective drugs appealing to hospitals

The NRDL announcement also demands that all provinces accelerate the establishment of a medical insurance payment system based on China approved drug names (CADN) rather than on brand names. That is to say, on the premise of being equal in quality and curative effect, drugs under the same CADN will be reimbursed at the same price level by the medical insurance agency, and the hospitals are allowed to retain the difference between the selling price and the reimbursement price as profits. The hospitals are thus incentivized to procure drugs at lower prices, which will benefit domestically produced innovative drugs (as they can replace expensive imported drugs) and make the competition amongst generic drug producers more intense.

Provincial reimbursement drug list is the next arena

For those drugs excluded from the new NRDL, provincial reimbursement drug lists are the next arena, especially in those provinces with large populations and relatively advanced economies. The current policy stipulates that provinces can make adjustments to the varieties of drugs in Category B within 15% of the total number. At this stage, the pharmaceutical companies selling non-exclusive drugs will probably make concessions in price to secure larger market shares.

In conclusion, China is now committed to medical cost control through a policy mix that includes tendering and medical insurance. Medical insurance is being transformed from a "passive payer" to a "strategic buyer" which can dictate drug prices, giving rise to a "New Normal" for pharmaceutical enterprises.