Perspectives

The Deloitte Research Monthly Outlook and Perspectives

Issue XLVII

30 April 2019

Economy

China: real economy and a roaring stock market

2019 has been a good year for equity markets in general, and especially good for risky assets such as emerging markets. Amongst the latter, China stood out (Shanghai A shares up by 24%) as the best performing bourse following a dismal 2018 (down by almost 26%). As we all know, the stock market is a fairly reliable leading indicator of corporate profits as well as the health of the broader economy. But the question is, are roaring A-shares a prelude to a cyclical recovery in China or not? If so, would such cyclical upswing be able to offset some of the adverse effects of a potential US slowdown? For, in the final analysis, the Fed's decision to halt its tightening was partially predicated on considerations of a potential slowdown in China. Should policymakers in Beijing reassess their policy responses gearing for growth if the `upswing’ is stronger than expected? While a nearly completed, "epic" trade deal (as proclaimed by President Trump) may pave the way for another Xi-Trump summit, would any mutually agreeable measures be put in place to ensure implementation of the deal and to track progress?

Let's begin with the inherently volatile A-share market in China. 2018 was a very poor year as domestic deleveraging and worsening US-China trade tensions exacerbated the bearish sentiment in the market. However, the breakthrough in trade talks last December at the G20 meeting in Argentina and the halt on regulatory tightening somewhat restored investor confidence. Moreover, a slew of policy pronouncements since China's 2019 two sessions meeting have resulted in both enhanced liquidity and increased business confidence. First and foremost is Premier Li Keqiang's reiteration of his pledge to cut taxes/fees for firms and consumers (roughly RMB 2 trillion in 2019). Second, is the easing of monetary conditions. Although the PBOC has not officially lowered the reserve requirement ratio, the message of easing is loud and clear since last autumn. Commercial banks have been given strong incentives, including fiscal subsidies, to ramp up their lending. For example, if a bank charges a firm 6% on its loans for equipment purchase, the government will give the banks a 1-2% rebate. Hence, for firms there is a real reduction in the cost of borrowing.

Apart from the easing of borrowing costs, China's stock market rally is also underpinned by other factors such as the US Fed's drastically changed stance vis-à-vis interest rates (the yield curve points to a rate cut in 2020), a likely trade deal between China and the US, and a slowdown in domestic deleveraging. In addition to the above, MSCI's decision to increase the weight of China’s A shares in its indexes from 5% to 20% could entail more capital inflows in the long run. We believe that the greatest boost to investor sentiment will come from the expectation of further liberalization based on a fruitful trade deal and the rapid and concrete implementation of its clauses. Should this be the case, and if economic growth has stabilized, policymakers will need to make sure they don’t end up "overdoing" fiscal relief.

Given the above scenario, it should come as no surprise that the IMF has raised its 2019 growth forecast for China from 6.2% to 6.3% on the back of a surprisingly strong showing of Q1 GDP growth at 6.4%. Interestingly, the phrase "structural adjustment" has once again resurfaced in the most recent briefing by the Politburo after disappearing for over six months since late October last year. At the same time, policymakers have been talking repeatedly of how important it is to ensure `greater efficiency of fiscal stimulus’. Hence, what we are likely to see is a policy bias that is pro-growth with targeted fiscal relief measures rather than a flood-irrigation type stimulus as in 2008.

But what if policymakers cannot resist a strong dose of pump priming? While there is a risk and it is not trivial, we must also put such risk into perspective. In a low interest rate environment, pump priming will have a lesser impact on the debt/GDP ratio. The Chinese debt/GDP ratio, which stood at around 260% in 2018, would rise to 265% or 270% at most. However, given that the Fed is likely to put short-term interest rate hikes on hold for at least a year, China will have much room for maneuver. The real issue is whether policymakers will indeed `turn off the tap’ and gradually bring down leverage once growth is firmly entrenched. And finally, financial markets (famous for their short memories) may sell off by more than profit-taking on the news, should "an epic trade deal" lack substance and not live up to market expectation.

Financial Services

Preparing for NPL disposal in response to "the Dual Rises"

In 2018, the share of non-performing loans (NPLs) of Chinese commercial banks continued to rise, with the NPL ratio rising to 1.83%. This is partly a result of the classification of loans having become stricter. Regulators have been encouraging some banks to record loans 90 or 60 days overdue as NPLs, which will keep the heat on bank credit asset quality for the next few years and while raising the bar on how NPLs are disposed of.

Pay attention to "the Dual Rises" and 2020

Both the amount of NPLs and the NPL ratio (the Dual Rises as they are commonly referred to within the industry) at commercial banks have been on the rise in the past five years. At the end of 2018, the total NPLs broke through the RMB 2 trillion ceiling, recording a CAGR of 28% over the past five years, double that of total assets (which stood at 14%). Given the ongoing structural adjustment and the uncertainty in the global economic environment, it is highly probable that a slow uptick in “the Dual Rises” will continue for the next 3-5 years. Bank balance sheets will not be something to write home about for some time.

The China Orient Asset Management Company (COAMC) which has been conducting surveys of China's financial non-performing asset market for the last 12 years released its 2019 annual report on April 10. According to 44.55% of the respondents, NPLs would peak in 2020 as the quantity of special mention loans (SMLs) (less than 90 days overdue) will peak and then be turned into NPLs, swelling the amount of NPLs to their highest level ever. However, once this bitter moment is passed, NPL numbers will fall dramatically.

Others believe that the scale of banks' NPLs may already have peaked but that default issues will come to a head as the economy restructures and new risks emerge. What all those surveyed were unanimous about is that, whatever the reason, the current level of bad debts will certainly continue for quite a long time.

Pay attention to NPLs in real estate

The rapid development of the real estate (RE) market in the past few years has been fueled mainly by multiple leverages, hence to determine the quality of bank loans one must look closely at the real estate market. Regulatory data has revealed that industries with high NPL ratios include, in descending order, wholesale and retail, manufacturing, mining, construction and RE. Data from banks shows that the NPL ratio of the RE industry doubled from 0.48% in 2013 to 1.10% in 2017 – a figure that in itself is not high, especially in comparison to the NPL ratios of other industries, but which could very well prove inaccurate as many RE enterprises turned to other channels such as commercial paper and trust products for financing after the banks tightened access to credit. Hence repayment pressure on RE enterprises is probably higher that what it appears to be on the balance sheets.

In 2019 the RE market will remain under pressure. As the shantytown transformation program in third and fourth-tier cities and the related monetization bonus (government compensation) programs wind down, property prices in these cities will probably fall. In 2016 and 2017, the NPLs related to housing increased by 27% and 23% respectively, and the growth rate of NPLs is expected to be above 20% in the next few years. The NPL ratio of the RE industry is projected to increase to 1.3% in 2019, and banks will remain under significant pressure.

Improving the efforts of NP asset disposal

"2020 is the time when commercial banks are sad and the real economy is under greater pressure", the COAMC survey reported. To create an appropriate environment for disposing of NPLs, careful attention must be paid to the regulatory framework and the relevant market mechanism.

Thus risk prevention should be done in advance to create an appropriate environment for disposing of NPLs, including both the market and regulatory environments.

In the current NP asset market, except for the traditional four Chinese Asset Management Companies (AMCs) (the Great Wall, Huarong, Cinda and Orient) which were established in the 1990s, there has been much more players including provincial, local and bank AMCs, with a high degree of marketization. Also, opening up the financial sector will benefit domestic institutions as they will be able to learn from the practical experience of their foreign counterparts in areas of information technology, risk management and asset disposal.

Recent regulatory measures have prompted banks to speed up their NPL disposal efforts. First, the loan loss provision coverage standard has been reduced to between 120% and 150% with the loan loss provision ratio reduced to between 1.5% and 2.5%. Higher profits due to lower provisions will help banks make room to dispose of NPLs.

Secondly, it is not a mandatory requirement to "include loans 60 days overdue into NPLs" at present. But if the implementation scope expands, it will put pressure on the NPL ratio and force banks to continue to reduce non-performing assets.

Automotive

A 5G bonanza for the auto industry

Powered by 5G C-V2X technology, fully autonomous cars are all set to become a reality as both carmakers and internet companies rush to embrace the new C-V2X technology.

Touted for its high bandwidth, low latency and highly reliable communication links, 5G technology has played a vital role in enabling precise positioning, 3D mapping in real time (both are considered essential to autonomous driving) as well as remote updating of software and firmware. Besides, the 5G-based C-V2X system (a high-speed wireless technology that enables vehicles to talk with one another, pedestrians and road infrastructure) will allow vehicles to share their views of the surroundings and their intentions, which will help solve many problems facing autonomous vehicles.

Nevertheless, the impact of 5G on the auto industry goes far beyond an enabling technology that allows for greater inter vehicle connectivity and the realisation of the self-driving car dream. 5G is expected to bring about a paradigm shift in the auto business because of the way it brings on board a host of other complementary technologies.

- For starters, 5G technology will recast the automobile value chain by remapping the profit landscape. For example, vehicle connectivity sustained by 5G technology will help forge a new way through which auto OEMs serve customers directly and increase their share of profit in the after-sales business. (Software updates are usually performed at authorised dealerships). 5G has amplified the cost and time saving benefits of OTA software/firmware updates, providing auto OEMs with direct control over in-car data management throughout a vehicle’s lifecycle and continuous touch points with consumers.

Meanwhile, the vehicle itself is all set to be a mobile data platform. With the massive boost in network speed that comes with the adoption of the 5G network, vehicles will be able to capture and save in-car data and position information and transmit the data back to the OEMs in real time, enabling the later to remotely monitor and take control of the vehicles in case of an emergency. In addition, in the near future, cars will become giant mobile phones, helping to make reservations and receive online coupons whenever they are near a restaurant or a hotel within range of communication. - Secondly, 5G will usher in new business opportunities. Vehicles with V2V, V2P, V2I capabilities will make them more proactively involved in smart transportation networks. We have observed that many Chinese cities, since last year, have conducted vehicle-to-vehicle communication trials on highways with multiple scenarios from platooning and advanced driving to remote driving.

- Thirdly, there’ll be a major structural change within the auto OEMs. In-car data will witness exceptional growth thanks to the speed of 5G. But existing commercial structures do not support a large-scale use and monetization of vehicle data. In our opinion, automakers will have to create a new ecosystem that has the capacity to utilize data to power new services or contribute to increasing customer satisfaction. This will mean that automakers will, in effect, be able to act as data distribution centres for upstream and downstream players.

Energy

Powering GBA with smart energy

If the Guangdong-Hong Kong-Macau Greater Bay Area (GBA) is to be the growth engine for China's new economy, the energy industry will be the fuel of that engine.

Decoding GBA's energy landscape

There are three key words at the core of the region's future energy security – reliability, sustainability and affordability.

Reliability is the top priority. Growth in electricity consumption in the region has outpaced generating capacity, with Hong Kong importing about 30% of its total electricity consumption from mainland China and Macau 80%. Moreover, electricity demand is slated to reach 700 billion kwh by 2023. At the same time, the region is vulnerable to typhoons and other extreme weather conditions, therefore its power grid needs constant monitoring and capital investment. This is why China Southern Power Grid has announced plans to invest 170 billion yuan in the region by 2022 to safeguard the power supply from natural disasters and meet the growing demand for electricity.

Sustainability is another shared goal. According to Guangdong's 13th Five Year Energy Plan, the share of renewable energy in overall energy generation will increase “significantly” between 2016 and 2020. Hong Kong's latest `Scheme of Control Agreements’ (SCAs) between government and power companies introduced a feed-in tariff rebate to promote renewable energy. Power companies will pay HKD 3-5 per kWh to businesses and households who install solar capacity (e.g. roof top solar panels) for the energy they generate.

Affordability can't be compromised. Although rapid advances in renewable technologies have reduced the cost of construction and operation of renewable power projects, some projects remain economically unviable without the aid of government subsidies in the form of feed-in-tariffs. Guangdong has recently ditched plans to construct 32 onshore wind power projects, which would have provided and an additional 1.62GW of electricity capacity. The move is a response to the growing financial difficulties faced by the wind energy operators in the face of the termination of government subsidies. But as consumers (including tech data centers and manufacturing companies) are unwilling to pay more for their electricity, energy companies expanding their renewable portfolio will need to adjust their business models in order to remain profitable.

Keeping pace with smart energy innovation

In the future, de-carbonization will be interwoven with digitalization. Hence, smart energy solutions will be a growth engine for both energy providers and technology providers.

Integrated energy solution providers are already reaping the benefits in industrial parks as the proprietors switch to systems that combine electricity, heating and air-conditioning services in a single package. Guangdong itself contains over 80 industrial parks with increasing demand for integrated energy management systems that allow for the integration and digitization of multiple assets such as solar, biomass, combined heat and power, water turbines, wastewater turbines, battery storage and EV charging infrastructure.

We expect a wave of M&As between utility companies and technology providers. One reason behind the deals is the need for improved analytics to manage intermittent renewable generation. Another is to develop innovative products, services, business models and test use cases. For example, the largest power company in Hong Kong, CLP (China Light and Power), invested in AutoGrid, an energy management software developer based in Silicon Valley in 2018.

We believe smart energy will bring new opportunities for utility companies in GBA. However, the integration of multiple systems and the allocation of subsidies is not an easy job. They will have to pursue new projects in a disciplined and selective manner.

Life Science & Healthcare

Navigating a changing environment

The establishment of the National Healthcare Security Administration (NHSA) was one of the most significant things that happened in the healthcare sector last year. The "super" NHSA centralizes the power of all healthcare-related authorities, its mandate spanning everything from drug pricing to medical insurance payments. In addition, the NHSA has taken procurement rights away from hospitals and centralized it in their hands. After a year of operation, NHSA has successfully implemented several programs including insurance negotiations and "4+7" centralized procurement, signaling a brisk acceleration of a centralized procurement system in China.

As the procurement environment changes, market players need to review their planning framework to include short-term, medium-term and long-term strategies for growth.

Short-term——Establish the right team

A good short-term strategy should focus on reviewing the existing organizational structure with a view to enhance operational efficiency and reduce operational costs. Establishing teams with the right mix of staff is also extremely important. In addition, companies need to centralize major functions such as marketing, market access and sales in response to a centralized payment system. Another key component is to constantly follow a top-down strategy, which means that those at the corporate level should strengthen their leadership role when working with local teams.

Mid-term——Diversify channels and business models

In the medium term, market players should seek to diversify business models and channels instead of only focusing on the municipal hospital market. For example, they need to allocate more resources for discovering new retail and digital channels. Currently in China, only around 10% of prescription drugs are sold through retail channels in contrast to around 40% in the US. Hence, sales channels other than hospitals need to be developed.

At the same time, more attention should be paid to the county-level market as the government is promoting a tiered medical system which will empower them.

Forging alliances, especially with market disruptors such as technology companies, could be another way to create new business models.

Clinical innovation is the only way to long-term success

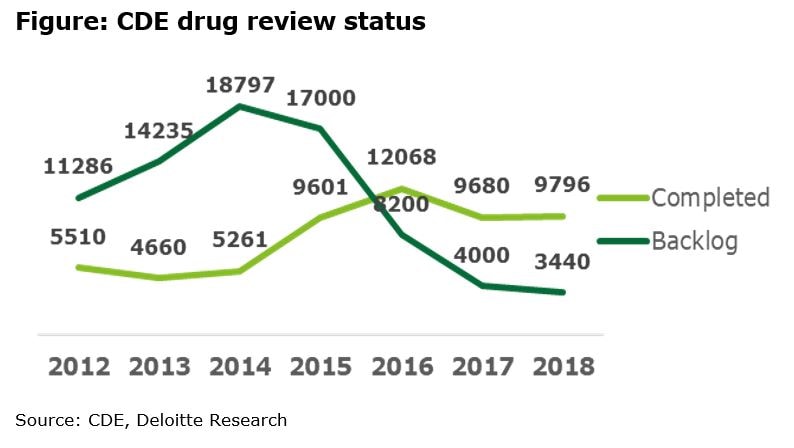

In the long term, clinical innovation is still the best way to create value and generate profit. In the past few years, the process of medical product reviews, approvals and launches in China has been significantly improved. The average launch lag of innovative drugs in the past decade used to be anywhere between 5 and 7 years. In the last two to three years, however, the launch lag has decreased significantly, and many innovative drugs have been successfully launched in China less than two years after their debut in the US.

Therefore, market players should devote more resource on new product development, pipeline management and launch excellence in order to drive long-term business growth.