Perspectives

The Deloitte Research Monthly Outlook and Perspectives

Issue XLVIII

30 May 2019

Economy

How to avoid escalation?

Are the US and China heading towards a new kind of cold war as the Economist magazine proclaimed or is what we are witnessing simply high-stakes brinksmanship in the run up to the next G20 meeting? The cover article in the most recent issue of `The Economist’ (May 18, 2019) expresses its concerns over the changing dynamic of the relationship between the US and China, the two largest economies in the world, where rivalry appears to have begun to prevail over reason. The main obstacle here has to do with creating rules when rule-breaking is becoming ever more tempting. But can rules be created before these two superpowers get locked in a bitter, mutually destructive battle?

These questions are indeed difficult to answer especially for the next 90-day reprieve (May 20 through August 19) before the Huawei ban takes effect, when a previously unthinkable level of tariffs has nonetheless been attained despite the 3-month truce. Meanwhile, financial markets continue to exhibit an almost unbelievable resilience. Most major global stock markets were at first rattled by President Trump's tweet on May 5 that he was going to hike tariffs on $200bn of Chinese imports to 25% ahead of the "last round" of trade talks (Dow Jones Index and A shares came off by 0.3% and 5.6% respectively). They subsequently recovered some of their sang-froid in the past two weeks. In particular, even the US stock market has held up despite the trade talk impasse and pressures from the US Administration to block Huawei (though, most recently, President Trump has said that Huawei can be part of the trade deal). Does this mean that global investors are sanguine in the belief that some sort of deal will be struck at the upcoming G20 meeting in Osaka (June 28, 29)? If such an assumption were plausible, would a resilient US stock market create more incentives for President Trump to play hardball?

In contrast, policymakers in China seem to be behaving quite cautiously. They have taken certain precautionary measures against a possible economic slowdown caused by an escalation in the trade conflict. For instance, they have permitted a mild depreciation of the RMB from 6.70 to 6.90 to the dollar. This is a sensible move and was expected by markets as it partially offsets the adverse effects of higher tariffs. Unlike in the summer of 2015 when a movement of less than 2% on the RMB exchange rate shocked global financial markets, there was no panic this time. The consensus is that the PBOC is likely to draw a line in the sand at 7.0, a widely viewed psychological threshold in China this year (we are slightly more bearish than the consensus for the simple reason that a weaker RMB is a necessary monetary lever at the present time). In addition, a special group to maintain employment stability has been set up this week and is led by deputy prime minister Hu Chunhua. The message is therefore clear: the Chinese Government will take whatever it takes to ensure social stability.

From China's perspective, the short-term goal, in our view, is to avoid escalation and to seek a resolution on trade and certain so-called structural issues. On the trade issue, we have been of the view throughout the trade talks that lower tariffs would be both a tactical and a strategic move for China. In the short run, if China slashes tariffs to the level of developed countries, it will prove that bilateral trade imbalances are indeed not so important in a highly intermeshed global economy. Such a move will also mitigate much of the criticism on China's trade barriers against US products.

We have been skeptical about the policy of greater purchases of US products. The recent breakdown in trade talks suggests that the US side is less inclined to take a quick-fix approach in addressing bilateral trade relations. Given that both have fired some bullets in the ongoing trade war (China has imposed retaliatory tariffs on $60bn of US imports of late), is lowering the tariffs still the right policy response for China? We think so. China has been vocal in confronting protectionism (President Xi's speech in Davos in 2017) and has pledged to share with other countries the economic fruits of China's vast domestic market (Global Times editorial on April 26, 2019). Lowering tariffs will help China achieve a number of objectives. First of all, it is in line with the stated policy of narrowing the gap between Chinese consumers' wants and domestic constraints. That is why it is prudent not to raise tariffs on imported drugs from the US. Second, various bilateral free trade agreements (e.g., China and Australia) are aimed at boosting trade between China and her key trading partners (China's import of iron and wines from Australia is a case in point). Why not take a bolder step to put China in a better position when dealing with more trading partners? Will lower tariffs perhaps better prepare China to join TPP? If the US wants to rejoin TPP one day, it is not in China's best interest to be locked out of the biggest trading bloc and deepest market in the world, and stuck in a managed trade relationship with the US. Therefore, it is fair to say that, in terms of improving market access, what the US demands from China is not inconsistent with China's reform agenda in the long run.

On the other hand, China should not yield to pressure from the US on maintaining a stable RMB exchange rate at any cost. It makes sense for China to target the RMB exchange rate based on a currency basket and gradually reduce interventions so that the economy could have the RMB as an important shock absorber. China purposely kept the RMB strong until May this year as a gesture of goodwill towards the US. But this could leave it open to accusations of manipulating the exchange rate if the trade talk impasse persists after the G20 meeting? The short answer is to have a more flexible exchange rate. Needless to say, such a more flexible exchange rate regime requires a more robust financial system. What could China do to improve its financial system and to defuse external criticism on artificially keeping the RMB undervalued? Again, the answers lies in taking bolder steps to improve market access. In practice, what we are advocating is to fast-track approvals of licenses for foreign brokerages, insurance companies, asset management companies etc. The reality is that current difficulties in trade talks should have injected even greater urgency into the move to open up the domestic economy in China. And finally, on the economic front, it is rational to beef up necessary social programs in order to prevent the social dislocation that would result from external shocks, but at the same time policymakers should resist the temptation of a 2008-type fiscal stimulus.

In conclusion, the present trade talk impasse can be mitigated by a faster pace of domestic reforms in China which will strengthen MNCs' supply chains. One of the challenges is that some of the contentious issues such as subsides simply can't be quantified as yet. Therefore, the only thing that can be done is to take concrete steps in opening up China's domestic market.

Retail

‘New retail’ evolution continues

With no let-up in the slow decline of online retail sales over the past 12 months, major retail players have placed more importance on ‘New Retail’ strategies to re-ignite demand. Fresh grocery service, with its untapped market potential, is seen as the next new retail battleground. According to iResearch, the fresh produce market represents RMB100 billion of inelastic demand. E-commerce companies have penetrated only 1% of it, with traditional farmers markets commanding a market share north of 80%.

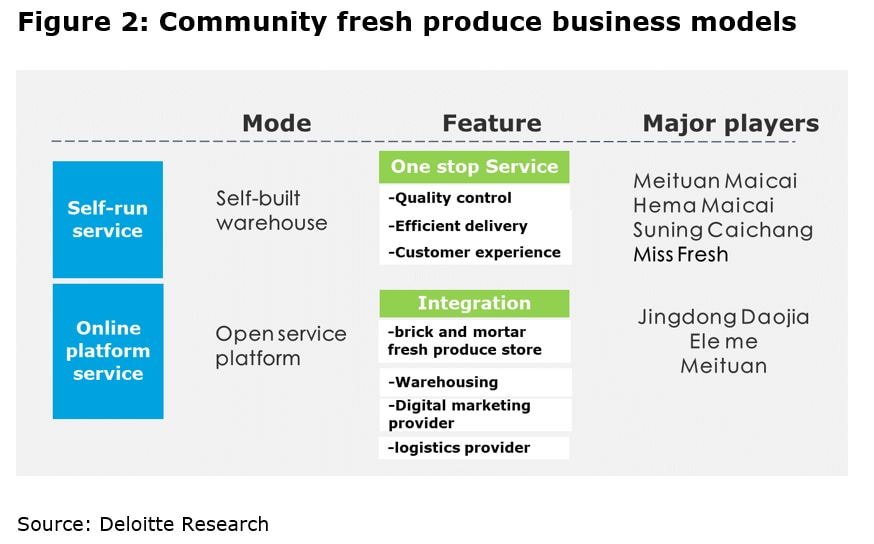

Until recently, large internet based companies such as Alibaba, Meituan, Shunfeng, Sunning were not only proactively transforming local brick-and-mortar fresh produce stores into their integrated online/-offline fresh produce supply chain, but also setting up self-run community warehouse to improve quality control and efficiency of delivery services. This is because the major players want to recast people’s fresh produce shopping experience through convenient online ordering, consistent quality products and efficient logistics. The fresh produce market is segmented. Consumers in first tier cities value convenience and instant gratification above price while those in second and third tier cities are very price sensitive. Hence, two community fresh produce business models dominate: self-built warehouse and platform operation.

The major self-built warehouse players include Tencent backed vertical e-commerce start-up Miss Fresh, Dingdong Maicai and large e-commerce companies such as Alibaba, Meituan Maicai and Sunning Maicai. The advantage of this model lies in its being able to control product and shopping experience quality through efficient delivery. However, self-built warehousing is asset-heavy. In order to ensure instant delivery, major players have to build a network of community based warehouses, which increase their inventory, labor, logistics and other costs.

Platform operation, the other model, seeks to serve suppliers and consumers through retail technologies. Its major proponents are large, internet based companies like Jingdong, Eleme and Meituan. This model, which relies more on the capacity to integrate existing resources into the supply chain, and concentrates on improving warehouse logistics, is asset light. Players only need to invest in technology and logistics. However, this model cannot assure the same level of quality control as the self-built warehouse model and hence the players’ brand image may suffer.

As the evolution of new retail continues, the future is becoming more defined …

- New retail is moving from single format to multi format and accelerating the exploration of community-based operations. At the high-end, selected supermarkets are being transformed into O2O integrated stores focused on selling high frequency, rigid demand products. Multi format, community-based stores aim to explore new markets for high margin household consumption.

- Start-ups now face rising barriers to entry as retail industry operations, logistics and supply chains become more digitized. Competition between internet giants and unicorns also continues to intensify.

Technology

Navigating through AI fog

In the next decade, artificial intelligence will be recognized as one of China’s most innovative and disruptive technologies. At the very top, the central government has set a lofty goal for China to become the world’s leading artificial intelligence (AI) power in the next decade. The Chinese government has also published a national AI strategy and laid out grand plans to invest over a billion US dollars in AI research and development.

At least 15 Chinese cities have joined the AI bandwagon: Beijing, for instance, announced a US$2.1 billion AI-focused technology park while Tianjin plans to set up a US$16 billion AI fund. In addition, private capital is flowing into the AI industry. In 2017, Chinese AI startups garnered 48 percent of all global AI venture funding, surpassing the United States for the first time. China is home to the world’s highest valued AI company, SenseTime Group Ltd. and also has the world’s second-highest number of AI companies right behind the United States.

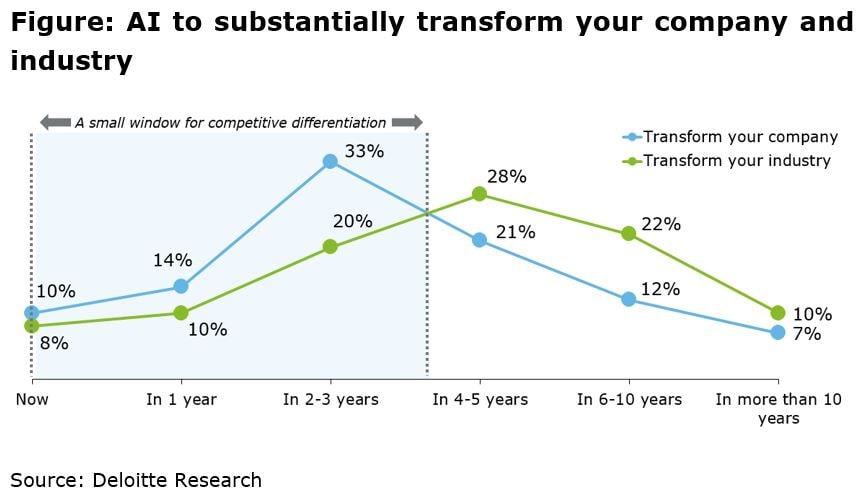

Our recent global AI survey showed that early AI adopters in China are embracing the Chinese government's grand strategy from the following perspectives:

- AI offers competitive edge. They believe that AI is helping to widen a lead or leapfrog over their competition (55% versus 37%).

- AI is crucial to success. Some 54% of the respondents consider AI to be “very” or “critically” important to the success of their businesses. We expect the percentage of respondents holding this view will grow to reach a global high of 85% in two years.

- AI is set to improve the workforce performance. Over 80% of the respondents believe that human workers and AI technologies will augment one another to create new ways of working. They also think that AI allows their employees to make better decisions and that will enhance employee performance and job satisfaction.

However, when it comes to integrating AI, many companies still don't understand how best to use AI to increase their productivity. Many others are struggling to identify ways to create business value using AI. The vast potential of AI has often resulted in unrealistic expectations on the part of organizations.

To navigate the "fog of confusion" that surrounds AI and maximize its potential, companies must prioritize their needs and identify transformative AI business cases. To realize business value from AI technologies, specific and measurable business outcomes must be tracked to individual business cases. For example, a retail store can utilize AI vision to track consumer's shopping behaviors such as how much time they spend looking at a particular rack and trace their walking path around the store. But how can these data turn into business value to drive more purchase is something that needs to be considered.

In other words, the challenge for management is to link technology initiatives to specific business results. For most companies, this means integrating AI capability into their existing or new applications. The highest area of impact in the short term will most likely come from realizing automation and helping humans to work, saving billions of hours in worker productivity. In the long run, the ability to improve and differentiate products via AI will drive business value and revenue.

Thus, companies can adopt a strategy combining the short-term and long-term approaches to manage their AI deployment and clarify achievable business goals for near-term opportunities, particularly in business use cases where AI can complement human work and decision making while, at the same time, focusing on the long-term potential of AI.

Logistics

Investment on the rebound

As the structure of the logistics industry continues to improve, greater investment is coming into the industry.

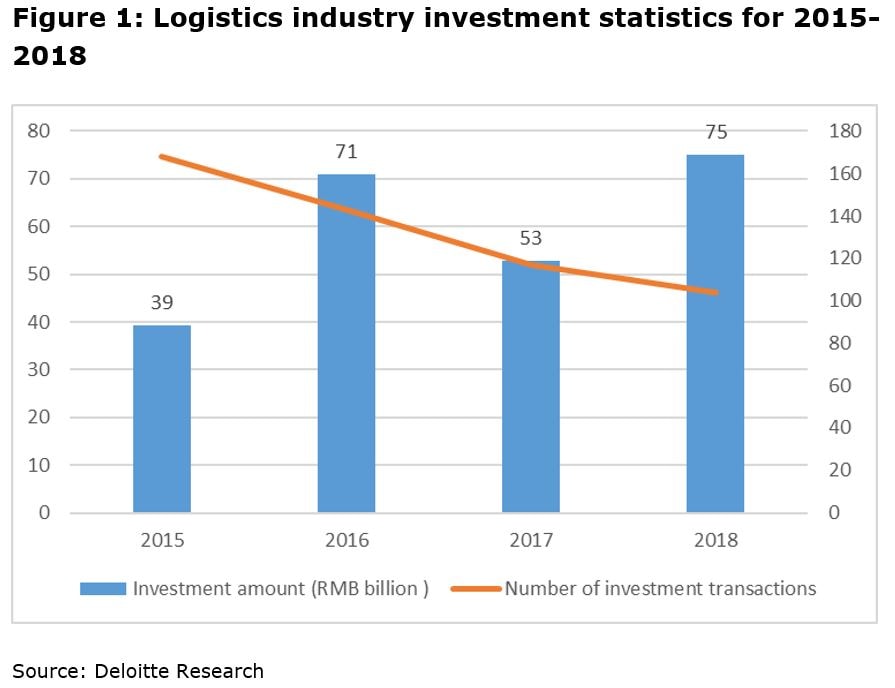

In 2018, amongst investments which were over RMB 100 million, logistics informatization, LTL (Less Than Truckload) express and the intra-city express delivery accounted for more than 60% of total investment, while warehousing, logistics hardware and supply chains accounted for 34%. These investments reveal a clear trend: the logistics industry is undergoing a yet one more upgrade.

This trend has continued in 2019. In Q1, investment in the express delivery business accelerated and a total of 11 logistics express service companies, including UC Express, Lala Move, and STO Express, secured financing worth RMB10 billion. The single largest transaction on record was Alibaba’s investment in STO Express on March 11, which topped RMB 4.66 billion.

There are several ways one can understand the new round of investment in the logistics industry.

Policy perspective: One reason for the new round of investment lies with the State. In 2019 Central Economic Work Conference defined "5G, Artificial Intelligence, Industrial Internet, and Internet of Things" as the "New Infrastructure", a key area of emphasis for the government. As a result, logistics infrastructure such as smart logistics parks, logistics networks, rural logistics and cold chain logistics will not only see further increases in investment but will also experience a jump in the scale of investment.

Technical perspective: In the 5G era, the demand will continuously increase for efficiency enhancement of new retail. As technologies (especially 5G) advance, there will be greater pressure put upon on the logistics industry to improve efficiency and accelerate the development of smart logistics. With the application of intelligent technologies in the scanning, sorting and transportation of goods, the efficiency of logistics operations has greatly improved allowing consumers to receive their goods faster and in good condition. With the scope of 5G connectivity increasing, there will be billions of smart devices connected to the network in the future and logistics efficiency will be greatly improved. Accordingly, investments in smart devices and logistics enterprises will increase.

Capital perspective: The BATJ-led capital investment in the logistics industry has set the standard for investment.

While “BATJ” – Baidu, Alibaba, Tencent and Jingdong - have all invested substantially, Alibaba has led the way, investing over RMB10 billion, far more than the combined total investment of the other three companies. As a result of BATJ's investment strategy, the entire market is moving from growth-oriented investment to M&A-oriented investment. The rationale behind the change is that the logistics industry has entered a stage of industry integration as the essence of investment is to establish a complete industrial chain for industry development. As the entire logistics industry will form a stable, profitable infrastructure once it achieves economies of scale and the network expands sufficiently, in the long term, this is a worthy industry to invest in.

Market perspective: Logistics in emerging markets are still hot. With a further influx of capital and technology in 2019, the logistics industry will be further transformed. Traditional logistics enterprises will have to struggle to survive while emerging markets will continue to grow strongly. There will be increased segmentation in the logistics industry and a change in scale. For example, the cold chain has reached a market scale of hundreds of billions of RMB while the scale of the LTL is worth over RMB 1 trillion and the scale of the intra-city express delivery is estimated at hundreds of billions yuan as well. The rapid development of these new markets is undoubtedly attracting active investors with capital. In addition, the intelligent logistics infrastructure, shared capacity systems, cross-border e-commerce logistics, and multimodal transport will all become the new growth drivers for the logistics industry in the next two years.