Perspectives

The Deloitte Research Monthly Outlook and Perspectives

Issue LV

16 March 2020

Economy

Another round of global monetary easing calls for targeted fiscal expansion

Over last weekend, the Fed has unveiled its latest easing by bring short term rates close to zero and rolled out $700bn of QE in order to stabilize financial market. Indeed, global financial markets have experienced heightened volatility in the past two weeks due to COVID-19 fears, namely an outbreak in the US and in the rest of Europe beyond Italy. Overall, equity prices have gone down and so have bond yields (10-year US Treasury yields crashed below 0.4% but only rose to around 1% recently) and both IMF and the OECD have slashed world economic growth forecasts in 2020 by about 0.5%. The risk of an economic downturn has resulted in another round of interest rate cuts. The US Federal Reserve was the first in line on March 5, followed by a number of countries including Canada, Australia, Malaysia, and the Bank of England on March 11.

In such an atmosphere of fear and uncertainty, the effectiveness of traditional economic tools such as monetary easing to restart a halted economy is highly doubtful. On the other hand, were central banks to flood the market with liquidity, there would be no downside at this point. This is the rationale behind the call for further easing coming from central banks across the globe. This call will become louder if oil prices go down even further. The $64,000 question is whether further correction of risky assets (equities mainly) would adversely affect consumer behavior in the US whose economy has been chugging along steadily as evidenced by the most recent payroll data which are highlighting a strong job market. The answer will depend on how fast and how far COVID-19 spreads and the resultant panic it causes.

China is likely to join the global easing chorus (on March 11, Premier Li Keqiang called for cuts of RRR and interest rates). The main objective of China's monetary easing will be about giving greater incentives to banks to channel funds into the real economy. On this, China does have a certain comparative advantage – a strong RMB, falling oil prices and policymakers' capacity to guide lending during crunch time and etc.. But banks may not have incentives to help SMEs even with lower cost of capital and less stringent oversight from bank regulators. So the heavy-lifting (where reigniting an economic recovery is concerned) will have to be done on the fiscal front. There now seems to be a policy consensus that fiscal policy ought to be more audacious. Against the global backdrop of low interest rates, China is in a good position to spend its way out of a temporary economic slump. But how to spend matters a great deal.

Chart: Lower oil prices will enable China to reflate its economy with gusto

China's economic recovery depends, first and foremost, upon a successful containment of the virus. But the coronavirus containment program has already exacted a huge social cost and will continue to do so. Hence policymakers must make the prevention of large layoffs their top priority through various forms of fiscal relief for beleaguered enterprises. Once COVID-19 fears subside, the goal of policy should be to release pent-up demand and delayed investment. All of this requires a large dose of fiscal stimulus. There are several versions of stimulus being talked about - some as large as RMB 24 trillion or $3.5 trillion, about 25% of China's total GDP (according to local press such as First Finance, a major financial newspaper).

The big question is: can the New "infrastructure" make traditional pump priming more efficient? Given that we seem to be living in a time of quasi perpetual low interest rates, a focused fiscal stimulus with vision and precision, could make the original growth target of 6% less compromised. Moreover, some of the evident pitfalls which have been exposed by COVID-19 (lack of public health facilities, for example) could be addressed and the economy could leapfrog into a better future. At the same time, fiscal budget constraints still hold even at low interest rates, and it is well worth remembering that the side effects of the RMB 4 trillion stimulus package in terms of debt buildup and potential non-performing assets still haunt the economy.

Chart: Bulk of pledged investment likely to face budget constraint in 2020

Moreover, while de-leveraging could be put off for a year or so, it cannot be put off forever. The planned opening-up of the financial services sector to foreign companies will make it increasingly difficult to strike a balance between macro stability and a rising debt/GDP ratio. In the very short run, a “flood irrigation” stimulus is highly unlikely as the investment figures quoted in certain provinces are disproportionally large in relation to their fiscal revenues. On March 12, NDRC categorically ruled out a "flood irrigation" type stimulus.

In short, China should and will make fiscal policy more expansionary but is unlikely to repeat the mistakes made in late 2008. The resulting package will include a combination of tax cuts and subsidies, some infrastructure projects, and most certainly projects relating to social welfare and health. There is one caveat however: a global slowdown that would apply the brakes on China’s H2 recovery trajectory through weak external demand. In that case, China’s 2020 GDP growth could fall below 5%.

Energy

Coronavirus infects global oil market

As the regional outbreak has become a global pandemic, industry forecasters scramble to revise their 2020 global oil demand forecasts. While coronavirus has sapped the world's demand for oil, on the supply side, OPEC+ failed to reach an agreement and Saudi Arabia fired the first shots in a price war, sending Brent crude prices tumbling over 20% to $36/b. Now is the time to re-evaluate how the coronavirus "black swan" will affect the outlook for the global oil market this year.

Global oil market is now facing an unprecedented double whammy—the coronavirus-sparked collapse of demand compounded by the spectre of unrestrained production—that will likely push crude prices to multi-decade lows. Against this backdrop, high-cost, small-scale, and highly leveraged oil companies across the globe could face potential bankruptcy. Low oil prices would entail profit losses for international oil companies, putting a brake on upstream investment and forcing them to scale back production. Likewise, Chinese oil majors would feel the financial stress and are more likely to lower their pledged targets for domestic upstream investment under the Seven-Year Action Plan. Meanwhile, slump in crude prices could have oil companies switch focus to their downstream business. The short-term slide in oil prices could offer a window of opportunity for domestic refineries to restock crude. High-end petrochemicals such as medical PVC and polypropylene are also expected to grow at least 30% in 2020. The outbreak could also prompt oil and gas companies to adopt more digital and contactless modes of operation.

Despite possible recovery in H2, overall oil demand to decline in 2020

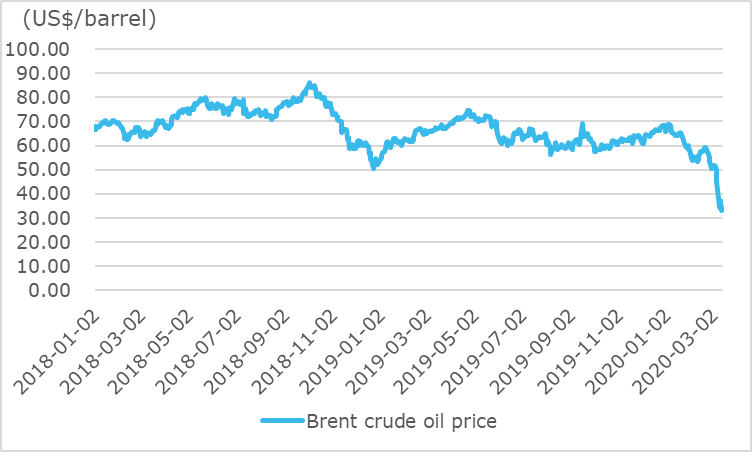

Oil prices were already low in the past year due to the unusually warm winter, large stockpiles, booming US shale production and tepid economic growth. Then, as the coronavirus brought China's once bustling cities almost to a standstill, demand fears gripped the oil market. Oil prices plummeted 23% by February 10 from their previous peak in early January, just before the virus began to spread. After briefly rallying thanks to the steady decline in new cases and resumption of business operations in China, oil prices again tumbled on the back of a surge in the number of coronavirus cases in Korea, Japan, Italy and Iran.

Chart: Brent crude halved on recession fears

On the demand side, while initial demand reductions could mostly be traced to China (the second largest oil consumer after the US fell by as much as 4 mb/d at the peak of lockdowns in the country), the spread of the virus to the rest of the world provided the second shock: further depressing an already lacklustre OECD demand. However, as the outbreak turns into a global spread, it's not just about a dent in China's colossal takings of 14 mb/d in crude imports anymore. What the market now fears is that even smaller-scale lockdowns in the US and Europe will cut deeply into oil consumption. Worse still, the world's top three importers of LNG—Japan, China and South Korea—are also the three hardest hit countries in the outbreak. IHS Markit predicts that global oil demand will suffer its steepest decline on record in Q1—worse even than during the 2008 global financial crisis—as schools and offices close, airlines cancel flights, and a growing number of people hunker down at home. Major energy watchdogs including the International Energy Agency (IEA) have reduced their demand growth forecasts by 25%-30%. Goldman Sachs now expects 2020 global oil demand to fall by 150,000 b/d.

We see two possible scenarios for oil demand this year. If the global spread of the virus can be contained by the end of Q2, a demand recovery could arise in the second half of the year, but the oil industry should brace itself for a reduction in overall demand in 2020 – a first since the financial crisis. If the pandemic cannot be brought under control by Q2 as it strikes the developing world where medical facilities are inadequate or spreads across the US, oil consumption will fall off a cliff. In this case, Brent crude prices will remain low for the whole year.

How long will the oil price war last?

On March 6, oil prices plunged more than 9% to $45/b as Russia and OPEC split over supply cuts aimed at addressing the drastic fall in demand caused by coronavirus. Saudi Arabia, in response, almost immediately launched a price war, by raising production and discounting its crude. As a result, Brent crude prices crashed by a fifth to as low as $36/b, marking its biggest one-day drop since the 1991 Gulf war. Russia then responded that it would boost production at the beginning of April. This raises the prospect of a huge supply glut, because some of the world's largest oil producers will open the taps just as global oil demand is falling.

The Brent crude price has already halved this year, a plunge that will have a wide range of implications, including lower earnings for oil companies. As a result, shares in the largest listed European oil and gas majors fell sharply, with BP and Shell both down more than 5% on March 6. Both have lost more than a fifth of their market capitalization since mid-January. Saudi Arabia, itself too, feels the immediate impact from the price crash. Shares of Saudi Aramco plummeted by more than 9% on March 8, falling below its December initial public offering price for the first time.

Nevertheless, there are no winners in oil market's price war, since the current ultra-low prices are unsustainable for all three top producers. Although Saudi Arabia enjoys the world's lowest oil production cost, its economy is highly dependent on oil exports, and it needs a hefty $84/b of oil price to balance this year's budget. Should Brent crude remain at $35/b, without an adjustment in spending, Saudi Arabia would run a deficit of nearly 15% of economic output in 2020, while its net foreign reserves could run down fast and its ambitious plan to diversify the economy would come to a halt. Russia, too, feels the squeeze as it would have to tap in its sovereign wealth fund to support tumbling ruble amid the oil price crash. Their target could be the US shale sector, which, for a decade has grown so rapidly that it has squeezed the market share of OPEC and other large producers. US fracker’s golden days may well be coming to an end as US investors have become increasingly wary of funding shale's expansion. This is because shale exploration has largely failed to turn a profit and has relied on access to financing in order to expand – something that may be close to drying up. The current crude price has already fallen below US shale's break-even point. Hence ExxonMobil recently decided to slow the production of its flagship shale project in the Permian Basin. If low prices persist, we may well see a slew of highly indebted shale companies going bankruptcy and a spontaneous reduction in production from American frackers.

Chart: Breakeven of US shale producers is lower than the level at which most exporters balance their budgets

Meanwhile, exports have already plummeted from Venezuela, Libya and Iran, mitigating the supply glut to some extent but not enough to turn this around. As Iran is fast becoming the Middle East's coronavirus epicenter, oil supply disruptions may also arise in Iran and other Gulf producers.

What does it mean for Chinese oil companies?

For Chinese oil majors, a low oil price implies revenue decline and share prices slide; This, combined with their pledged targets to revive domestic upstream investment under the Seven-Year Action Plan to reduce energy dependence on imports, is bound to put them under a certain amount of financial stress. In this regard, it would be reasonable for them to reduce exploration investment for the year.

Meanwhile, Chinese companies may switch focus to their downstream business. In addition to lower crude feedstock costs, refiners' profit margins would be further boosted by a domestic fuel pricing scheme in place since 2016 that puts a floor under retail fuel prices whenever the global crude price goes under $40/b. As fuel demand is recovering along with economic activity in China, refiners should seize this window of opportunity to step up crude purchases and crank up run rates. While state-run refineries maintain their production cuts (given that their tanks are near full due to depressed demand of jet fuel), China's private refiners, often called "teapots", would be the first to benefit from the sharp plunge in crude prices. Moreover, some subsectors in petrochemicals such as medical PVC and fiber polypropylene which is used to produce face masks, is likely to see a sharp upthrust in demand thanks to the coronavirus outbreak.

Furthermore, the outbreak has pushed large energy companies to adopt digital and contactless modes of operation, accelerating the transformation of oil and gas operations with the induction of big data, advanced analytics, and Internet of Things into their business practices.

Financial Services - Real Estate

Housing policy unlikely to shift amid price pressure

Since the outbreak of the COVID-19 epidemic, housing sales have fallen sharply. With work suspended and sales offices in more than 60 cities closed, the capital-intensive real estate (RE) sector is reeling. RE enterprises' capital flows are strained and, in some cases, have dried up completely. Whether the sales situation can be improved in the short term depends largely on the development of the epidemic and how soon the virus can be contained, both of which is uncertain at the moment. In the second half of the year, whether the market displays a V-shaped recovery or an L-shaped one depends largely on the strength of policy support.

Higher financial costs and construction delays likely

With home purchases being put on the back burner the industry faces depressed demand, a situation that may take months to reverse itself. In this case, RE enterprises are likely to face a liquidity crisis as a result of reduced inflows of capital, high finance costs and debt repayment pressure in the coming months. According to Moody's estimates, about RMB3.6 trillion in domestic bonds and US$27.6 billion in overseas bonds will mature or be sold back in the next 12 months starting February 1. RE enterprises’ demand for refinancing will remain high. At present, restrictions remain in place on migrant workers returning to work in the cities. Construction sites are also facing problems such as a lack of protective materials such as masks, and procedures for isolation and site shutdown in case of infection. As a result, project completion delays are bound to occur. Hence, RE enterprises will face higher financial costs.

On their hand, RE enterprises have been quick to respond, offering discounts and other incentives in order to spur sales and generate cash. Recently, Evergrande enterprises took the lead by offering a 25% discount on online sales. The debt risks faced by highly-leveraged small- and medium-sized enterprises may lead to an increase in corporate bankruptcies, which will lead to a reshuffle of the industry and a further increase in industry concentration.

RE regulation tenet will not change

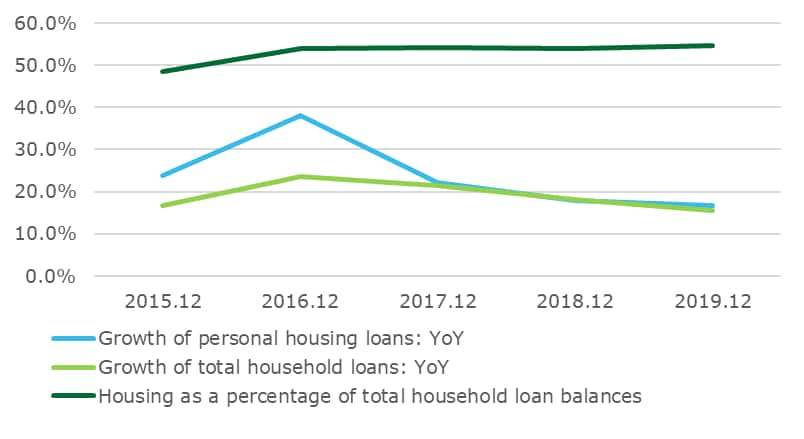

The policy of "A house is for living in and not for speculation" is a long-term policy, whose basic tenet, the prevention of a rapid rise in housing prices, will remain unchanged. In the past two years, the growth rate of personal housing loans continued to decline, falling below the growth rate of total household loans for the first time since 2018. This was mainly due to the slowdown of housing price increases as a result of this policy. By the end of 2019, personal housing loans had increased 16.7 percent year on year to RMB 30.2 trillion, accounting for 54.6 percent of the total household loans. The policy goal of preventing the household leverage ratio from rising too fast will remain unchanged while growth of personal housing loans will continue to show a slight decrease in 2020.

Chart: Growth of personal housing loans continues to decline

Recognizing the importance of RE industry

The Central Economic Work Conference reaffirmed that "the RE industry will not be used as a short-term means of stimulating the economy". However, the rapid decline in housing prices can trigger financial risks and economic shocks. Whichever way one looks at it, the Real Estate industry has been a strong contributor to the growth of China's economy and RE investment is an important part of fixed asset investment both for individuals and companies. In 2019, GDP of the RE industry and construction industry accounted for about 7%, and 14.2%, respectively. But there are two other areas in which the impact of the Real Estate Industry cannot be ignored - tax revenues for local governments and employment.

Tax revenue from the RE industry has always been an important source of income for local governments. In addition, the RE industry has a long industrial chain and a large number of associated upstream and downstream enterprises, which provide the lion's share of jobs in the economy – especially to less educated, less skilled workers. In 2018, the construction industry employed nearly 54,000 migrant workers, contributing heavily to the stability of labor employment in the face of structural adjustments in other sectors of the economy. Thereforeits impact on the economy cannot be ignored.

In short, the RE industry will face more risks in 2020. In Hubei Province which has been highly affected by the epidemic and most tier-3 and tier-4 cities all over China, due to the declined demand, a new rising cycle will start as a housing price bubble develops and the related housing stock builds up. Additionally, possible bankruptcies of debt-ridden property enterprises will put further pressure on local governments. In such a period of emergency, we suggest that priority be given to "city-specific policies", i.e. policies formulated on the basis of the actual situation of specific locales. Some possible easing measure would be to relax the pre-sale requirements and purchase restrictions and provide tax relief and credit reliefs. These would go a long way in maintaining stability in the RE industry.

Technology

2020 - still a promising year

Cracks are beginning to emerge in the tech supply chain as the fallout of COVID-19 is being felt across the globe. Apple issued a warning to investors that it would not hit its Q2 2020 revenue expectations due to iPhone supply constraints and reduced retail demand in China. In South Korea, Samsung had to shut down operations at a production plant in Gumi City even though it resumed operations shortly afterward. Multinationals with exposure to the Chinese market are now weighing the potential impact on their supply chains. However, as workers return to work and production gradually ramps up, these issues will be sorted out in time. However, the long term effects of the corona virus will begin to show itself in the course of 2020, and it will probably be seen as the year that intelligent technology became ever more entrenched in business operation and everyday life.

Professional service robots set for double-digit growth

In contrast to industrial robots, professional service robots are mainly used outside of manufacturing, and they usually assist humans rather than replace them. Most are designed with wheels to make them mobile or semi-mobile; although some professional service robots have arms, they are a minority, and the arms are not capable of (nor intended for) the kinds of heavy-lifting tasks that most industrial robots tackle. Thus far, professional service robots have been most popular in the retail, hospitality, health care, and logistics (in warehouse or fulfillment settings) industries while some are also deployed in such fields as space and defense, agriculture, and demolition sectors.

Of the almost 1 million robots we expect to be sold for enterprise use in 2020, we predict, over half will be professional service robots, generating more than US$16 billion in revenue, 30 percent more than in 2019. Additionally, enterprise spending on professional service robots is growing much faster than that for industrial robots. If recent trends are any indication, professional service robots may surpass industrial robots in terms of units in 2020 and revenue in 2021.

This is not to say that the industrial robot market is stagnating. We expect revenues from industrial robot sales in 2020 to reach nearly US$18 billion, a 9 percent increase over 2019. But, while industrial robots will remain important in the years to come, the professional service robot market is poised to take off with a vengeance, fueled by new developments in 5G telecom services and artificial intelligence (AI) chips.

Edge AI chips come into their own

We predict that in 2020, more than 750 million edge AI chips — chips or parts of chips that perform or accelerate machine learning tasks on a digital device rather than in a remote data center — will be sold. Furthermore, the edge AI chip market will continue to grow much more quickly than the overall chip market. By 2024, we expect sales of edge AI chips to exceed 1.5 billion in quantity. This represents an annual unit sales growth of at least 20 percent, more than double the longer-term forecast of 9 percent CAGR for the overall semiconductor industry.

These edge AI chips will probably find their way into an increasing number of consumer devices, such as high-end smartphones, tablets, smart speakers, and wearables. They will also be used in multiple enterprise markets: robots, cameras, sensors, and other IoT (internet of things) devices in general.

The spread of edge AI chips will significantly change ways of living and doing business for consumers and enterprises respectively. For consumers, edge AI chips can make possible a plethora of features—from unlocking the phone using biometrics such as facial recognition to having a conversation with its voice assistant. Or taking quality photos under extremely difficult conditions —a thing that previously was only possible with an internet connection, if at all. But in the long term, the greater impact on society may come from the use of edge AI chips by enterprises, where they can enable companies to take their IoT applications to a whole new level. Smart machines powered by AI chips could help expand existing markets, threaten incumbents, and change the ways profits are shared within various industries.

Private 5G networks: Enterprise untethered

To enable ultra-reliable, high-speed, low-latency, power-efficient, high-density wireless connectivity, a company really only has two options. Either it can connect to a public 5G network. Or it can opt for a private 5G network, either by purchasing its own infrastructure while contracting for operational support from a mobile operator or by building and maintaining its own 5G network using its own spectrum. For many of the world’s largest businesses, private 5G will probably become the preferred choice, especially for industrial environments such as manufacturing plants, logistics centers, and ports.

We expect that more than 100 companies worldwide will have begun testing private 5G deployments by the end of 2020, collectively investing a few hundred million dollars in labor and equipment. In subsequent years, expenditure on private 5G installations, which may be single-site or spread across multiple locations, will climb sharply. By 2024, the revenue from cellular mobile equipment and services for use in private networks will probably add up to tens of billions of dollars annually.

There are several factors favoring the use of private 5G networks. Unlike a public network, a private 5G network can be configured to the specific needs of a location as configurations can vary by site, depending on the type of work undertaken in each venue. A private network also allows companies to determine the network’s deployment timetable and coverage quality. Furthermore, the network may be installed and maintained by onsite personnel, enabling faster responses to issues. Security can be higher, affording network owners a degree of control that may not be possible on a public network. Keeping data onsite can reduce latency as well. The private network may even run on a dedicated spectrum, reducing the risk of variable service levels due to usage by third parties.

High speed broadband from low orbit

In 2020, corporate efforts to bring internet access to the world will take off — literally. We predict that by the end of 2020, there will be more than 700 satellites in low-earth orbit (LEO) seeking to offer global broadband internet, up from roughly 200 at the end of 2019. Though these won’t be enough to connect all the consumers and enterprises around the globe, they may offer partial service in late 2020 or early 2021, possibly starting with countries in the higher latitudes.

A number of companies from the United States, Canada, China, Russia, and Europe are trying to establish themselves in the satellite broadband market. Various commercial and government organizations are currently looking at ways to amend rules governing how conjunctions are handled as well as how satellites are de-orbited safely at the end of their life. They are also exploring the use of machine learning algorithms and trying to improve tracking technologies such as ground-based radar. International collaboration around this issue is on the rise and companies themselves are seeking to get to the forefront of it.

Operating in space and starting a new business at the same time is extremely difficult, with little room for error. And many of the companies going into the satellite broadband business are attempting to do both. As a result, they face a vast number of technical and operational challenges that could delay or derail their plans, including, but not limited to, ground station construction and operation, potential radio frequency interference with other satellites, user terminal pricing and availability, battles over spectrum rights, and even concerns about the visual pollution from bright satellites disrupting ground-based astronomy.

The smartphone multiplier: toward a trillion-dollar economy

Smartphone sales, to state the obvious, are big business. But even that market may soon begin to pale next to the sums commanded by the sales of products and services that depend on smartphone ownership—the so-called “smartphone multiplier.” From selfie sticks and ringtones to mobile ads and apps, smartphone multiplier revenues may eclipse the revenue generated by smartphones themselves in just a few short years.

We predict that the smartphone multiplier will generate US$459 billion of revenue worldwide in 2020 alone. With smartphone sales in 2020 expected to reach US$484 billion, the entire smartphone ecosystem - smartphones plus smartphone multipliers - will be worth over US$900 billion.

The smartphone multiplier includes a wide array of products and services, most of which fall into one of three categories: Hardware (including audio accessories), Content (including mobile advertising and games), and Services (including repairs and insurance). Mobile advertising, the smartphone multiplier’s top money-maker, has thrived despite the smartphone’s relatively small screen.

Globally, approximately 3.6 billion smartphones are in use today. This huge user base is the cornerstone of the smartphone multiplier effect and it is still growing. Every successful device cultivates — and in turn relies upon — an associated ecosystem. The better the device, the more vibrant the ecosystem.

Automotive

Coronavirus epidemic signals wake-up call to prepare for future disruption

After a nationwide lockdown that has lasted a month, the coronavirus epidemic has started to show signs of abating in China. A majority of sectors have resumed production. According to CAAM, more than 75% of automakers and suppliers have resumed production although they are not yet at full capacity. Dealerships and showrooms, on the other hand, are struggling to go back to normal operations – less than half of them have managed to reopen.

As market observers, we need to identify and distinguish between the short-term difficulties that have been amplified by the epidemic and long-term challenges that will continue to plague the industry. China’s auto industry has been hard hit with cyclical and structural problems in the last two years. For instance, increased regulation and competition have pushed a lot of low-end auto manufacturers out of business as vehicle sales declined for two straight years. As the nation shows signs of aging and the youth population shrinks, second- or third-time buyers have become the main drivers of automobile sales.

That said, we are confident that the auto industry remains resilient enough to bounce back when the epidemic is successfully reined in and business returns to normal levels.

Before we address the issue of long term challenges to the automobile sector, we’d like to focus our attention on some of the hidden vulnerabilities within the industry that have been exposed by the epidemic.

Digital gap in auto sales channels

In stark contrast to other retail sectors which have been able to re-boot operations during the epidemic via various digital tools, automakers and dealers that had not fully established a systemic and well-organized online sales strategy were caught unprepared. They scrambled to put in place novel digital approaches, but because they were in a hurry problems were quick to emerge. As a result, we had seen advertisements ill-tailored to customer’s interests and habits, ineffective sales campaigns and growing compliance risks, resulting in wasted efforts and tarnished brand images.

Behind this lies the fact that the auto industry has been slow to transition to an omni-channel sales model that allows customers to seamlessly switch between online and offline models and to get a fully integrated experience. The epidemic undoubtedly will accelerate this transition. But both dealers and OEMs have to realise that in order to remain competitive in the long run, it is in their long-term interest to invest in digital technologies. That said, with the coronavirus epidemic put strains on cash flow and worsen business situation, dealers need to make tradeoff decisions, first by identifying problems and weaknesses in their existing practices, measuring the ROI on their digital investment, and taking potential risks more fully into account.

Escalating supply chain risks

A growing number of global OEMs have announced that they have had to shut down some of their factories outside China due to shortages of necessary parts from China, especially those coming from heavily-affected provinces. From Hyundai to Nissan to Toyota, South Korean and Japanese automakers have been hardest hit by the supply chain disruption.

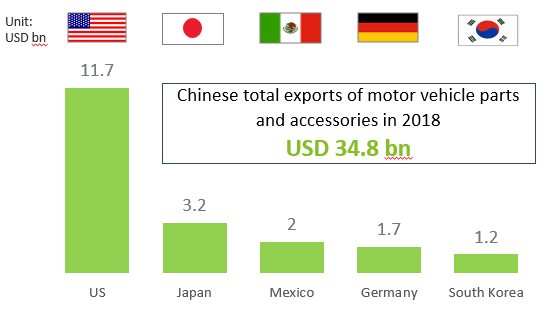

Chart: Top 5 export market for Chinese auto parts in 2018

There are several reasons behind this. First, the strategy of “putting all eggs in China’s basket” has backfired. The Wuhan epidemic has highlighted the fragility of a globalized supply chain and all the attendant risks attached to it. Automakers were one of the main beneficiaries of global trade. Over the last decade, they sourced parts and materials worldwide and thus obtained the best products at the lowest prices. China, with its skilled and relatively cheap labour forces, has risen ever since, and the global auto industry is increasingly dependent on Chinese factories for key parts. In the case of South Korea, about 87% of the wiring harness-the assembly of which is quite labour intensive-that Korea imports are from China. The single-sourcing practice also made it difficult to shift to alternative suppliers as it takes time to complete

Second, an overly spread-out sourcing system with many sole producers in lower-tier levels. It takes 30,000 parts to assemble a single vehicle. OEMs outsource most of the manufacturing of these parts to tier-1 suppliers which in turn outsource to smaller firms. OEMs normally have little or no knowledge of what goes on at the majority of lower-tier suppliers. And those are the levels at which you have the sole producers of a certain part or component.

Third, the disruption in supply chains was further exacerbated by the fact that most manufacturers were functioning under the Just-in-Time production system. JIT’s underlying goal is to reduce waste and increase efficiency. But in times of disruption of supply chains, lean inventories result in the suspension or delay of production. Compared with European and the US counterparties who keep a relatively high safety stock given the long shipping time, Japanese and Korean automakers tend to keep a relatively small inventory considering their geographic proximity to China, thus they had to really scramble to resume production during the epidemic.

Since the Japan earthquake in 2011, many global automakers have worked to increase supply chain resilience. They have regionalized the supply chain network, and put production in proximity to end-consumers. Some of them have changed their sourcing practices to double or multiple sources, or increased the usage of common parts that can be mass-produced in the rest of their manufacturing locations. In addition, a few of the auto OEMs have managed to map out the entire supply chain, tracking all the subsidiary suppliers, their locations and stock levels.

But there is a strong argument against moves such as multi-sourcing, raising inventory and creating back-up production capacity and that is the increased cost. Thus, it is important for companies to weigh the trade-offs between supply chain resilience and overall competitiveness.

In the ultimate analysis, while we cannot prevent the occurrence of events of disruption, what we can do is to be better prepared when they do happen, and to bounce back much faster than our competitors.

Retail

The move to online business boosts retail digitization

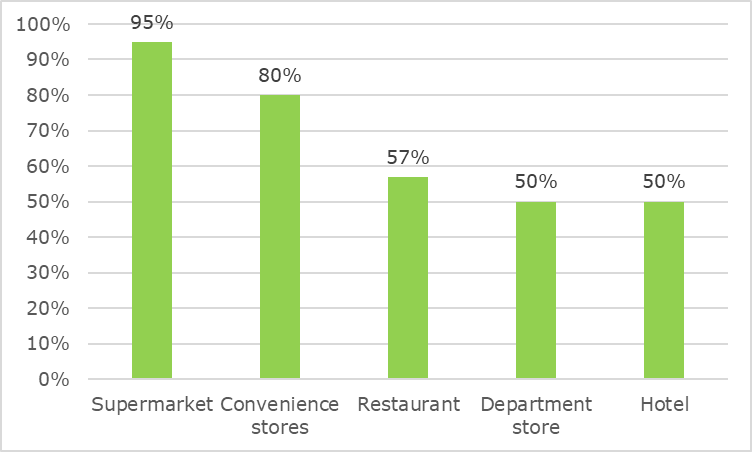

As the epidemic is gradually coming under control, retail businesses have resumed operations. However, the reopening of physical stores has generally been slower than online retail business such as e-commerce. According to the Ministry of Commerce, the average opening rate of chain stores and convenience stores across the country is about 95 percent and 80 percent now. Conversely, the opening rate of department stores and shopping centers is still relatively low at around 50%. Even when stores are open, business hours have been greatly shortened. At present, foot traffic at department stores has only reached 10 to 15 percent of normal business as most of the customers are concentrating on supermarkets, pharmacies and daily necessities stores. It is expected that normal restaurant and brick-and-mortar operations will not be fully resumed until quarantine of retail businesses and communities in all regions is completely lifted.

Figure: Consumer industry resumption status (Updated as of February 26, 2020)

As the retail industry as a whole is struggling to return to normalcy, "returning to work via cloud" has become the option of choice for many retailers. Large-scale chain restaurants operate through O2O while food, cosmetics and infant product brands carried out community group buying based on WeChat and e-commerce via livestreaming. With the substantial increase in `contactless’ demand, "cloud consumption" which relies on retail technology may become the new normal of the consumer goods industry.

The consumption scenario of integrated online and offline operations will become a new incremental driver for traditional retailers.

Backed by a solid supply chain, traditional supermarkets are able to meet consumers’ demands for fresh food and daily necessities through online orders — which have greatly increased over the coronavirus crisis. The current epidemic has made traditional supermarkets witness the potential of online consumption in all categories, and made them realize the business value of O2O. This has probably given them the confidence and motivation to build a standardized and all-encompassing online service platform to accelerate the digital transformation of their physical stores.

Restaurants too will increasingly resort to delivery apps based on WeChat, local life or e-commerce through self-run and third-party delivery, providing more standardized and AI-based community home business. Data shows the repeat rate of 20 large-scale catering enterprises that the Ministry of Commerce closely monitors has reached 57%, and O2O delivery mode has become the mainstay of the catering industry.

The consumer goods industry has accelerated the establishment of online sales channels and flexible supply chains.

With the closure of shopping centers and department stores as a result of the epidemic, sales of many fast-moving consumer goods such as clothing, shoes and cosmetics were adversely affected. During the epidemic, many cosmetics, home cleaning, clothing and shoe brands engaged their customers either through live-streaming e-commerce, and/or through community-based flash sales. What began as a reaction to a crisis seems to have become a blueprint for the future, and online operation has become the entry point of customer traffic for the consumer goods industry. Through a combination of e-commerce, social media and self-run website operation, retail companies have finally understood that they can effectively engage their consumers through the Internet.

During the epidemic, consumer goods such as food and beverages, clothing, shoes and daily necessities faced the risk of disruption of their supply chains, a breakdown in the production and supply of raw materials and the postponement of product research and development. Forced to work from their homes, these companies turned to aggressive digitization at all levels of the supply and delivery chain. This has made for flexible supply chains which will in turn help enterprises to achieve the supply chain front and greater organizational efficiency. Through big data, the entire supply chain of raw materials, production, packaging, warehousing, logistics, and sales will be coordinated and supervised to keep production cycles and inventories at the most efficient level. In the future, digitized, flexible supply chains will be adopted by more enterprises as an industry standard.