Perspectives

The Deloitte Research Monthly Outlook and Perspectives

Issue 85

Published date: 25 September 2023

Economy

Tentative signs of stabilizing growth

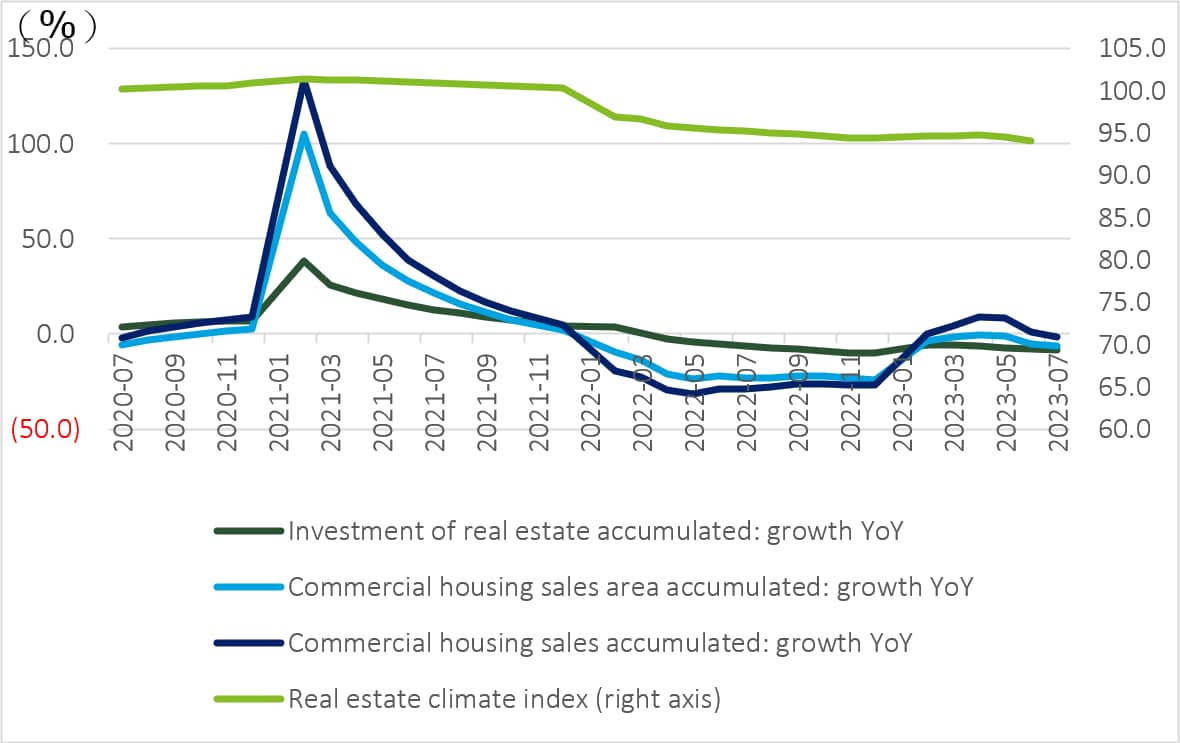

The property sector continues to dominate headlines in China for valid reasons given that its impact is felt right across the economy. Considering its sheer size in terms of total investment (nearly 25%) and economic activities (about 1/3); and the property cycle being less shallow, the mighty property sector is expected to be a drag on overall economic growth in the coming few years. As expected, August housing data has shown declines across the board, with investment falling by 8.8% between January and August 2023 compared to the same period last year. In the short run, sagging share prices of major developers have sparked concern among investors around further financial distress, which is weighing on the corporate sector and local government finances. China is unlikely to face a Lehman moment or systematic risk triggered by corporate failures, which has been our long-held view, but the distressed level of property companies’ stock prices has severely constrained even the most viable investments. Has policy-induced consolidation in the property sector gone too far? Most other countries have only recently recovered from such a shift.

Both the central and local governments have unveiled a slew of measures aimed at boosting housing demand. Many restrictive policies designed to deter speculation have been eased over the past few months. Notably, cities such as Beijing and Shanghai have allowed families who have previously used a commercial loan to purchase property but do not own a house in these cities to qualify as first-time home buyers, meaning that for them, the high initial down payment will be substantially reduced. Taking Beijing as an example, the down payment ratio will be reduced to 35-40%, down from 60-80% previously. This suggests that consumers still view homes as the principal form of wealth. On August 21, the People’s Bank of China (PBOC) eased interest rates by 10 basis points, which was more of a signal that policymakers will nudge banks to tilt their lending towards the housing sector. In more recent developments, lawmakers have signaled that controversial property taxes won’t be on the cards for the foreseeable future. In the past, rumors about pilot programs levying property taxes often served as moral suasion for dampening housing demand. Taking all these measures together, the objective for policymakers is to convince consumers to take on more leverage while local governments tighten their belts. Meanwhile, investors continue to long for a large fiscal stimulus, but policymakers’ continued emphasis on high quality growth seems to be an implicit rejection of such expectations.

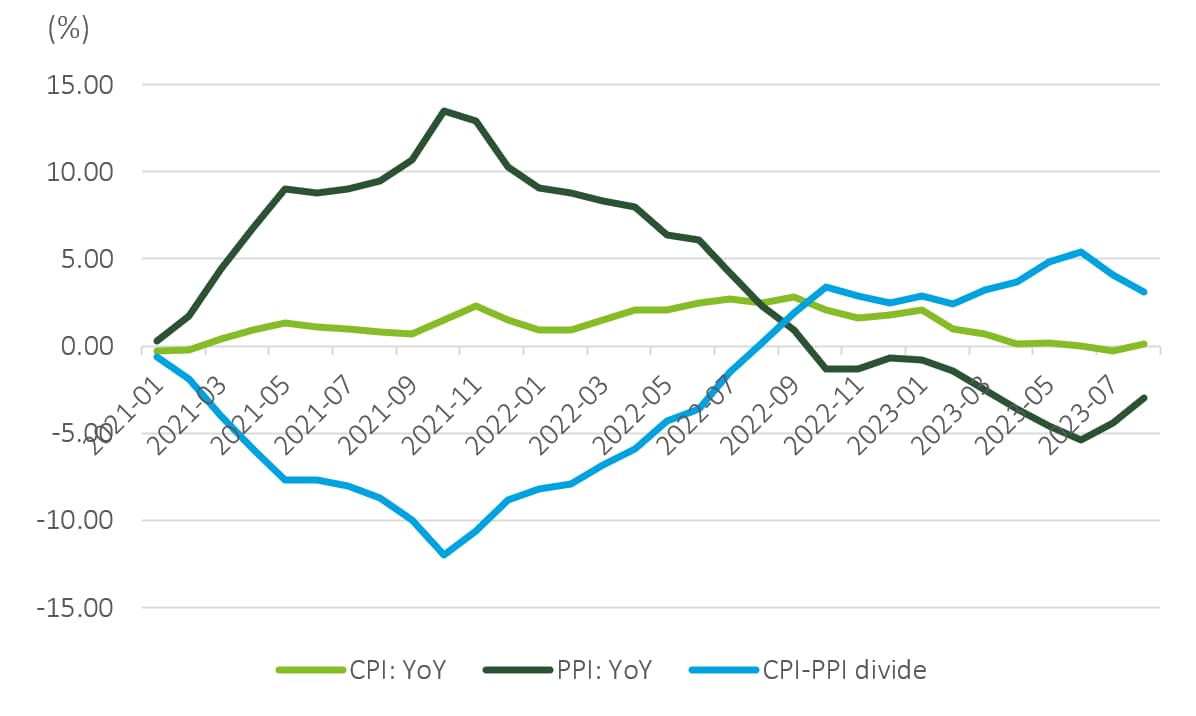

On the data front, August has shown some signs stabilizing growth. A rebound in the CPI figures in August (0.1% YoY) and a narrowing of the CPI-PPI divide have suggested that the notion that China could have fallen into a deflationary spiral without a big dose of fiscal stimulus is premature. The automotive market, a bellwether industry in China, is holding up steadily, with retail sales of passenger cars increasing by 2.6% YoY in August, while the domestic tourism sector is booming. The critical difference between China today and Japan yesterday is the fact that the former is still in the catch-up phase, while the latter was a fully developed economy by the 1990s. We are of the view that if consumption could continue to outpace GDP in terms of growth rate, consumers will have contributed more than 2% to growth. So, the medium-term growth rate on a five-to-seven-year horizon is likely to be around 4%. Of course, reforms in the labor market, such as easing restrictions on the resident registration (hukou) system and a better social safety net, are critically important to sustaining long-run growth.

Chart: China is unlikely to fall into a deflationary spiral

Source: Wind

Returning to policy responses, if demand for improved housing remains relatively unscathed while pent-up demand is weighed down by lackluster sentiment, fiscal relief should be more targeted towards the less wealthy. This is indeed the argument for “consumption coupons” which were widely used in many economies during the pandemic. Looking ahead, 2024 might be an easier year for the economy as global interest rates are expected to peak and the elevated dollar could come off in the changed interest rate cycle. Finally, regarding China’s 2023 growth target, “around 5%” remains an achievable goal despite a plethora of headwinds.

Financial Services

Paying more attention to risks with countercyclical regulation increasing

Since August, certain developments in the real economy have shown contra-cyclical characteristics and hence have caused concern in the market: for example, private real estate (RE) company Country Garden defaulted on 2 US dollar bonds, and a Trust defaulted on its wealth management products (WMPs); both total social financing (TSF) and RMB credit loans in July sharply missed the market's expectations; both the Consumer Price Index and the Producer Price Index showed negative growth in July.

In mid-August, PBOC (Peoples Bank of China) started a second round of interest rate cuts after June, further increased its efforts to stimulate the offtake of easy credit, and released the Q2 Monetary Policy Report, emphasizing a "stable to loose" monetary policy environment. A countercyclical policy requires monetary, fiscal, and other measures to work together in order to stimulate demand in the economy. However, the current pressure on bank profits, the rising local government and real estate debt risk, and the stability of investor confidence needs be faced rationally and given the importance that is due. The key is always to“balance stable growth and reduce risk”.

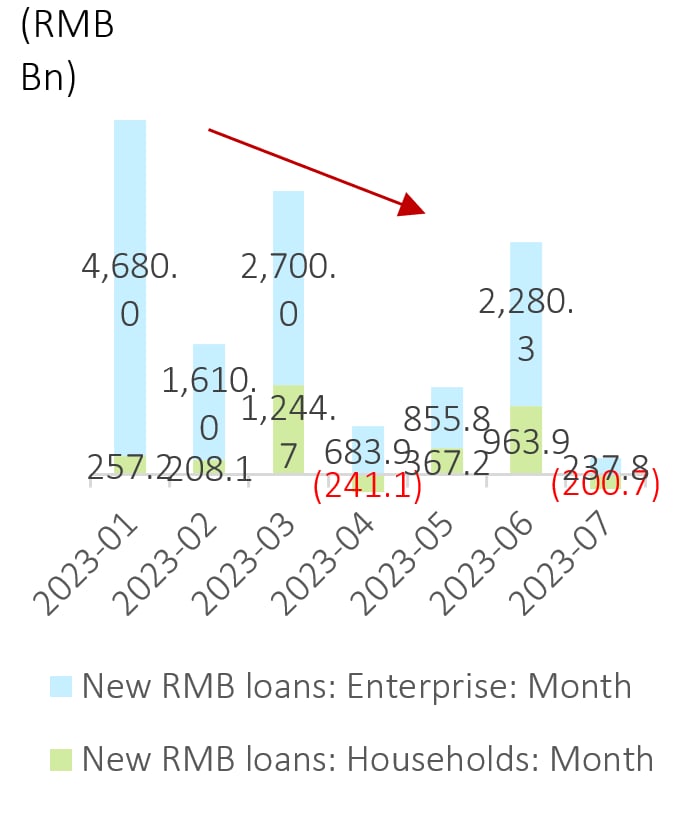

Enterprises and households are showing a reduced willingness to increase leverages, making demand slow to recover

Since pandemic control measures were removed at the end of 2022, demand has been slow to recover. In April, household sector loans dropped sharply by RMB 241.1 billion, partly due to early repayment of loans, but mainly due to the low expectation of income growth, and a strong propensity to save. In the PBOC questionnaire survey of urban depositors, nearly 60% of depositors chose “to increase savings”; in July new RMB loans amounted to RMB 345.9 billion. This was sharply lower than market expectations (RMB 780 billion).

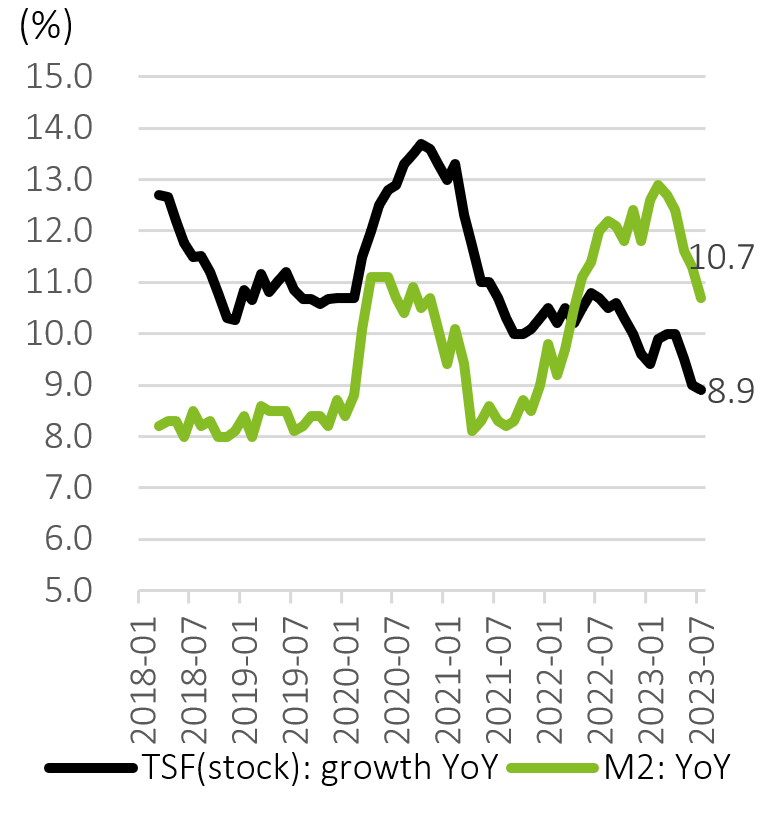

In July, the TSF stock growth rate slipped to 8.9%, the lowest point since these statistics began to be collected. This was mainly due to lagging local bond issuance and weak loan growth; M2 growth has been declining month by month since February this year. The decline is however slowing as the result of a declining trend in the degree of monetary easing.

Chart: Financing continued to be weak

Chart: TSF stock growth at a record low

Source: PBOC

Hitting the pain points, credit easing to stimulate demand

On August 15, PBOC started the second round of interest rate cuts by lowering the 7-day Reverse Repo, Medium-term Lending Facility (MLF) and Standing Lending Facility (SLF) by 10bp, 15bp and 10bp, respectively. Compared with monetary easing, interest rate cuts are a clear signal of credit easing, designed to stimulate the demand for bank loans from terminal enterprises and residents by lowering the cost of financing.

The falling money market interest rates will also have a positive effect on capital market liquidity. As of the close of trading on August 18, the yield of the 10-year Treasury Bond fell to around 2.56% . This will further stimulate corporate bond financing.

However, the loan prime rate (LPR) dropped asymmetrically in August: the 1-year LPR was lowered by 10bp, indicating that the current policy intention is more inclined to stimulate short-term consumer demand, while the 5-year LPR remained unchanged mainly due to the current pressure on the RMB exchange rate and Chinese banks’ interest rate spreads.

More attention to risks and disturbing factors

The negative effects of a contracyclical stimulus are the risk of capital idling and arbitrage, a further accumulation of debt in high-risk areas, and pressure on the profit levels of the banking sector. Therefore, here are some concerns for risks during the stimulus.

The first area of concern is the RE sector which remains weak. It is estimated that the default issue of Country Garden’s bonds may trigger a restructuring of the sector; the failure to pay the WMPs by the Trust is another indicator that there is growing risk of a chain reaction in RE debt default because the trust industry has been an important source of finance for RE developers.

The second area of concern is the level local government debt. Land transfer revenue used to be an important source of local government revenues. As the boom years of RE enterprises have ended, urban investment and RE projects, which used to represent high-interest assets, are now unable to bring local governments their earlier high returns. Accordingly, the credit structure and profitability models of banks have changed.

Chart: the RE sector is still weak

Source: National Bureau of China

However, we also see some positive signals: in the first half of the year, the growth rate of RE development loans increased by 5.3% YoY. This has improved financial data ahead of economic data, due to the government’s proactive policy. The PBOC has also set the tone by urging the financial sector to “adapt to the new situation created by major changes in the supply and demand relationship of the RE market”. The impact of a series of other measures including the “16 Financial Measures” and reduction of interest rates on stock mortgage remains to be further observed.

In short, when interest rates are falling, the banking sector can do a better job of risk buffering by helping enterprises to cope with the pressure on their profits and thereby lowering the risk of a rise in non-performing loans. Currently, the asset profitability of the Chinese banking sector is decreasing, and profit growth mainly relies on expanding the scale of assets (lending) to “compensate the price by volume”. Considering that the financial and economic cycles are often not completely synchronized, it will take some time for banks to fully assess their credit risk exposure. They should, accordingly, make comprehensive use of internal profit growth and external capital supplements (i.e. issuing stocks or bonds) to consolidate capital and prepare sufficient financial resources to hedge risks and maintain stable operation.

Technology

Getting ready for Generative AI

China’s internet watchdog and several other authorities, including the National Development and Reform Commission and the Ministry of Science and Technology, have jointly issued interim regulations for the management of generative Artificial Intelligence (GAI) services. These came into effect on August 15, 2023. As per these regulations, China is expected to encourage innovative applications of GAI technology in various industries and will support organizations, enterprises, and research institutes to enter into collaborations for this purpose.

Generative AI is a subset of Artificial Intelligence, which refers to techniques for generating content such as text, images, sound, video, code and the like, based on algorithms, models, and rules. Numerous forms of generative AI have emerged in the last decade. However, large-scale language modelling (LLM) has led to a major breakthrough in generative AI. The technology stack behind generative AI consists of three layers: the infrastructure layer, the model (platform) layer, and the application layer. The Infrastructure layer is the most mature, stable, and commercialized layer, providing computing, networking, and storage. The Foundation Model (i.e., the Generative AI platform) is what really distinguishes Generative AI from existing AI models. At the core of the Foundation Model are Machine Learning (ML) models pre-trained to solve problems on a wide range of datasets and connecting application developers with optimized hardware to accelerate the adoption of generative AI.

Graph: Generative AI Technology Stack

The most mature base models are currently in the text domain, driven primarily by the large amount of available training data. Beyond text, generative AI can go further to create code, images, video, audio and 3D models in a variety of modes, driving incremental productivity gains in the industry. For example, in the advertising industry, generative AI can create original copy, product descriptions and images in seconds. It can also generate synthetic X-ray images in the healthcare industry to help train doctors in diagnosis. Generative AI can change the way businesses operate and interact with customers and may even redefine what we know as an “employee”. This shift is already taking place in a number of consumer and business sectors.

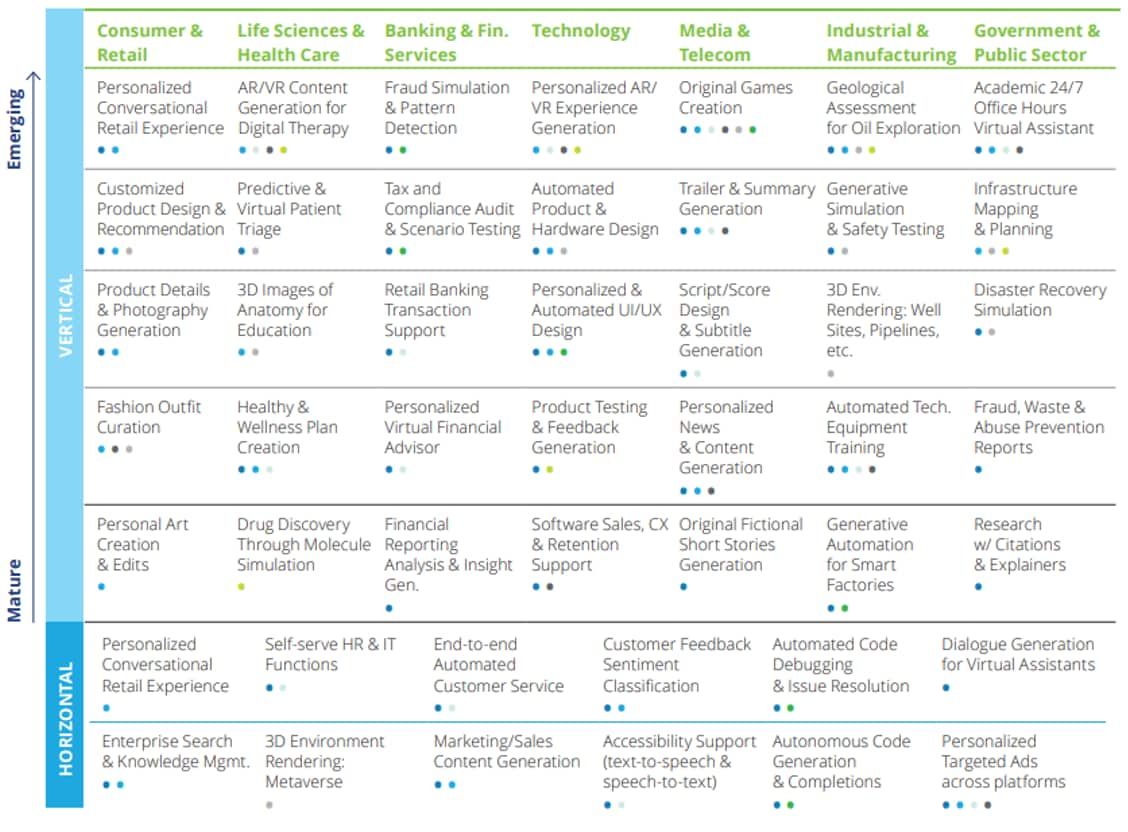

In the consumer space, the most common AI applications fall into four broad categories, covering tasks such as optimizing planning, research, and product discovery; delivering personalized instruction or learning content; generating or augmenting content and replicating the creative process; and building games, avatar characters, and other entertainment. The most popular application scenarios will be generic or applicable across industries (“horizontal”).

Unlike consumers, businesses need more advanced functionality, customization capability, guaranteed security and technical support, and verifiable ROI. The most popular application scenarios will be generic or applicable across industries (“horizontal scenarios”), however, enterprise scenarios in specific industries (“vertical scenarios”) will typically emerge where more sustainable value creation opportunities typically arise. Vertical scenarios target industry-specific workflows that require domain knowledge, context, and expertise. For this reason, the underlying models may need to be fine-tuned and may even require new specialized models. Generative AI, for example, can be used to create customized portfolios of securities based on risk-reward descriptions, or to recommend personalized treatment plans based on a patient’s medical history and symptoms. However, delivering high-performance vertical use cases requires a nuanced understanding of the domain. In software development, for example, generative AI can design composable blocks of code based on simple hints, which requires implicit knowledge of efficient coding, coding languages, and an understanding of technical terminology.

Table: Vertical and Horizontal Use Cases

As application scenarios for generative AI continue to emerge, we believe the market will evolve in the following five ways:

- Data-rich industries will get quicker adoption: All industries can benefit from generative AI. However, data-rich industries (e.g., banking, retail, hospitality) or those whose products utilize data (e.g., information services) may, and should, adopt the technology more quickly. Conversely, judgment-based industries (e.g., law, medicine) are likely to adopt AI more cautiously.

- Vertical application scenarios have higher value: While horizontal application scenarios will likely provide value first, vertical-specific application scenarios will, most likely, have higher value due to their reliance on proprietary data. As a result, data will create new economic systems to utilize and access proprietary and synthetic data.

- Investment will flow into application scenarios that have a clear ROI: As enterprise costs climb, this will drive organizations to invest in business scenarios with a clear ROI. As a result, scenarios that directly impact cost (e.g., chatbots), productivity (e.g., search), or revenue (e.g., marketing copywriting) are more likely to be adopted than those that eliminate labor.

- The pace, scope, oversight and regulatory compliance may vary: The pace, scope, oversight and regulatory compliance may vary as regulatory actions will differ in different markets. As a result, organizations need to take proactive steps to ensure data quality, transparency, fairness, and security, which will be the key factors in building Trustworthy AI.

- Generative AI will be a “critical companion”: There are numerous ethical issues with current generative AI, including the possibility that it could lead to job losses in the labor force. However, as with previous AIs, it is likely that this technology will be primarily an aid to human performance rather than a replacement of human beings. In fact, AI could become a common tool in the worker’s toolbox, just as coders use GitHub or marketers use the Creative Cloud.

The generative AI market is expected to continue to grow over the next few years, but there are many challenges to overcome before generative AI can be deployed at scale, and we recommend that leaders avoid blindly following the trend but think holistically about the opportunities, from the underlying technology to the impact on all parties involved:

- Create a generative AI strategy: Decide whether it can be adapted to, and can augment, existing processes and corporate strategies, and then integrate these with the organization’s existing AI strategy. Past AI principles also apply to the use of generative AI (e.g. AI governance; process transformation, etc.). In the context of rapidly-evolving technologies, is there a need to seek support and knowledge from partners and third parties operating in this area? This will have to be decided on a case-by-case basis.

- Assemble cross-function teams to co-create application scenarios: Identify areas of the value chain in which generative AI can solve problems, digitize progressively from basic productivity use to higher-level opportunities such as new and differentiated services or business models. When business leaders, technology leaders, and external experts collaborate, valuable applications can be identified, and the deployment of generative AI can be designed to mitigate business and cyber risks and comply with laws and regulations.

- There is a need to conduct in-house training to understand the organization’s current capabilities: This requires benchmarking knowledge gained through training, to educate employees on the capabilities, uses and risks involved in the use of AI. Additionally, companies need to continuously monitor technology advancements and the impact these can have on emerging business risks and opportunities, even as they ascertain whether their current AI talent pool is equipped to utilize GAI. This will enable them to assess how GAI adoption will impact their future search for, and acquisition of talent.

- There will be a need to monitor legal regulation and compliance: This will require constantly assessing how current or anticipated laws and regulations will affect the use of generative AI and whether the organization’s governance capabilities and processes will be able to adapt existing processes and hire, or retrain, personnel to fulfill these requirements.

- Need to fully understand the risks for, and impacts upon, stakeholders: Training data are inherently biased, and complex models are often costly to use. Therefore, it will be necessary to guard against premature and excessive expectation. “AI hallucination” will also need to be studied closely and guarded against. Care will also need to be taken to protect the organization’s confidential data, and guard against cyber malware.

Government & Public Services

Improve the utilization of computing resources

The rapid development of the artificial intelligence industry has increased the demand for computing infrastructure. It has been a year and a half since the “National Computing Network to Synergize East and West”project was launched. Due to the latency of data transmission caused by distance, data centers in the western part of China cannot easily respond to changes in the demand for computing power in the eastern coastal provinces. A number of eastern cities have therefore built large “smart- computing” centers locally to make up for the lack of computing power supply. The pertinent national agencies therefore need to strengthen the scheduling capacity of the national computing power network to avoid an unnecessary duplication of computing power buildup.

The development of generative AI such as ChatGPT has unleashed the need for computing infrastructure. Generative AI has been applied to more scenarios such as smart city, smart manufacturing, auto drive and digital twin modelling systems. When applying generative AI technologies, the mechanism and physical models use massive amounts of data. Building multi-tasking, multi-modal capabilities require the foundational support of a strong computing infrastructure. Computing infrastructure has therefore become an important part of the digital industry and a key link in enabling the digital transformation of industry.

Progress in the construction of national computing hubs located in western China is lagging behind their development in the east.

It has been a year and a half since the “National Computing Network to Synergize East and West Project” was launched, but construction is still behind schedule. Although building data centers in the west can reduce the cost of electricity, the cost of creating long-distance data networks between the east and the west is huge. That apart, the latency caused by long-distance data transmission is a serious obstacle to east-west linking of artificial intelligence applications and video conferencing facilities that have a low tolerance for data delay. These still rely therefore on data centers in the eastern region to meet their need for instant calculation and analysis. Only the data with high tolerance of data delay, such as background processing, offline analysis, and storage backup has so far been transferred to data centers in western China. This has led to a low utilization of data centers there.

Many cities in eastern China have built smart computing centers to support the growth of local artificial intelligence industries. The Guide for the Innovation and Development of Smart Computing Centers, co-authored by the National Information Center and Inspur Electronic Information Industry Co., Ltd, shows that city government investment in the smart computing centers can create 2.9 to 3.4 times higher growth of AI core industry production as well as a 36 to 42 times higher growth of related industries from 2021 to 2025 if the utilization rate of smart computing centers is able to hit 80%. At present, more than 30 cities in China are building or planning to build smart computing centers.

The White Paper on the New Generation of Smart Computing Center Network Technology, released by the China Mobile Research Institute, believes that smart computing centers can be networked to create a new type of infrastructure that can provide larger capacities and higher speed for AI computing. Smart computing centers emphasize the capability and quality of data storage and transmission per unit of time, or per unit energy consumption, while the traditional data centers continue to provide service deployment efficiency and an automation network.

Source: IDC, 2022

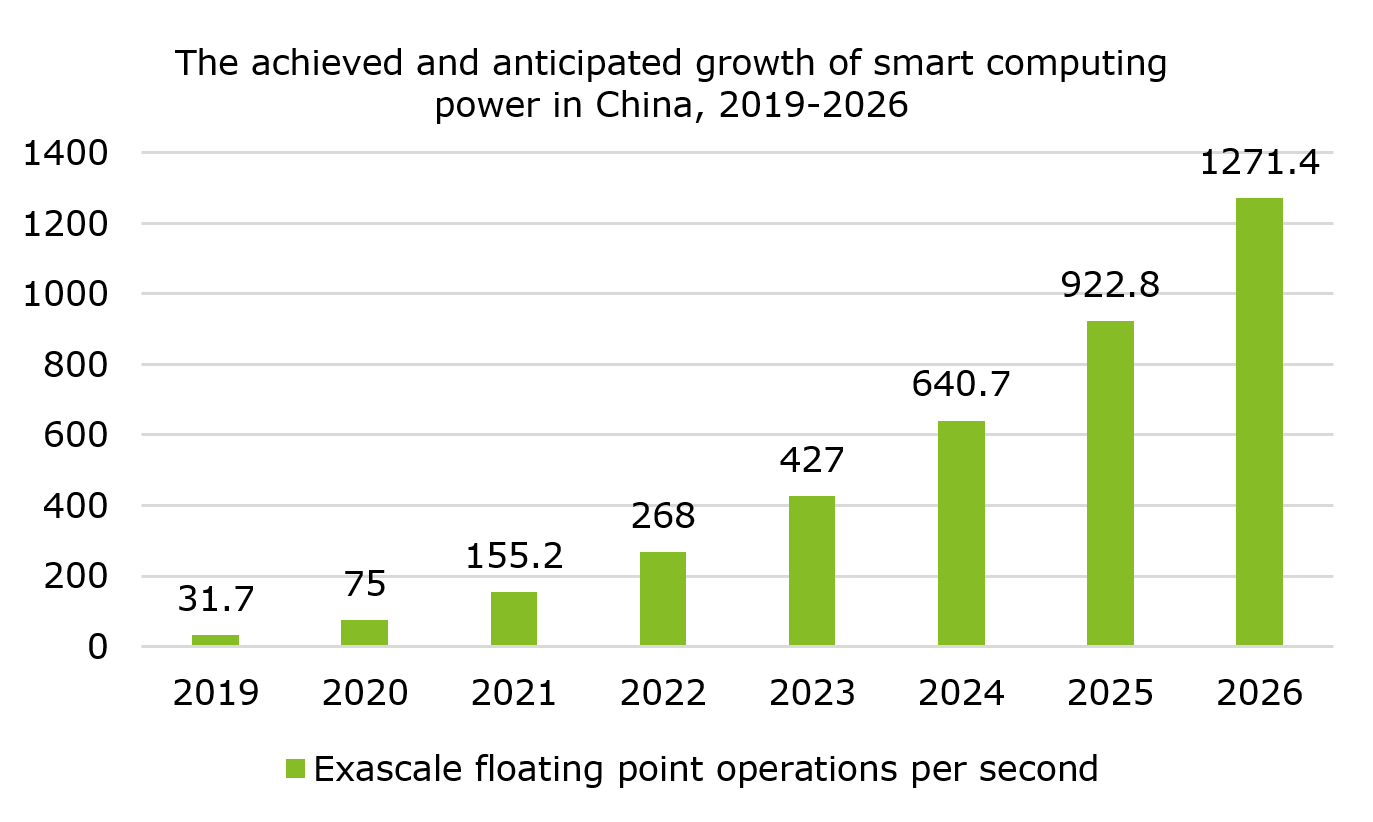

According to the China Artificial Intelligence Computing Power Development Evaluation Report 2022-2023 jointly released by IDC and Inspur Company, it is expected that the compound annual growth rate of China's computing power will reach 52.3% during 2021-2026. Currently the distribution of computing power is very scattered, making the importance of computing power scheduling increasingly urgent. The government should enforce a dynamic deployment of computing power according to the real-time demand of each city, by managing a nationally integrated computing power network and avoiding unnecessary investment in, or low utilization of, computing power resources. The nationally integrated computing power network will lead to a coordination between the computing power of eastern and western China, and therefore improve the overall capacity of computing power supply on a national scale.