Perspectives

The Deloitte Research Monthly Outlook and Perspectives

Issue 87

China's economic and industry outlook for 2024

Published date: 29 December 2023

Economy

The Chinese economy in 2024 – more pro-growth policies to come

Will the economy stage a recovery if backed by additional policy support? To what extent will the property sector be a drag on growth? Will a growth target be set? If so, is "around 5%" growth for 2024 the consensus? These are the key economic questions for China heading into next year.

It is almost certain that the growth target of "around 5%" for 2023 would have been comfortably achieved without additional stimulus. Assuming a growth rate of 5.3-5.4% for 2023, would this diminish the likelihood of further fiscal stimulus (monetary policy, as expected, will stay accommodative)? Should China set a lower growth target and prioritize 'higher-quality growth'? Does a higher growth target signal an emphasis on economic development amid geopolitical tensions? This policy dilemma reflects a dichotomy between broadly stable macro data in 2023 and subdued investor sentiment. Pro-growth policies and structural reforms are often trade-offs, but geopolitics has made such a trade-off more acute in this case.

In the property sector, the offshore USD bond market has experienced liquidity drying up, and the stock prices of major developers are trading at distressed levels. Prices in residential property markets in first tier cities, considered core assets by most domestic investors due to their concentration of healthcare and educational resources, have declined by roughly 20% this year. Price corrections in second and third tier cities are even more significant. While we believe that China has entered into a post-property era and must find new growth drivers, we do not see any potential for systemic risk arising due to consumers' vast savings and strict capital controls which allow the People's Bank of China (PBOC) to maintain an easing bias without concern for exchange rate fluctuations.

Can the green economy or various forms of the New Economy emerge as the principal growth driver if the property sector remains stagnant? The answer seems unlikely in the short-run, given the profound impact of real estate on various sectors and consumer balance sheets. Reflation may have therefore become a more necessary condition for China to transition towards a different growth model.

Let's review the pros and cons of a major fiscal stimulus. On the pro side, the primary argument is to prevent a potential deflationary spiral or a Japanese-style protracted slowdown. Investors are clearly eager for a substantial stimulus, often referred to as a "bazooka" stimulus. This would entail improved liquidity and would confirm economic development as the overriding policy objective.

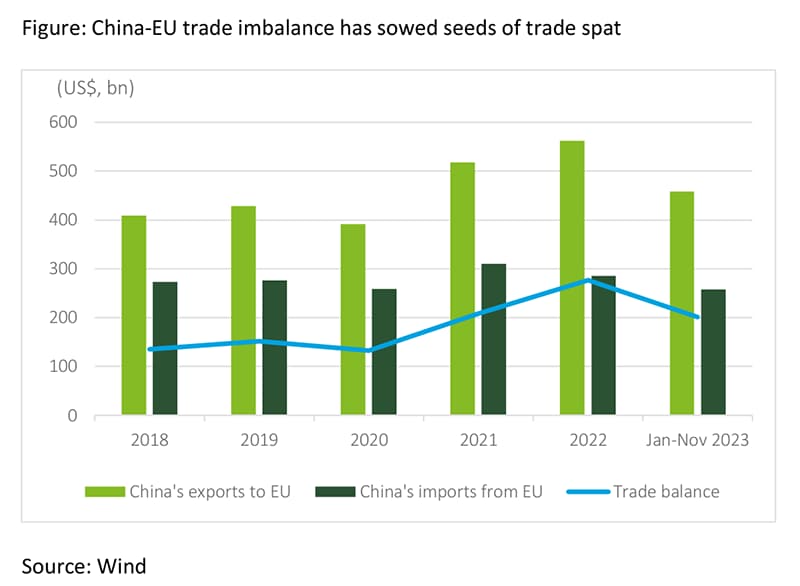

However, we have placed ourselves in the opposing camp for several reasons. China's lack of inflationary forces stems from over-capacity in the manufacturing sector and inadequate demand. Policymakers have increasingly pointed to the lack of demand as a key challenge. A large fiscal stimulus, akin to late 2008, could worsen both leverage overhang and over-capacity. The externalities from over-capacity cannot be easily shrugged off, especially amid rising protectionism. During the EU-China summit on December 7, EU leaders highlighted a persistent trade imbalance, while reiterating that a recent EU anti-subsidy probe into Chinese electric vehicle imports could result in double-digit tariffs. A significant fiscal stimulus may exacerbate trade tensions between China and the EU if certain zombie companies are getting more government support. That is why we advocate for more fiscal relief to the households and firms most impacted by the lingering effects of Covid-induced lockdowns.

The immediate priority is clearly the property sector, given its sheer size. Measures to ease restrictions in Beijing and Shanghai, such as reductions to the initial down payment, the extension of mortgage duration, and cuts to mortgage rates on December 14, are steps in the right direction. Similar measures have been taken in most cities, but actions taken in Beijing and Shanghai carry more weight in terms of setting the policy direction.

Easing in Beijing and Shanghai signals a few changes. Firstly, policymakers are demonstrating more commitment to encouraging consumers to contribute to growth, as housing demand in these cities represents more of a demand for improvement. Secondly, removing restrictive policies on the demand side effectively rolls back previous housing policies. Of course, more could be done; a 30% initial downpayment is still high and could be further reduced. The government also has ample means to boost pent-up demand, which has been deterred by concerns over developers' potential inability to deliver finished homes. Can the government underwrite this? The government could certainly designate some unsold flats as affordable housing units, for example. The key point here is that, notwithstanding excesses in terms of volume and valuation, Chinese consumers on the whole are not highly leveraged.

At the Central Economic Work Conference on December 12, the public sector was instructed to maintain fiscal prudence. This is logical, considering that many local governments have tended to rely on land sales as their primary source of revenue. Interestingly, the notion of "building the new before breaking the old" implies a recalibrated trade-off between reforms and reflation. The emphasis is now on the latter, at least until the property sector has stabilized, given the context of low inflation.

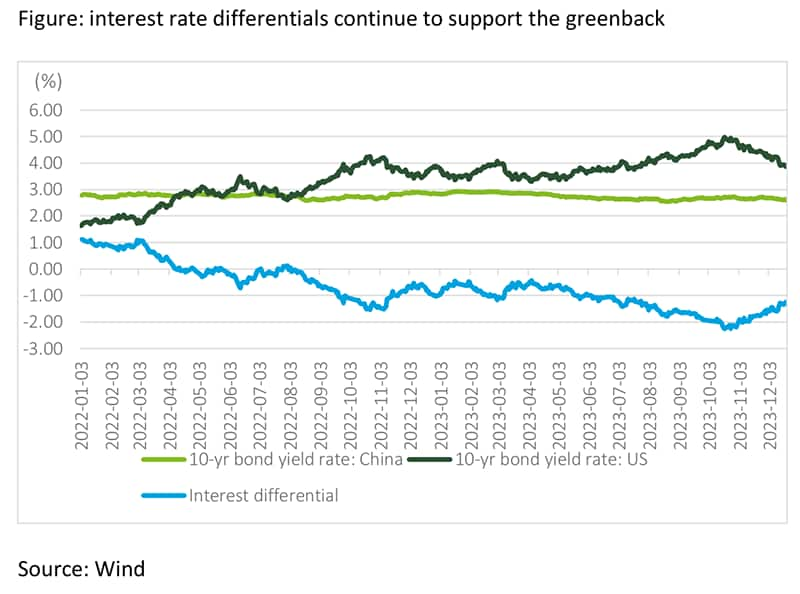

In conclusion, we anticipate more supportive policies to be unveiled in 2024, but these measures won't amount to a bazooka. Regarding the growth target, we foresee it hovering around 5%, which aligns with our current forecast of 4.5% for next year. Additionally, we expect a mild rebound of the renminbi due to an anticipated fall in US dollar interest rates. However, it is unlikely that the USD/CNY exchange rate will fall below 7.0, as interest rate differentials are likely to continue favoring the greenback.

Financial Services

"A nation with a strong financial sector" is the new goal of the Chinese financial industry

After the establishment of the Central Financial Commission and the Central Financial Work Commission, the Central Financial Work Conference was held at the end of October. It established a unified leadership on all matters relating to finance and enunciated the goal of building "a nation with a strong financial sector " for the first time.

A modern financial system with Chinese characteristics: China's financial industry should match the global status of its economy.

China is the world's second largest economy. In terms of asset size, China has the world's largest banking market and the second largest insurance market. Its stock and bond markets continue to be ranked second in the world. But while China's financial industry is large and plays an important role in supporting economic development, it is not strong, as its product quality, trading capacity, and risk control mechanisms still lag behind developed countries.

There has been a growing realization that "a nation having a strong financial sector" should have the power to issue international currencies and the capacity to price international financial products, to allocate global financial resources and formulate financial rules and regulations. This means that the internationalization of RMB, the internationalization of Chinese financial institutions, the opening-up of capital markets, the convertibility of RMB capital accounts, and the ability of China's international financial centers to attract and retain talent and resources, all need to further develop accordingly.

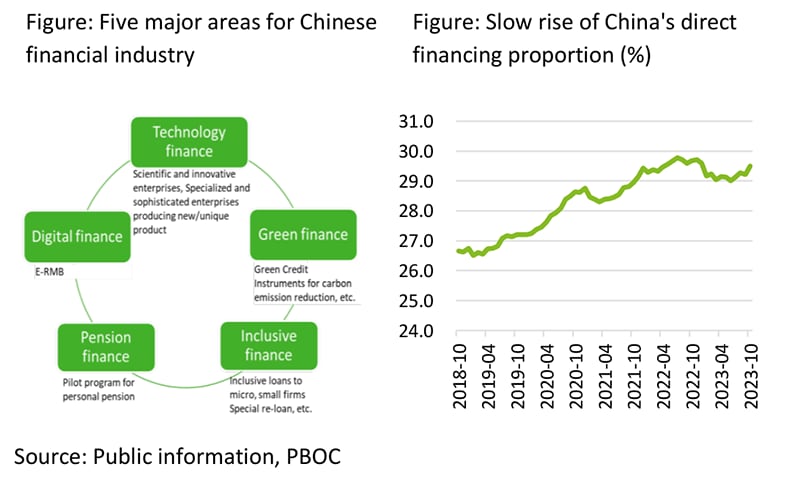

Financial services pivoting to five areas: technology finance, green finance, inclusive finance, pension finance, and digital finance.

In 2024, the coordinated efforts of a loose monetary policy and fiscal policy will continue. PBOC may cut interest rates in order to create a suitable monetary and financial environment for the resolution of government debt and the issue of various special support bonds.

We also think that the capital supply structure will become much clearer as more financial resources get allocated for technological innovation, advanced manufacturing, green development, and small- and medium-sized and micro enterprises. Second, support is to be provisioned for China's coordinated regional development strategy which involves a comprehensive revitalization of the northeast and the development of the central and western regions. Third, food and energy security will be given priority through agricultural modernization schemes and the establishment of new energy industries. The financial industry itself will pivot and focus on five areas: technology finance, green finance, inclusive finance, pension finance, and digital finance, injecting vital sources of capital into these key economic areas. We expect more precise guidelines by the relevant financial authorities in the course of 2024.

Establishing modern financial institutions and market systems to cultivate first-class investment banks and enhance the proportion of direct financing.

China's financial industry has been dominated by banks. At the end of Q3 2023, the proportion of assets of banks, insurance and securities institutions in the total assets of financial institutions were 90.4%, 6.5% and 3.1%, respectively. Correspondingly, the proportion of direct financing (issuance of bonds, and stocks by non-financial enterprises) was less than 30%, which is far lower than the 65-75% level commonly to be found in G20 countries.

From 2024 onwards, the registration-based initial public offering system will promote IPO financing. This should allow the A-share market to return to its previous high levels and increase the proportion of direct financing. The construction of a modern and multi-level capital market system depends on the establishment of first-class investment institutions that can be benchmarked internationally. Compared to Goldman Sachs and Morgan Stanley, whose international business income ratios are around 25-40%, Chinese securities companies need to accelerate their international business competitiveness, including increasing international business income and improving the types of derivatives.

Risk resolution focusing on local debt reduction, capital supplement for small- and medium-sized banks, and real estate regulation.

In 2024, macroeconomic stabilization, market confidence restoration, and loose and moderate monetary conditions will reduce risk and alleviate debt problems. There are three components to this:

First, banks will participate in the resolution of local government debts. At the end of October 2023, the issuance of RMB 1 trillion of special treasury bonds had a positive effect on the bond market and local government finance. In 2024, a "comprehensive debt reduction package" will be implemented in an orderly manner. Banks may participate in the resolution of local debts by reducing financing costs, extending maturities, and debt restructuring. As banks' earnings will be under pressure, the PBOC may provide liquidity by reducing the required reserve ratio or extending the MLF (Medium-term Lending Facility).

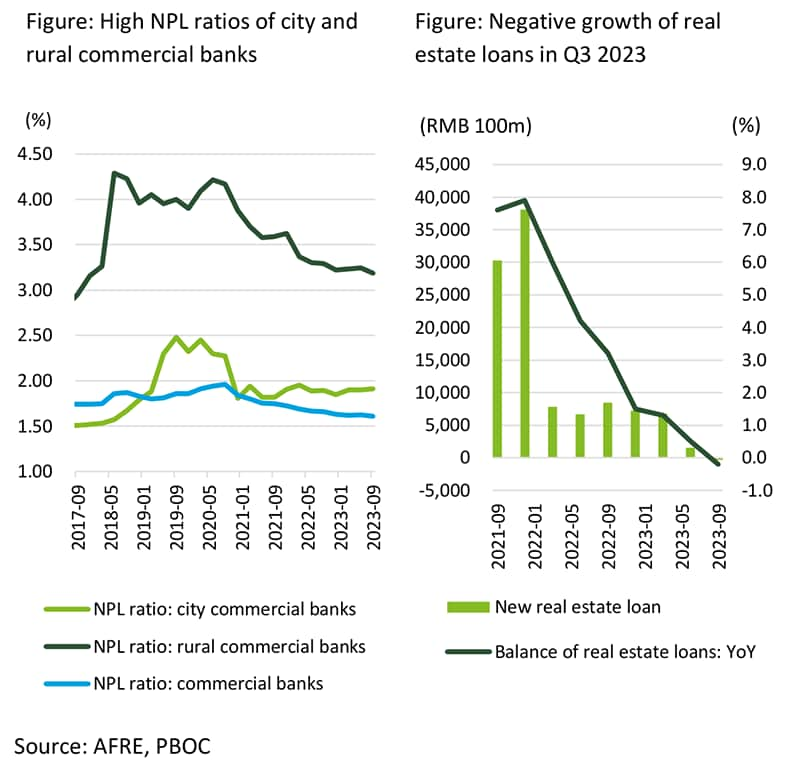

Second, the trend of excessive finance in real estate has been curbed, paving the way to a stabilization of the real estate sector. At the end of the Q3 2023, new real estate loans and balances showed negative growth which means that in 2024, to slow down the drag of the real estate sector on the overall economy and to stabilize the willingness of residents to purchase houses, there is now room for loosening the mortgage policy and interest rate adjustment.

Third, the issue of special bonds for capital replenishment of small- and medium-sized banks (SMBs) has accelerated. The non-performing loan (NPL) ratios of city and rural commercial banks has been growing rapidly, and is significantly higher than the industry average of 1.61 percent. These banks are also faced with the contraction of interest margins, increasing their vulnerability. Special bonds for capital replenishment of SMBs have been created to support these banks as they play an important role in their local communities. From January to the end of October 2023, a total of RMB 152.3 billion has been issued, an increase of 142% compared to the whole of 2022. In 2024, participation by local financial holding companies and local governments via shareholding and finance subscription will help SMBs to defuse risk.

Continuing the institutional opening-up in the financial sector: solidifying Shanghai and Hong Kong as international financial centers

Financial system-based opening will focus on facilitating cross-border investment and financing, the internationalization of the RMB, Sino-US cooperation in auditing, and building closer ties between the mainland and Hong Kong markets. Shanghai and Hong Kong will be developed further as international financial centers open to the outside world by increasing their level of performance. They need to play their part in maintaining confidence in the capital market and attracting more foreign financial institutions and long-term capital to invest and operate in China.

Energy

Navigating the green energy transition by understanding the new market dynamics

At this crucial moment in the race to achieve net zero emissions, the global need for green energy is greater than ever and China continues to play an integral role in this. In 2024 China's investment in green energy is expected to maintain a strong momentum and expansion into overseas markets, as well as into those 'hard-to-abate' sectors such as steel, cement and petrochemicals, will accelerate. In the near future, the following four trends will shape the development of green energy in China:

China's renewable energy companies accelerate their overseas expansion, and the rapid development of new energy technologies will lead to new investment hotspots.

Driven by multiple factors such as overseas markets, supply chain security, and global deployment, China's renewable energy companies have accelerated their overseas expansion, especially into "Belt and Road" countries (BRI countries). As of the first half of 2023, Chinese companies have invested more than US$60 billion in the renewable energy sector in BRI countries.

This trend is expected to continue in 2024, and the rapid development of new energy technologies such as hydrogen, floating wind power and new battery materials for energy storage. In October 2023, the Suez Canal Economic Zone (SCZONE) inked a $6.75 billion agreement with China Energy Engineering Group to build a project with an annual production of 210,000 tons of hydrogen and 1.2 million tons of green ammonia. To meet emerging technologies' higher requirement for production facilities, greenfield investments would be preferable to M&A investments.

This means that upstream and downstream companies, as well as financial institutions and service institutions, will be linked more closely than ever. There will be opportunities to further overseas investment in renewable energy through cooperation with existing overseas firms or through industrial chain linkages or by launching investment alliances. All will serve to increase China's influence in the renewable energy sector.

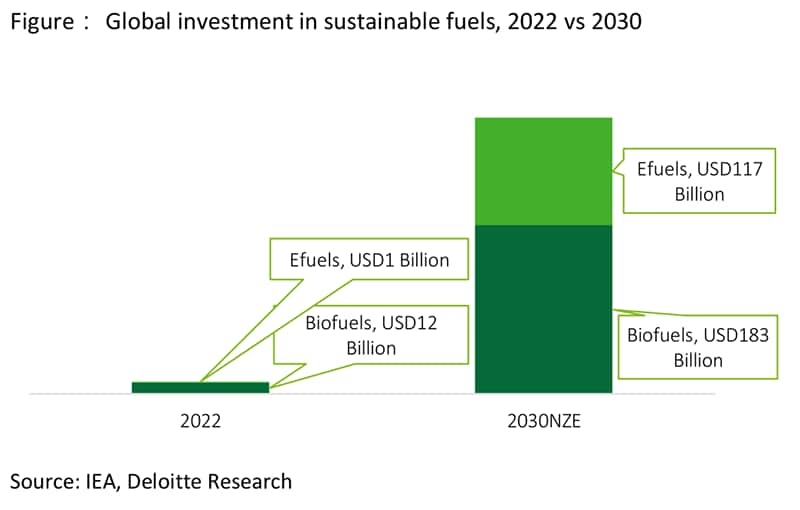

Sustainable fuels will make for a greener future in hard-to-abate sectors, and the development of SAF will enter the fast lane.

Sustainable fuels, including "biofuels" produced from agricultural and forestry residues and "E-fuels" produced from green electricity, are becoming increasingly popular given their significant potential in carbon reduction. The ReFuelEU Aviation Regulation, released by the EU in October 2023, sends a positive signal for establishing a sustainable fuel market. Starting 2025, aviation fuel suppliers at EU airports must distribute an increasing share of sustainable aviation fuels (SAF), and the minimum share of SAF in the total transport fuel available must go up from 2% in 2025 to 70% by 2050.

Although at present SAFs cannot compete in price with fossil fuels, with the development of relevant technologies and the growth of demand, investment in SAF is expected to enter the fast lane in 2024. According to public information, the combined operational and announced SAF production capacity in China has already exceeded 1.6 million tons per year, and Chinese airlines such as Air China and Cathay Pacific are engaged in SAF flight tests.

The promotion and application of SAF in the aviation sector could provide a novel way to achieving net zero targets for the hard-to-abate sectors such as shipping or heavy industry, where electrification or other options are more difficult and expensive.

The "Green Trade Barrier" is fast approaching, and green power will help enterprises promote their green transformation.

The CBAM (" Green Trade Barrier "), implemented in the EU in October 2023, includes on the collection list inputs indirectly involved in the production of goods such as purchased electricity and raw materials during production, in addition to imposing carbon tariffs on direct emissions generated by production of goods. In 2022, China's exports of high-carbon emission products such as steel, aluminum and cement to the EU reached 19.96 billion euros. The implementation of CBAM will increase the cost of China's high-carbon exports to the EU.

In this regard, traceable "green power" can be an effective way to break the carbon barrier. In 2022, China's first 100% traceable clean energy green big data center - China Telecom (National) Digital Qinghai Green Big Data Center has been completed and put into operation, reducing about 300,000 tons of carbon in one year of operation, with the data center achieving "carbon neutrality" and "zero carbon" status.

In 2024, China will continue to deploy traceable green power to improve the green standards of production of goods. The development of traceable green power will not only help promote the green transformation and upgrading of export enterprises, effectively breaking through the Green Barrier such as international carbon tariffs, but also promote the realization of sustainable development goals.

Intelligent technology reshapes power sector, and the market role of new business become clear.

Digital transformation of the power system is accelerating towards ubiquitous intelligence. AI can be used to forecast power generation capacity and enable optimal operation of the power plants while robots can complete the inspection and maintenance task of transmission lines instead of human operators with lower costs and smart charging stations can save charging costs by scheduled charging period. The application of emerging technologies reshapes electricity production and consumption, giving rise to emerging business as well as new business models.

Looking forward to 2024, with the development of relevant support policies, the market roles and business models of emerging business such as independent energy storage and virtual power plants (VPP) will be realized. Currently, VPP pilot programs have been carried out in many regions in China, including Hebei, Shanghai, and Shenzhen. In July 2023, grid companies successfully completed joint operation of VPP in Guangzhou, Shenzhen, and Liuzhou, which means that VPP could be actualized at different levels from small areas to greater regional areas in the future.

New business models not only provide a new way for emerging technologies to create value, but also provide suitable application scenarios for technology verification and iterative innovation. Thereby they could provide better support in the decarbonization of the power sector.

The increasing demand for green energy brings new opportunities for the energy sector and companies need to enhance their technological competitiveness, as well as strengthen their supply chain resilience and climate strategy. They also need to develop the capacity to respond quickly to external changes so as to seize opportunities as they arise and avoid costly penalties. This will enable them to achieve high-quality development.

G&PS

Easing the debt burden of local government through special bonds

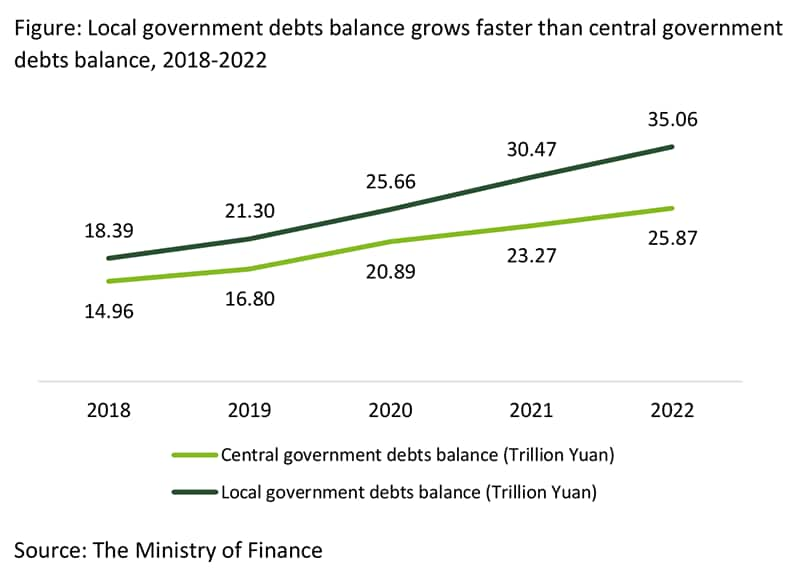

Easing the debt burdens of local governments is a long-term task, and the pressure on local government debt interest payments in 2024 should be a top priority. The treasury department of central government has helped local governments ease hidden debt stress by issuing special refinancing bonds, and many city investment companies owned by the local government have made hidden debts explicit by using special refinancing bonds. Next year, the financial sector is expected to accelerate the process of easing local government debt stress but, at the same time, the central government will increase the central government debt rate to alleviate the imbalance between local government revenue and expenditure.

The issue of special refinancing bonds makes the hidden local government debts explicit, and the financial sector will step up its efforts to support the easing of local government debt stress. Since local governments restarted the issuing of special refinancing bonds in October this year, a substantial volume of these bonds has been issued, making it possible for many city investment companies owned by local governments to replace their high-interest debt instruments with low-interest ones. As of December 1, RMB 1.37 trillion worth of special refinancing bonds were issued to repay local governments' high-interest debts. According to Essence Securities data, in October alone local governments' "borrow new to retire old bonds" policy accounted for more than 80% of the local government bonds issued. The issuing of bonds has hit a new high since 2022, reflecting the local government's urgent need to ease debt stress. These special low-interest refinancing bonds with will be used to repay existing high-interest debts, helping to reduce financing costs and alleviate the short-term liquidity pressure for those provinces and cities. However, the estimated maximum amount of the special refinancing bonds to be issued is RMB 2.6 trillion, which can repay only 4.7% of the bonds issued by the city investment companies owned by the local governments. It is still inadequate for avoiding debt risk. A large part of the debt of city investment companies owned by the local governments is debt to banks and other financial institutions. According to a guidance of the Central Financial Work Conference, banks will continue to use loan extensions, rate cuts, and debt replacement in the next 2 to 3 years to support easing local debt stress. It is expected that in 2024, the central government will establish working groups on financial support to ease local governments' debt stress at the inter-ministerial level and the local government level.

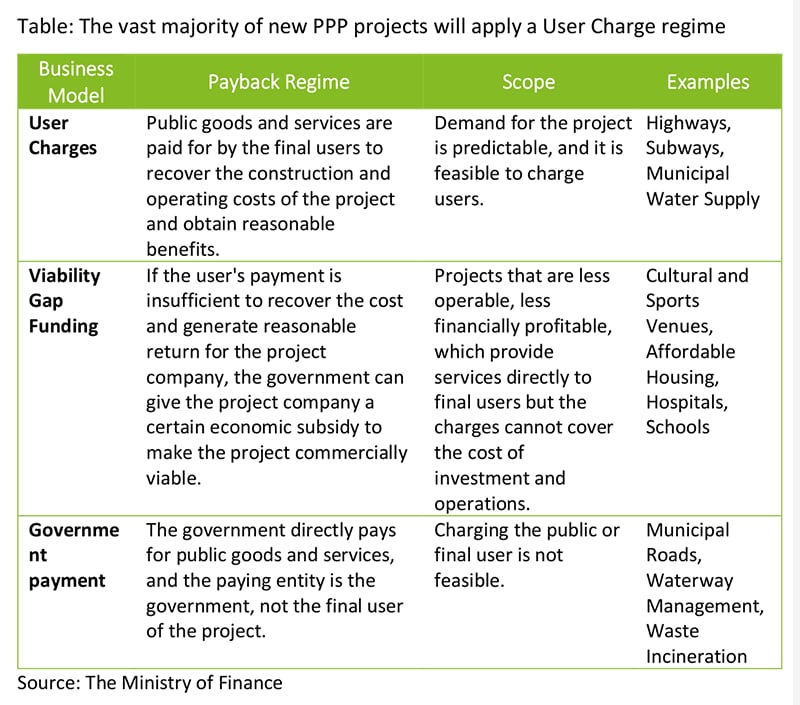

The new public-private partnership (PPP) mechanism requires most new PPP projects to focus on user-pay projects, which will prevent local governments from incurring new hidden debts. On 8 November, the National Development and Reform Commission (NDRC) and the Ministry of Finance (MoF) jointly issued the Guideline to Regulate the New Mechanism of Public-Private Partnership (PPP), which has been the most significant adjustment to the PPP mechanism since 2014. According to MoF statistics, from 2014 to 2022, a total of 6,687 PPP projects were initiated, with a total investment of RMB 11 trillion. These projects can be divided into three business models: Government Payment, Viability Gap Funding, and User Charges. The first two types with lower or even no income accounted for more than 90% of all projects and investments, inducing a heavy burden of debt to the local government. The new mechanism requires all PPP projects to use the concession mode, which requires social capital to account for most or all the investment and shares the benefits and risks with the public sector. It means that there will be no additional responsibility for future expenditure on local governments. Shortly after the announcement of the new guideline, the NDRC revised the Measures (Regulations) for the Administration of Concession for Infrastructure and Public Utilities which defined the concession of infrastructure and public utilities as a public-private partnership (PPP) model based on user charges. To prevent local governments from increasing their hidden debts, the new administrative measures prohibit project financing from being guaranteed by government funds or using government funds as a source of repayment. The new policy also required that operating income from the PPP projects cover its construction investment and operating costs and have a certain profit. These requirements have raised the threshold for PPP projects, which means the number of PPP projects will significantly decrease in the short term. From a long-term perspective, however, the new administrative measures will encourage insurance funds to provide diversified financial support for concession projects and actively support eligible concession projects to issue infrastructure real estate investment trusts (REITs).

The central government will increase its debt to support proactive fiscal policies of local governments. In 2024, there will still be a fairly considerable imbalance between local fiscal revenue and expenditure, and local governments will need incremental financial support to implement proactive fiscal policies. The central government's borrowing did not rise substantially during COVID-19, which makes it possible for the central government borrowing to increase to fulfil proactive fiscal policies. The central government has just issued government bonds of RMB 1 trillion (USD 136.7 billion) for the fourth quarter and has allocated the money raised to local governments, with the principal and interest of these bonds paid by the central government instead of by local governments. This means that in future, certain expenditures of local governments may be financed by the central government. It is probable that the central government will continue to increase its spending next year, assuming a more substantial role in proactive fiscal policy.

"Data Finance" is expected to become a new channel for increasing government revenue. In August, MoF released the Interim Provisions on Accounting Treatment of Enterprise Data Resources, which is scheduled to take effect on Jan 1, 2024. The document clarifies that enterprises could recognize data resources as intangible assets and represent their value and business contributions in their financial statements. Some financial institutions estimate that the potential data asset market could reach tens of trillions of yuan, while the tax revenue generated by data assets, codenamed "Data Finance", might replace the declining "Land Finance", and become a vital source of fiscal income. Nevertheless, the institutional foundation of data assets is not yet mature, making it unrealistic to count on "Data Finance" in the short term. To quickly address the issue, some cities will first expedite the construction of fundamental regulation systems for data assets, such as data rights confirmation, pricing, transaction circulation, and revenue distribution. For example, in November Beijing began a data infrastructure pilot zone to create an institutional environment conducive to promoting the capitalization of data resources.

TMT

AI and sustainability to take center stage

In 2024, the pace of technological innovation will accelerate and artificial intelligence and sustainable technologies will take center stage. Through the application of sustainable development strategies and generative AI, it is expected that enterprises will further reduce costs, increase efficiency, promote innovation, and thus garner advantages in the face of increasingly stiff competition.

Driven by enterprise software, Generative AI adoption will increase.

As we enter 2024, we have three projections: First, we predict almost every enterprise software company will embed generative AI in at least some of their products. Second, there will be a mix of pricing models: explicit per seat pricing (per user per month), consumption-based pricing, and a hybrid approach or free. And finally, we predict that the revenue uplift for enterprise software companies will be approaching the USD 10 billion run rate by the end of 2024.

For most enterprises, the "gateway to generative AI" will likely be through the three categories wherein generative AI features are embedded in existing software. The most common software tools with AI embedded in them are: "broad enterprise productivity software suites", "enterprise software tools" and "engineering, design, and software development tools". But generative AI is expensive to operate and its value to customers may not yet be clear. End users, for their part, may take some time to determine how AI capabilities can translate into direct value for their businesses. But, as more companies are able to increase profitability through the use of these software tools we will soon get a better sense of their value and how much people are willing to pay for them.

In China, we predict that the scale of commercial applications of generative AI will grow rapidly and will reach RMB 207 billion in 2025. The current application implementation is mainly focused on value enhancement and efficiency improvement, and implementation at the commercial value level is still being explored. We expect that generative AI will be adopted in three stages by different types of businesses based on the maturity of technology and data accuracy: first the marketing and customer service sectors, then human resources, manufacturing and supply chain that require higher data accuracy, and finally, more sophisticated business scenarios such as R&D, legal affairs, and finance.

More generative AI to be trained on private enterprise data.

In 2024, globally, enterprises will pay more attention to the industry-changing potential of generative AI. But relying on widely available public solutions may bring unnecessary information and data security risks. Therefore, many companies will opt for training generative AI on their own data to enhance productivity, optimize costs, and unlock complex insights - such as industry trends and market predictions. This will greatly reduce risk in the decision-making process. We predict that enterprise spending on generative AI will grow by 30%, from an estimated US$16 billion in 2023 to around US$20.8 billion in 2024. We could also see growth in private data centers as larger businesses – and government entities – seek to bring more generative AI capabilities in-house and under their control.

In China, enterprises are still the main force in the domestic large language model R&D, about 46% of which are independently developed by enterprises. But at the same time, companies are paying more attention to issues such as the source of training data, data quality, intellectual property protection, and personal information leakage. Therefore, we believe that in the near future more companies will want to have their own in-house private data centers. It is expected that the scale of private enterprise data centers in the country will reach RMB 178.6 billion in 2025.

New solutions to make the telecom industry more sustainable.

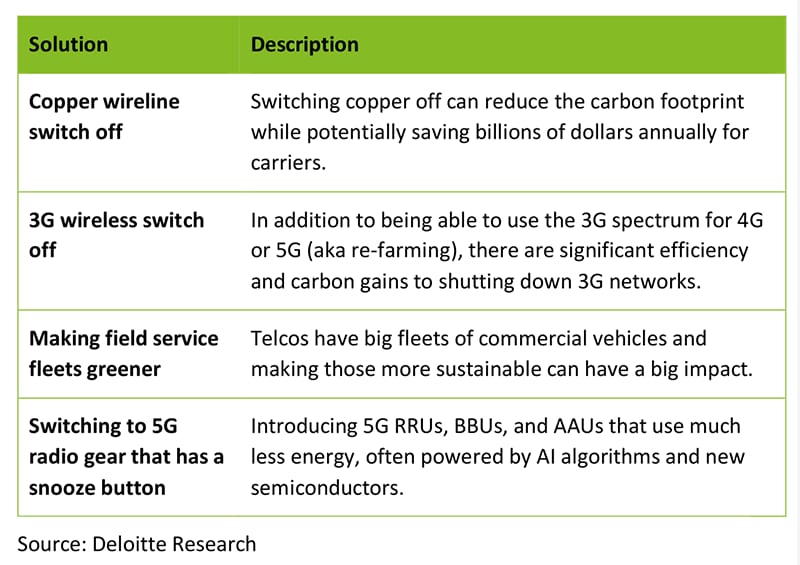

We predict that telcos worldwide will be able to reduce their carbon footprint by 2%, or 12 million tons of carbon dioxide equivalent (CO2e) in 2024 and do the same again in 2025. Telcos are publicly listed, consumer-facing, for-profit companies, and improving sustainability can help them comply with regulations, attract subscribers, and shore up their bottom line. In addition to the traditional ways of making the industry more sustainable (e.g. buying more renewable energy, running data centers more efficiently, getting consumers to keep devices longer, and encouraging the growth of the refurbished devices market), four new solutions will be implemented in 2024:

China's telecommunications infrastructure has gone big on resource-sharing, including the construction of supporting facilities such as shared towers. By the end of 2023, China Unicom and China Telecom had a jointly deployed 5G network of about 1 million base stations, the world's first, largest and fastest 5G shared network. Currently, the energy consumption of a single 5G base station site has been reduced by more than 20% compared with the initial commercialization period. The site sharing experiment has been so successful that it is forecast that by 2025, the site sharing rate of new 5G base stations will be no less than 80%, and the power utilization efficiency (PUE) of newly built large data centers will be reduced to less than 1.3 while the energy efficiency of 5G base stations will be improved by more than 20%, and the PUE of renovated core computing facilities will be reduced to less than 1.5. Energy consumption will have a green upgrade.

Making chips greener and leaner

Making chips is energy intensive. The chip industry was responsible for approximately 0.2% of global CO2 equivalent emissions in 2021. It may increase to 0.4% by 2030 as the industry doubles in market size. Currently, most of the industry progress towards greater sustainability will come from implementing manufacturing transformation on those older plants (brownfields): We predict that a full manufacturing transformation project can significantly reduce the intensity of energy, water, and process gas use over a multi-year period.

China is accelerating the construction of a green manufacturing system. So far, China has established 3,616 green factories and 267 green industrial parks at the national level. In addition, chip manufacturers are actively exploring effective measures to reduce carbon emissions. For example, a chip factory in the city of Chengdu adopted upgraded cooling tower management systems and control equipment which produced an annual power savings of more than 2 million kilowatt hours, reducing carbon emissions by approximately 2,100 tons. In the future, more and more chip companies are expected to use renewable energy and greener alternative materials in the manufacturing process. They also aim to promote green manufacturing through measures such as improving energy efficiency and resource recycling.

Retail

Changes in consumption patterns bring new opportunities and adjustments in policy

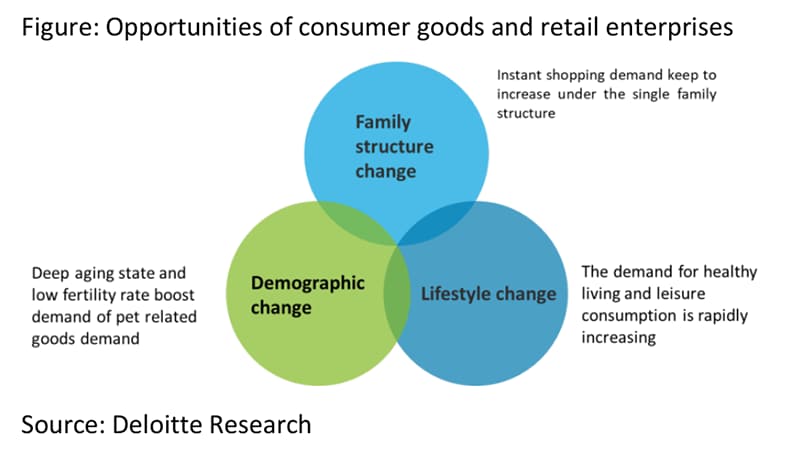

In 2023, there was a very important change in the pattern of goods and service consumption. For, while the consumption of "physical goods" decreased, the consumption of "services" such as restaurants, catering tourism, and entertainment and concerts registered gangbuster growth. From January to November, the retail sales of goods and services increased by 7.2% and 19.5% year-on-year, respectively. Service consumption is now being seen as the new engine for restoring and expanding consumption. Looking ahead to 2024, with stable economic growth and increased household income, the policy effects of "restoring and expanding consumption" and "promoting high-quality development of the tourism industry" will be gradually become evident. At the same time, the changes in inter-generational demographics, family structure, and lifestyle in China are becoming increasingly obvious, and China is experiencing a new round of structural changes in consumption. By analysis of national demographic and lifestyle changes, we have identified new trends of consumer market as follows,

The demand for healthy living and leisure consumption Is rapidly increasing.

In recent years, due to longer working hours and heightened pressure in their lives, young people have increasingly suffered from age-related diseases. As COVID-19 wreaked havoc on people's lives, consumers have begun to pay greater attention to their own health and that of their families. In this context, there have emerged niche markets for nutrition, health care, and wellness related services as well as ill health prevention and chronic disease control. The demand for services that teach people how maintain a reasonable diet, take regular exercise, quit smoking and reduce the consumption of alcohol has increased. With consumption increasingly focused on healthy food and beverage habits, retail enterprises should emphasize the green, natural and healthy aspects of their products in order to win customers.

The sustained growth in demand for leisure activities will continue in 2024. In September, the General Office of the State Council issued several measures to unleash the potential of tourism and promote high-quality development of the tourism industry. They proposed the rapid implementation of relevant policies to strengthen inbound tourism work. China announced in early December a pilot program to expand the scope of unilateral visa-free countries, which was welcomed by all sectors. The visa-free policy will not only increase the revenue of inbound tourism and related industries such as duty-free shopping, hotels, and catering in China in the next year, but also promote investment in the entire tourism related industry chain. In the future, we expect continued growth in service-oriented consumption; outdoor sports, short-distance tourism, staycations, and entertainment related markets will continue to grow as will outdoor hobbies such as horticulture, camping and mountaineering.

An aging state and low fertility rate boost demand for pets and related goods.

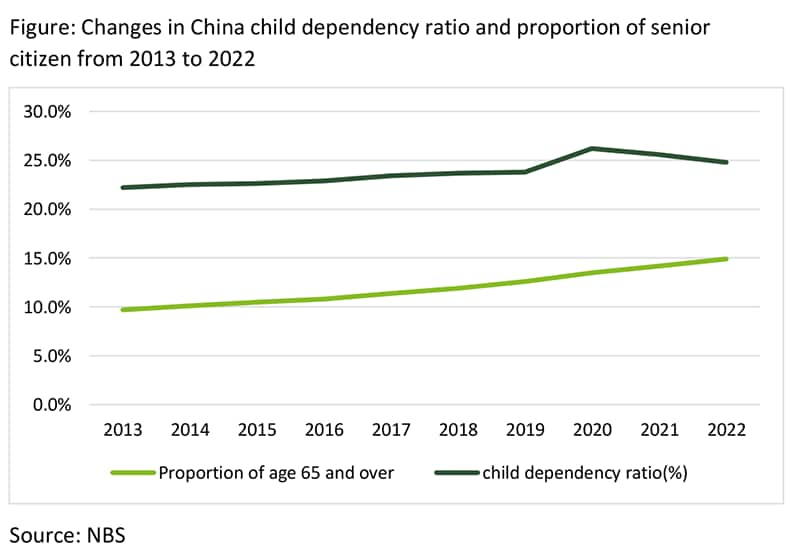

In the second decade of the 21st century, China's demographic changes have accelerated. According to data collected in the decade from 2013 to 2022, the proportion of elderly people in China increased from 9.7% of the population in 2013 to 14.9% in 2022. Meanwhile, the child dependency ratio has decreased from 26.2% to 24.8% for two consecutive years since 2020. These decreases reflect the reduced willingness of young couples to have children. We see a corresponding shift in household expenditure from child related expenditures to pets.

This shift has created rapid growth in demand for goods and services related to food, nutrition, daily necessities, and healthcare for pets. The rise of the pet economy has created opportunities for dairy, food, and beverage enterprises with diversified businesses. Industry leaders should accelerate the adjustment of their business portfolios and efficiently enter the pet market.

Instant shopping demand keep increasing under the single-generation household structure.

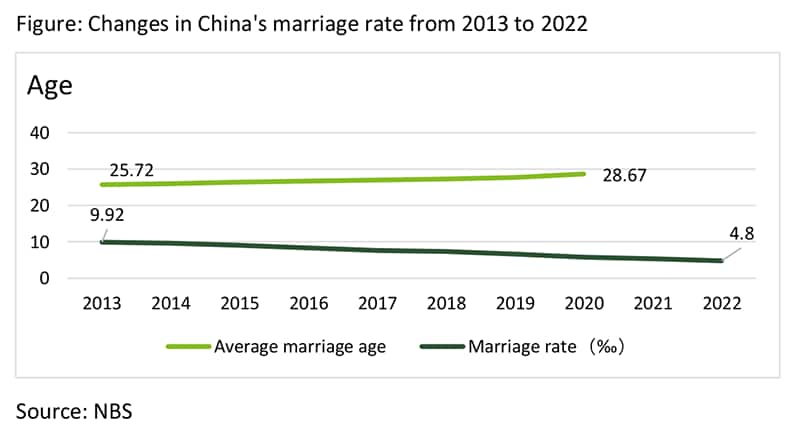

With China's continuous decline in marriage rate and rapid increase of marriages later in life, single and "dual income, no kids" (DINK) families have become the most common family structure among young consumers. The increase in single-generation households and the faster pace of life have rapidly increased demand for convenience, accessibility, and entertainment among consumers born in the 1980s, 1990s, and 2000s. This has meant processed foods, convenience stores, and mobile entertainment have become essential consumption segments for such households.

Instant retail enterprises and product suppliers should focus on consumers' desire for convenience that suits the lifestyles of single or DINK family members. At the same time, their simple structure gives these families more time to socialize, which means there are opportunities for the development of various online and offline interest communities and experiential entertainment services.

In summary, in 2024, with the growth of household incomes and the promotion of consumption policies by the government, the willingness and confidence of residents to consume will be enhanced, which will accelerate the recovery of the domestic consumer market. Meanwhile, a new round of changes in consumer structure will bring about new market opportunities in the consumer goods retail market.

Automotive

Price wars in the domestic market while exports face headwinds

In 2023 automobile sales in China did not see the anticipated growth they had expected to see from post-pandemic 'revenge' purchasing. Instead, a year-long price war ensued. The intense competition over pricing accelerated the deterioration of profitability in the automotive manufacturing industry and lengthened the amount of time the many new EV startups required to reach break-even point.

Weak domestic demand coupled with cut-throat competition prompted major OEMs to seek expansion through exports. In 2023 automobile exports increased from less than 1 million in 2019 to over 4 million, becoming an emerging growth driver for the Chinese automotive industry. Looking ahead to 2024, domestic demand for cars is unlikely to reach pre-pandemic levels. However, the trends of electrification and artificial intelligence integration will continue to lead the industry towards high-quality development. Additionally, geopolitical risks and the rise of trade protectionism may mean that automobile exports could face headwinds overseas.

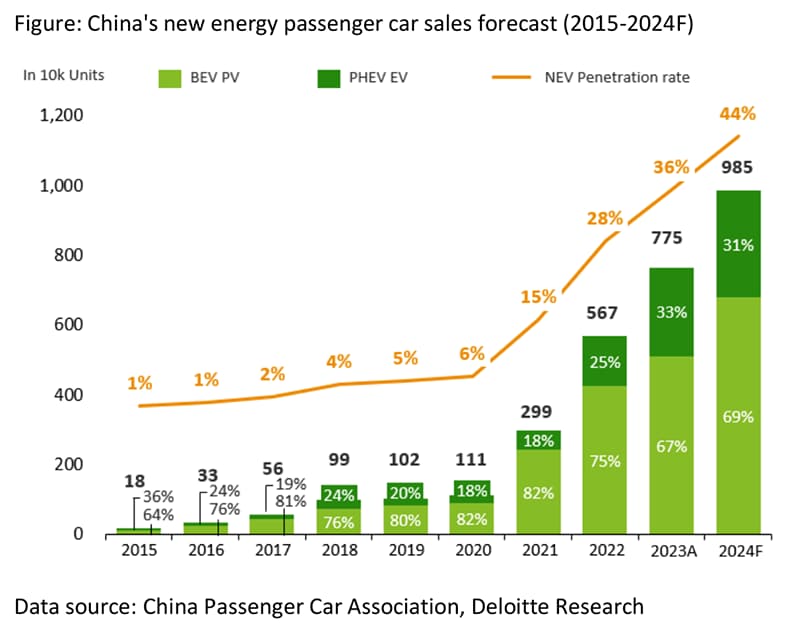

Fuelled by an increase in product offerings, a reduction in costs and technological innovation, China's NEV penetration rate is projected to punch through the 44% ceiling to reach 44%, increasing its competitive advantage over gasoline rivals. Since 2020 NEVs have achieved high growth for three consecutive years with sales increasing from a meagre 1 million to over 7 million units, and the penetration rate climbing from 6% to 36%, making NEVs the undisputed growth engine in China's car market. This report projects that NEV sales will climb to about 9.8 million in 2024 with a penetration rate reaching 44%.

i. More choices of NEV products across all price ranges. In 2024, 151 new car models are expected to be launched in the Chinese market, among which 77% (about 117) are electric ones. The soon-to-be launched NEV products will cover a broad range of price segments – from entry level to premium, thereby catering to needs of consumers with different levels of income. For instance, entry-level EV sedans are mostly catering to mid-to-low-income buyers who are looking for a good bargain without sacrificing on overall performance. Premium EVs target high-end buyers who prioritize luxury and technological innovation. At the same time, some newly launched models will also cater to niche market consumers such as electric off-road vehicles.

ii. Continuous decrease in raw material prices provides boost for NEVs reaching cost parity with its ICE counterparts. The current mainstream automotive batteries have a high dosage of lithium carbonate. It is estimated that if the price of lithium carbonate decreases by RMB 100,000 per tonne, then the cost of an average new energy vehicle can theoretically be reduced by RMB 2,000-4,000. The average price of lithium carbonate has fallen from a high point of RMB 560,000/tonne in 2022 to RMB 150,000/tonne in November 2023, a drop of more than 70%. Looking ahead to 2024, the continued release of upstream mineral production capacity will mean that lithium carbonate prices still have room to drop. This will provide the necessary foundation for NEVs at different price segments to achieve parity with their gas-powered counterparts.

iii. Technological advancements to alleviate range anxiety on EV charging. Range anxiety and charging time used to be the biggest obstacles affecting wider EV adoptions. With average driving ranges of existing mainstream NEV models reaching more than 500 kilometres in the Chinese market, consumers' worries over ranges have substantially waned. However, with the increasing popularity of electric vehicles, the time it takes to charge them has become a concern for many. EV makers have adopted a two-pronged strategy to tackle this, placing great emphasis on improving the charging experience; 1) implementing a high voltage electrical system in its electric vehicles, which allows for faster charging. 2) launching supercharging networks with higher power capacities, thus shortening the charging time from 10-80% to less than 15 minutes.

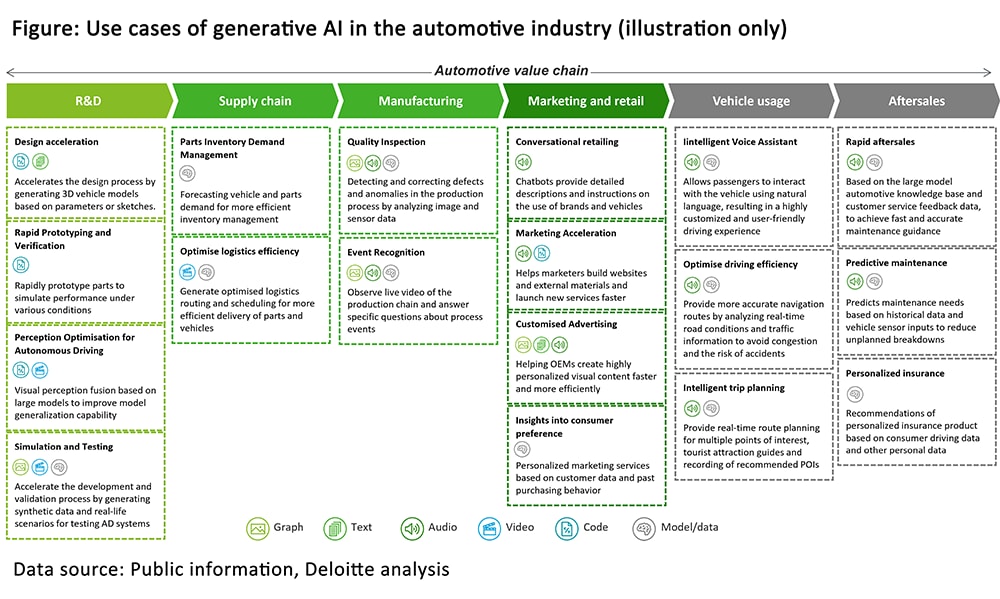

Empowered by AI, the trend of intelligent vehicles is expected to usher in a pivotal moment. AI large language models are expected to generate a wide range of application potentials across the entire value chain of automobiles, including autonomous driving, intelligent cockpit, human-machine interaction, smart manufacturing, marketing, sales, and after-sales service (as shown in the figure), and will provide significant value to product improvement, operational efficiency enhancement, and the transformation of traditional business model for auto OEMs.

i. Currently, Chinese auto OEMs are focusing on two prominent areas - smart cockpit and autonomous driving, hoping to enhance user experience and highlight their differentiated technological capabilities with the help of AI large models. For example, the new-generation smart cockpit based on AI large language models will shift from the previous version of "passive commands" - where drivers tell the virtual assistant what to do - to versions with active interactions - where the system will provide active services that meet users' personalised preferences and habits. In the field of autonomous driving, the introduction of large models can improve the perception and generalisation capabilities of autonomous driving system. For example, Tesla's bird's-eye view and occupancy network utilize a network of cameras and sensors to achieve a detailed understanding of the vehicle's environment, enabling precise object detection, path planning, and decision-making without the need for LiDAR technology, which not only improves the accuracy and robustness of its FSD system but also reduces the cost of hardware at the same time.

ii. The automotive industry is making headway in harnessing the power of large AI models. Currently, automotive manufacturers are exploring the application of large AI models in the automotive field in two ways: in-house R&D and external collaboration. 1) In-house development representatives such as Li Auto have constructed the entire architecture of MindGPT from the ground up and have begun training the entire large language model. 2) The collaborative approach is what most car companies adopt. Broadly speaking, there are two approaches: platform-level and application-level cooperation. The former involves building application layers on top of mainstream large model platform layers and the latter refers to purchasing off-the-shelf solutions from AI companies, as exemplified by companies like Hongqi, Great Wall, and Dongfeng Nissan. These companies announced their access to Baidu's big AI model -"Wenxin Yiyuan," which has allowed the OEMs to directly integrate customized AI experiences into their native in-vehicle applications.

In 2024, it is expected that the export of automobiles will potentially reach 4.5 million units amidst fluctuations. With the rise of trade protectionism and other geopolitical risks, the outlook for automobile exports remains uncertain. The focus areas for expansion will include the ASEAN, Middle East, and Australia, as exports to Europe are expected to slow down. Emerging markets such as Thailand, Indonesia, and Saudi Arabia are actively promoting the electrification of their automotive sectors. These markets have large consumer bases, a younger demographic, and a high willingness to embrace emerging technologies, with local governments making efforts to create a favourable policy environment for electric vehicles. Furthermore, learning from the experiences of early movers in the field, Chinese automotive companies venturing into international markets are optimizing their entry strategies, overseas organizational structures, and talent development. Additionally, the recent partnerships of Volkswagen and Xpeng, Stellantis and Leapmotor among others, provide a new paradigm for Chinese automotive companies who want to enter the overseas markets: using partnerships to leverage their existing production capacity against the sales networks of their multinational partners to access foreign markets and circumvent political and trade risks.

Logistics

Cross-border e-commerce logistics has become a new growth point

Entering 2024, as China's overall economy continues its transformation towards higher quality, the development of the logistics industry and the evolution of the competitive landscape have entered a critical period. While in the domestic logistics market companies continue to achieve the goal of cost reduction and efficiency enhancement through digital empowerment, in the international market, due to the weak global freight market and increased geopolitical and other uncertainties, they still face challenges. However, it is optimistic that the booming development of cross-border e-commerce will drive express logistics enterprises to achieve deployment and expansion in dedicated lines and international express networks, and the competitiveness of Chinese logistics enterprises will be further uplifted.

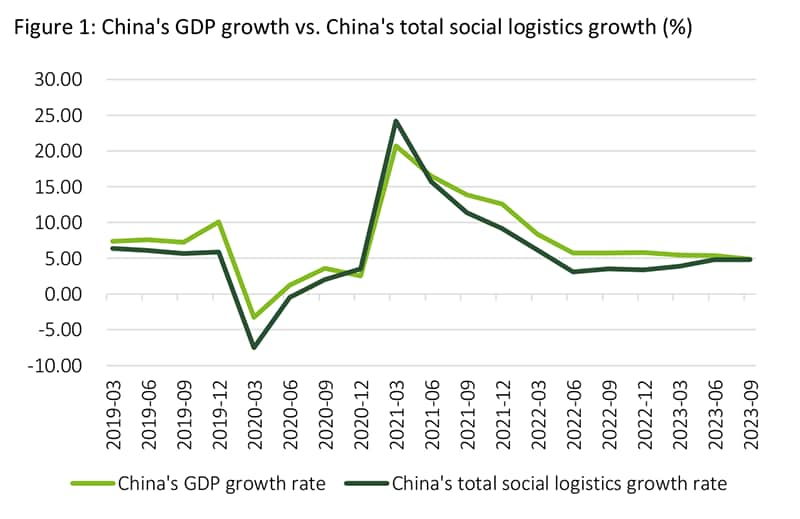

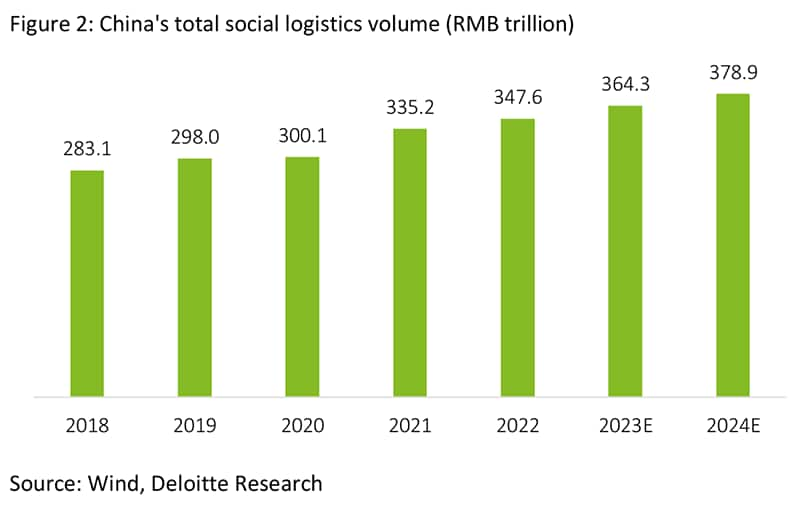

The modern logistics industry, as the cornerstone of important industries such as manufacturing, e-commerce, and foreign trade, has always been positively correlated with the overall growth rate of China's economy (see Figure 1). Since 2023, with the recovery of the Chinese economy, quarter by quarter, the logistics market has correspondingly achieved steady growth. It is estimated that in 2023, the total amount of China's social logistics revenue is expected to reach around RMB 364 trillion, an annual growth of about 5%. By 2024, this figure is expected to reach RMB 378.9 trillion, an increase of about 4% year-on-year (see Figure 2). Looking ahead to 2024, we should see the following four trends in the logistics industry: market, technology, social responsibility, and capital operation.

Source: Wind, Deloitte Research

Market expansion: Cross border e-commerce logistics continue to develop, and overseas warehouse construction has become a key task.

At present, China's e-commerce is ranked first in the world in terms of scale. In the field of cross-border e-commerce, Chinese enterprises continue to use big data to integrate the resources of the entire supply chain and create a flexible supply chain to solve the conundrum of traditional export of goods in mass production and cross-border e-commerce exports which are based upon the personalization of consumer demand. The transition from B2B (traditional trade) to B2C (e-commerce trade) brings more opportunities for Chinese logistics enterprises. The construction of overseas warehouses will become one of the key tasks in the development of cross-border logistics.

The essence of an overseas warehouse is to localize cross-border trade and enhance the shopping experience of consumers, thereby improving the local competitiveness of cross-border sellers in destination markets. Where overseas warehouses are concerned, Southeast Asia is expected to become the first choice of destination as Southeast Asia's e-commerce market size growth ranked first in the world in the past three years, and demand for overseas warehousing is therefore also rising rapidly. Expanding from a single point logistics transfer station to a comprehensive service center that can provide more ecological chain services will be the future development direction of overseas warehouses, as this enhances the core competitiveness of service providers.

Technological innovation: Accelerate digital transformation and technological empowerment, and build a digital supply chain.

At present, enterprises in express logistics, storage parks and other fields actively employ advanced digital and intelligent technologies to develop integrated service supply chains. This has greatly improved their operational efficiency and allows them to continue to expand the trinity of software, hardware, and system integration of supply chain technology advantages. Automatic handling robots, sorting robots, intelligent delivery vehicles, as well as self-developed warehousing, transportation and order management systems are some of the core technology products and solutions they use to improve efficiency. These technological innovations cover the main processes and key links of the supply chain including campus, warehousing, sorting, transportation, and distribution. At present China's logistics industry is still in a period of development and there is a lot of untapped demand. Providing specialized and intelligent integrated logistics services will be a new growth point for logistics enterprises in the future.

Social responsibility: Jointly build an efficient and shared logistics ecosystem to achieve green logistics transformation.

Climate change has brought green and low-carbon development center stage globally. Because the logistics industry is heavily dependent on energy and transport fuels, the green and low-carbon development of the logistics industry is an indispensable part of the green and sustainable development of the supply chain and the industrial chain. Under the guidance of the green development concept and the green and low-carbon development policies successively introduced by the Chinese government, Chinese logistics enterprises in 2024 will continue to work in tandem with upstream and downstream parties in the supply chain to do the following:

- To jointly implement green and low-carbon strategies such as gradually increasing the use of clean energy and promoting the use of clean energy and new energy transport vehicles;

- To build digital warehouse and digital transport capacity platforms to improve operational efficiency;

- To carry out technological transformation, improve the energy efficiency of equipment, and build green warehouses;

- To implement innovations in management, and build energy and carbon emission management systems.

Capital operation: Under the trend of industry consolidation, the demand for investment, financing and listing still exists.

From January to October 2023, investment and financing events and M&A activities in the logistics industry have decreased, but under the general trend of industry consolidation, demand has remained high for investment and financing, mergers and acquisitions and public offerings. Investment and financing needs are mainly concentrated in the new intelligent equipment market while mergers and acquisitions are concentrated in the overseas expansion of the international market, especially the cross-border supply chain infrastructure in Southeast Asia.

In the IPO market, from January to October 2023, a total of 6 logistics enterprises have completed the listing process, and 2 enterprises, SF Holding and Cainiao Logistics, have submitted applications for listing. Among them, the successful listing of Polar Rabbit Express in October 2023 raised a net capital of HKD 3.528 billion and today its current market value is about HKD 105.7 billion. Sixty per cent of the funds raised are being used to expand their logistics network, upgrade their infrastructure, and strengthen their sorting and warehousing capacity, as well as for research and development and technological innovation. Therefore, its listing sends out two signals to other logistics enterprises: 1/use capital to move towards global logistics and continue to expand into more international markets and 2/ continue to upgrade express delivery speed and service capabilities. In the next two years, in addition to the integrated logistics enterprises eager to go public, logistics technology enterprises and supply chain service enterprises may also join the listing fray.

Life Science & Healthcare

A new start that 'brings out the best'

In 2023, China's life science and healthcare (LSHC) industry underwent significant reforms and changes, with a clear direction for future development that encourages the survival of the fittest. The ongoing reform has begun to show initial results, with "rectification" and "innovation upgrade" becoming the two key words in 2023. Entering 2024, the capacity to innovate will be even more critical as both policies and capital markets favour companies with 'Original Innovator' characteristics. This will further high-quality development of the industry.

The levelling-up of rectification and compliance efforts in the LSHC industry deepens the concept of 'people-oriented' development. In 2023 we saw the national anti-corruption campaign in the healthcare sector go into high gear. In May, 14 ministries, led by the National Health Commission, jointly issued the Notice on Printing and Distributing the Key Points of Rectifying Unhealthy Practices in the Field of Pharmaceutical Procurement and Sales and Medical Services in 2023. This initiated a comprehensive corrective action across the entire industry chain and all aspects of the LSHC sector. The self-examination and self-correction phase lasted from May to June 2023. Beginning in July, a centralized rectification phase began that should last 10 months. A report on the rectification campaign is expected in mid-2024 and a series of new regulations may be introduced to further enhance the supervision of the LSHC sector and improve public welfare. Therefore, for LSHC companies, the urgent task is to re-examine and adjust their own compliance business, increase investment in compliance affairs, stay updated with the latest regulatory scheme, and be prepared for the upcoming new regulatory landscape.

The "clinical value driven" and "high-quality development" requirement has been strengthened for pharma companies, raising the bar on survival. In April, the National Medical Products Administration issued new regulations that further optimized the marketing approval process and evaluation of novel drugs. While accelerating the approval process of high value innovative products, it also raised the marketing approval threshold for homogenized and fast-follow ones. Additionally, in November, in order to help companies achieve commercialization and recover R&D costs as soon as possible, the National Healthcare Security Administration proposed the "Newly Approved Drug Initial Price Formation Mechanism" which aims to provide reasonable returns for innovative products in the early stages of commercialization. With the gradual normalization of volume-based procurement (VBP), the mature product market continues to shrink, and low pharmacoeconomics value products gradually lose market competitiveness. In the future, LSHC companies in China need to focus more on high-quality innovation in order to produce truly original, innovative products. Meanwhile, companies with insufficient innovation capabilities may be pushed out of the market.

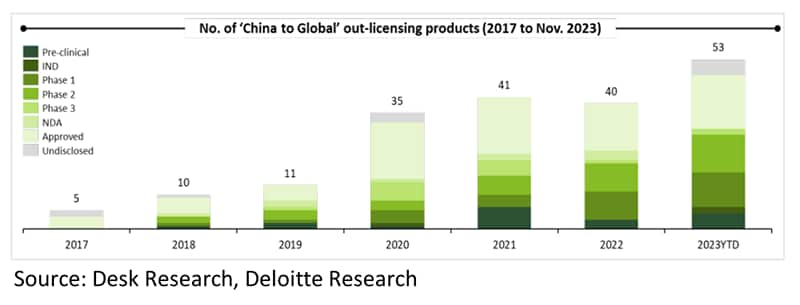

On the other hand, original pharmaceuticals from China have gradually gained global recognition, hastening the pivot away with from 'importing into China' and ushering in an era of 'exporting from China'. In recent years, the number of core clinical trials in China has significantly increased, rising from 177 trials in 2017 to 322 trials in 2022 so that China is now ranked number two globally. In addition, the number of out-licensing deals for China's locally developed innovative products recorded a five year high in 2023, including many FIC and BIC products while many locally developed innovative technology platforms have also gained recognition overseas. With the continuous encouragement of innovation from top to bottom and the reform of the domestic market, we can expect to see more innovative pharmaceutical and Medtech companies seek opportunities to go global in the coming years. Thus, China's capacity to innovate will gain greater recognition on the international stage, either through indigenously built teams or strategic collaborations such as M&A and out-licensing deals.

In the capital market, the value of the LSHC sector continues to adjust and investors are paying close attention to both innovation and profit. The anti-corruption drive that was in force throughout 2023 made investors cautious about investing in LSHC companies and hence, stock prices declined in the second half of the year. However, with the new regulations, which should come out in mid-2024, compliance will improve and this will restore investor confidence. Also, the China Securities Regulatory Commission announced a temporary tightening of IPOs coming to market in mid-2023. Investors, based on economic considerations and changes in risk preferences, are more inclined towards early-stage investments and value the technological strength of companies. Finally, investors are also exploring new exit channels, such as the M&A deals and stake acquisitions. Although the overall LSHC M&A deals in China are still on a decline, an upsurge in deal-making is expected in 2024 due in part to the tightening of IPO regulation. The series of policies supporting innovation allows qualified innovative LSHC companies to receive more attention. In 2024, investors may favour companies which are more innovative and regulation compliant. They may prefer early-stage investments through venture capital and other means while exploring more diverse exit mechanisms.

With the implementation of the Healthy China program, the threshold for innovation has been raised and greater value on will be placed on 'high-quality' products than ever before. The new guidelines such as the Action Plan for High-Quality Development of the Pharmaceutical Industry (2023-2025) and the Action Plan for High-Quality Development of the Medical Equipment Industry (2023-2025) have created a framework for future development and innovation. In the short run this will mean that LSHC companies will face tougher challenges in innovation and monetization capability. Meanwhile, the supervision of the entire industry chain will become the new normal. Adjustment of the strategic planning and business models needs to be expedited to for companies to survive in the new LSHC industry landscape.