Article

Riding out oil price volatility

Oil, Gas, & Chemicals Insights

Riding out price volatility

The current collapse in oil prices is very different from the one in 2008 in its causes and supply/demand pattern. Oil companies need to minimize expenditure to ensure business continuity while protecting the value of their core assets to prepare for a market recovery.

Double whammy

The oil market has been experiencing the double whammy of flagging demand and a record low price. The stagnant economic growth outlook, combined with the spread of COVID-19, has crushed demand. Furthermore, a supply shock has hit the market, with Saudi Arabia and Russia disagreeing on production cuts, triggering a price war that further depressed prices in March.

On 12 April, OPEC+, led by Saudi Arabia and Russia, agreed to cut 9.7 million barrels a day (Mb/d) of production during May and June. They will trim production cuts to 7.7 Mb/d in the second half of 2020 and 5.8 Mb/d between January 2021 and the end of April 2022. A G20 meeting was then held amid calls for a broader production cut, but failed to reach a final agreement.

The OPEC+ and G20 meetings were not enough to change market sentiment. Indeed, oil prices have dropped since the finalization of the OPEC+ deal as markets deemed production cuts insufficient to compensate for the drop in global oil demand.

Market attitudes could change depending on how the OPEC+ agreement is followed through, actions taken by other producing countries, and the actual extent of any drop in oil demand in the following quarter.

Inherent volatility

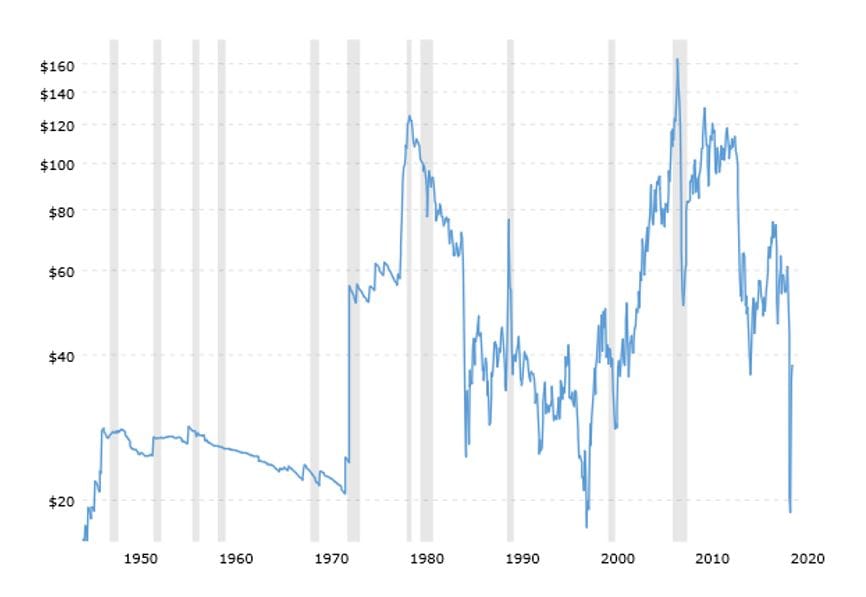

Oil prices are inherently volatile. WTI generally ranged between USD17 to USD20 (adjusted for inflation) between 1948 and 1970. Political, economic and other changes have consistently rocked the oil landscape since 1970, with sharper and more frequent volatility in the past three decades.

In the 22 years since January 1998, oil prices increased from USD10 per barrel in 1998 to a peak of more than USD145 in July 2008; dropped 80 percent in the following six months; fluctuated between USD80 and USD120 from 2010 to 2014; started a relentless drop in mid-2014 to under USD40 due to booming US shale oil production; then fluctuated between USD50-USD80 in 2016 before crashing to USD18 in April 2020.

Figure 1: Inherent volatility (WTI, USD per barrel, adjusted for inflation)

2008 Deja Vu?

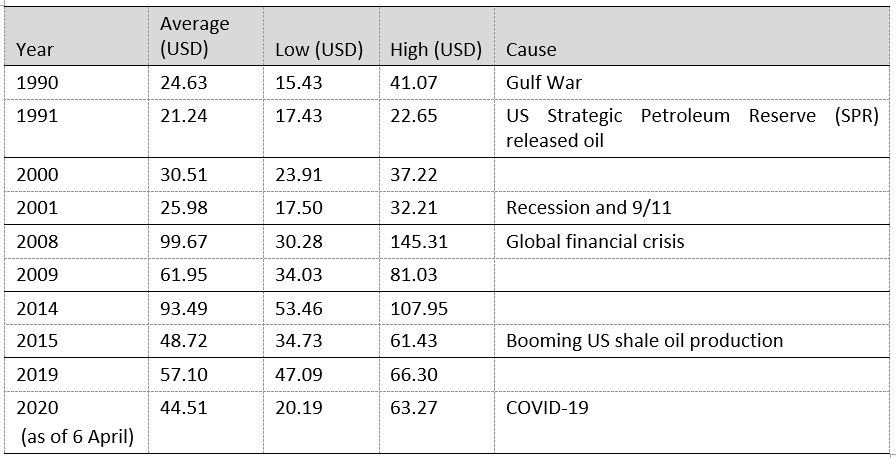

Some people see the current oil crisis as a repeat of 2008's that will last for some time. This view, however, ignores the fundamental difference between the current downturn and the 2008/9 crisis. The origins of the current oil price collapse, like most of the earlier episodes, such as those in 1991, 2001 and 2014, are in declining demand or excess supply. The 2008 crisis, by contrast, was caused by the collapse of financial institutions. Academic research shows that recessions originating in the banking system tend to be more severe and last longer.

Historical data suggests the same. The oil crisis in 1990 originated from Iraq's invasion of Kuwait, which led to the Gulf War. The potential loss of supplies from both countries, coupled with threats to Saudi Arabian oil production, prompted oil prices to rise from USD21 per barrel at the end of July to USD46 in October. The US reacted by releasing oil reserves, which brought prices back to about USD20 in 1991. The Gulf War oil crisis lasted about seven months before prices return to their pre-war level. The oil crisis in 2001 was a combined result of the US recession and 9/11. Oil prices fell from USD23.77 a barrel in August 2001 to USD15.95 in December, and then took about six months to stabilize.

In 2008, consumption and production took a hit as global markets dealt with the worldwide financial crisis. Oil prices dropped from historic highs of about USD147 in July 2008 to USD33 that December, and then took nine months to stabilize by August 2009.

Consumption patterns during the current oil price down cycle are also very different to those in 2008. Global oil consumption fell 0.5 percent and 1.5 percent in 2008 and 2009 respectively. However, this time around, there is hope of a modest increase in oil demand as global recovery consolidate, although slowly and unevenly.

China, the largest oil-importing country, is already recovering from COVID-19. The Government has lifted bans on road, air and train travel. Air transportation is showing sign of recovery. Crude processing, steel and construction are picking up. By end of April, China's oil demand has recovered to 90 percent of pre-pandemic level and the resumption continues.

This cycle will not be like the one in 2008, as global trends in production and consumption, as well as the roles of the world's major oil producers, have shifted. What the future holds is impossible to say for certain, but it will certainly look different to the post-2008 cycle.

Figure 2: Causes of WTI crude oil price variations since 1990

Putting the crisis to work

Two objectives—minimizing expenditure to ensure business continuity and protecting the value of core assets to retain competitiveness—are becoming clear in oil majors' response to the crisis. Chinese oil majors need to maintain viable domestic production levels to meet the country's energy security needs. China has set a floor price of USD40 per barrel for retail fuel as a buffer against international oil price volatility. However, prices of products already below USD40 will not be adjusted. Extremely low oil prices and sagging demand remain a drag on oil majors' profits.

The latest Deloitte survey of Chinese oil and gas companies shows three-quarters of respondents have cut their 2020 performance targets, as they expect crude and refined product prices to remain low throughout the year. Companies face huge challenges to manage commodity price volatility, ensure cash flow and protect asset value, and shore up sales and marketing, amid COVID-19 induced limitations on business activities.

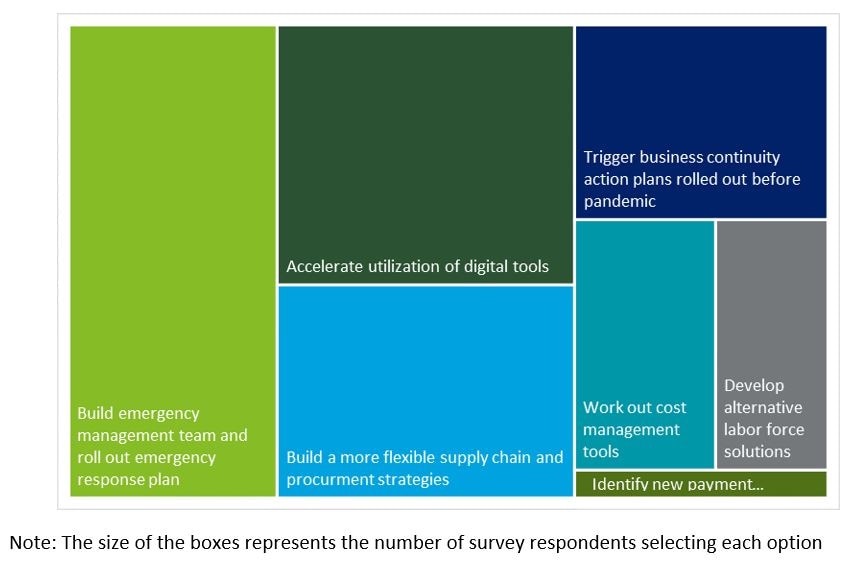

The survey found companies are looking at establishing or enhancing emergency management, accelerating their utilization of digital tools, adjusting their supply chain models, and pursuing cost management tools to counter the short-term impact of the pandemic (Figure 3). When the survey was conducted in mid-March, companies were already going all out to ensure business continuity, including by identifying alternative procurement channels or launching online and mobile business applications. With more Chinese oil and gas companies "feeling the squeeze", cost management has become increasingly important in corporate strategy, and they are joining the race to boost productivity and reduce operational cost.

Over the medium to long term, survey respondents will prioritize the following improvements to cope with extended market volatility: accelerating digital transformation; strengthening supply chain management; implementing new strategies; and optimizing cash flow and cost management. Some companies see digital transformation through a cost-saving lens and prioritize having an overarching, consistent digital strategy over plans for specific projects. Moreover, building flexible supply chains to improve resilience has now become a major task for executives.

Figure 3: Most popular measures to ride out the storm

Facing a double whammy, companies need to tailor their responses to the severity of the shocks they face: steering through price volatility before improving their resilience and portfolios to preserve options that will deliver growth when prices stabilize.

Cost management

Oil companies are downsizing oil and gas exploration and development.

Shell has reduced its planned business expenditure to USD20 billion from a planned USD25 billion to ensure its financial strength and resilience. It also plans to cut operating costs by between USD3 billion and USD4 billion this year. Exxon Mobil has reduced its 2020 capex budget by USD 10 billion, or 30 percent. Total S.A. is cutting capex by more than USD3 billion, reducing net 2020 investment to less than USD15 billion.

Chinese oil majors are also taking action. CNPC has built a steering group to work on improving productivity, ensuring positive cash flow, cutting costs and optimizing capital expenditure. Across Asia Pacific, close to USD35 billion of pre Final Investment Decision (FID) and development spend is at risk in 2020-2022, according to Wood Mackenzie.

The announced budget cuts are mostly in high cost upstream activities. Chinese oil majors are no exception, although they are maintaining domestic production and cutting foreign budgets first. As well as eliminating costly upstream activities, companies are also considering changing their approaches to achieve sustainable cost management— assessing their business value chains to identify where additional cost savings can be made. For example, construction and third-party contractor activities weigh heavily on oil company's production costs. Oil majors are talking to oil field service companies to alter contract terms or adopt new contract models, such as unfixed service fees with oil price changes factored in. Improving procurement is also having a substantial impact on earnings before interest and taxes (EBIT ). Oil majors are working with equipment providers to turn fixed costs into variable costs through leasing. This also benefits equipment providers by preventing inventory pile-up caused by reduced exploration activities.

Resilience

Volatility is a fact of life in the oil industry, and is tending to increase in impact and frequency. To deal with increasing volatility and growing supply chain complexity, oil companies need to rethink supply chain management. Those with many suppliers across different spend categories need to identify cost and sourcing options in each category and determine appropriate action, such as seeking alternative suppliers and altering contract terms. Meanwhile, oil majors are realizing that early engagement with suppliers can help identify opportunities for large-volume purchases. These allow buyers to receive discounts and suppliers to move inventory and maintain cash flow.

Data asset optimization is also critical. Data come from all divisions and departments, has various levels of detail and different time horizons. Oil majors need to align information strategy to broader business approaches and priorities, review their existing data asset layouts, identify needed improvements and implement effective information management.

Opportunities in restructuring

Many oil and gas companies face immediate problems in servicing debt as revenues dry up. These loans usually have oil and gas reserves as security, and these reserves are now worth less than they were few months ago. Distressed companies often consider M&A a way to survive a crisis, so Chinese oil majors will likely have opportunities to acquire high-quality assets. Oil companies need to be disciplined in their approach to deals, however.

Looking forward

Oil prices will rise again—just as day follows night, night will follow day. Crude oil prices will average USD33 a barrel for 2020 and USD46 a barrel in 2021, according to EIA's Short-Term Energy Outlook, although there will be occasional surges towards USD60, and the odd plunge to USD10. This low price environment will result from the interaction of the economic slowdown, environmental regulations, e.g. new shipping fuel requirements, persistent oversupply (i.e. shale oil). For companies in the oil sector, adopting aggressive cost management programs, building resilience, and capturing restructuring opportunities are the key to preserving options for future growth.