Article

COVID-19 potential implications for the banking and capital markets sector

Maintaining business and operational resilience

Learn what questions banking and capital markets leaders should be asking themselves right now and what action steps they should consider in the face of COVID-19.

COVID-19’S impact on individuals, communities, and organizations is rapidly evolving. A recent Deloitte Insights article posited four different scenarios for the global economy resulting from COVID-19, which ranged from a mild and temporary hit to the worst-case scenario, a global financial crisis.1Unfortunately, COVID-19 arrived when the global economy was already showing signs of a slowdown.2

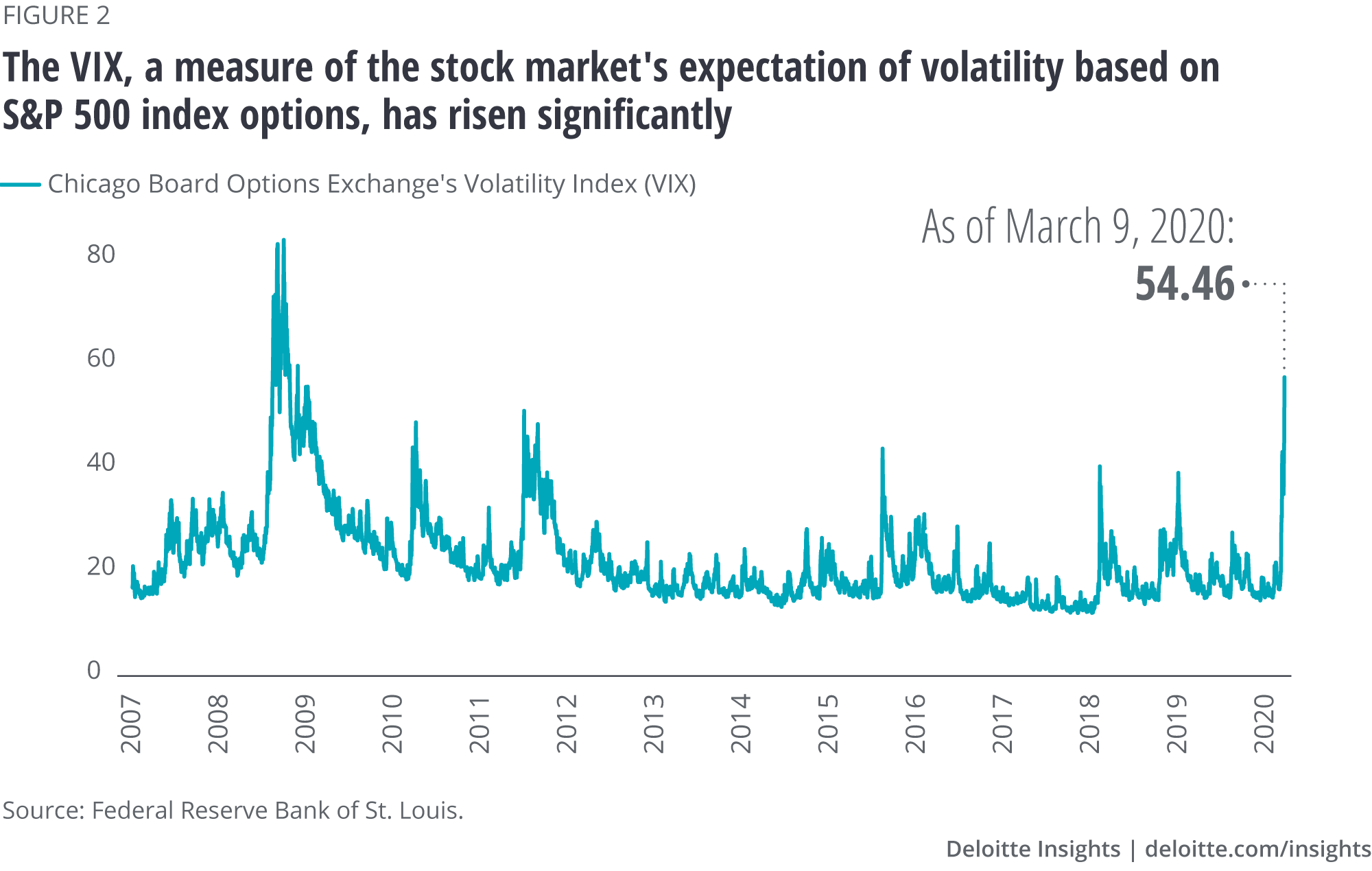

In addition to the effects on the supply and demand side, COVID-19 has already jolted financial markets. Since February 21, 2020, bond yields, oil, and equity prices have sharply fallen, and trillions of dollars, across almost all asset classes, have sought safety. In the United States, 10-year bond yields have tumbled below 0.5 percent3 (figure 1), and equity prices on major stock indices around the world have fallen. It appears, as of now, that the markets are trying to price using the worst-case scenario, which has increased volatility recently (figure 2).

With ongoing shocks to the supply and demand side, there is potential for further market disruption. Institutions and individuals may be experiencing liquidity stress, including limited access to credit. This might, in turn, increase the probability of default, especially near or in the speculative grade of corporate debt. Private debt, including corporate and household debt, has reached record levels recently, and approximately one-half of the investment-grade market currently holds a triple-B rating.4

Central banks around the world, meanwhile, have already proactively intervened to calm markets and show commitment to using all possible measures. In its first emergency move since the recession in 2008, the US Federal Reserve (the Fed) recently cut the federal funds rate by 50 basis points.5 The Fed has also actively intervened in the repo market to add further liquidity.6 The Bank of Japan (BoJ), meanwhile, issued an emergency statement signaling that it would inject liquidity into the market by increasing asset purchases.7 The People’s Bank of China (PBoC) has also pumped more than US$240 billion of liquidity into the financial system as a countermeasure to the virus.8 Additionally, the Bank of England and the European Central Bank (ECB) have announced various plans to counter COVID-19 in the coming days.9

But as the situation develops, more action may be required by central banks, regulators, and governments, which would necessitate quick coordination at the national and international levels.

Meanwhile, banking and capital markets firms around the world are mobilizing and taking steps to minimize COVID-19’s effects on day-to-day operations. Firms are testing and implementing business continuity/contingency plans, which include alternate workplace arrangements such as split work sites, working from home, and rotating shifts for all types of employees, even traders.10 Many have also instituted universal travel bans beyond the countries experiencing the most severe effects, and have canceled large events. Institutions have also heightened measures to ensure the safety and health of their employees through various means. Banks have also requested that regulators ease capital requirements.11 Some regulators, such as the US Securities and Exchange Commission (SEC), have proactively granted relief for regulatory financial reporting to companies affected by COVID-19.12

Many banks are also acting as responsible citizens by extending loans to hard-hit borrowers, renegotiating credit terms, and even donating face masks to their clients.13

Beyond the operational actions already underway, banks and capital markets must remain hypervigilant. They need to also actively consider the short- and medium-term financial, risk, and regulatory compliance implications that are resulting from the continuing uncertainty around COVID-19.

This article explores these implications. It also raises questions around key areas that banking and capital markets leaders should be asking themselves right now and provides action steps for them to consider.

Of course, any actions taken will depend on the specific context of the organization and its unique circumstances regarding exposure to the virus. Also, organizational priorities may change dramatically depending on how the situation develops.

We do not know the long-term implications of COVID-19 for financial markets and banking and capital markets firms. But when normalcy returns, banks and capital markets firms will likely have learned a few lessons. These may include how to best retain operational resilience when confronted with future pandemics, and possibly how to design new operating models such as alternate work arrangements. COVID-19 may further accelerate migration to digital channels and connectivity.

Specific implications for banking and capital markets firms

| Operational resilience | |||

| Topic/issue | Current and potential developments | Relevant questions | Actions banks and capital markets firms should consider |

| Branch/ATM operations | As the pandemic advances, some branches/offices may need to close temporarily, or employees may not want to come in to work. | How can banks ensure operational consistency with branch/office operations if there are temporary closings or employee absences? | Consider reducing branch hours or, if possible, utilizing only drive-through operations. |

| ATMs may need to remain open and have enough cash to dispense. | How can branches sufficiently replenish cash for ATMs? | Assess opportunities to deliver services solely through digital channels. | |

| Trade compliance | Many institutions already have traders working from home and remote offices, and some regulators such as the Financial Industry Regulatory Authority (FINRA) have temporarily waived rules in this regard. | What flexibility might regulators grant that would enable traders to work from home? | Be in close contact with industry groups, such as the Securities Industry and Financial Markets Association (SIFMA), and regulators, such as the Commodities Futures Trading Commission (CFTC), National Futures Association, and the FCA, for information and updates on obtaining waivers. |

| Meanwhile, the United Kingdom’s Financial Conduct Authority (FCA) has stated that all firms are expected to meet their regulatory compliance obligations regarding trading orders transactions, timely entry of orders, using recorded lines, and giving staff access to compliance support. | What systems/tools/support need to be provided to traders who may be forced to work from home? | Work with vendors to set up alternate recording options. | |

Sources: Rachel Louise Ensign, Liz Hoffman, and Justin Baer, “Wall Street scrambles to harden virus defenses,” Wall Street Journal, March 1, 2020; Pete Schroeder and Michelle Price, “Wall Street regulator paves way for home trading as coronavirus spreads,” Reuters, March 9, 2020; Laura Noonan, Nicholas Mcgaw, and Primrose Riordan, “Banks seek trading rule guidance as coronavirus spreads,” Financial Times, March 6, 2020.

| Financial and business impacts | |||

| Topic/issue | Current and potential developments | Relevant questions | Actions banks and capital markets firms should consider |

| Liquidity management | The Federal Reserve has intervened in the repo market to ensure adequate market liquidity. | If there is a liquidity crunch, what current plans and activation steps are in place? To what degree have they been reassessed in light of recent market conditions? | Adequate liquidity across the enterprise globally should be ensured. Banks should be closely reviewing and monitoring daily liquidity stress testing reporting, limit/threshold monitoring, liquidity coverage ratio (LCR) results, etc. They should be monitoring market activity against their liquidity stress indicators for triggers that would activate the CFP. |

| The ECB, BoJ, and PBoC have taken a variety of actions to ensure market liquidity. | If institutions needed to sell assets to cover liquidity shortfalls, are the requisite legal documents up to date? | Analyses should be conducted to determine the size and impact of any liquidity shortfall if liquidity stress indicators are being triggered regularly. Impacts to secured funding/asset sales (including market access) should be included in the analysis. This information should be presented to management across liquidity and liquidity risk (liquidity crisis team) as part of the CFP being activated. | |

| Some institutions’ contingency funding plans (CFPs) may have already been invoked. And due to market volatility, there could be big swings in stress testing results and limit/threshold breaches. Some market participants may already be experiencing increased liquidity tightening. | Liquidity preservation actions should be part of banks’ CFPs and would include options for ensuring liquidity if the CFP has been invoked. | ||

| Requirements should be recalibrated based on emerging market conditions and likely future scenarios. | |||

| Banks should go beyond the LCR requirements when communicating their liquidity status to regulators. Regulatory relations teams should be part of the liquidity crisis management team/committee under the CFP. | |||

| Capital management | Risk-weighted assets (RWA) may be impacted by higher charges from increased volatility levels and higher counterparty risks. | How do increased volatility and price movements of assets affect RWA? | Assumptions driving the valuation of asset values should be revisited. |

| With the implementation of Current Expected Credit Losses (CECL) and a potentially less favorable economic outlook, banks’ loss allowances may be negatively impacted. Also, borrowers may want to refinance at longer maturities to lock in lower interest rates. Under CECL, this could result in additional loss allowances. | Does the current economic and market environment warrant additional stress testing? How severe would a worst-case scenario be? | Additional stress tests with different underlying scenarios specific to COVID-19 should be conducted. | |

| With changes in economic assumptions, how will loan loss allowance estimates change? | |||

| Revenue and cost management | If general economic conditions deteriorate and lead to lower GDP growth, there could be reduced demand for banking products and services. | Do leaders know where potential revenue losses could be the steepest? | Work with relevant departments and units globally to develop an understanding of potential revenue hits and outline steps for mitigation. |

| With central banks aggressively cutting interest rates, banks’ net interest income will likely be challenged. | With potential declines to net interest income, what options exist to boost noninterest income? | ||

| Loan book, covenants, and exception management | With clients potentially experiencing stressed financial conditions, credit quality/ratings may be affected. | How can firms best assess and proactively work with clients who may be affected by the virus to renegotiate loan terms and conditions? | Find out which sectors/regions/clients are most at risk. |

| Also, pledged collateral may experience a decline in value. | Are borrowers/clients at risk of violating loan covenants? Is there an exception management process in place? | Reach out to clients with communications and information requests to provide temporary help as appropriate. | |

| Customers, both retail and institutional, may resort to minimal or delayed payments on their loan balances. | Will firms need to increase loan loss provisions? | Loan loss provisions under different economic scenarios should be reexamined. | |

| Trading/hedging strategies | Currently, increased volatility and decline in prices across many asset classes have impacted the trading books and increased market risk as well as counterparty credit risk. | How can capital allocations be determined across trading books in stressed markets? | Capital allocations and hedging strategies across trading books should be revisited. |

| Are precautionary steps, such as trading asset divestments, required, and if so, which assets could be disposed of first? | |||

| How quickly can hedging strategies be adjusted across foreign exchange, commodities, equities, or fixed income, as the situation develops? | |||

Sources: Federal Reserve Bank of St. Louis, “Overnight repurchase agreements: Treasury Securities purchased by the Federal Reserve in the temporary open market operations,” accessed March 9, 2020; European Central Bank, “Statement by the president of the ECB,” March 2, 2020; John Ainger and Anooja Debnath, “Investors dodging market meltdown say they can’t find liquidity,” Bloomberg, March 9, 2020; Sohini Chowdhury and Cristian deRitis, “Beyond theory: A practical guide to using economic forecasts for CECL estimates,” Moody’s Analytics, August 2018; Laurent Birade, “CECL: Credit cards and lifetime estimation—a reasonable approach,” Moody’s Analytics, September 2018; David Enrich, James B. Stewart, and Matt Phillips, “Spiraling virus fears are causing financial carnage,” New York Times, March 6, 2020.

| Risk and controls | |||

| Topic/issue | Current and potential developments | Relevant questions | Actions banks and capital markets firms should consider |

| Market risk | A sharp drop in interest rates and increased volatility in securities and FX prices increase banks’ market risk, potentially leading to losses. | Has the exposure of the institution’s earnings or economic value of capital been adversely affected, and is it materially different from model-implied scenarios? | Revisit internal models capturing market risk and account for potentially higher correlation. |

| Does the current environment warrant an update of internal models? | Communicate with the regulator if capital is adversely affected and materially differs from model-implied scenarios. | ||

| Counterparty credit risk | Recent market events may have affected counterparties’ credit profile. | How should any potential changes to counterparty creditworthiness be addressed in existing contracts and arrangements? | Assess/revisit existing contracts with counterparties most at risk. |

| How are market intermediaries, such as clearing agents, responding to any decline in counterparty credit standing? | Work with market intermediaries to stay informed about any changes to counterparties’ standing. | ||

| Nonfinancial risks | Nonfinancial risks such as conduct risk/culture, model risk, third-party risk, and cyber risk may also become more pressing. | How can risk controls regarding conduct risk be upheld in alternate work arrangements? | Rethink risk controls for alternate work arrangements and potential disruptions that could warrant a reassessment of conduct risk, cyber risk, and third-party risk. |

| Potential disruptions to trading infrastructure may require that trades be rerouted to other venues, locations, and countries. | To what degree are recent market conditions impacting model risk? | Revisit to what extent model assumptions reflect current and possibly future market conditions. | |

| What would regulatory requirements look like under alternate trade routing? | Obtain clarity from regulators about alternate trade routing. | ||

| As business process and flows change, what is the best way to manage cyber risk? | |||

| Risk governance | If a bank’s operating model needs to change, it may become difficult for the board of directors to continue to meet governance obligations such as overseeing risk, providing credible challenge to management, and acting as responsible stewards of the organization. | How should the board of directors adapt its governance? | Management should err on the side of overcommunicating with the board of directors, keeping them apprised and seeking their guidance on alternate operating procedures. |

| Flexibility in work arrangements and speed of decision-making among the board of directors could become paramount in these circumstances. | |||

| Dividends and stock buybacks | Banks have been returning capital to shareholders in the form of dividends and share buybacks over the past few years. | What is the appropriate strategy for dividends and buybacks, given current liquidity preferences? | Assess institutional shareholder interest and preferences for share buybacks and dividends and communicate any potential changes. |

| Recent market stress may put liquidity pressure on banks, which may want to preserve capital by halting or reducing dividends and share buybacks. | If there are commitments in place about dividends and/or stock buybacks, and banks want to temporarily halt these actions, how should this be communicated to shareholders? | ||

| Credit ratings | The COVID-19-induced market environment may negatively impact banks’ credit rating profile. | How are rating agencies accounting for the changes to these risk factors? | Stay in active communication with rating agencies and apprise them of changes to the credit standing. |

| New systemic, country, or other business risk factors may intensify and affect the creditworthiness of banks, counterparties, and borrowers, especially in the high-yield grade. | How should any potential changes to the credit profiles of counterparties and borrowers resulting from COVID-19 be accounted for? | Determine whether any rating actions flowing from COVID-19-induced stress would necessitate giving counterparties and borrowers some slack. | |

| LIBOR transition | LIBOR will be replaced with alternative reference rates in various jurisdictions by 2021. | Does the current market disruption impact transition plans and timing to replace LIBOR? | Stay abreast of regulators’ guidance and market developments in the alternate reference rate markets, such as the Secured Overnight Financing Rate (SOFR) in the United States. |

Sources: Laura Noonan, Nicholas Mcgaw, and Primrose Riordan, “Banks seek trading rule guidance as coronavirus spreads,” Financial Times, March 6, 2020; Alexandra Dimitrijevic and Paul F. Gruenwald, “Coronavirus casts shadow over credit outlook,” S&P Global Ratings, February 11, 2020; Sinead Cruise and Lawrence White, “The end of Libor: the biggest banking challenge you've never heard of,” Reuters, October 8, 2019.

General implications for banks and capital markets firms

| Operational resilience | |||

| Topic/issue | Current and potential developments | Relevant questions | Actions banks and capital markets firms should consider |

| COVID-19 crisis readiness | COVID-19 is disrupting the operations of many banks and capital markets firms globally. | Has a comprehensive reassessment of exposure to the full vectors of threat been done? | Banks and capital markets firms should reexamine their crisis readiness, run tests, reexamine governance, and streamline decision-making and communication approaches. |

| Financial institutions have already taken a number of actions, but they may need to do more as the situation evolves. | How is the playbook for pandemics being updated as a result of unfolding events? | Determine what constitutes a proportionate response and encourage decisive action. | |

| What is the best way to determine the appropriate organizational response? | Playbooks already in place should be reviewed with necessary updates made to ensure organizational resilience. | ||

| How is the COVID-19 task force empowered? | Activation and deactivation triggers should be determined and continuity procedures reviewed. | ||

| The COVID-19 task force should be empowered to make decisions at both the global and local level, where applicable. The task force should be connected to and actively align its priorities with the CEO and board of directors. | |||

| Ensure empathetic responses to employees’ situations. | |||

| Communications | Communicating regularly with various stakeholders may continue to grow in importance. | How quickly can tailored communications be initiated with employees, customers, business partners, vendors, investors, regulators, etc., across offices, regions, and businesses, nationally and internationally? | Appropriate communication mechanisms tailored to different audiences should be prepared and tested. |

| Monitoring and review | The evolving developments regarding COVID-19 call for institutions to be agile/flexible. | Is scenario planning being done proactively? | Consider testing preparedness using interactive, scalable crisis exercises. |

| Are plans, policies, and procedures adaptive and flexible, and are they in line with national and local regulations and laws? | Actively monitor results and iterate as needed. | ||

| Is there a clear governance mechanism in place if the pandemic worsens? | Ensure that policies, procedures, and plans are in line with current local, state, and national laws, and any updates. These may include Leave of Absence (LOA), the Americans with Disabilities Act (ADA), the Family and Medical Leave Act (FMLA), the right to privacy, Occupational Safety and Health Administration regulations, National Labor Relations Act regulations, state safe environment laws, and discrimination laws. | ||

| Flex and remote work | As the situation continues to rapidly develop, alternate work arrangements are being implemented to limit the spread of the illness and ensure employee safety. | What flex and remote work policies are currently in place? | Based on the most up-to-date information, whenever possible, consider instituting work-from-home or flexible/rotating schedules. |

| For those with business models that preclude remote work arrangements, have flexible or rotating schedules been considered? | Ensure that technology options are in place to connect employees working remotely without compromising access/data security. | ||

| What are the risks associated with remote work? | |||

| Do organizations have tools and solutions to implement remote work? | |||

| Infrastructure/capacity | To enable flexible or remote work, organizations need to have the right infrastructure in place. | Is the necessary technical infrastructure in place to support alternate work arrangements, and how secure is it? | Review infrastructure that is currently in place, such as VPN connections, security tokens, bandwidth, and laptops. |

| Which existing tools could enable remote work collaboration? | |||

| Quality of work/productivity and employee well-being | The spread of COVID-19 could result in further work disruptions and delays, as governments, public transportation agencies, and educational institutions adjust their practices and policies. | How can organizations ensure that the quality of work and productivity remain high? | Prioritize which projects, workflows, and deliverables matter most, and communicate these clearly to employees. |

| How can organizations ensure they are nimble enough to adjust workflows if work needs to be reprioritized? | Provide appropriate tools and employ relevant tactics to maintain quality of work/productivity. | ||

| How can they modify plans to sustain employee engagement, well-being, and motivation? | |||

| Offshore delivery centers | Many organizations have offshore delivery centers, from IT services to call centers. | How can firms ensure delivery from offshore centers with minimal disruption? | Maintain frequent communication with offshore delivery centers and develop appropriate contingency plans if they are not yet in place. |

| Are there alternate/secondary delivery options in case the offshore delivery center is compromised? | Consider testing alternate work arrangements from offshore delivery centers to determine if service performance is affected in any way. | ||

| What is the business continuity plan for offshore centers? | Find alternate venues for service delivery if a particular center experiences an operational disruption. | ||

| Global operations | Each market could experience varying levels of stress and disruption. | How efficiently can critical activities be rerouted to local offices around the world? | Identify which operations and/or activities can be rerouted or sent to other global offices, or even third parties. |

| How resilient are global entities/offices operationally? | |||

| Digital/IT infrastructure | There may be increased demands on organizations’ digital infrastructure to replace manual operations. | Are digital banking, payments, trading platforms, and other systems robust and resilient enough to handle disruption? | Consider testing and planning for alternate capacity to process and continue to deliver services whenever possible. |

| Legal matters | At any institution, legal contracts that deal with labor, clients, counterparties, and/or vendors, may be at risk. | Are there any work/projects/deliverables that are at risk of missing deadlines or not being fulfilled? | Confirm if existing contracts include force majeure clauses. |

| What are the third-party and client implications? | Contracts or statements of work should be revisited or amended, whenever possible. | ||

| Tax, financial, and regulatory compliance reporting | Looming deadlines for tax filings, financial reporting, and regulatory compliance reporting may be jeopardized due to operational disruptions. | How would changes to operations and alternate work arrangements or reduced capacity affect tax filings, financial reporting, and regulatory compliance reporting? | Be realistic about meeting deadlines. Proactively communicate with tax authorities and regulators, such as the SEC or OCC in the United States, or the ECB, Bank of England, and local tax authorities in Europe. |

| There may be tax implications as employees work remotely, potentially in different cities or states. | What are the tax implications from work being done remotely? What would the potential losses be for tax-loss carry forwards? | Gain an understanding of the tax implications. | |

Acknowledgments

The authors, Val Srinivas, Jan-Thomas Schoeps, and Tiffany Ramsay, wish to thank Vik Bhat, Gopi Billa, Craig Brown, Joan Cheney, Margaret Doyle, Marjorie Forestal, Sebastian Gores, Ed Hida, Mike Jamroz, David Myers David Strachan, Troy Vollertsen, and the many others who provided insights and perspectives in the development of this article.

Endnotes

- Daniel Bachman, The economic impact of COVID-19 (novel coronavirus), Deloitte Insights, March 3, 2020. View in article

- International Monetary Fund, “IMF data mapper: Real GDP growth (October 2019),” 2019. View in article

- Federal Reserve Bank of St. Louis, “10-Year Treasury constant maturity rate,” accessed March 9, 2020. View in article

- Mohamed El-Erian, “Coronavirus raises the risk of real trouble in corporate bonds,” Financial Times, March 3, 2020. View in article

- Jeanna Smialek, “Fed official says central bankers are aligned in coronavirus response,” New York Times, March 5, 2020. View in article

- Federal Reserve Bank of St. Louis, “Overnight repurchase agreements: Treasury Securities purchased by the Federal Reserve in the temporary open market operations,” accessed March 9, 2020. View in article

- Robin Harding and Hudson Lockett, “BoJ spurs Asia markets rebound with vow to fight coronavirus,” Financial Times, March 2, 2020. View in article

- Ibid. View in article

- Bank of England, “Governor statement to Treasury Select Committee, on behalf of the FPC, MPC and PRC,” March 3, 2020. View in article

- Rachel Louise Ensign, Liz Hoffman, and Justin Baer, “Wall Street scrambles to harden virus defenses,” Wall Street Journal, March 1, 2020. View in article

- Renae Merle, “Big banks want regulation eased because of coronavirus. Experts call it opportunistic,” Washington Post, March 3, 2020. View in article

- US Securities and Exchange Commission, “SEC provides conditional regulatory relief and assistance for companies affected by the coronavirus disease 2019 (COVID-19),” March 4, 2020. View in article

- Elliot Wilson, “Coronavirus is cost and opportunity for Asia’s banks,” Euromoney, March 2, 2020. View in article