Article

2018 Insurance Industry Outlook

Shifting strategies to compete in a cutting-edge future

As technology innovation, higher customer expectations and disruptive newcomers redefine the marketplace, insurers remain focused on growing top-line sales, bottom-line profitability, addressing challenges, and competing in a dynamic industry. Our 2018 Insurance Industry Outlook pinpoints key opportunities and threats that should demand attention from insurers over the next 12-to-18 months.

Explore Content

- Setting the agenda

- Where do insurers stand as they enter 2018?

- Growth options: Insurers can capitalize on connectivity, digitalization

- Insurers deal with a shifting landscape

- Final word: Carriers start to flex their muscles in the new InsurTech ecosystem

Setting the agenda

Insurance company leaders have a lot on their plates. Political and regulatory upheavals around the world are changing some of the ground rules about how carriers may operate. An accelerating evolution in the way business is conducted is being driven by innovation and higher customer expectations, while disruptive newcomers are looking to take market share from incumbent insurers. In particular, carriers have been racing to keep up with insurance technology development, as we recently documented in Fintech by the numbers, which analyzes startup financing activity and trends.

However, in preparing our annual insurance outlook, we recognize that most insurers remain focused on two overarching goals: growing top-line sales while bolstering bottom-line profitability. Standing in the way of insurers achieving these objectives are a wide range of challenges. Not all of them are within the industry’s control, such as rising interest rates and catastrophe losses. But how effectively insurers anticipate, prepare, and adapt to their shifting circumstances, both strategically and operationally, is well within their control, and can help differentiate them in the market.

In this report we pinpoint key opportunities and threats that should demand attention from insurers over the next 12-18 months. We’ll look at why it could be important for companies to address each of these issues sooner rather than later, include examples of how these developments seem to be already impacting the market, and offer suggestions on what could be done to respond proactively.

As always, regulation and compliance requirements are important and seem ever-changing, and this report will touch on some of the broader implications likely to result from the most significant shifts in policy. The Deloitte Center for Regulatory Strategies is publishing a companion paper dealing with these issues in greater detail, leveraging the expertise of our insurance practice and research team.

Our outlook is based on the firsthand experience and insights of many of Deloitte’s subject matter specialists, supplemented with research and analysis by the Deloitte Center for Financial Services. We hope you find it thought-provoking as you contemplate your strategic priorities and adjust your agenda for the year ahead. Please share your feedback or questions with us. We would welcome the opportunity to discuss our findings directly with you and your team.

Gary Shaw, vice chairman, US insurance leader, Deloitte LLP

Jim Eckenrode, managing director, Deloitte Center for Financial Services, Deloitte Services LP

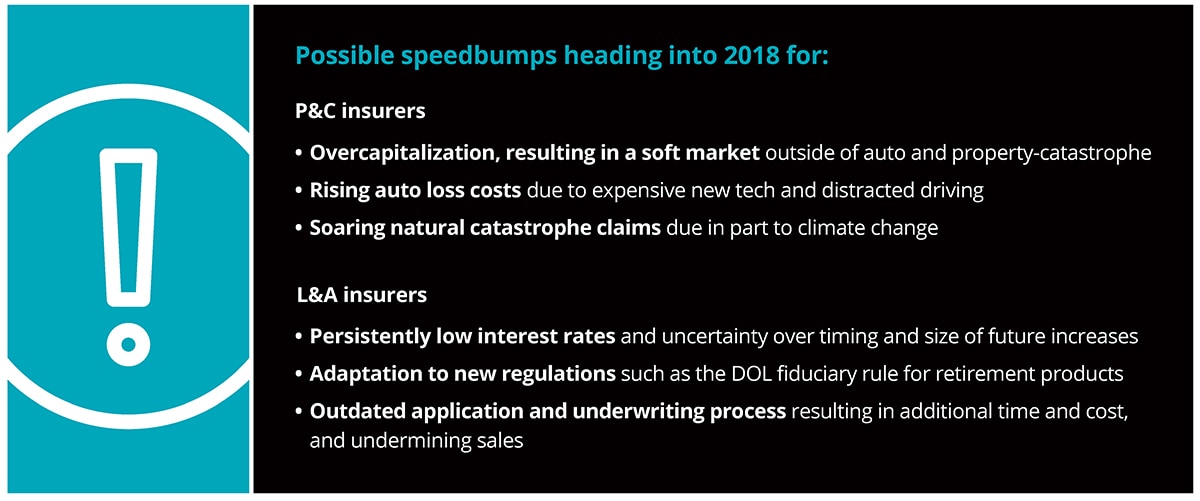

Where do insurers stand as they enter 2018?

Insurer hopes for accelerated growth and improved bottom-line profitability were tempered throughout 2017 by the emergence of major speed bumps, both natural and man-made, although there seems to be cautious optimism for improving conditions in the year ahead.

US property-casualty (P&C) insurers saw underwriting losses more than double, to $5.1 billion, for the first half of 2017 compared with the year before—an even more dramatic downturn when you consider the industry was in the black on underwriting by $3.1 billion during the same period two years ago.1 Soaring loss costs, led by higher catastrophe and auto claims, drove net income down 29 percent in the first half,2 and this was before huge third-quarter disaster claims from Hurricanes Harvey, Irma, and Maria. These storms reverberated globally, particularly within the reinsurance sector, as did claims from other massive natural disasters outside the United States, most notably September’s earthquake in Mexico.

On the other hand, a soft market beyond auto and property-catastrophe lines continues to prevail, with global insurance renewal rates falling for the seventeenth consecutive period in the second quarter of 2017.3 This appears mainly due to an overabundance of capital, particularly in the US market, with industry surplus as of June 30 at an all-time high of $704 billion.4 Even record storm losses would be unlikely to put more than a temporary dent in those reserves, most likely making recent hurricanes earnings events rather than serious capital concerns for most primary insurers—although reinsurers and those issuing insurance-linked securities may be harder-hit over the long term as mounting catastrophe claims are settled.

On the life insurance and annuity (L&A) side of the business, most carriers seemed to enter 2017 expecting small, but steady US interest-rate increases to put their portfolios on a more solid foundation. However, those expectations likely quickly abated, given the economic headwinds keeping the Federal Reserve from taking more aggressive action, thus leaving rates at historically low levels and undermining industry profitability. Stubbornly low fixed-investment yields are prompting L&A writers to cut the crediting rates offered to policyholders.5

The MIB Life Index, which tends to give a strong indication of individually underwritten life insurance activity, fell 3.2 percent the first half of 2017, while activity in the critical 45-59 target age segment was down 5.5 percent.6 Meanwhile, revenue from annuity sales was down 18 percent in the first quarter of 2017, according to the Insured Retirement Institute.7

Life insurance and annuities could be a harder sell in the United States in 2018, given the potential impact of new fiduciary standards set by the US Department of Labor on the sale of retirement-related products. While the final form of the fiduciary rule is still being debated following the change in US presidential administrations, many insurers have already made substantial changes in their business model to accommodate the regulation, and most are unlikely to turn back the clock at this point, instead adapting to their new operating environment (see “L&A insurers in a ‘hurry up and wait’ position over DOL fiduciary rule”).

A similar challenge faces carriers in the United Kingdom, where “pension freedom” was established two years ago, allowing pensioners to draw down their retirement accounts at will. Before the rule change, most retirees had purchased annuities offering regular payments for life. Annuity sales have plummeted 91 percent since "pension freedom.”8

Growth prospects on the horizon

Looking ahead and abroad, emerging markets— particularly China—appear to be a better bet for rapid growth, at least on a percentage basis, especially for P&C insurers. A report by Swiss Re’s sigma research unit found that emerging market P&C premiums rose 9.6 percent in 2016, compared with overall global growth of 3.7 percent—with China, now the world’s third-largest insurance market, seeing non-life premiums soar 20 percent.9

In addition to expected hikes in property-catastrophe premiums, particularly for reinsurance, look for a large share of US P&C premium gains to be generated by higher auto insurance rates (which were already rising in 2017 due to worsening loss frequency and severity). Even with price increases, however, profitability could remain elusive, given the multitude of emerging risk factors confronting auto carriers, such as the rise in distracted driving and the proliferation of more expensive sensor-laden vehicles. Recent disaster losses are exacerbating this trend, as Hurricane Harvey is believed to have damaged more vehicles than any storm in history—perhaps as many as one million.10

On the L&A side, insurers can still recover their footing in 2018 if interest rates are raised on a more regular basis. There are already some positive signs. The gap is widening between what consumers can earn on fixed annuity contracts and bank certificates of deposit, with annuity holders having the added benefit of tax-deferred status on gains.11 And while the life policy count fell by 4 percent in the second quarter of 2017 and 3 percent in the first half, new annualized premiums were actually up 4 percent in the first half.12

The individual market is just one channel where L&A insurers can seek growth. Group life sales—which have the advantage of guaranteed issue and little, if any, direct contact with the insured—have surpassed individual policy purchases for the first time.13

There remains plenty of room for expansion across the board. While nearly five million more US households had life insurance as of 2016 than in 2010, those gains were fueled by population growth rather than higher market penetration, which remains at its record low of just 30 percent.14 However, to accelerate growth, L&A insurers should consider simplifying their products and streamlining their application process to make policies easier to understand, underwrite, and purchase.

In short, insurers can take advantage of growth opportunities, operational improvement, and expense reduction in 2018 if they can overcome a host of internal and external obstacles standing in their way. The following are among the options they should consider to potentially improve their top and bottom lines, as well as stay ahead of the competition in the year ahead.

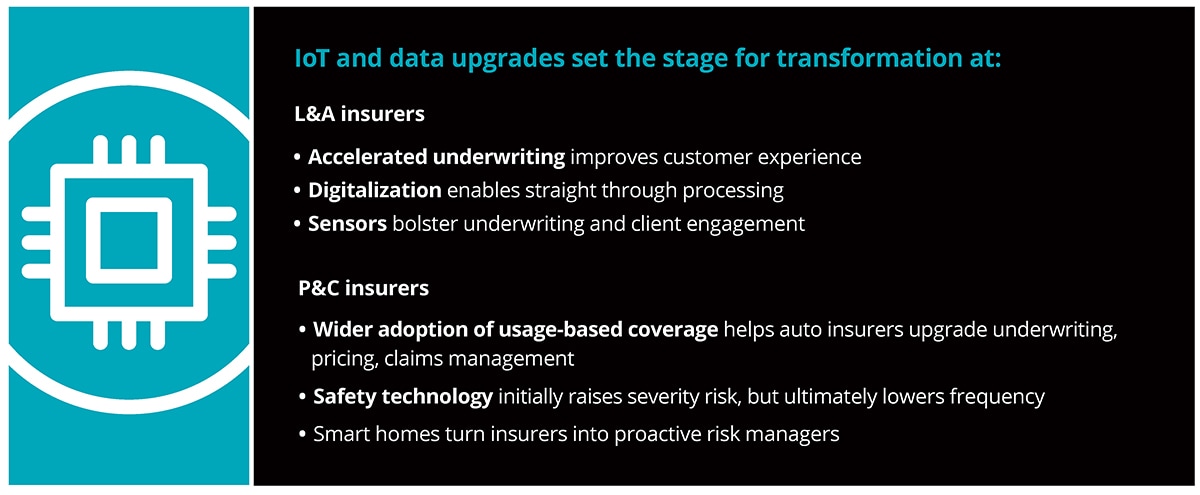

Growth options: Insurers can capitalize on connectivity, digitalization

Life and annuity carriers look to break the mold on underwriting, distribution

Why should this be high on insurer agendas?

An age-old enigma is how to overcome buyer reluctance to purchase life and annuity products. The stage is seemingly set, with nearly half of the US population uninsured or underinsured,15 and a similar percentage of US families having no retirement account savings,16 yet sales of L&A products remain relatively sluggish.

Historically low interest rates may have undermined the take-up of rate-sensitive L&A products, and stymied company profitability for the last several years. While the likelihood of additional interest rate increases in 2018 should help, macroeconomic factors alone are unlikely to substantially boost penetration rates absent more fundamental business-model changes.

As digital capabilities infiltrate nearly every industry, there appears to be a big opportunity for L&A companies to transform their business model. In fact, unless the industry commits to integrating transformative technologies more rapidly into their operations, L&A companies could risk not only continued stagnation, but potential leakage to InsurTech innovators as well.

What is changing?

Several insurers are experimenting with connectivity and advanced analytics to narrow the life application-to-closing process from weeks to minutes, lowering onboarding costs, and minimizing the consumer dropout rate. Accelerated underwriting metrics, based on digitally available medical data, drug prescription information, and potentially even facial analytics technology can be used to estimate an applicant’s life expectancy and eliminate traditional medical tests.

Digitalization of underwriting can also enable online distribution capabilities, allowing insurers to cast their nets wider and embrace younger demographics that often prefer a more virtual experience. Underwriting digitalization also could remove a barrier to purchase with those of all ages discouraged by the long and complicated life insurance application process. Indeed, Deloitte’s work on life insurance underwriting suggests that the likelihood of prospects buying a policy once they apply increases from about 70 percent to nearly 90 percent as the underwriting and application process gets closer to real time.17

Beyond underwriting, distribution also seems ripe for digitalization. In one example, Abaris, an InsurTech startup, launched a direct-to-consumer online platform for deferred income annuities. On the life insurance side, Ladder, another InsurTech startup, is now offering direct-to-consumer policies within minutes, particularly targeting younger consumers who may often avoid purchasing such coverage, given the time it traditionally takes to do so. Moreover, Ladder does not charge annual policy fees or employ commissioned agents, potentially gaining a competitive advantage relative to incumbents.18 Then there is the Swedish InsurTech startup, Bima, which is offering accident and life micro-insurance to low-income consumers in developing regions of Africa, Asia, and Latin America via prepaid credit on their mobile devices.19 The game-changing potential of such automated lead-generation and direct-sales platforms could challenge L&A providers to modernize their business models to maintain, let alone expand, their client base.

In addition, by connecting with clients via sensor devices, insurers can build more regular and meaningful client engagement. For example, insurers can harness data from devices that monitor vital signs, activity, nutrient consumption, and sleep patterns for more precise underwriting and pricing while offering value-added fitness and lifestyle feedback. John Hancock’s Vitality program is one such initiative, offering policyholders premium savings and rewards for completing health and fitness related activities, tracked by smartphone apps and fitness devices.20

What should insurers do?

L&A insurers should embed digital technology across their organizations—as part of an offensive strategy to expand their market share and defensive measure to fend off potential competition from nontraditional InsurTech companies. By harnessing and harvesting big data sources—perhaps with the help of third-party managed services specialists—insurers can streamline their often cumbersome and expensive operating models while both improving customer experience and lowering costs.

Insurers may also want to consider teaming up with, investing in, and/or purchasing InsurTechs not just to expand digital capabilities, but to inject a more innovative element into their culture, and to accelerate the disruption of more time-consuming and expensive standard business processes.

For further consideration

L&A insurers in a ‘hurry up and wait’ position over DOL fiduciary rule

Much uncertainty remains over compliance demands under the US Department of Labor Fiduciary Duty Rule for the sale of retirement related products. However, most insurers didn’t wait for fiduciary rule challenges to play out before repositioning themselves to comply. Nearly all of the 21 members of the Securities Industry and Financial Markets Association (SIFMA) surveyed by Deloitte reported making changes to retirement products in response to the fiduciary rule, including limiting or eliminating asset classes and certain product structures.a The study also indicated an accelerating shift of retirement assets into fee-based or advisory programs rather than commission-based sales.a

Adding to the confusion is that a handful of individual states have also begun imposing their own versions of a fiduciary standard, while others are considering similar action.b Outside the United States, United Kingdom (UK) regulators are also examining how annuities are sold.c

Some SIFMA members cited “significant operational disruption and increased costs” for compliance, and indicated they expected “additional real costs as well as ongoing opportunity costs,”a even before it was announced that implementation of some of the fiduciary rule’s components would be delayed for further review until July 2019.

In the interim, those insurers that have already made substantial moves—such as changes in their product lines, compensation structures, or distribution systems—will need to solidify their place in the new business environment they’ve chosen. Others may decide to put off some changes they had planned for January 2018, such as “levelizing” commissions or cutting their product inventory.a This issue will likely remain in flux as carriers get accustomed to the changes they’ve implemented while trying to figure out what more they need to do to meet a moving target.

a “The DOL Fiduciary Rule: A study on how financial institutions have responded and the resulting impacts on retirement investors,” Deloitte Consulting LLP, Aug. 9, 2017.

b Lisa Beilfuss, “States to Trump: Leave Retirement Rule Intact or We’ll Act,” The Wall Street Journal, Sept. 12, 2017.

c Josephine Cumbo, “Savers not given all annuity options, regulator warns,” Financial Times, July 15, 2016.

Tech upgrades drive added value, new risks for auto insurers

Why should this be high on insurer agendas?

The conventional wisdom among stakeholders in the emerging mobility ecosystem is that one day universal deployment of autonomous vehicles could reduce the likelihood of auto accidents to near zero. In the meantime, a variety of factors—including record numbers of miles driven in an improving economy, and a proliferation of expensive, embedded technology in vehicles—seem to have created a perfect storm for higher frequency and severity of auto insurance claims (figure 1).21

Many auto insurers could continue to struggle to avoid red ink in the coming year, as loss costs mount from a rise in accident-generated medical expenses, escalating repair charges (with damage for technology in sensor equipped vehicles five times higher than traditional vehicles22), technology related driver distraction, and catastrophe losses. According to James Lynch, chief actuary for the Insurance Information Institute, “If the cost of claims continues to rise, rate increases are inevitable.”

Figure 1: Auto claim costs on the rise

What is changing?

In an increasingly crowded and commoditized market undermined by minimal customer loyalty, many auto insurers are looking to differentiate their value beyond price to maintain or raise customer satisfaction. Otherwise, they could risk declining retention. The real-time data furnished by auto telematics offers a way for insurers to become an integral daily influence for connected policyholders through offers of frequent, mutually beneficial value-added services to establish brand stickiness. This doesn’t seem to be a pipe dream, as price satisfaction scores are higher among customers who participate in auto telematics programs, even when they have experienced premium rate increases.23

In addition to telematic driving monitors, a variety of safety sensors are slowly but surely being introduced to consumers via new car sales, with the eventual goal of full vehicle autonomy. Intuitively, this safety technology should reduce crashes despite the recent increase in miles driven. However, estimates by some insurers are that 25-to-50 percent of vehicles would have to be equipped with forward-collision prevention systems before crash rates decline sufficiently to offset higher repair costs associated with damaged sensors and computer systems. We have a ways to go to reach that tipping point, as only 14 percent of 2016 car models in the United States are equipped with technology to mitigate accidents.24

What should insurers do?

As rising loss costs pressure carriers to keep raising rates, insurers that deliver more value for the premiums charged can position themselves as market leaders and attract higher-quality risks. Telematics seems the most obvious first step. Nearly 100 million drivers globally are expected to have usage-based insurance (UBI) policies by 2020, with Italy, the United Kingdom, and the United States leading the way.25 Those insurers still on the sideline when it comes to using telematics should get in the game before more proactive competitors co-opt them.

For such programs to translate into greater bottom-line growth, UBI carriers should leverage their telematic data to price policyholders more effectively. This would require development of more predictive underwriting models based on actual driving performance, as opposed to many of the proxy data sources used by traditional auto policies. Many are also making arrangements with third parties to provide added value to policyholders.26 Progressive Insurance, Insure The Box Ltd., MAPFRE, and Metromile Inc. are among those that have formed several alliances to expand their markets and product lines.27

In the meantime, insurers can partially compensate for higher severity costs with the safety benefits provided by embedded sensors, which can also be used as marketing tools. Liberty Mutual is offering discounts to customers who drive Volvos with active or passive advanced safety features, not only to encourage consumer adoption, but also to collect valuable data to evaluate more accurately the impact of these components on accident frequency and severity.28

Insurers should also pay close attention to the emergence of entirely new competitors. More auto makers producing “smart” cars may decide to include insurance in the price of their vehicles, following the example of Tesla, which has been selling auto coverage with its cars in Asia and may one day include insurance in the final sticker price worldwide.

IoT shifts value proposition for homeowners’ carriers

Why should this be high on insurer agendas?

Internet of Things (IoT) connectivity is surging and the technology’s potential to reshape the way homeowners insurers assess, price, and limit risks appears quite promising. Eighty-million smart home devices were delivered globally in 2016, and expectations of a compound annual growth rate of 60 percent could result in over 600 million such devices in use by 2021 (figure 2).29

This also presents a unique opportunity for insurers to transform the insurer/customer dynamic from a defensive to an offensive posture, by helping policyholders prevent losses and driving down claims costs.

What is changing?

Smart home sensors could potentially facilitate an insurance revolution. For example, sensors can monitor indicators of possible problems—such as wall strength, pipe or plumbing fissures, faulty wiring, or even home invaders. Alerts can be sent to homeowners and insurers, as well as trigger automatic shut-off valves and notifications to local service providers who can preemptively intervene prior to major incidents. For example, American Family Insurance struck a deal with Ring to offer policyholders discounts if they use Ring Video Doorbells. The device offers safety-connected technology that streams video to a homeowner’s mobile device to identify the person at their door, and even allows homeowners to virtually answer from anywhere using their smartphones.30 In addition, Ring offers to cover an insured’s deductible if their home is burglarized.31 With wider deployment of such InsurTech safeguards, carriers may receive fewer and less-severe claims and be able to gather data for more personalized and profitable pricing.

Providing loss-prevention capabilities as well as after-the-fact reimbursement will likely also enhance client perception of an insurer’s tangible value, which can strengthen retention. Real-time connectivity could also fuel a surge in customer touchpoints to reinforce relationships, an opportunity long elusive to insurers.

However, as with many connectivity opportunities that oblige policyholders to share data, there appears to be some initial reluctance. Consumer hesitance may be related to how smart devices might be tapped to gather more private, home-life-related information, as well as what assessments might be made by insurers on the basis of that data.

What should insurers do?

While 24/7 connectivity may be an insurer’s Holy Grail, facilitating both higher profitability and stronger customer relationships in the long term, to get to that point more consumers will likely need to be convinced of the value and ease of opting into such invasive monitoring programs. Transparency would be necessary so policyholders understand exactly what type of data are collected and how the company plans to use the information. Effective marketing to highlight opportunities for loss prevention, education on product benefits and use, and incentives for reducing risk are additional strategies insurers can deploy.

Insurers would also need to team with manufacturers and service providers to deliver and capitalize on many of these potential capabilities. Connectivity execution may also require more nimble data management and warehousing, as well as increasingly advanced underwriting models to reflect the additional risk parameters. Insurers may want to accelerate this transition by subsidizing installation of the sensors needed to prevent home disasters. While this may initially be expensive, smart homes likely offer returns on multiple fronts that could offset such upfront investments.

Insurers should also try to stay ahead of security and privacy regulations prompted by increased data sharing. As an example, for companies that store data on residents of the European Union (EU)—even those based outside the region—the General Data Protection Regulation (GDPR), which takes effect in May 2018, will require higher levels of data breach reporting and may compel an increase in cyber insurance coverage for those impacted by the legislation.32

Insurers deal with a shifting landscape

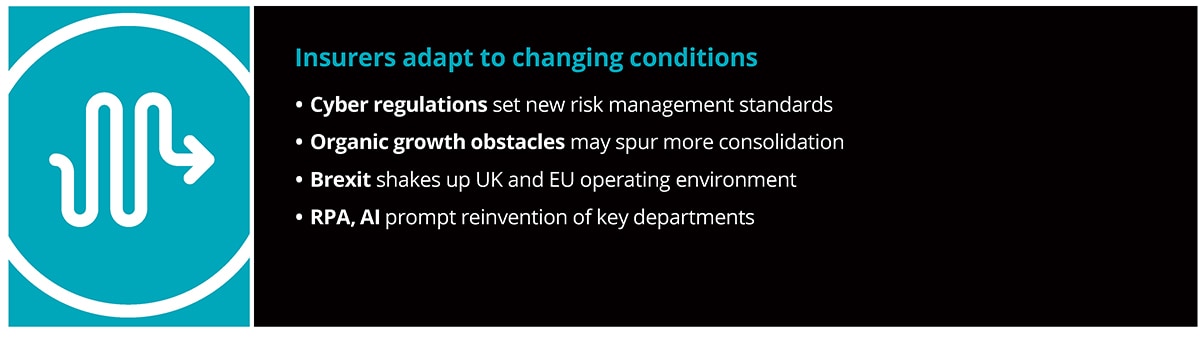

Cyber risk regulations set new standards for insurers

Why should this be high on insurer agendas?

While more carriers look to break into the cyber insurance market (see “For further consideration”), or expand what they’re already writing, data-rich financial services companies—including insurers—themselves remain a prime target of cyberattacks. Despite extensive mitigation efforts, financial services still leads the pack in terms of average annualized cost of cybercrime by industry sector at $18.28 billion—6 percent higher than second-ranked utilities and energy, and 26 percent more than aerospace and defense companies, which rank third (figure 3).33 As a result, there has been increasing pressure from insurance company officers and directors to enhance cyber security, vigilance, and resilience.

Until recently, insurers have been relatively free to follow their own path and timeline in their cyber risk management efforts. However, many carriers now have to cope with new loss control and reporting standards laid down by regulators that could increase compliance budgets for those that haven’t already taken such steps.

Insurer spending on cognitive/artificial intelligence technologies is expected to rise 48 percent globally on a compound annual growth basis over five years, reaching $1.4 billion by 2021.

What is changing?

Front and center for US insurers are the regulations that went into effect on Aug. 28, 2017, from the New York State Department of Financial Services. Insurers under New York’s jurisdiction must now appoint a chief information security officer (CISO), have a written data security policy approved by its board or a senior officer, and begin reporting cyber-related events.34

A model law very similar to New York’s has been approved by the National Association of Insurance Commissioners, setting the stage for a likely nationwide rollout.35 Globally, as noted earlier, the EU’s GDPR will take effect in May 2018, while the International Association of Insurance Supervisors is studying regulatory approaches in its member countries with an eye towards setting worldwide cybersecurity standards.

While most insurers have already taken significant steps to fortify their defense systems and limit damages if and when breaches occur, research by the Deloitte Center for Financial Services found a wide disparity of cyber risk management maturity levels and capabilities within the industry.36 New regulations seem to have been designed to establish uniformity and minimum standards, increase transparency, provide accountability, and protect policyholders from privacy violations.

What should insurers do?

Insurers should account for multiplying compliance demands, domestically and globally, which could be especially challenging for midsize and smaller companies that lack in-house cyber talent, expertise, and resources. These new rules will likely take cyber risk management beyond the CISO’s purview and put the chief compliance officer on the hot seat as well.

Finding enough qualified talent to handle cyber exposures seems to have been as daunting for many carriers as it has for their commercial policyholders. Similar to the industries they cover, insurers will likely need to bolster their in-house capabilities with outside talent and managed services, particularly loss control specialists to enhance risk management, recovery, and compliance programs.

For further consideration

Carriers have yet to crack the code on cyber insurance

The market for cyber insurance has persistently been slow to develop, leaving the bulk of companies without coverage or underinsured, and denying the P&C industry what is likely to be its biggest organic growth opportunity. A recent survey by the Council of Insurance Agents & Brokers found that only one third of their members’ clients have bought cyber coverage of some sort,d while a global study by the Ponemon Institute revealed that companies have only insured 15 percent of the potential loss to their information assets.e

A big part of the problem has been the difficulty of underwriting a constantly evolving risk, along with the dearth of historical data. To capitalize on the growing demand for coverage and to avoid losing business to alternative risk-transfer vehicles, such as cyber bonds, insurers might need to underwrite based on each applicant’s risk management maturity, perhaps confirmed for bigger accounts by independent third-party assessments.

Developing a cyber resumé template for smaller prospects on a mass scale could help insurers establish standard, preferred, and substandard risks. To close the information gap, the industry could press for greater sharing of anonymous, aggregated loss data, an advantage they already enjoy with auto and workers’ compensation claims.

d “Cyber Insurance Market Watch Survey,” Council of Insurance Agents and Brokers, May 2017.

e “2017 Global Cyber Risk Transfer Comparison Report,” Ponemon Institute/Aon Risk Solutions, April 2017.

Tech objectives, macroeconomic factors should reboot M&A activity

Why should this be high on insurer agendas?

Investor uncertainty leading up to and following the 2016 US election seemed to significantly restrain merger and acquisition (M&A) activity through the first half of 2017 as insurers waited to see how policy and the economy would play out under the incoming administration. Improved insurer stock prices as well as a scarcity of targets on the market for potential sale were additional factors that could have put a damper on the M&A market. As a result, the number of insurer transactions in the first half was down 5 percent from the same period a year earlier, although aggregate transaction size was substantially larger.37

That said, organic growth remains elusive and a robust US stock market suggests share buybacks may not be the most productive use of the industry’s excess capital, leaving crystal-ball gazers predicting a more positive outlook for insurance industry M&A in 2018.

What is changing?

M&A deals will likely wear a number of faces over the near term, from global investments and innovative modernization to divestiture of non-core assets and run-off business.

The US insurance market remains the largest globally in terms of premium volume, and on a pure premium-dollar basis still offers the most growth potential and economic stability. However, breaking into the US market can be difficult, given high valuations, which are often hard for many foreign acquirers to justify. As a result sales of US insurers to buyers in Canada, Europe, and Latin America will likely be few in the near-term. In Asia, the formerly robust Chinese investment activity in the United States has also waned, given a Chinese regulatory clampdown on speculation by insurers and new limits on outbound capital flows.38 However, the Japanese continue to pursue foreign deals to seek growth outside their own stagnant insurance market.

One potential M&A growth area is being spurred by digitalization, with insurers seeking to enhance distribution, customer experience, data collection, advanced analytics, and operational efficiency by homing in on InsurTech investment and acquisition targets. Although outright purchases of InsurTechs are still relatively few to date, such acquisitions through the first nine months of 2017 are already nearly twice that of the high point in 2014, with a full quarter remaining (figure 4).39 Looking ahead, nearly half of global insurers recently surveyed expect to make deals over the next three years to acquire new technologies, and 14 percent of those expect to make more than one acquisition.40

In addition, slowing of loss reserve releases across the industry will likely drive divestiture of non-core assets, as well as a run-off of some long-tail legacy liabilities on insurers’ books. This could encourage redeployment of capital into higher return options.

What should insurers do?

As stakeholders seek to make productive use of excess capital and counter stagnant organic growth prospects, M&A could become an increasingly viable means to those ends. US insurers may see growing interest from buyers looking to broaden their global footprint and increase scale, allowing US sellers to divest non-core assets.

In addition, more insurers around the world are likely to be on the lookout to invest in and acquire InsurTechs to bolster their own capabilities and import a more innovative culture.

To fund investments for growth, insurers may consider unlocking capital that supports non-core assets or legacy liabilities. These transactions may be outright divestitures to free up funds, or an attempt to “clean up” underperforming parts of the business ahead of a sale to increase valuation and remove drag from non-core or run-off business.

For further consideration

Brexit spurs insurer adaptation even before separation terms are finalized

Brexit’s long-term impact on insurers doing business in the EU is still uncertain, partly because the details of the post-Brexit world remain unknown. Many companies have already taken steps to adapt, even as negotiations continue between the EU and the UK on separation terms.

The March 2019 Brexit deadline may not allow enough time for some insurers to fully transition their EU operations, but they need to set alternative plans in motion nonetheless. Among the significant issues still to be resolved are the free movement of talent between the EU and UK, as well as passporting rights, which allow companies based in one EU country to do business in all.

Some insurers already have or will soon need to relocate or bi-locate their offices, staking their ground within one of the remaining member EU states by opening up or even acquiring a new base in another EU jurisdiction, or utilizing alternative structures to enable them to continue easily serving the EU market.f Companies planning to enter the EU market that had intended having the UK as their base will also have to reconsider their options.

Fundamental decisions around target operating models, governance structures, and capital and liquidity requirements should be made as early as possible, as precursors to necessary discussions with regulators. Insurers without advanced contingency plans should be accelerating assessments of their options, while those with strategies already determined need to decide on an implementation schedule, especially involving the hiring and transfer of key talent.

As this situation plays out, there could be a renewed focus on the UK insurance market’s unique relationship with the United States, which was established long before the EU came into existence. The UK in general, and Lloyd’s in particular, is a key supplier of coverage for US risks, especially in the excess and surplus lines and specialty markets, and Brexit won’t change that.

f Reuters, “Factbox: Impact on Insurers From Britain’s Vote to Leave the EU,” New York Times, September 11, 2017.

Robotics, artificial intelligence help insurers do more with less

Why should this be high on insurer agendas?

As insurers continue to be challenged by rapidly evolving customer needs and expectations amid heightened competition, many have resorted to belt-tightening and “doing more with less” to shore up returns. However, as the pace of productivity improvements slows with existing staff and systems, many carriers are looking to boost their transformation efforts by integrating more advanced automation, fueled by software applications that run automated tasks, also known as “bots,” as well as machine-learning algorithms.

Robotic process automation (RPA) and cognitive intelligence (CI) technologies are fast-becoming a reality, given rapid increases in computing power and decreases in data storage costs.41 These options give insurers an opportunity not just to reduce expenses, but also to possibly reinvent how they conduct business.

What is changing?

RPA gives carriers the ability to automate mundane, box-checking-type tasks in underwriting, policy administration, and claims, potentially freeing up thousands of people hours. RPA solutions use bots to mimic the way individuals interact with applications and follow simple rules to make decisions and automate routine business processes, improving efficiency without the need of any fundamental process redesign.42 For example, about a third of the tasks in claims management typically deal with data entry and validation using multiple in-house and external data sources. A large insurer that automated these basic tasks realized a productivity gain of 68 percent, coupled with improved accuracy and compliance.43 Another major carrier utilized RPA to automatically aggregate 86 data points into a centralized document, leading to 75 percent faster adjudication of claims.44

CI goes one step further by providing insurers with tools to automate non-routine tasks requiring soft skills, such as intuition, creativity, and problem-solving. This is primarily driven by the refinement in several key CI technologies, such as handwriting recognition; image, audio, and video analytics; and natural language processing.

How are carriers employing these technologies? One P&C insurer built a cognitive virtual agent that could conduct a conversation with customers in natural language. With the automated ability to answer a wide variety of consumer questions while gathering information for a quote, the insurer realized a higher percentage of completed applications and increased online conversion rates, as well as an overall improved customer experience.45

These InsurTech solutions could eventually fundamentally alter existing in-house operations. Indeed, a report by the World Economic Forum, in collaboration with Deloitte, forecasts a potential future scenario where cognitive technologies are so pervasive that underwriting becomes much more automated than today, perhaps leading to the emergence of third-party underwriting specialty providers.46

In the meantime, cognitive technologies, combined with RPA and advanced analytics, can improve productivity of existing staff performing non-routine tasks—or could automate those tasks entirely.47 The potential benefits of RPA and CI go beyond cost reduction to offer decreased cycle times, flexibility and scalability, improved accuracy, and higher employee morale—at least among those who can make the transition.48

Insurer spending on cognitive/artificial intelligence technologies is expected to rise 48 percent globally on a compound annual growth basis over five years, reaching $1.4 billion by 2021 (figure 5).49 Spending on these InsurTech solutions is expected to increase by 50 percent for automated claims processing, 47 percent in fraud analysis and investigation, 42 percent for program advisors and recommendation systems, and 35 percent in threat intelligence and prevention systems.50

What should insurers do?

Insurers should start doing more with less by considering accelerating deployment of RPA and CI throughout their operations, automating routine, transactional, rules-based functions so that talent and capital may be repurposed for more complex tasks. The savings in time and money can be considerable. (For an example in claims, see “The proof is in the pudding on automation”.) Part of the planning for such a transformation is determining whether and how to reinvest expected savings, as well as redeploy displaced staff.

In terms of talent, RPA and CI initiatives will likely entail redesigning job descriptions and perhaps entire functions within the company, as well as retraining employees for higher-level duties requiring human judgment. Therefore, insurers should execute their automation strategy as part of a long-term talent transformation, ensure buy-in from all department leaders, and put in place a comprehensive change-management program.

For further consideration

The proof is in the pudding on automation

In a sluggish growth market, saving time and money will likely remain high on insurer agendas. To provide an idea of the potential savings offered by automation, we applied to the insurance industry a methodology created by the Deloitte Center for Government Insights.g

Consider the likely impact of automation on the claims function. RPA can cull through data faster and more thoroughly than staff can do on their own, while CI can help pick out anomalies and red flag possible frauds, releasing personnel to focus instead on particularly complicated or problematic situations.

While actual savings will depend upon many factors, some strategic and some operational, our preliminary analysis suggests that just in one type of occupation—claims adjusters, appraisers, examiners, and investigators—the US insurance industry could potentially free up between 54 million and 285 million hours of their workforce time annually, amounting to potential cost savings between $1.7 billion and $8.9 billion, within five to seven years, depending upon their level of investment.

Insurers will have the choice of cashing out savings from these efficiencies or reassigning the resources—both capital and personnel—to more value-added tasks that could improve revenue growth and customer satisfaction.

g Peter Viechnicki, William D. Eggers, “How much time and money can AI save government? Cognitive technologies could free up hundreds of millions of public sector worker hours,” Deloitte Center for Government Insights, Deloitte University Press, April 26, 2017.

Final word: Carriers start to flex their muscles in the new InsurTech ecosystem

At the recent InsurTech Connect forum, many of the themes we explore in this report were front and center—such as collaborating with innovative startups, capitalizing on connectivity, reinventing traditional operating and distribution models, accelerating globalization, and enhancing customer engagement. The event seemed to be a microcosm of the emerging insurance community—diverse and cutting-edge in terms of the skill sets, expectations, and personalities on display.

What was encouraging was that longtime incumbent insurers appeared to be interacting naturally, smoothly, and comfortably with the new breed of disruptors making names for themselves in the InsurTech business. Indeed, most insurers appear to be settling into the new ecosystem rather nicely. They seem to realize that while technology is a terrific enabler of progress, it is a means to an end rather than an end in itself.

While insurers should consider leveraging the latest technologies to improve their top and bottom lines, it is becoming clear they are not going to be run out of business by InsurTech disruptors anytime soon. Insurers still have a lot to offer in terms of capital, market reach, brand recognition, product design, and infrastructure. Most are recognizing InsurTechs as potential collaborators rather than competitors, and vice versa.

There may still be a bit of a frontier mentality about it all, as the industry sorts through which InsurTech solutions and startups are going to offer practical value and survive the inevitable shakeout. But the industry appears to have collectively caught its breath and is proceeding more confidently. Insurers seem to recognize that their future could increasingly be shaped not just by emerging technology products and services, but by the quality and capabilities of the tech-oriented people they have on staff and those with whom they collaborate from outside their organizations.

Most carriers are focusing on the problems to be solved or value to the consumer as the guiding principles for filtering through the seemingly endless possibilities being offered by InsurTechs. As the industry goes forward into this brave new world, insurers that make digital transformation not just a priority, but a continuous improvement process, are most likely to reenergize their cultures as well as grow their top and bottom lines.

Endnotes

1 “P/C Insurers Lost $5.1 Billion on Underwriting in First Half of 2017: A.M. Best,” Insurance Journal, August 29, 2017.

2 Ibid.

3 Marsh, “Global Insurance Market Index, Second Quarter 2017.”

4 “P/C Insurers Lost $5.1 Billion on Underwriting in First Half of 2017: A.M. Best,” Insurance Journal, August 29, 2017.

5 “Low Yields Squeeze Annuity Renewal Rates,” ThinkAdvisor.com, May 7, 2017.

6 Jay Cooper, “Ominous Signs Loom for Life Insurance Sales,” Life Annuity Specialist, July 21 2017.

7 “Q1 Annuity Sales Fell 18%: IRI,” ThinkAdvisor.com, June 6, 2017.

8 Teresa Hunter, “Using the pension freedoms? You could run out of money after 16 years,” The Telegraph, October 14, 2017.

9 Matthew Lerner, “Emerging markets drive property-casualty insurance growth,” Business Insurance, July 5, 2017.

10 Nathan Bomey and Aamer Madhani, “Harvey may have wrecked up to 1M cars and trucks,” USA Today, August 31, 2017.

11 “Annuities Now Pay More Than CDs,” ThinkAdvisor.com, September 8, 2017.

12 “Limra: US Individual Life Insurance New Premium Increases in First Half of 2017,” Limra press release, September 26, 2017.

13 Jay Cooper, “Employer-Based Life Insurance Sales Eclipse Individual Channels,” Life Annuity Specialist, September 8, 2017.

14 “Limra: Nearly 5 Million More US Households Have Life Insurance Coverage,” PR Newswire, September 29, 2016.

15 Ibid.

16 Kathleen Elkins, “Here’s how much Americans at every age have in their savings accounts,” CNBC, October 3, 2016.

17 Sam Friedman and Christine Chang, “Blockchain in insurance: Turning a buzzword into a breakthrough for health and life insurers,” Deloitte Center for Health Solutions/Deloitte Center for Financial Services, November 2016.

18 “New Insurtech Ladder is digitizing life insurance,” Business Insider, January 11, 2017.

19 Oscar Williams-Grut, “This Swedish startup brings insurance to 24 million people in the developing world through their mobiles,” Business Insider, October 22, 2016.

20 “Beyond Fintech: A Pragmatic Assessment of Disruptive Potential In Financial Services,” World Economic Forum, prepared in collaboration with Deloitte, August 2017.

21 ISO/PCI Fast Track data, provided by the Insurance Information Institute.

22 Christina Rogers, Leslie Scism, “Why Your Extra-Safe Car Costs More to Insure,” WSJ.com, April 3, 2017.

23 “J.D. Power 2017 U.S. Auto Insurance Satisfaction Study,” J.D. Power Studies.

24 Christina Rogers, Leslie Scism, “Why Your Extra-Safe Car Costs More to Insure,” WSJ.com, April 3, 2017.

25 Sarwant Singh, “The Future Of Car Insurance: Digital, Predictive And Usage-Based,” Forbes.com, February 24, 2017.

26 Ibid.

27 Lucy Hook, “Usage-based insurance market set to grow 36.4% globally by 2022,” insurancebusiness.com, December 7, 2016.

28 John Huetter, “Liberty Mutual adds up to 10% discount for Volvo safety tech in new partnership,” Repairer Driven News, April 6, 2017.

29 IHS Markit, “Rapid Expansion Projected for Smart Home Devices, IHS Markit Says,” September 2016.

30 Anthony R. O’Donnell, “American Family Engages Customers with Ring Video Doorbell Discount/Deduction Offering,” Insurance Innovation Reporter, November 20, 2015.

31 Press release, “Ring, American Family Insurance announce unique effort to help prevent home break-ins,” November 18, 2015.

32 Sarah Veysey, “Privacy rules may boost cyber purchases,” Business Insurance, October 2, 2017.

33 “2017 Cost of cybercrime study: Insights on the security investments that make a difference,” Independently conducted by Ponemon Institute and jointly developed by Accenture.

34 “New York’s Cybersecurity Regulation Compliance Requirements Go Into Effect,” Insurance Journal, August 29, 2017.

35 Gloria Gonzalez, “NAIC cyber security model law hews to New York state’s standard,” Business Insurance, September 4, 2017.

36 Sam Friedman, “Taking cyber risk management to the next level: Lessons learned from the front lines at financial institutions,” Deloitte University Press, June 22, 2016.

37 Deloitte analysis utilizing SNL Financial M&A database.

38 “$100 Billion Buying Spree by Chinese Insurers Fizzles in 2017,” Bloomberg News, February 22, 2017.

39 Data from Venture Scanner, analyzed by the Deloitte Center for Financial Services.

40 Louie Bacani, “Half of insurers to make M&A deals in next three years,” Insurance Business UK, January 2017.

41 Robert Dalton, Craig Mallow, Scott Kruglewicz, “Disruption ahead: Deloitte’s point of view on Watson,” Deloitte Consulting LLP, March 2015.

42 Anthony Abbattista, Tadd Morganti, Matt Soderberg, Jan Hejtmanek, “Automate this: A guide to robotic process automation,” Deloitte Consulting LLP, March 2017.

43 “Insurance in the Age of Intelligent Automation,” UiPath, August 2017.

44 Bill Galusha, “3 Real-World Ways Insurers Can Use Robotic Process Automation,” Kofax Advisor, March 2017.

45 “Rethinking insurance - How cognitive computing enhances engagement and efficiency,” IBM, November 2016.

46 “Beyond Fintech: A Pragmatic Assessment Of Disruptive Potential In Financial Services,” World Economic Forum in collaboration with Deloitte, August 2017.

47 Anthony Abbattista, Tadd Morganti, Matt Soderberg, Jan Hejtmanek, “Automate this: A guide to robotic process automation,” Deloitte Consulting LLP, March 2017.

48 Ibid.

49 IDC Worldwide Semiannual Cognitive Artificial Intelligence Systems Spending Guide, 2016H2, September 2017.

50 Ibid.