Predictions

2024 Global Life Sciences Sector Outlook

Published date: 9 July 2024

In this year, life sciences enterprises are paying particular attention to those more disruptive trends including increasing pricing pressures and changes in regulation, the acceleration of Generative AI (GenAI) adoption and impact, the geo-political environment, and as always, breakthrough science and outcomes.

In this outlook we examine what we see as disruptive trends like the impact of Gen-AI, the growth of the obesity market and treatment with GLP-1s, the IRA's first full year of impact as well as those trends which are more evolutionary in nature—like the continued complexity around navigating globalization in an uncertain geopolitical environment or the continue advancement of more personalized patient experiences.

Life sciences will need to continue relying on innovation, agility, and collaboration as they build on their strong commitment to bettering the lives of patients.

The following are the key findings from the report:

1. Value creation: M&A, partnerships, collaborations, new sources of capital, and shifting portfolios

Over the past year, life sciences and medical technology (medtech) companies have been managing inflation, rising interest rates (which can curtail access to capital), and slower economic growth. However, in 2024, inflation seems to be lessening, rates appear to be stabilizing, if not dropping, and growth is likely to be moderate—setting up a cautious, but still active mergers and acquisitions (M&A) and capital environment.

- Over the next year, some big pharma companies will continue to look to M&A to plug portfolio gaps as a result of loss of exclusivity (LoE) across various therapeutic areas. In particular, late-stage development/early-stage commercial assets—that could contribute material revenue growth over the next few years—are expected to be attractive targets.

- More sponsor-backed companies may decide to go private in 2024. PE continues its interest in life sciences suppliers, deploying more than US$10 billion in capital into contract development and manufacturing organizations (CDMOs).

- Life sciences dealmaking in the startup space continues to decelerate after experiencing record highs in 2021 but is still above pre-pandemic levels. Venture capital (VC) remains active and resilient compared to many other fields.

- LoE is also driving market leaders to various types of partnerships. Partnerships are a growing trend and may be an alternative to M&A to boost values in 2024.

- Tighter capital markets for small and midsize biotech companies in 2023 required many companies to find alternative ways of financing, including cutting costs and private investment. Biotech companies are increasingly looking at partnerships and other creative collaborations as an alternative, or precursor, to M&A.

2. Extracting value from Generative AI and emerging technologies

Early traction for GenAI was seen from consumer releases, but GenAI is quickly showing its potential to add contextual awareness and human-like decision-making to enterprise workflows. In the year ahead, extracting GenAI’s value and managing its risks, while maintaining trusted enterprise status, are at the forefront of many leaders’ strategic priorities.

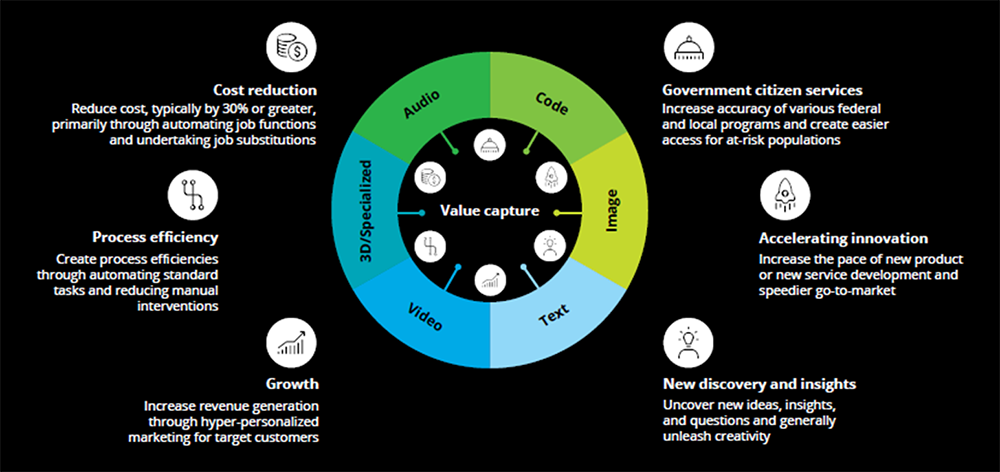

- Companies need to create value across the value chain to build competitive advantage. R&D represents the leading area for value opportunity, greater effectiveness can help companies advance their science and engage their customers and patients comparatively with others. Ultimately, greater patient outcomes could be achieved.

- Big pharma and big tech collaborating with GenAI, on more advanced GenAI in many areas that are constantly evolving.

Figure: Broad categories of value capture from GenAI

- As governments continue to chart the course to mitigate AI’s risk to society, with the advent of GenAI. Companies may need to upgrade enterprise technology and integrate GenAI into redesigned work processes.

3. Pricing pressures rising globally, threats of impacts on R&D innovation worldwide

Drug spending and growth is expected to accelerate globally over the next few years but varies across countries. Specialty medicines are projected to represent more than 40% of global spending by 2028, with more than half of total spending in leading developed markets. At the same time, China’s drug spending looks to be less volume-oriented and more focused on expanding access to novel drugs.

- Drug pricing and value continue to come under scrutiny as pricing pressures are being felt globally. In 2024, government-mandated pricing pressure and controls are expected to play an increased role in the affordability and accessibility of certain medicines.

- Over the next five years, the IRA is expected to have implications for how the industry makes decisions and allocates resources in both research and development (R&D) and commercial efforts with corresponding implications for access to drugs across the world.

- A good balance—between pharma cost containment measures, innovative medicine, and affordability—is critical to achieving optimal pricing and reimbursement, as the use of medicines is only expected to rise globally along with global calls for pricing transparency.

4. Accelerating speed of time to value in R&D

Large pharmaceutical companies account for almost two-thirds of total pharma research and development (R&D) investments and spent a record total of US$161 billion in 2023—an increase of almost 50% since 2018. As a percentage of companies’ net sales, spending reached a historic high of 23.4%.

- Speed to market has long been a leading priority for drug developers to accelerate patient access to life-saving therapies. Speed to market is only part of a success formula; companies should also be looking at ways to accelerate time to value.

- By adopting strategies to accelerate time to value, companies can start on their individual path to potential cost savings and competitive advantage. With the pace and development of AI-enabled digital solutions only expected to accelerate, leaders should start reengineering with an agile mindset.

- Financing for R&D can play a major role in whether the medicines and treatments that patients need are developed. Researchers calls for more research into drug development productivity/value creation.

5. Shifting trends in openness: Globalization vs. localization and impacts for multinational companies

Life sciences and medtech companies are increasingly global, and the global economy is moving toward a new normal—a shift away from peak globalization. Declining interdependence between countries may have negative consequences for global trade and overall prosperity. The Asia-Pacific (AP) region is expected to yield among the highest growth over the next several years—due to its sizable consumer base, increasing disease incidence, and supportive regulatory frameworks— and China and Japan are among the largest economies in the pharma and medical device markets.

- Globalization is not dead, it is changing. In the past two years, global trade is noticeably more concentrated and geopolitically close, relying on a smaller pool of trading partners.

- As geopolitical tensions rise, many top life sciences and medtech MNCs report they remain committed to China in 2024, but expect more regulatory scrutiny and market access challenges. Pharmaceutical MNCs are reworking business models as they watch price cuts play out and internal priorities shift.

- MNCs should be advancing their localization plans—to not just be competitive in the China market but also to address the increasing risks surrounding supply chain disruption and technology and data sovereignty.

6. Achieving better patient outcomes with personalized experiences and shared decision-making

Personalized care and treatments support better experiences, and there are many opportunities for life sciences and medtech companies to improve touchpoints throughout the patient journey. However, effectively and positively influencing a patient’s journey requires a thorough and specific understanding of that patient’s journey in order to be proactive and predictive about what patients may need.

- In 2024, life sciences and medtech organizations are considering novel ways to make experiences across the patient journey more customized for patients through technology. Many are experimenting with advancements in artificial intelligence (AI) all across the patient journey—from prevention to diagnosis, treatment, and monitoring.

- In medtech, successful organizations are embracing a more holistic view of the patient care journey beyond the physical device. More patients are taking an active role in their health care journey and turning to health solutions and services tailored to their prevention and wellness preferences over treatment alone.

- Life sciences companies are increasingly focused on “informed” decision-making to support SDM. A well-informed patient is more likely to actively participate in the decision-making process and better understand the potential outcomes and risks of any treatments.

- Optimizing touchpoints in the patient experience, as person-centered care continues to be a priority.