Article

"Future Consumer" Series: Omnichannel Transformation Begins by Grasping the Key to Consumer Mentalities

Our last article, "Situational Thinking + Multi-stage Readiness + Traversing the Trough—How Big Consumption & Retail can Conquer the Novel Coronavirus” analyzed recent performance in five main areas of retail consumption with reference to an archetypal consumer and their experiences in the 24 hours before and after the coronavirus outbreak. We recommended that businesses consider strengthening their awareness and cognizance of changes to consumer-end demand and venue preferences as the epidemic and campaign against it continues. Ideally, businesses will want to re-examine how their resources and competencies are arranged for the short-, medium- and long-term to seek to benefit from growth opportunities despite the outbreak, thereby achieving "leapfrog" growth.

The outbreak has pushed traditional offline retailers into the online realm, many of which now face a host of new questions as ordinary business services and local consumption appear to be returning to normality:

How can we balance offline channels with our online strategic focus to best embrace the return to normalcy? How can we determine the impact the novel coronavirus has had on consumer psychology to refine our products and adjust our channels? How can businesses wanting to build on new trends with a strong online focus go about establishing and supplementing these capabilities? How can they optimize online and offline channels, marketing and other resources?

Many businesses have clearly put new retail and omnichannel transformations very high on their agendas. But where should they start? We offer the following suggestions given the epidemic’s impact on industry and based on our experiences in facilitating omnichannel transformations for many businesses.

Unprecedented changes wrought on consumer psychology and behavior by the epidemic have not yet abated. Having deep insights into consumers is the bedrock of the transformation and upgrading of any business.

Many department stores have decided to reopen as the situation has evolved, including several major brand stores that are gradually welcoming cautious consumers back after shutting up shop earlier this year. Consumers are even showing more willingness to partake in outside dining, although they still have a quite cautious attitude due to the clouds cast by the virus's international spread.

Deloitte's Big Data team has examined consumers' current shopping preferences and presented these results as a hot topic word cloud. Consumers' psychology is still very much dominated by their material needs in relation to the virus and resulting changes to their consumption behavior.

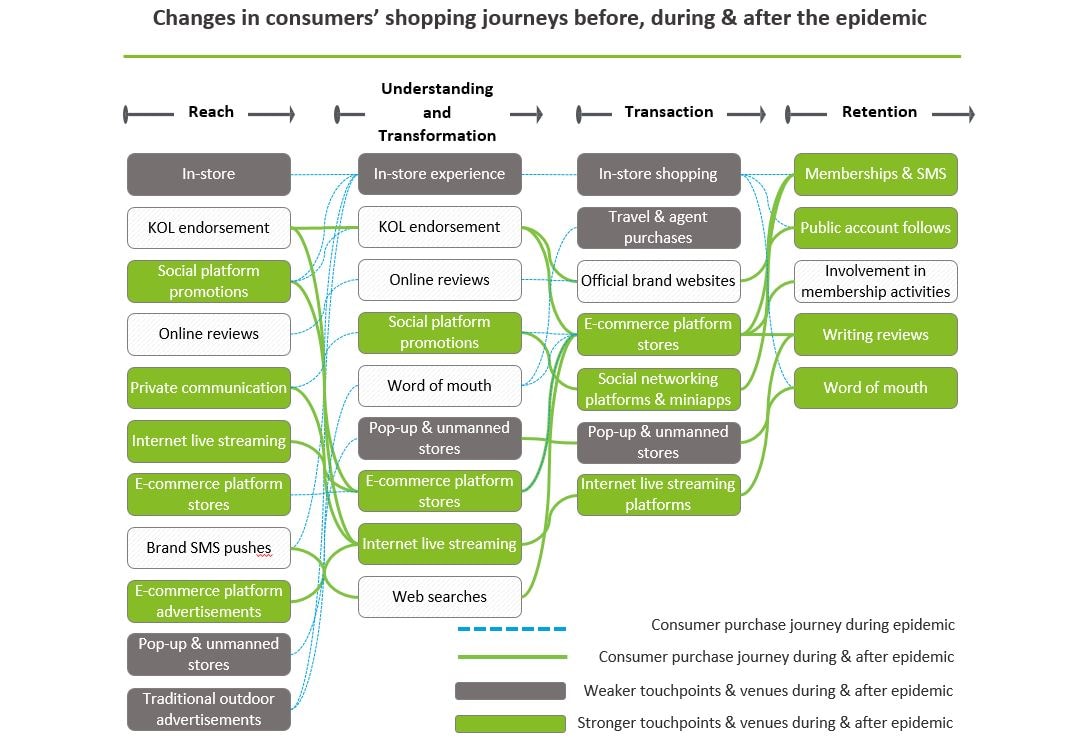

One effect of the epidemic has been a shift in the archetypal consumer's journey from "physical store shopping + platform-based e-commerce" towards a "life on the cloud" diversity of coexisting models, including integrated e-commerce, social networking sites, vertically-integrated platforms, official brand websites, online live streaming influencers and private traffic.

Life on the cloud: major characteristics and future trends

Product preferences

- Consumers have developed more interest in health and safety, particularly highly safe and immune system-enhancing products with strong protective features. This interest will likely persist for some time and to a high degree after the outbreak ends.

- There may be a divergence in consumers' purchasing behavior, with some splurging on "retaliatory purchases". Shoppers at Hangzhou Tower when it reopened on 20 February collectively spent more than RMB11 million in just 5 hours, which was more than the venue's operating income in a 12-hour day the previous 20 February. At the same time, many consumers are likely to lose purchasing power due to the direct or indirect effects of a slowing economy, making good value very important to them.

Brand attitudes

- Well-known brands that are seen as sophisticated have had an edge during the epidemic, but the online world still remains the key to victory. Brands that already had quite a strong online presence before the crisis, including many fashion and cosmetics names, have been rewarded with plenty of new online opportunities. However, frenzied purchasing and stock shortages have made consumers more willing to try less well-known or newer brands with strong online foundations. Meanwhile, brands that have recently rushed to embrace the online world might need to work harder, especially to retain long-term customer interest despite the preponderance of online traffic.

- Furthermore, brands and companies that have displayed a good sense of social responsibility throughout the crisis have enjoyed a big lift in consumer goodwill. Some brands have distinguished themselves through the recent crisis by offering extra support or attempting to protect the public interest, winning good word-of-mouth for future growth.

Channel changes

- There is a substantial shift from offline to online, including a new breed of online shopping experiences featuring multiple touchpoints for consumers. Consumers are finding themselves less hampered by familiarity with just a single shopping channel after experiencing recent frenzied buying and having more leisure time due to the crisis, becoming more willing to explore different types of retail touchpoints. The crisis has brought plenty of traffic to already dominant comprehensive e-commerce platforms and new or emerging social or vertical ones, as well as to online domains that have tended to get less online traffic, such as official brand websites and mini-apps.

- Consumers will start to emerge from their homes to enjoy the physical shopping experience once the epidemic situation improves. However, many of the online habits developed over this period will remain and flow naturally into consumers expecting a good omnichannel shopping experience. That said, some businesses are inexperienced, and their less than stellar performance during the outbreak could linger in the public mind and lead to generally higher expectations of and requirements for smooth integrated multichannel experiences.

Communication upgrades

- The rapid move from offline to online has also quietly shifted the ground in communications, with many new, innovative methods emerging. New favorites include live streaming, professional and niche KOLs. Apart from its use in the already sophisticated cosmetics sector, live streamed marketing has distinguished itself in promoting the latest cars, consumer electronics, health products and even real estate. Offline stores, meanwhile, will have to proactively embrace more private approaches to communication, such as community-based new retail purchases, as they continue to face intense sales pressure and will need to carefully cultivate O2O services to retain customers. Consumers' baptism of fire amid the COVID-19 outbreak will likely re-orientate them towards highly innovative, problem-solving and practical communication methods, and is likely to accelerate the emergence and development of new communication channels.

Changes in consumers' mentalities and shopping habits over several months of the epidemic will likely linger in one form or another, as all painful memories do, even after the situation has ended. Businesses and the overall industry will be driven and encouraged to work back from consumer desires to embrace the multichannel integration trend.

It is time for enterprises committed to creating a diverse landscape of online and offline touchpoints to seek in-depth insights into consumers, their shopping habits and personal preferences, as well as current and potential future trends. Businesses should also try to use the rich reserves of data they accumulated during the epidemic to outline the shopping journeys and alterations thereto experienced by different consumer groups and uncover the challenges consumers face. They can then transform those challenges into a basis for future products, better channel integration and outstanding shopping experiences.

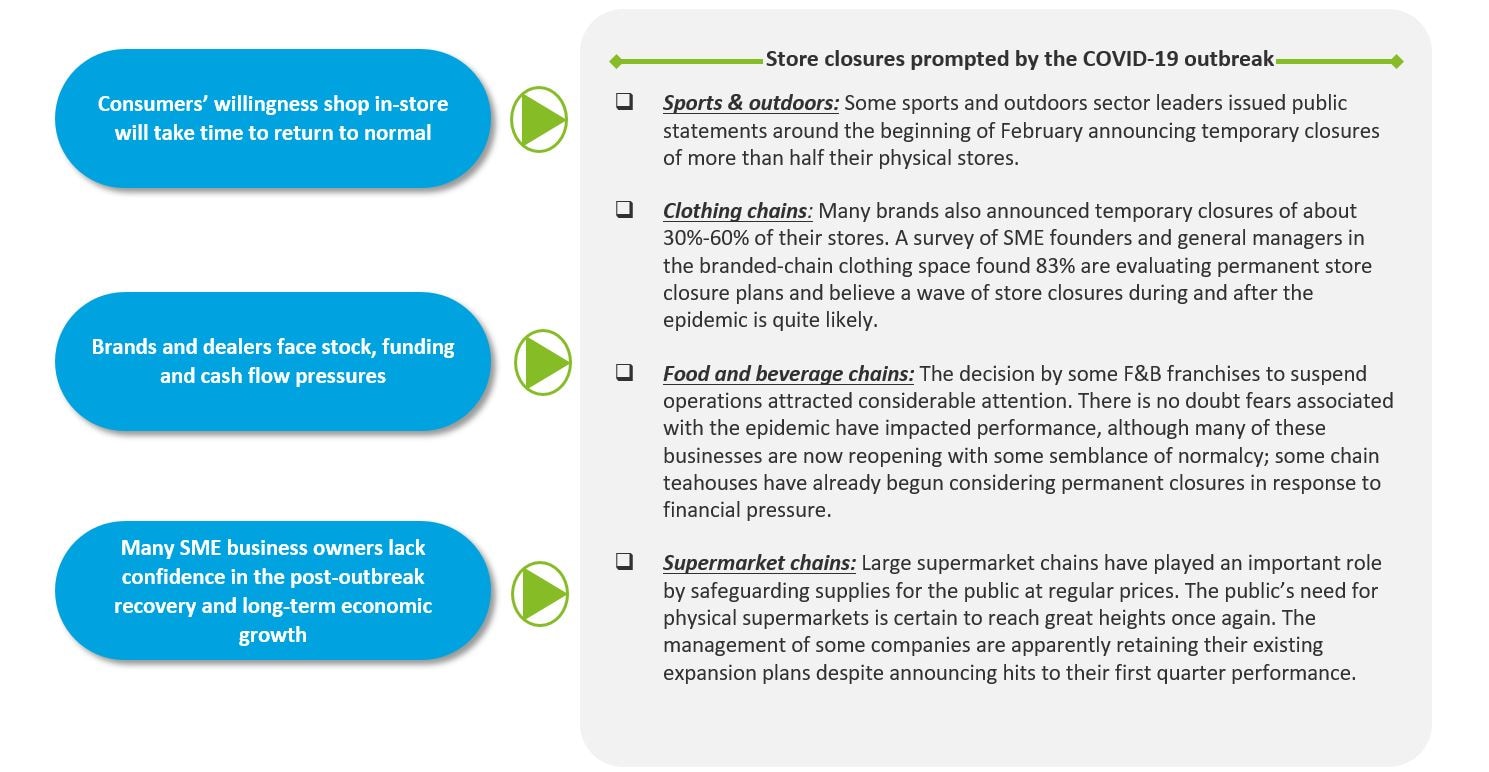

The epidemic has already had a dramatic effect on the offline landscape that will likely resonate for some time. Offline also urgently needs a period of optimization and adjustment.

Brand chains in Wuhan generally met the challenge posed by COVID-19 by suspending their operations as the city entered general quarantine. They have put cancelling planned expansions and permanently closing loss-making stores high on the agenda for 2020.

There is likely to be an industry-wide wave of SME closures soon, and industry leaders are likely to maintain a focus on proactively optimizing their store arrangements and a careful approach to store network expansion.

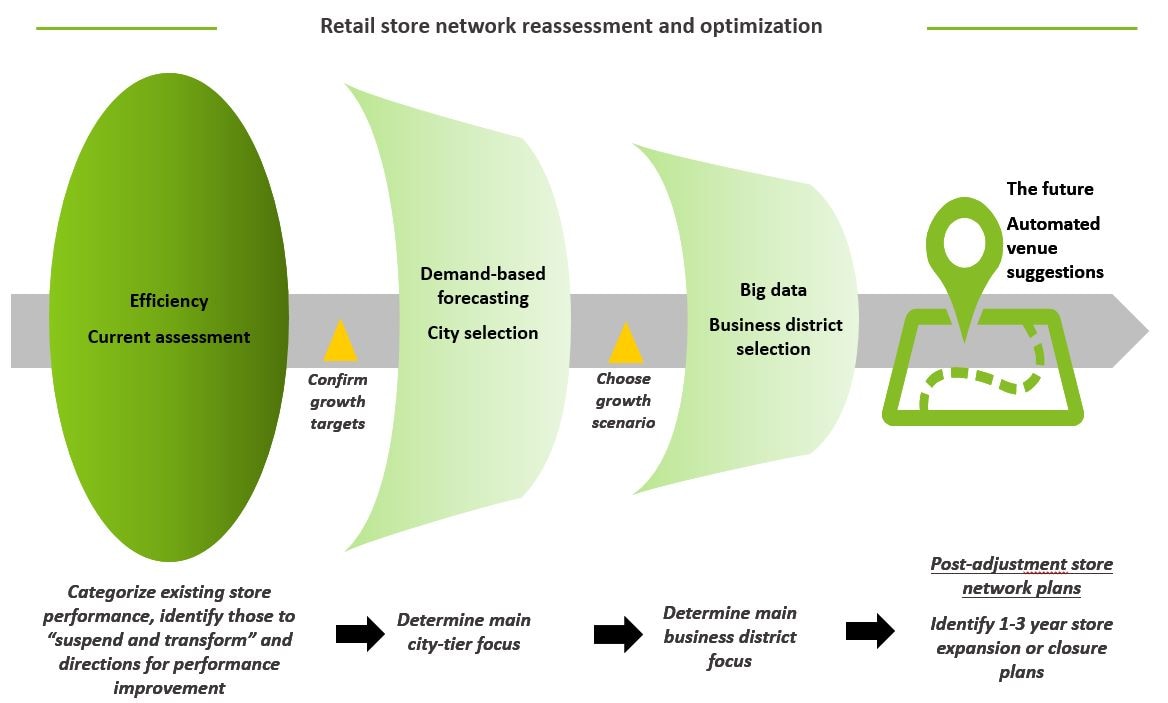

Under these circumstances, we recommend retailers prioritize a rapid assessment of current stores and seek more reasonable arrangements after multi-dimensional analysis of yields, growth and competition across different city tiers and dimensions; consider major restructuring and adjustment of any and all stores based on comprehensive evaluation of their profitability and age; and re-examine their 1-3 year store closure plans, focus on store optimization with their own resources, and take every possible step to minimize potential losses.

Having suffered the virus's impact on physical access and footfall, businesses could also consider establishing integrated offline-online prediction models using internally or internet sourced big data. These models could provide more tailored arrangements for structural adjustments or optimization across different cities, business district and individual malls.

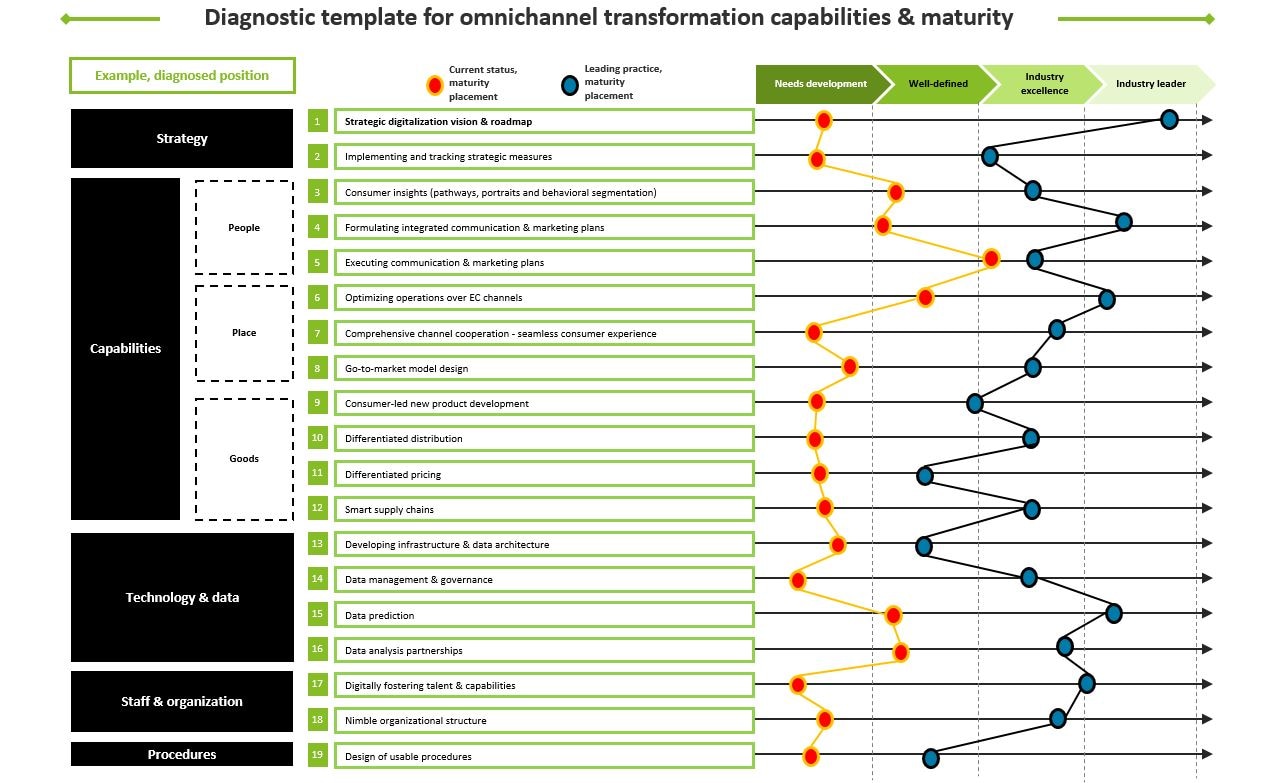

The epidemic has forced retailers to reach new heights in channel integration. They have had to diagnose their omnichannel capabilities and develop roadmaps for new situations—the first step for businesses seeking to achieve omnichannel transformation.

The virus has already shifted many brands’ services online and provided much food for thought and practical steps in relation to omnichannel competencies. Businesses with solid online footings prior to the crisis have had an obvious edge, proprietary e-commerce platforms with dependable supply and logistics have been embraced by consumers, and fresh food community-based retail has been pushed towards rethinking and improving omnichannel competencies. In addition, innovative forms of social networking, live streaming and similar forms of online marketing, have earned plenty of additional attention, acceptance, and uptake.

Brands with strong online presences have had a clear edg

- The epidemic has so far had somewhat less of an impact on some segments, such as cosmetics, which already has highly sophisticated online operations, than on others

- Some clothing businesses have jumped quickly into the online world, using initial groups of existing members to gain from integrated use of public accounts, WeChat groups and miniapps and get their products moving.

Consumers appreciate businesses with their own e-commerce platform

- Proprietary e-commerce platforms with strong, stable supply chains have a clear advantage over dealer merchant platforms that rely on external logistics, as reflected in the former's greater popularity with consumers. This should inspire businesses to engage in new thinking about their online service models and platform partnership choices.

Fresh food retailers lead the way in channel integratio

- Demand for fresh food e-commerce is challenging supply. A leading e-commerce company now has more than a million daily active users. Some other platforms have breached 400,000 daily active users each—a number that continues to grow.

- Some delivery services offered by traditional supermarkets have also experienced breakthrough growth. A leading retailer's O2O business grew 4.4-fold over 2020 Chinese New Year from the previous Spring Festival, with its miniapp seeing order volume surge 15-fold.

Private traffic and live stream marketing are being used more extensively

- Live stream influencer marketing is not only being used to sell otherwise slow-moving fruits and flowers, it is also being deployed in segments such as cosmetics, healthcare and education to maintain existing consumer networks and offer online services and courses. Businesses are now seeing some of the opportunities that can arise from the creative application of private traffic.

Online channels are in the midst of a pressure test that will eventually redraw the industry landscape and enhance business performance. Digital integration of channel and internet networks is destined to become an important strategic choice and path to transformation for many brands in 2020.

In these challenging times, we recommend retailers undertake a comprehensive, diagnostic overview of their omnichannel capabilities to systemically ascertain any shortcomings and set out a transformation roadmap with clear plans of action.

Our experiences in omnichannel construction and examining the digitalized transformations of service brands in recent years taught us that such integration has an inherent need for data and technical support, and that digitalization itself demands consistency across five main areas—strategy, competency, technology and data, staff and organization, and procedures. Competency also covers the major issues of "people, goods, and place", a multi-dimensional view including an organization’s degree of consumer insight, marketing communications, e-commerce channel services, omnichannel partnerships, distribution and pricing. To formulate an appropriate transformation roadmap, a company should be able to leverage these models to quickly determine its level of omnichannel capabilities and where these fall short.

Many large traditional retailers suffer from a lack of clarity around their omnichannel digitalization transformation objectives, and have not formulated a consistent approach to developing the online side of the businesses. These companies often have not have clearly set down or decided an expansion model; overlook or undervalue the importance of cross-channel big data consumer insights, consumer reach and a more finely-tuned set of operational skills; and often lack properly established grassroots staff organizations and procedures.

We advise such enterprises to focus their initial steps on an integrated, omnichannel model strategy. This can better clarify their future online and offline development targets, the value of cross-channel strategic pillars, and their corresponding relationships, to clarify strategic roadmaps and arrange the required resources. Given these businesses are also likely to be underdeveloped in data, technology and other areas, we also recommend they give full weight to the question of whether to build proprietary systems or enter partnerships, and choose 3rd-party partners carefully. Full and proper utilization of 3rd-parties will help these enterprises make huge short-term improvements in these areas to "traverse the trough".

Every business always has room to improve. This is where a more personalized, systematic analysis can help a business set out a path to omnichannel transformation that is more suited to its specific circumstances and comes with a greater understanding, and ability to meet, changes in consumer psychology and behavior. Through this roadmap, a company can reach a stronger position in tomorrow's consumption marketplace.

Conclusion