News

Hong Kong Tax Newsflash

Revised application forms for Certificate of Resident Status (CoR)

Published date: 12 June 2023

The Inland Revenue Department (IRD) revised the application forms for CoR effective today, i.e. 12 June 2023. A CoR serves as proof of Hong Kong resident status for the purpose of claiming tax benefits under the comprehensive double taxation agreements / arrangements (CDTAs). The most updated forms can be found on the IRD’s website. There are significant changes made to the forms for company / partnership / trust / body of persons (i.e. IR1313A and IR1313B) which applicants should be aware of.

Background

Change in the approach to the issuance of CoR

Historically, in deciding whether a CoR can be issued, the IRD would consider whether the applicant is a “resident of Hong Kong” and its “entitlement to tax benefits” under the relevant CDTA. In order to strengthen international tax cooperation and in view of the changing business environment, the IRD changed its approach to base its decision of whether a CoR can be issued on the plain definition of "resident of Hong Kong" in the relevant CDTA. As such, the information required in the application forms for CoR is adjusted accordingly.

Formalization of administrative facilitation measures

On the other hand, the IRD had committed to revising the application form (IR1313A) to facilitate applications for CoR where the claim for tax benefits in the Mainland falls within the Circular of the State Taxation Administration (STA) on matters concerning "Beneficial Owners" in tax treaties (PN9).

Back in 2018, the STA issued PN9, which provides for how the beneficial ownership test is applied to claim tax benefits on dividends, interest and royalties under the CDTA and introduces a look-through rule for a multi-tier holding structure and the extended scope of the safe harbour rule. A Hong Kong company is required to present a CoR to the Mainland tax authority to prove its tax resident status for the purpose of claiming such benefits. Previously, to facilitate the applications of CoR for PN9 purposes, CoR applications could be submitted in a bundle with a cover letter to provide the relevant information for the IRD’s consideration.

The IRD has now formalized the above administrative facilitation measures to include the information required for the application of CoR for PN9 purposes in the application form (IR1313A).

Key changes to the application forms for CoR

Details of the establishment and business activities

Previously, all applicants were required to provide details of the establishment and business activities in the appendix to the application forms. In the revised forms, only the following applicants are required to provide such details:

- Applicants incorporated / established outside Hong Kong

- Applicants claiming tax benefits under PN9

- Applicants claiming tax benefits under the CDTA between Hong Kong and Japan (HK-Japan CDTA)

Information required for the application of CoR for PN9 purposes

As mentioned above, the IRD includes the information required for the application of CoR for PN9 purposes in the application form, i.e. part 2 of the appendix to IR1313A. The IRD also makes clear certain information required in the revised form, e.g. applicants should provide the identity of the lead applicant in the multi-level holding structure, including the name, address and Hong Kong business registration number. The identification of each person included in the chart of the relevant multi-level holding structure should include the Hong Kong business registration number, the registration number in the place of incorporation / establishment, the Hong Kong identity card number / passport number, etc.

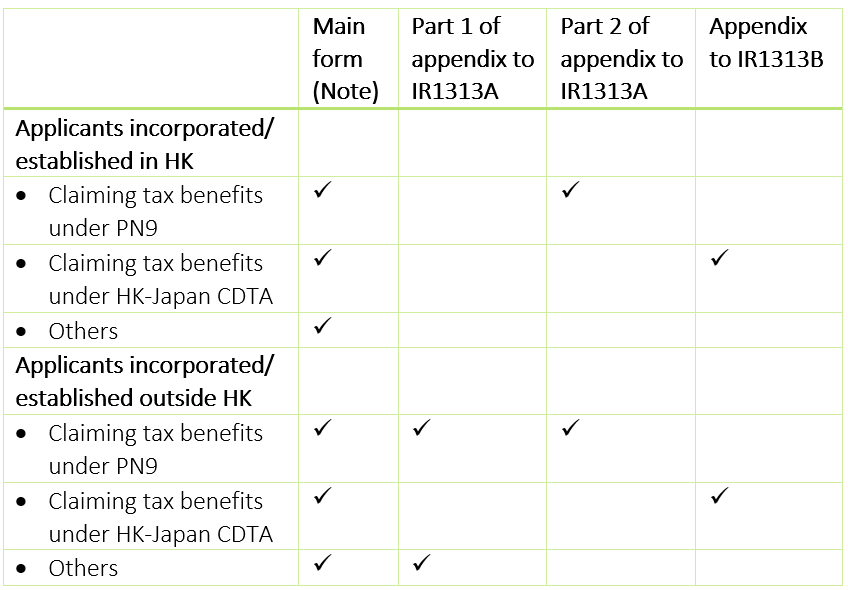

Impacts on applicants

We summarize which parts of the application forms are required to be completed by different applicants in the table below:

Note: Applicants claiming tax benefits under the CDTA between Hong Kong and Mainland China should complete Form IR1313A, while applicants claiming tax benefits under other CDTAs should complete Form IR1313B.

Applicants incorporated / established in Hong Kong

Much less information is required to be provided for most applicants incorporated / established in Hong Kong, except for those claiming tax benefits under the HK-Japan CDTA.

Applicants claiming tax benefits under the HK-Japan CDTA are required to provide all the information required in the appendix to Form IR1313B. The reason is that the HK-Japan CDTA adopts a “primary place of management”1 test in determining residence, which is different from the other CDTAs (which generally regard a company incorporated in Hong Kong as a Hong Kong resident). Some information is not required to be provided by applicants incorporated / established in Hong Kong previously if they have more than 2 shareholders or are part of a listed group, e.g. details of staff, meetings of directors, management activities, etc. Applicants should be aware of the changes and prepared for the additional information required.

The process for application of CoR under PN9 would continue to apply, i.e. applicants in a multi-level holding structure should submit their applications in a bundle, and the lead applicant and each of the co-applicants should fill in their own application form.

Applicants incorporated / established outside Hong Kong

The information required is more or less the same as in the previous practice.

Our comments

We are pleased to see the IRD change its approach to issuing CoR to base its decision on the plain definition of "resident of Hong Kong" in the relevant CDTA and reduce the information required for applicants incorporated / established in Hong Kong. It would reduce the applicants' compliance burden and may encourage companies incorporated outside Hong Kong to re-domicile in Hong Kong.

We also welcome the long-awaited update to the application form for CoR for PN9 purposes as it would facilitate the application of CoR under PN9.

However, it is worth noting that applicants are still required to provide the business address in Hong Kong, the number of management and other staff in and outside Hong Kong, etc. Applicants claiming tax benefits under PN9 are required to provide further details in the appendix to the forms. It is uncertain whether the IRD would issue a CoR simply based on the definition of “resident of Hong Kong” in the CDTAs, which generally define a Hong Kong resident as a company incorporated in Hong Kong. In other words, the IRD may still consider the business substance of the applicants in Hong Kong and the applicants’ beneficial ownership status for applications under PN9.

Update: As confirmed with the IRD, they will only consider the plain definition of tax resident per CDTA (e.g. location of incorporation) when issuing the CoR although information about the applicant’s personnel in Hong Kong are required in the CoR application form. This implies that Hong Kong incorporated companies should be able to obtain the CoR for all the tax treaties concluded by Hong Kong (except HK-Japan CDTA).

Applicants should also be aware that the issue of a CoR will not guarantee that they will be successful in their claim to benefits under the relevant CDTA. It was up to the CDTA partner to determine whether tax benefits under a CDTA would be granted.

Applicants are suggested to seek professional advice when applying for CoR.

1 Clause 3 of the protocol to the HK-Japan CDTA defines the “primary place of management” as the place where the senior management of the company (or person) makes key strategic, financial and operational policies and where its staff carries out the day-to-day activities necessary for making those decisions.

Tax Newsflash is published for the clients and professionals of Deloitte Touche Tohmatsu. The contents are of a general nature only. Readers are advised to consult their tax advisors before acting on any information contained in this newsletter.

If you have any questions, please contact our professionals:

Authors

Jackie Wong

Tax Director

+852 2238 7421

jackiewong@deloitte.com.hk

Carmen Cheung

Tax Manager

+852 2740 8660

carmcheung@deloitte.com.hk

Kiwi Fung

Tax Manager

+852 2258 6162

kifung@deloitte.com.hk

Global Business Tax Services

National Leader

Andrew Zhu

Tax Partner

+86 10 8520 7508

andzhu@deloitte.com.cn

Hong Kong

Raymond Tang

Tax Partner

+852 2852 6661

raytang@deloitte.com.hk