{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

India has been saved

Cover art by: Tushar Barman

After having battled one of the biggest recessions it faced in recent memory, there was some cheer for India’s economy that recorded a positive—albeit marginal—growth in Q3 FY 2021. Till recently, economic activity seemed to be gathering momentum at a sustainable pace with people demonstrating greater confidence in stepping out and spending. The vaccination drive has made good progress too; over 132 million people (at the time of writing this article)—mostly from the vulnerable segment of the population—have been inoculated in a span of three months.

Of course, the recent spike in infection and the imminent threat of variants cast a cloud of doubts. Mobility restrictions that hurt the economy the most, are being imposed back (although in a calibrated manner) by a few States. While it is easy to lose hope in tough times, similar experiences around the world provide some comfort. Much the same way the United States witnessed a sharp increase in infection rates during the second wave (starting November) yet experienced economic impact that was relatively low compared to the first wave, we expect the economic and health impact of the subsequent waves in India to be contained to a quarter or two.

We are cautiously optimistic and expect growth to touch 11.7% in FY 2022. Growth in FY 2022 will likely be a story of two halves, with economic activity picking up rapidly in the second half. While we expect a strong revival in the years ahead, it might be naïve to not accept the scars the pandemic may leave behind on the economy. One of the apparent aftermaths is the rise of a dichotomous world that we are currently witnessing. In this article, we take a sneak peek at the rising inequalities that may have implications on all walks of the economy.

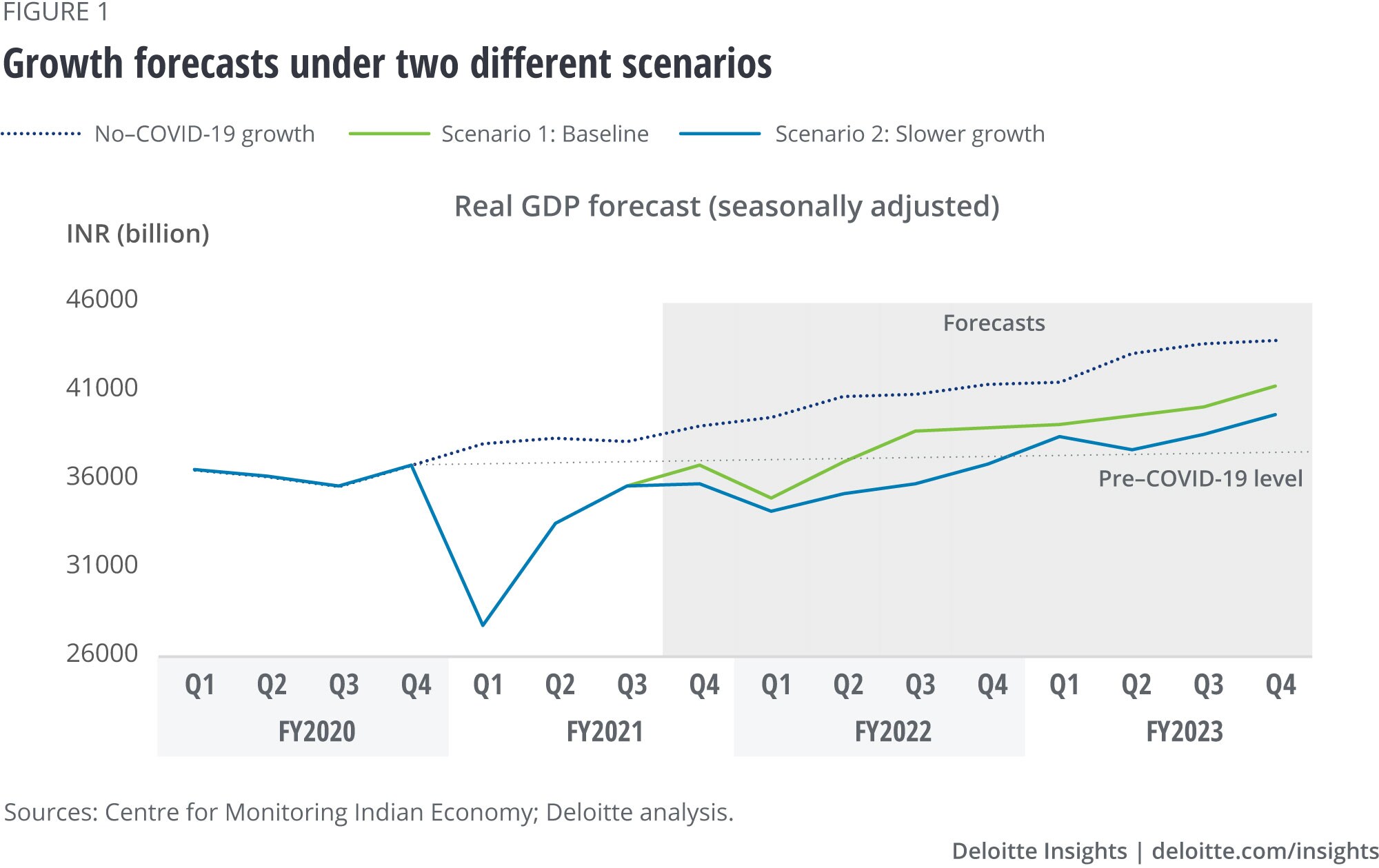

We were among the first few to have predicted double-digit growth in FY 2022 back in December 2020. We continue to remain optimistic about growth despite the rising number of infections. This is because of the strong rebound in manufacturing and several services sectors, while the agriculture sector—the knight in the shining armor amid the pandemic-led recession—continues to perform steadily. On the demand side, recent data suggests that capital investments have seen a strong rebound after a prolonged period of lull. The momentum is expected to continue as held-up or postponed investment decisions will likely see implementation after a lag of one year. More importantly, the base effect will give a big thrust to overall growth.

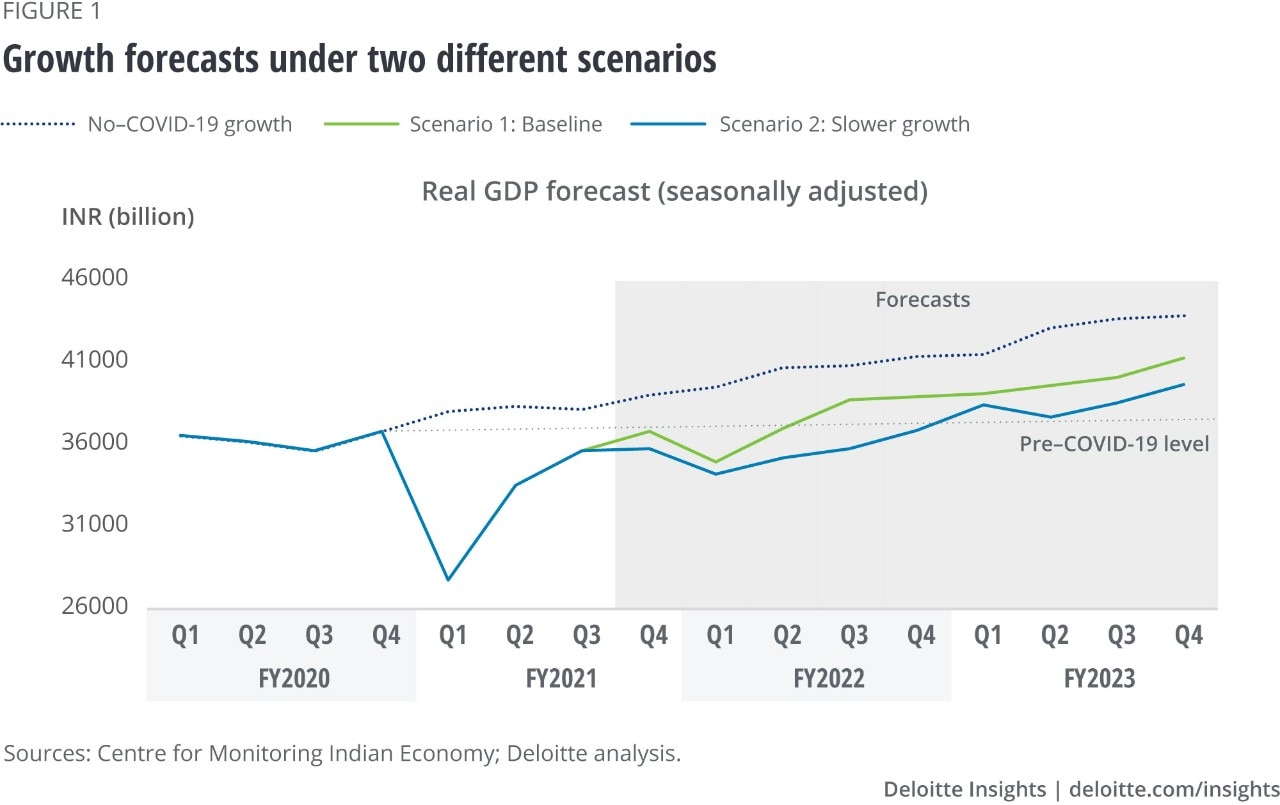

After a contraction in FY 2021, we expect the economy to grow at a modest pace in the first half of FY 2022. Growth is projected to reach 11.7% in FY 2022 in our baseline scenario. That said, slow recovery in a couple of quarters will likely have an impact on next year’s numbers as well. In FY 2023, we foresee growth of 6.9% (figure 1). In addition to the low base effect in FY 2021 and Milton Friedman’s plucking1 theory playing out, we believe five drivers will steer growth over the next two years:

The baseline accounts for the downside risks such as the possibility of a modest performance in the hospitality sector due to uncertainties around movement restrictions. While it’s highly likely that the aforementioned drivers will persist, our alternate growth projections show a modest recovery in the years ahead in case they don’t. (See sidebar, “Assumptions for the two scenarios” for our underlying assumptions for the two alternate forecasts.)

To keep things in perspective, it is important to highlight that despite a quicker rebound (even under our baseline scenario), the output levels will remain far below the potential GDP, the levels that we would have seen had there been no COVID-19. When compared to FY 2020, GDP growth in the next fiscal year will be a mere 3.5%, well below the potential GDP. It will likely take a while for the trajectory to reach the potential, which is way beyond our forecast horizon at this point in time. Clearly, the scars left by the pandemic on the economy are deep.

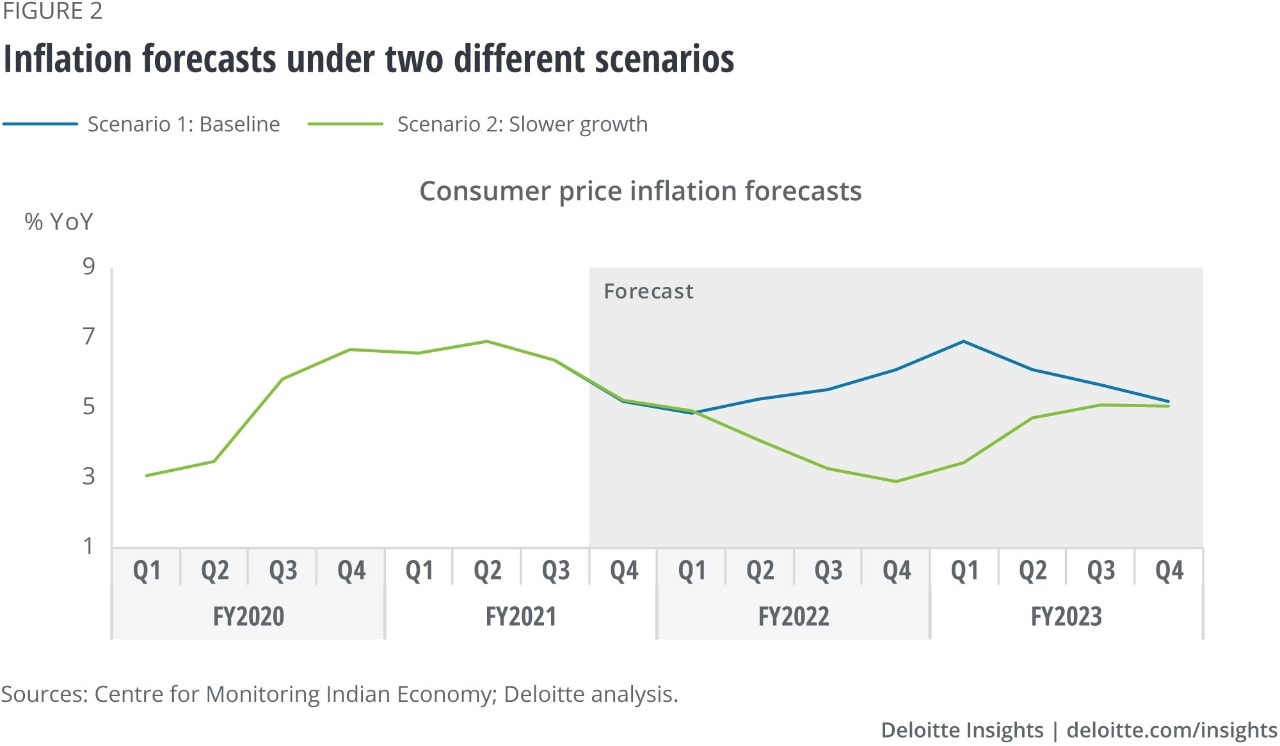

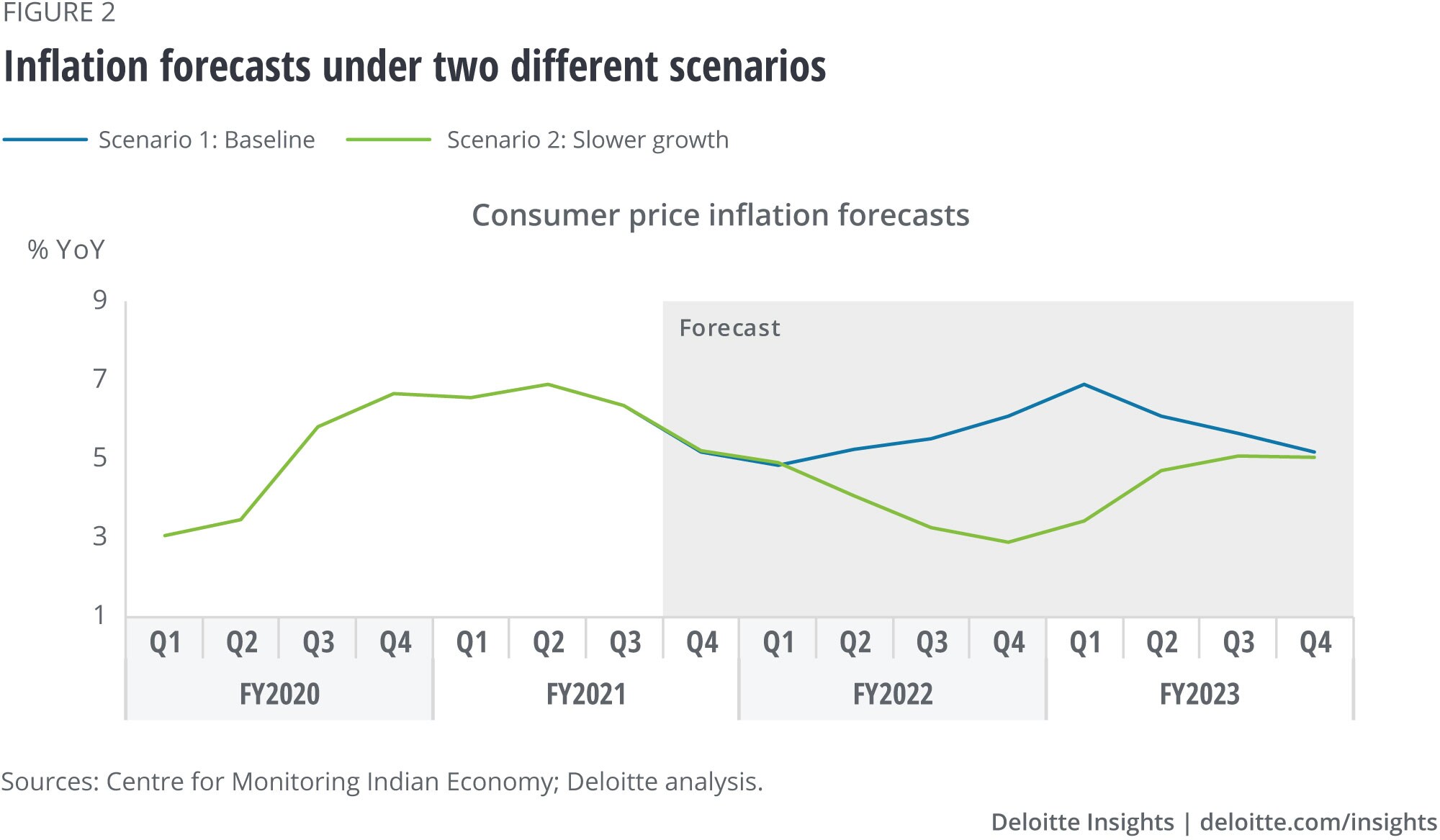

Under our baseline scenario, prices are expected to ease by mid-2021 due to low demand and supply, but rise quickly as soon as infection rates are under control (figure 2). This is because demand overshoots supply in a very short period, even though strong capital investment tries to meet the gap.

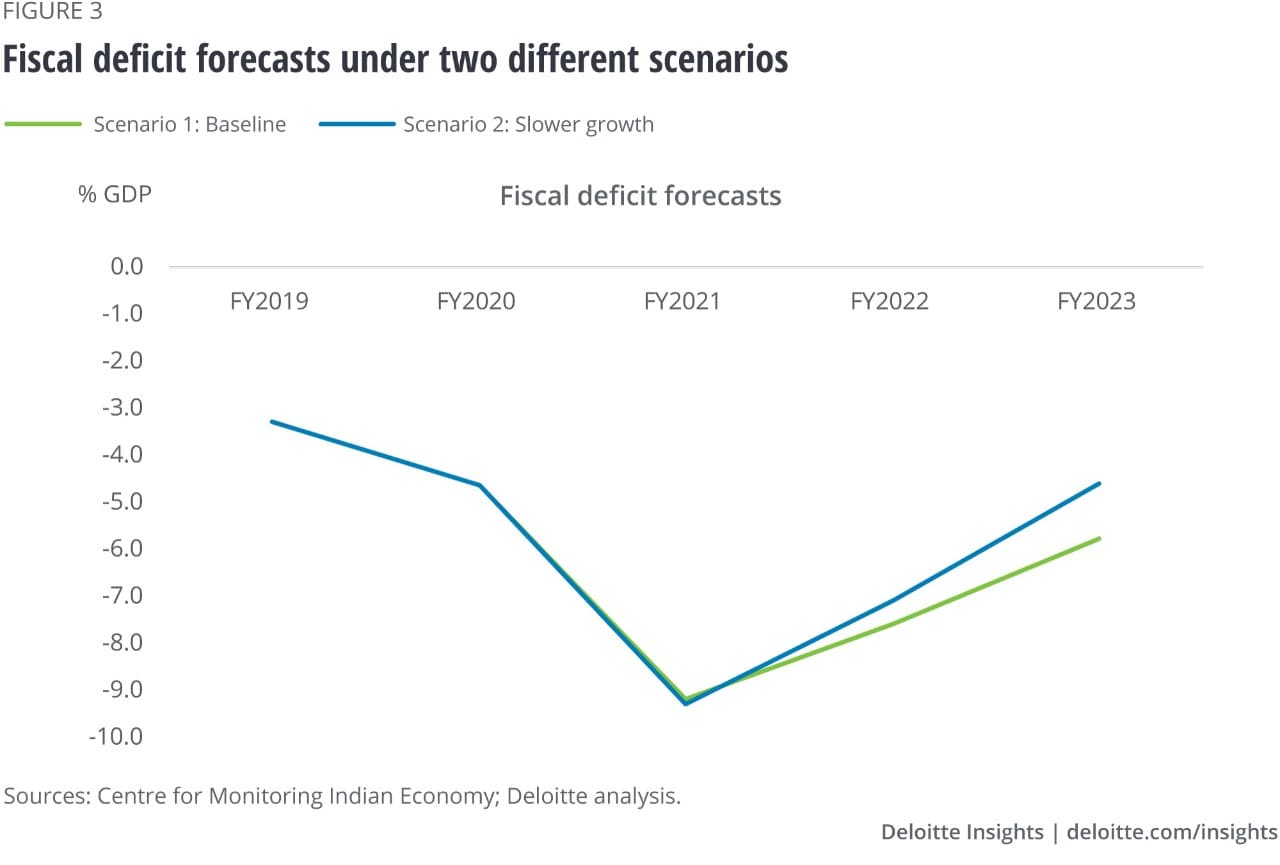

As explicitly indicated by the government in the Union Budget 2021, the fiscal deficit is expected to worsen in the next few years (figure 3). The government suspended the Fiscal Responsibility and Budget Management Act’s fiscal deficit goals provisionally to charter a new path to support the nascent recovery, and launch the economy on a sustainable growth path over the next few years. High spending backed by disinvestment strategy is expected to further boost the economy but at the expense of higher deficit and debt. Of course, a lack of funding may prevent the government from spending the budgeted amount (especially if disinvestment implementation takes longer than planned), in which case, our alternate scenario reports a lower deficit in the years ahead.

That said, a virtuous circle led by a stronger rebound can help the government to improve its fiscal and debt situation in the years ahead and consolidate in the medium term.

Assumptions for baseline:

Downside risks (which form the basis for the alternate scenario):

It is worthwhile to take into consideration the brewing inequality that is gradually coming to the fore. We tracked a few forward-looking indicators that threw up some surprising contrasts. A few of these will mitigate over time once the economy gains a steady momentum, while others may take more time.

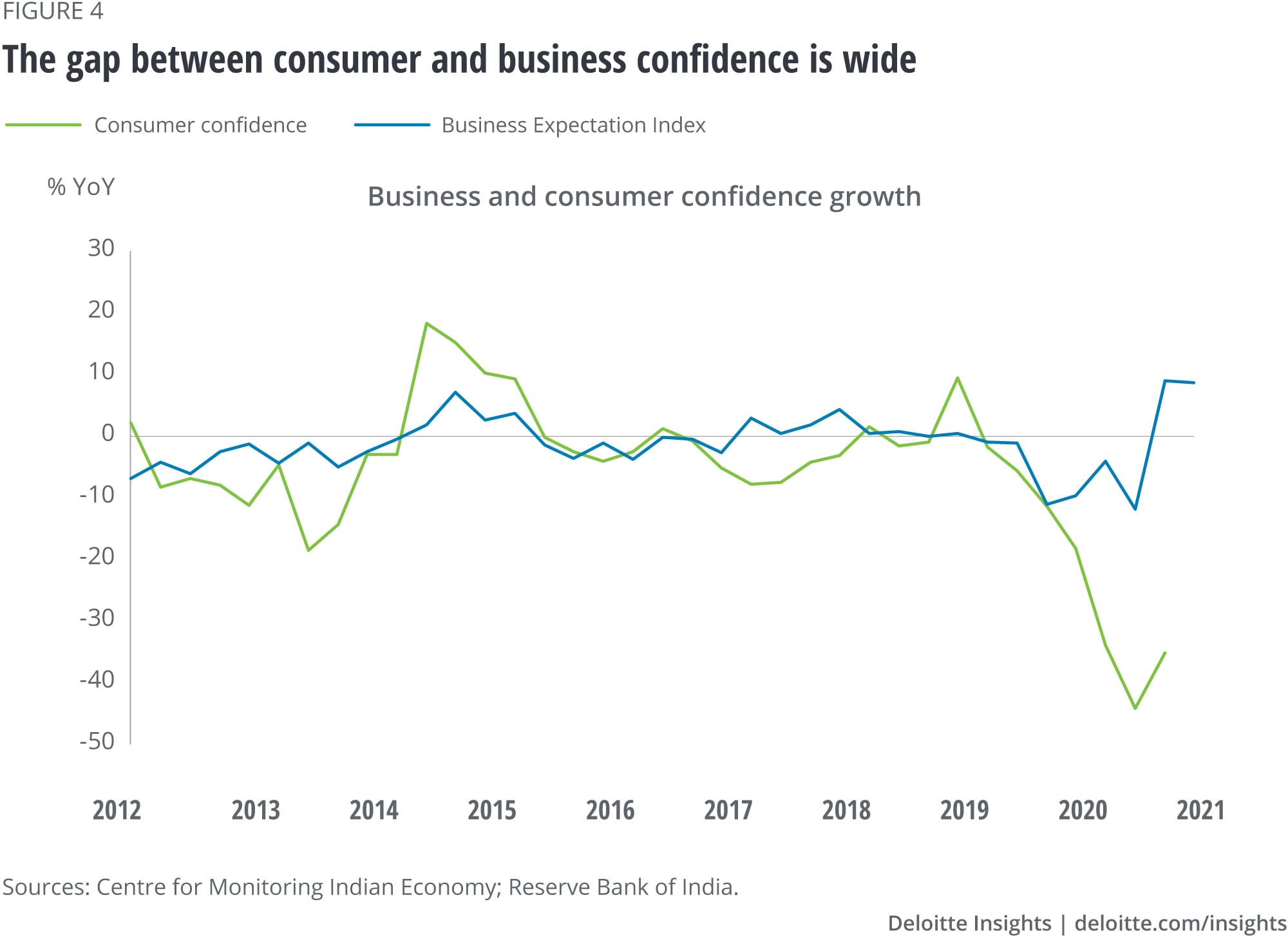

For instance, the gap between consumer and business confidence has never been as wide as it is today (figure 4). The removal of mobility restrictions and reduced supply disruptions helped businesses to bounce back with greater confidence. However, a gradual job market revival and health and financial concerns prevented consumers from spending, crushing their confidence in the economic revival. While this gap may reduce over time, a few others will likely take longer.

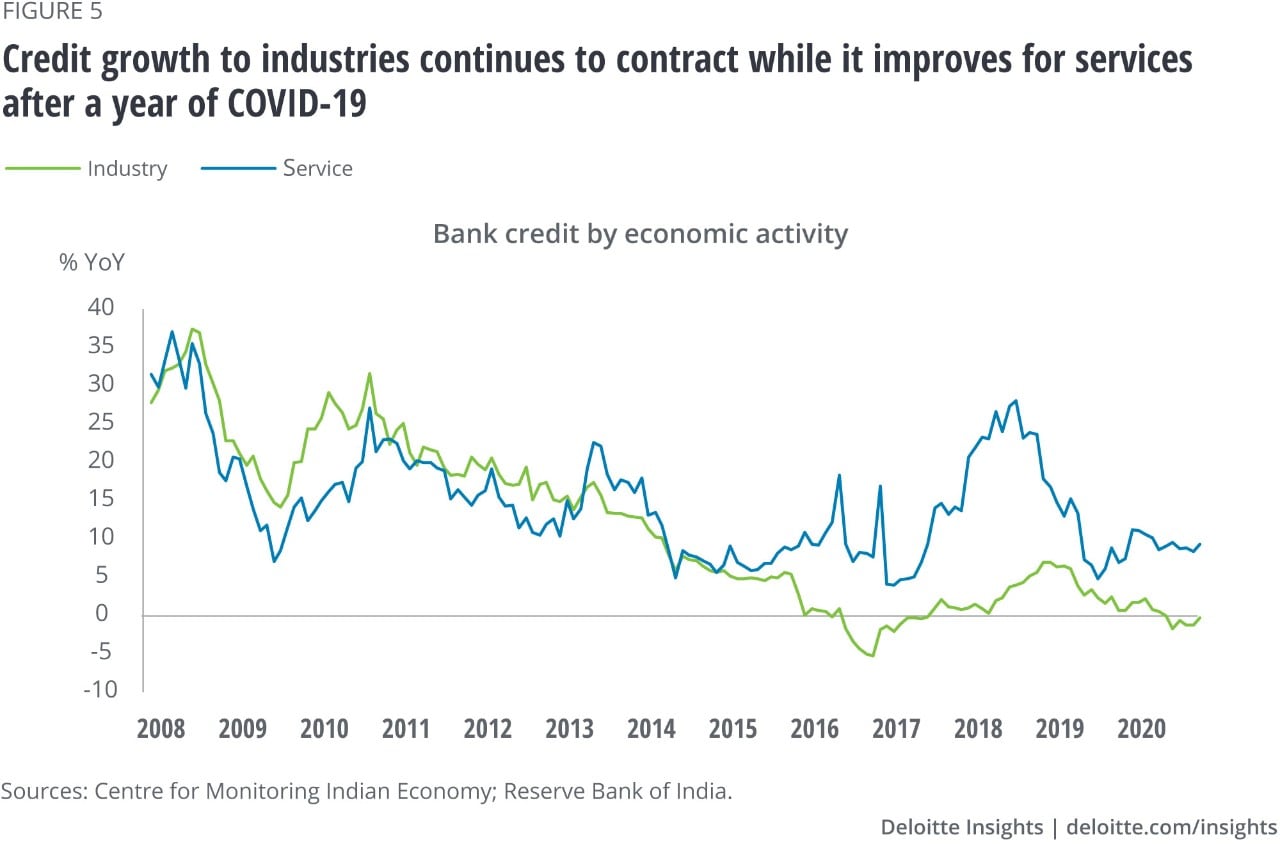

One such widening gap has been that of sectorwise credit lending in the economy. The disparity in credit lending by banks to services and manufacturing has been persisting since 2015 (figure 5). However, with uncertainties around COVID-19, the contrast has become more perceptible. Lending to the industry contracted year over year after August 2020, despite a quicker rebound in manufacturing as movement restrictions were eased. On the other hand, growth in credit to the services sector has remained fairly strong, although it is a lot slower compared to the growth seen during 2017–19.

This widening gap is a concern for a nation that wants to grow as a global manufacturing hub. Low credit growth can hamper the ability of the industry sector to spend and expand at a time when India is looking to be self-reliant and build economies of scale.

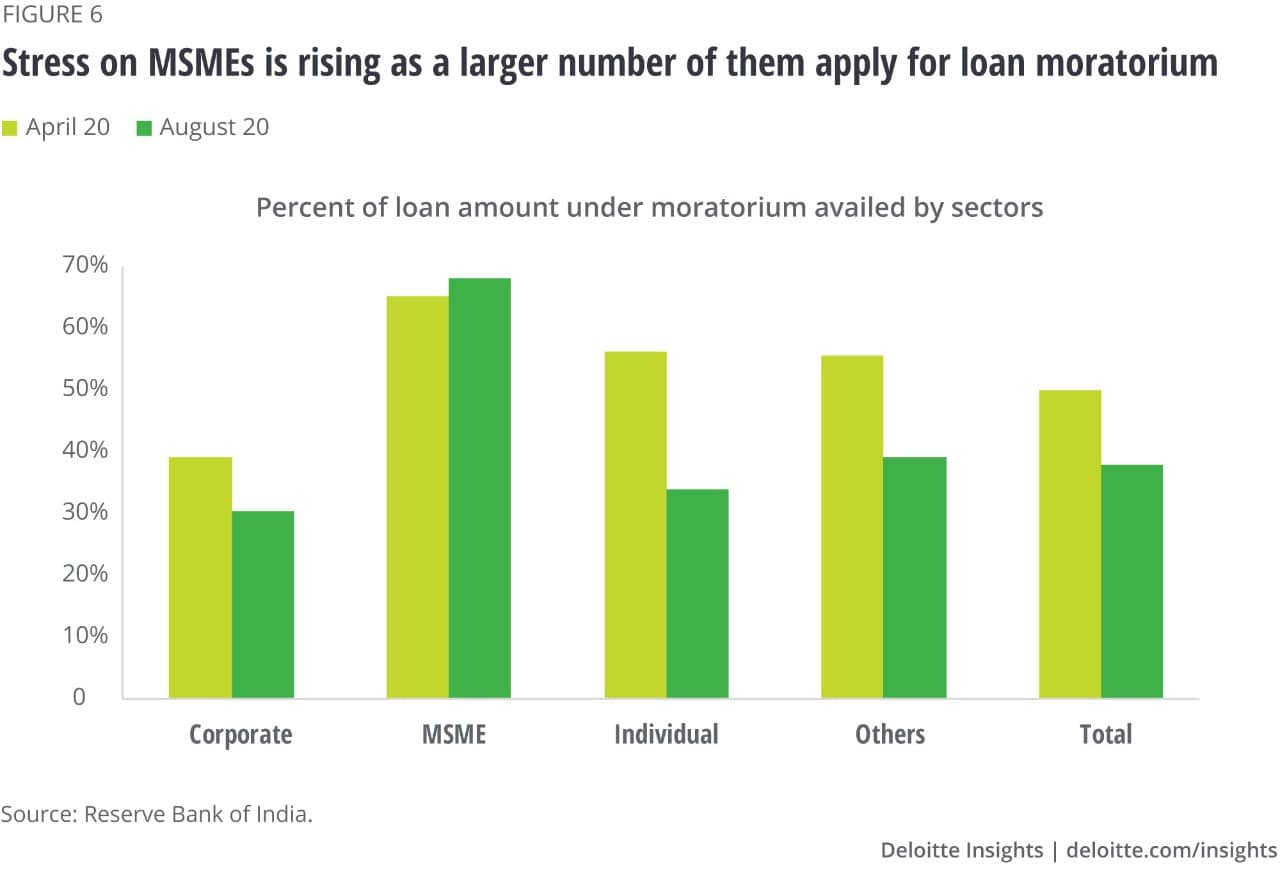

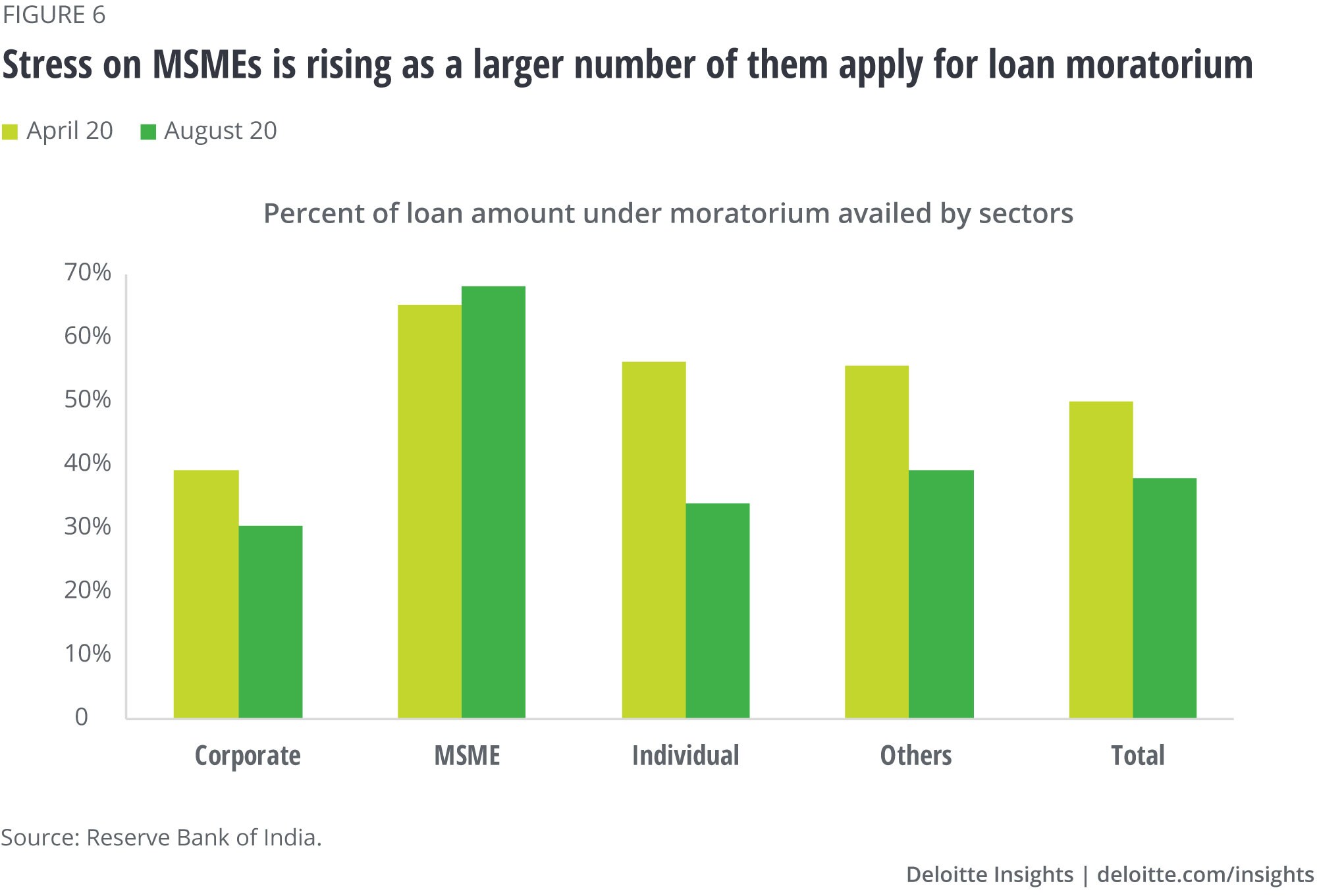

The MSMEs, which are the backbone of the manufacturing sector contributing 34% of the total manufacturing output, have been hit hard by the pandemic and are struggling to stay afloat even after several months. The larger enterprises weathered the pandemic storm better because of stronger balance sheets, more cash holding, and business continuity strategies. The MSMEs, meanwhile, were caught unprepared due to an acute shortage of working capital, canceled orders, customer losses, and severe supply chain disruptions. Most of the MSME portfolios and NPAs for select banks remain elevated relative to previous years. The fact that a larger number of recipients from the MSME sector opted for the COVID-19–related moratorium in August 2020 compared to April 2020, while the trend was exactly the opposite for corporate and individual borrowers, clearly indicates the high level of stress MSMEs are facing (figure 6).3

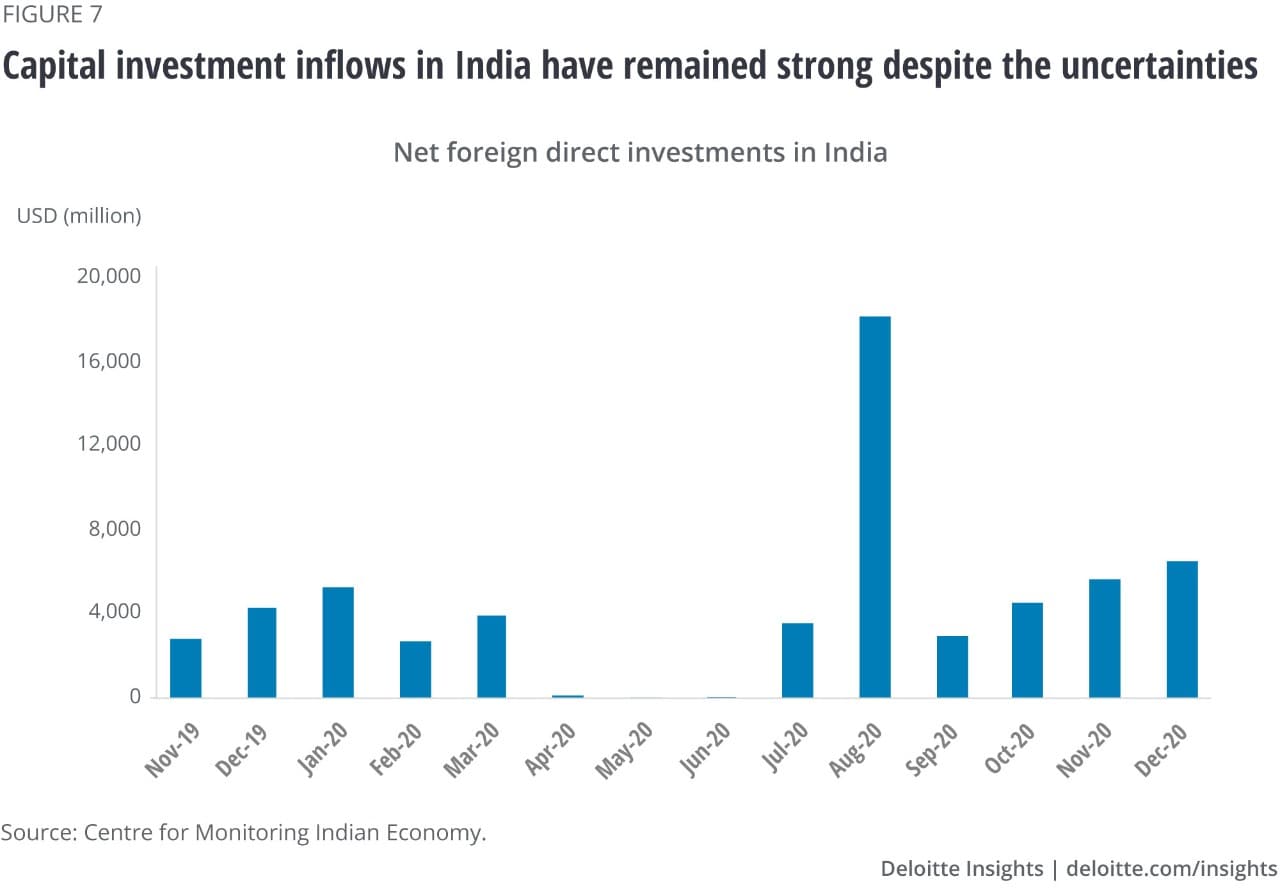

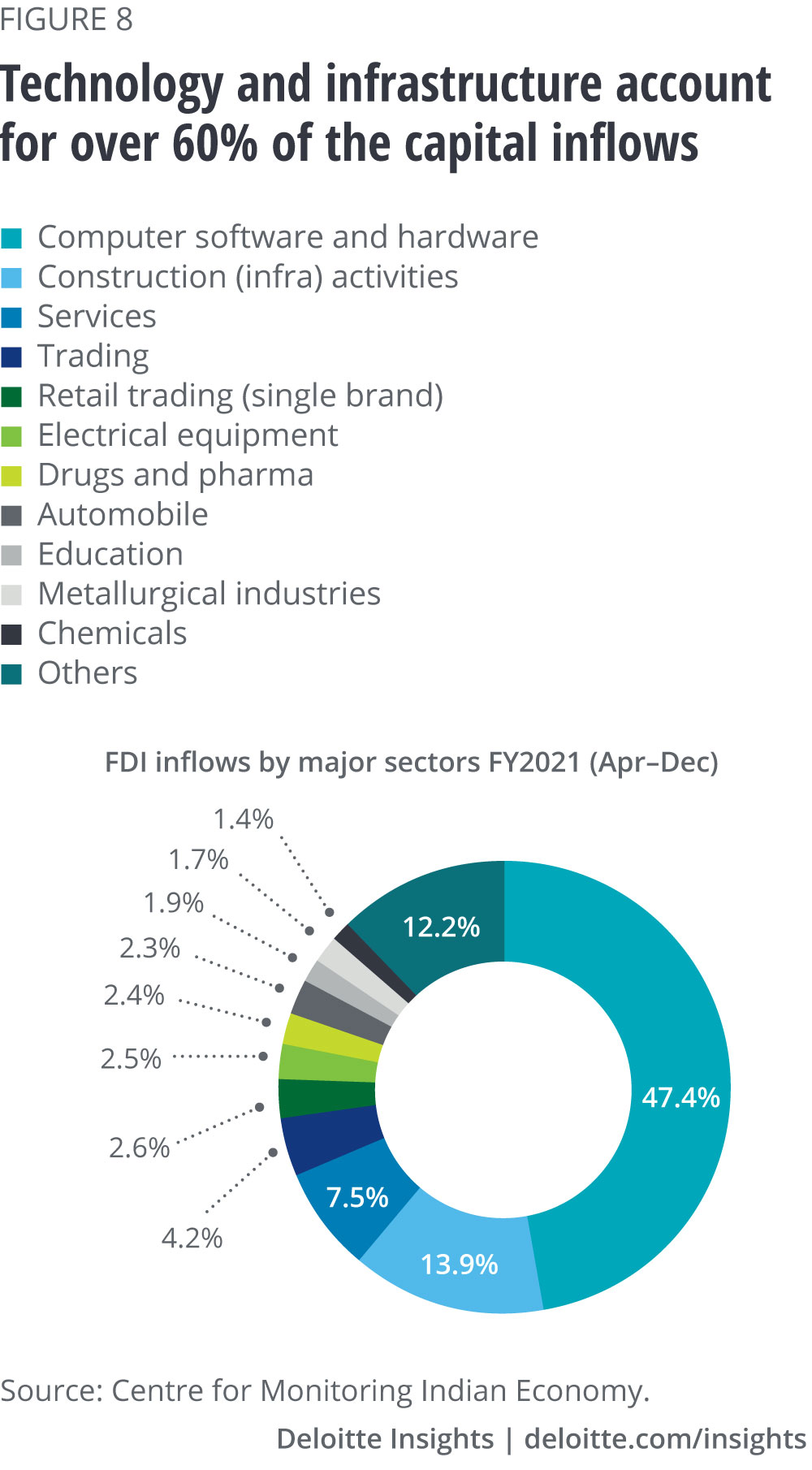

Net foreign direct investments (FDIs) since the pandemic have defied every possible prediction, and the trend has remained firm throughout (figure 7). However, a closer look at the sectorwise capital flows points to the disparity in the sectors that have received capital investments from global investors. Over 47% of the FDI has flown into the computer software and hardware sector, while construction (including infrastructure) accounted for 13.9% (figure 8). The share of the inflow into other sectors has been fairly small. Among them manufacturing, chemicals, metals and products, and transport had the most number of new projects announced.

The economy is likely to witness stress even if we witness a V-shaped recovery. Acknowledging the uneven path that it is treading will help policymakers and businesses to reflect on the next steps, even if it means experimenting with approaches a bit. As quoted by H.L. Menken, an American journalist, “every complex problem has a solution which is simple, direct, plausible — and wrong.”

Cover art by: Tushar Barman