{kind=link}

{kind=link}

{kind=link}

{kind=link}

Maybe you really can’t go home again: COVID-19’s impact on the housing market has been saved

Cover image by: Jaime Austin

The COVID-19 pandemic changed how we worked, learned, and chose to interact with others and these, in turn, caused some of those who could afford it to rethink where they live. It precipitated a substantial exodus from urban areas in mid-2020 as people began to consider moving to less congested areas or to be able to afford housing that could accommodate the entire household’s need to work and take classes remotely. Now, thanks to vaccines, restrictions (self-imposed or mandated) have largely disappeared, and some may be revisiting their decision.

However, those contemplating a return to their former environs and looking to purchase a home might reconsider as they will likely have to deal with higher housing prices and mortgage rates, and limited housing supply. The cities and states that lost population during the pandemic might not find it easy to get these domestic migrants (and their dollars) back, which might dim their fiscal outlooks.

The US population growth rate has been on a downward trend since the 1990s, but higher death rates and continued reduction in international migration and births reduced population growth in 2021 to only 0.1%—the lowest growth rate in US history, according to the Census Bureau.1 However, most of the differences in population growth among the states are being driven by internal migration. Among the 17 states where population declined over the year, losses were greatest in New York (–1.6%), Illinois (–0.9%), Hawaii (–0.7%), and California (–0.7%).2 Although we do not have direct evidence of why people moved out of these states, the New York case may offer some insight. The pace of population growth in nearby Connecticut, Maine, New Hampshire, and Vermont accelerated in 2021 over their 2010–2020 trend,3 which suggests people are leaving New York in response to the pandemic. In 2021, the two states with the fastest population growth were Idaho and Utah, growing by 2.9% and 1.7%, respectively; this is a continuation of the trend of fast growth seen over the prior decade as folks move in from other states.

A recent Brookings study looks at the same Census data with a focus on metropolitan versus nonmetropolitan areas, including a further breakout of metropolitan into major metropolitan areas (the 56 Metropolitan Statistical Areas (MSAs) with populations more than 1 million), and “other” metropolitan areas (the remaining 365 MSAs).4 As in the differences among the states, domestic migration is the primary determinant of differences in population growth among these groups.

Overall, the major MSAs had been experiencing net-negative domestic migration since 2014–2015, but the rate of exodus more than doubled during 2020–2021. The study states, “Thirty-one experienced domestic outmigration in 2020–21, and 35 showed either greater net outmigration or smaller net inmigration than in 2019–20. Among several major metro areas that experienced domestic inmigration in 2020–21 (such as Phoenix, Dallas, Austin, Charlotte, and Atlanta), those migration levels were smaller than in 2019–20.”5 Within these major MSAs, the population losses were concentrated in the urban core counties; their suburban countries saw a jump in inward domestic migration. The smaller MSAs and nonmetro areas were the recipients of the remainder of the domestic migration.6

Many choosing to make a move during the pandemic were renters—rental vacancy rates rose in states such as New York and California between 2020 and 2021.7 However, some of those migrating renters became homeowners with the move, as reflected in the rise in homeownership rates.8 This led to a boom in existing home sales starting in mid-2020, which only came to an end in January 2022 when mortgage rates began rising. The slowing of sales increased existing home inventories after reaching a low of 1.6 months in January 2022. However, this increase in inventories has not stopped existing home prices from continuing to rise at an increasing rate. Between January 2018 and January 2020, the price of single-family existing homes rose by 11.0%. According to the most recent data, between August 2020 and August 2022, the corresponding price increase was 25.9%.9

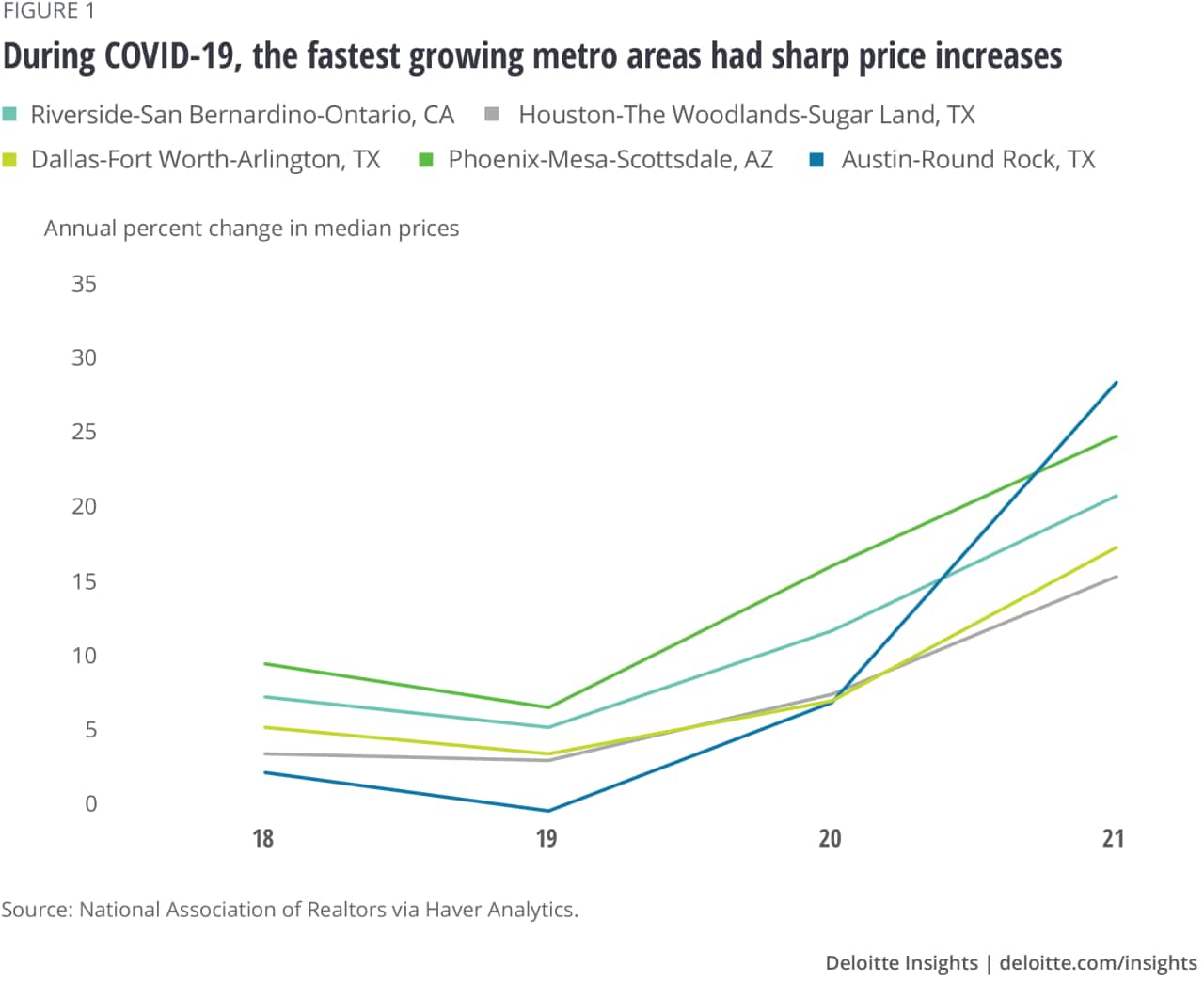

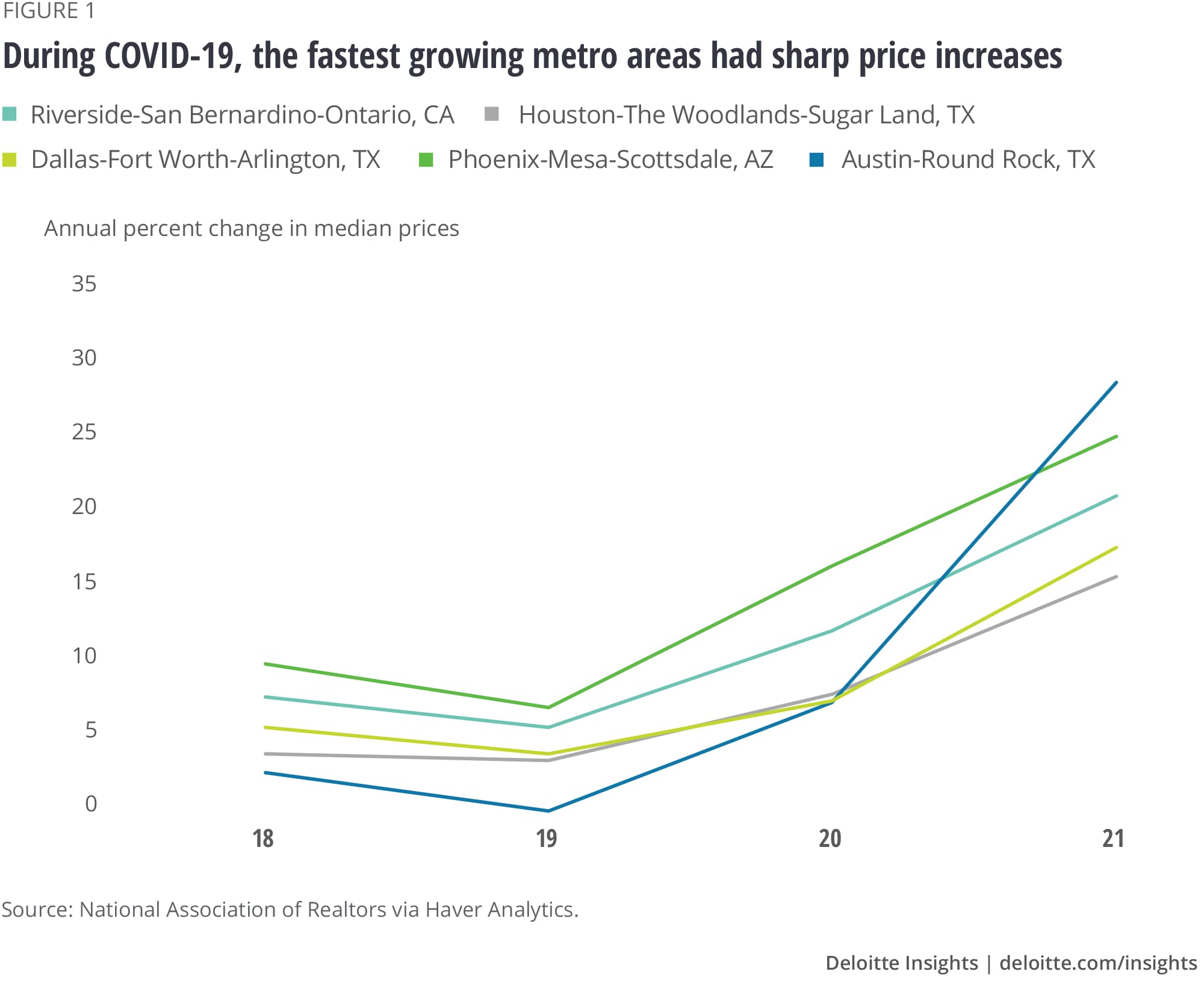

The major MSAs experiencing the highest increase in population between 2020 and 2021 were Dallas, Phoenix, Houston, Austin, and Riverside.10 These cities showed a noticeable uptick in the pace of home price increases from 2019 to 2020 and 2021 (figure 1). Interestingly, the MSAs experiencing the largest loss of population did not see declines in the median sales price of existing single-family homes over the same time span; rather, home prices continued to rise. This could be reflective of any number of factors, including increased demand from shifts from inner-city condos to nearby suburban detached homes.

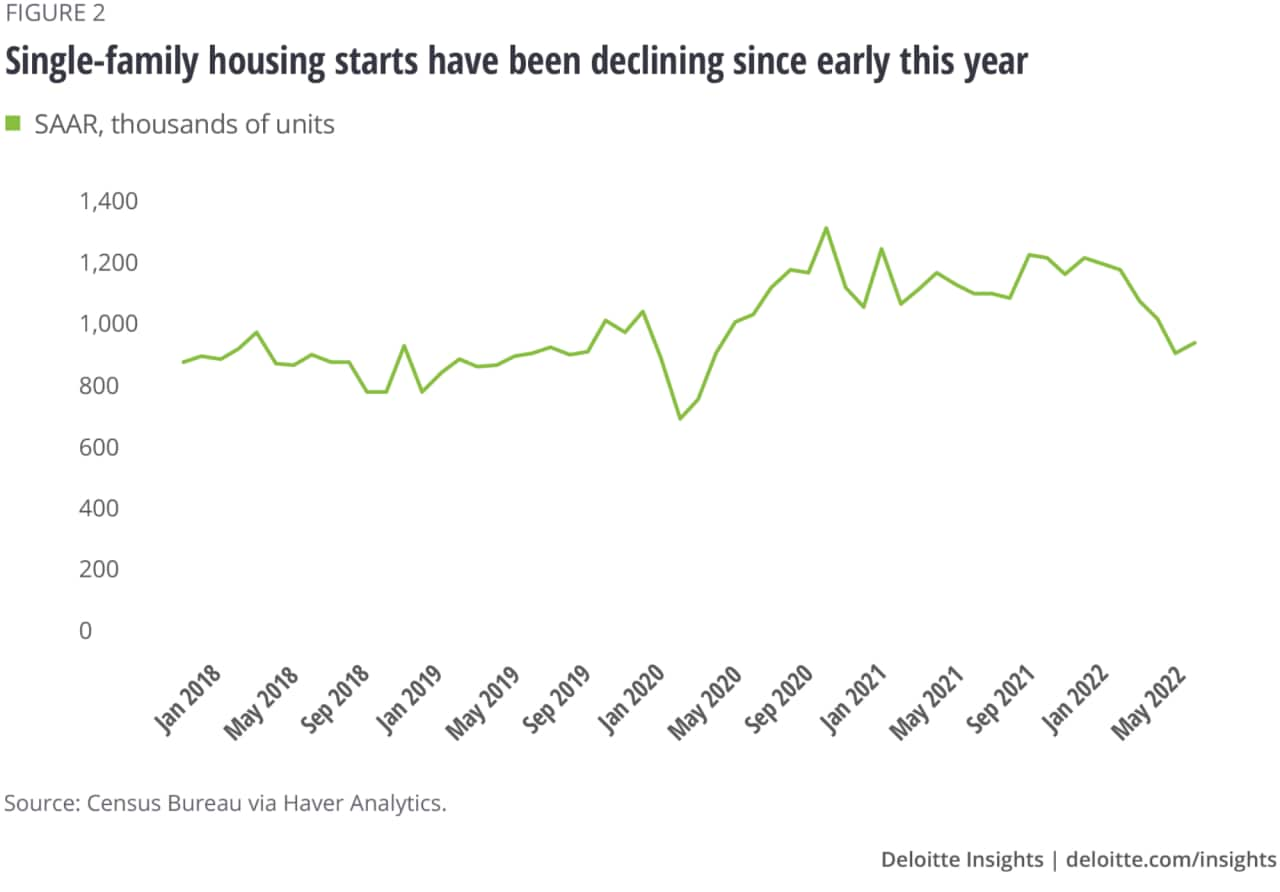

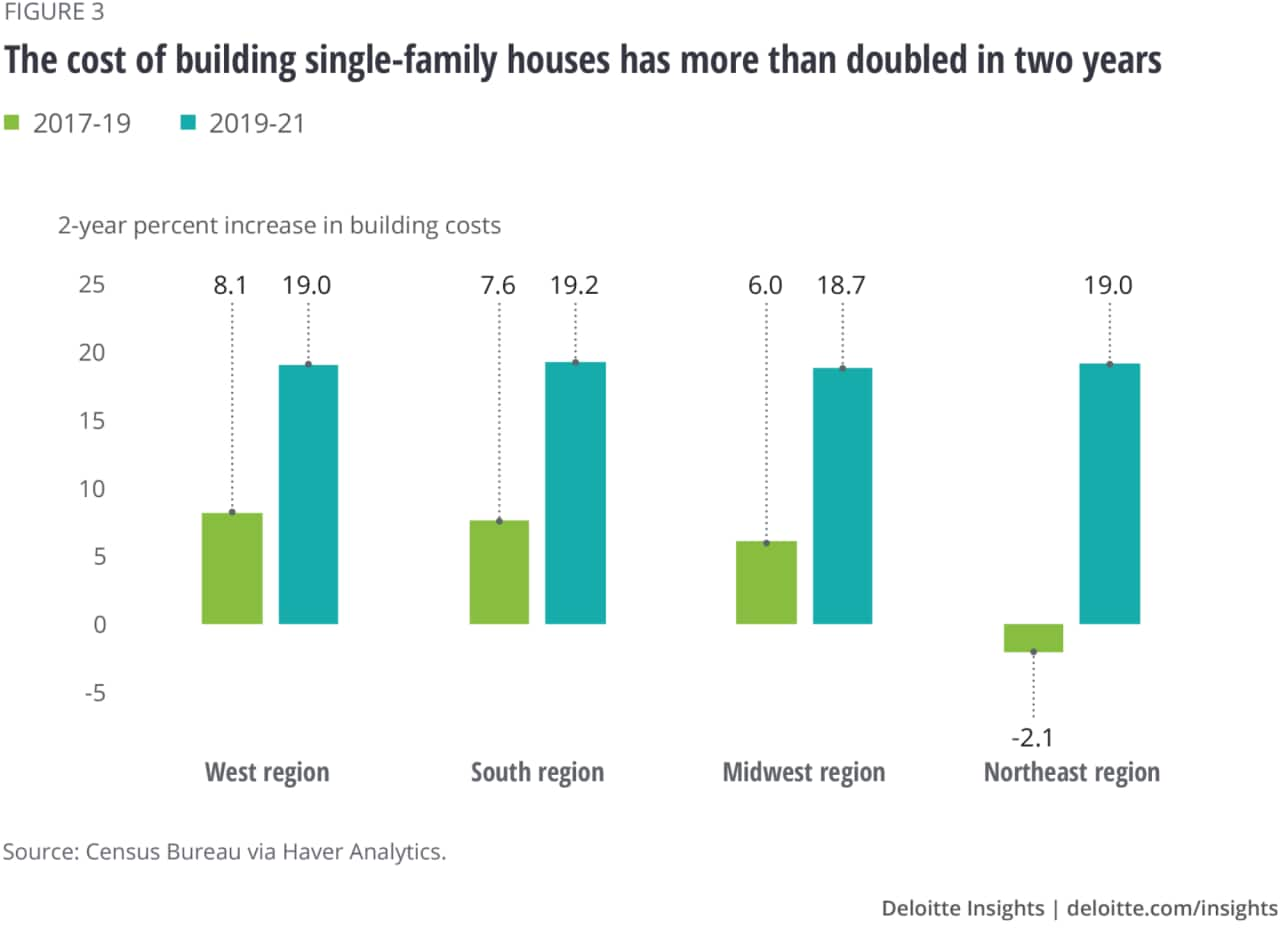

For those wanting a new home, the situation is even more complicated. Starts of new single-family homes have dropped by 19.2% since the beginning of the year and the cost of building has skyrocketed (figures 2 and 3). And the pain is not over. CBRE projects that with the significant growth in labor and materials costs that has already occurred year-to-date, construction costs are projected to increase by 14.1% for 2022 as a whole.11

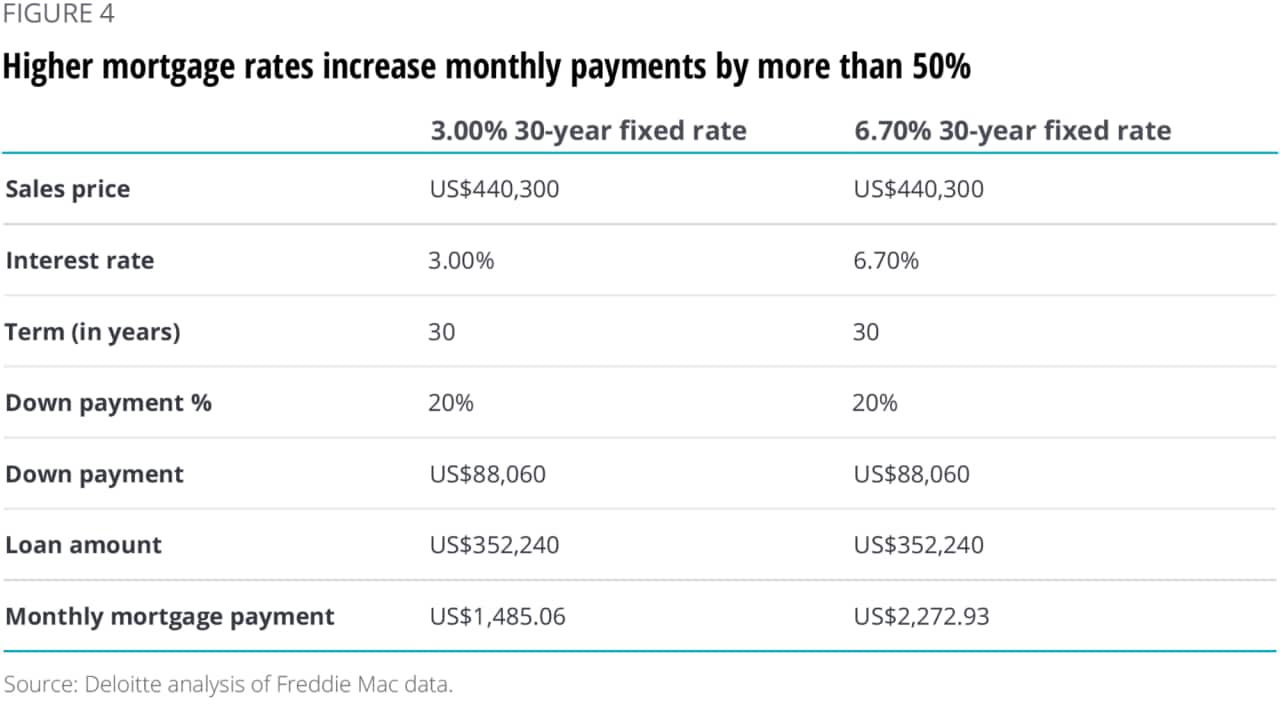

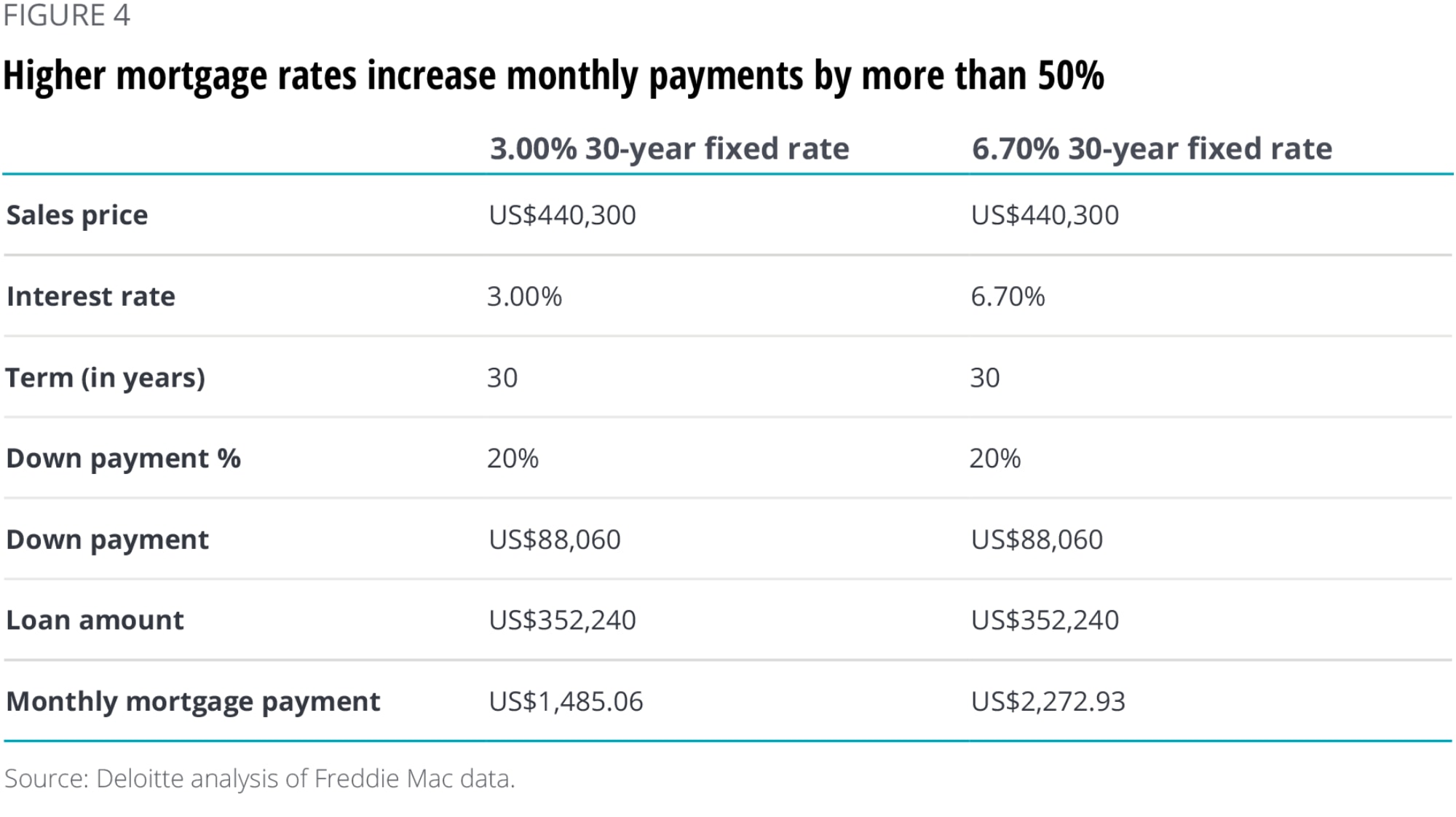

People looking to relocate might be able to cope with the higher home costs, particularly if they are currently living in owner-occupied housing that has similarly appreciated. However, in addition to the higher home prices, prospective buyers must contend with mortgage rates that have more than doubled over the last year. Figure 4 shows how significant an impact this is to the monthly cost. In Q2 2022, the median price for a house sold in the United States was US$440,300.12 For most of 2020 and 2021, 30-year fixed mortgage rates were at around 3.00%. Most recently, the average 30-year fixed rate was 6.70%.13 For a similarly priced home, the higher mortgage rate increases the monthly payment in this example by US$787.87 or 53%.

Higher mortgage rates are also likely to further limit the supply of houses for sale as anyone seeking to sell their house will also need to take into account that they will be trading a low-interest mortgage for a higher-interest one.

Since the detailed domestic migration data is only available annually, we will need to wait months until we get complete information on what happened this year. However, there is some evidence that prospective buyers are considering buying in some of the cities hardest hit by COVID-19 outbound migration. Realtor.com® reports that in Q1 2022, the percentage of prospective buyers looking to relocate outside of their current home area continued to rise, and New York City and Washington DC made the top 10 for out-of-state searches. The percentage of inbound searches from shoppers in other areas continued to rise in the second quarter, with New York and Washington DC dropping out of the top group to be replaced by San Francisco. However, the majority of out-of-area searchers are focused on smaller, lower-priced areas.14 The fiscal outlook for the large MSAs and their states will be impacted by the decisions these domestic nomads make.

Luke Rogers, “COVID-19, Declining birth rates and international migration resulted in historically small population gains,” US Census Bureau, December 21, 2021.

View in ArticleThe District of Columbia had the largest percent population loss.

View in ArticleJoanna Biernacka-Lievestro and Alexandre Fall, “A Third of States Lost Population in 2021 | The Pew Charitable Trusts (pewtrusts.org)” Pew Charitable Trusts, May 12, 2022.

View in ArticleWilliam Frey, “THE AVENUE: New census data shows a huge spike in movement out of big metro areas during the pandemic,” Brookings, April 14, 2022.

View in ArticleIbid.

View in ArticleIbid.

View in ArticleUS Census Bureau, “Quarterly residential vacancies and homeownership series,” sourced via FRED, accessed on October 6, 2022.

View in ArticleUS Census Bureau, “Quarterly residential vacancies and homeownership, second quarter 2022,” August 2, 2022.

View in ArticleNational Association of Realtors sourced through FRED.

View in ArticleWilliam Frey, “THE AVENUE: New census data shows a huge spike in movement out of big metro areas during the pandemic.”

View in ArticleCBRE, “2022 U.S. construction cost trends,” July 6, 2022.

View in ArticleCensus Bureau and Housing and Urban Development sourced via FRED on October 4, 2022.

View in ArticleFreddie Mac sourced via FRED on October 4, 2022.

View in ArticleRealtor.com, “Realtor.com® reveals top destinations for out-of-state home shoppers,” May 3, 2022; Joel Berner, “Q2 2022 Cross-market demand report: Interstate home shopping reaches new heights as prospective homebuyers seek out affordability,” Realtor.com, August 9, 2022.

View in ArticleCover image by: Jaime Austin