Brazil economic outlook, October 2022 has been saved

Cover image by: Jaime Austin

Brazil’s economy has continued to surprise the upside, with real Q2 GDP coming in stronger than consensus forecasts. The economy managed to grow 1.2% in Q2 alone,1 with consumer spending outstripping declines in government consumption and exports. Moreover, economic growth in the quarter was widespread, with every major industry posting a positive gain. High commodity prices had previously supported growth in Brazil, as the country received higher prices for its substantial exports of oil, iron ore, and agricultural commodities. Unfortunately, many of those commodity prices have come down amid fears of a global recession. The economy is also struggling with lofty inflation and the higher interest rates that come with it. Although inflation has begun to ease and the central bank has paused its rate hikes for now, the economy is expected to slow dramatically into next year.

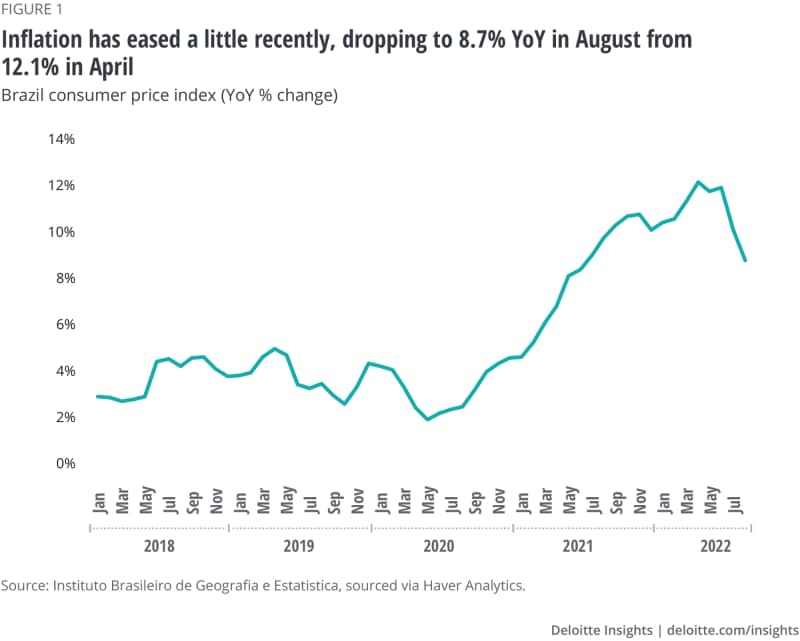

Brazil, like many other economies around the world, is struggling with high inflation (figure 1). Fortunately, Brazil’s central bank, the Banco Central do Brasil (BCB), has been among the most aggressive when it comes to monetary policy, first raising rates in early 2021. Since then, the BCB implemented 12 consecutive rate hikes before pausing in September 2022, with the central bank policy rate ultimately reaching 13.75%.2 Over this period, consumer inflation accelerated to 12.1% year over year (YoY) in April 2022 before easing to an 8.7% YoY rate in August.3 Higher interest rates accompanied by weakening inflation have effectively raised the real (or inflation-adjusted) interest rate. Despite the hawkish policy stance, the BCB may struggle to get inflation back within its target range. The central bank’s own projections show inflation would remain above the upper target range until Q4 2023.4 Some members of the Monetary Policy Committee, which sets interest rates, preferred to raise rates again in September to better tackle inflationary pressures.

One of the challenges the BCB is facing is that the disinflationary pressures seen in the second half of this year were largely due to fiscal policy interventions.5 Recently enacted tax cuts and subsidies for fuel have dramatically lowered transportation costs. For example, transportation costs were up just 7.6% YoY in August, which is a notable moderation from a 20.1% YoY reading in June.6 Such fiscal interventions are to expire after the runoff presidential elections scheduled for October 30, removing this key source of disinflation. Another major source of disinflation has come from lower energy prices, including a sizable drop in the cost of residential electricity. The war in Ukraine and the global economic outlook are highly uncertain factors that will ultimately determine the cost of energy worldwide and in Brazil. The related price drops could reverse should the war in Ukraine worsen or if the global economic outlook improves.

The BCB will need to see continued evidence that lower inflation is here to stay. Pushing inflation expectations down to its target rate will be critical for the BCB to feel confident that lower inflation is persisting. Inflation expectations have come down a little, but at 9.9% for the next 12 months,7 further moderation of expectations will likely be needed to bring inflation back within target. Ensuring that external events do not generate inflationary pressure at home will also be critical. The hawkish response from the BCB supported the value of the currency. However, with the BCB on hold as other central banks turn more hawkish, the currency could depreciate further, creating upward pressure on import prices and therefore inflation. Indeed, the Brazilian real weakened slightly between August and September8 as the global outlook worsened and central bankers upped their hawkish rhetoric and policy.

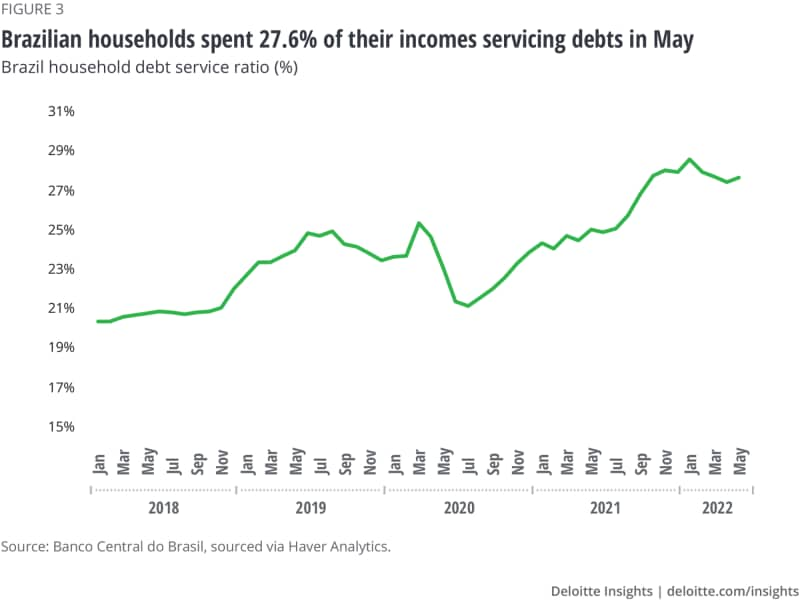

One of the strongest upsides to Brazil’s economy has been from exports. In August, year-to-date goods exports were up 19.1% in US dollar terms from the same period a year earlier (figure 2).9 High commodity prices and strong global demand for goods allowed Brazil’s exports to surge since the pandemic hit. However, export growth is expected to come down. A weaker global economic environment, the threat of global recession, and the related drop in commodity prices will all lower demand for Brazil’s exports. Brazil’s largest exports, which include iron ore, crude petroleum, and soybeans, have all posted price declines this year.

One possible support for exports is demand from China, which is by far Brazil’s largest export market accounting for more than a quarter of its goods exports.10 After relatively weak growth this year, China’s economy is expected to accelerate next year, which could support demand for Brazilian exports. Historically, more than half of Brazil’s exports to China are crude petroleum and soybeans. Although the prices of these commodities may slip further, China may purchase a larger volume of these goods from Brazil. However, exports of other commodities, such as iron ore, which account for roughly 20% of Brazil’s goods exports to China,11 are unlikely to rebound. China’s rapidly growing property sector required large volumes of steel and iron ore to make it. Unfortunately, China’s property market ran into trouble last year and will no longer act as an engine of economic growth. Other types of infrastructure investments in China could support demand for Brazil’s commodities, but so far, infrastructure investment has been unable to make up for the decline in the property construction market.12 This casts doubt on the narrative that China can offset the coming decline in demand for Brazil’s exports.

Brazil’s fiscal health improved earlier this year. In the 12 months ending in July, the general government primary surplus, which subtracts interest expenses, had grown to 2.5% of GDP.13 Revenue has been relatively strong thanks to high commodity prices and a tightening labor market. Unfortunately, commodity prices are already coming down and a weakening global economy will hit export volumes, lowering revenues from imports. Government spending will also need to drop next year. The fiscal stimulus enacted earlier this year will have to be reversed after elections as the measures were meant to be temporary. Plus, the interest expense on government debt reached 6.3% of GDP in the 12 months ending in July.14 Interest expense could rise further if the central bank is forced to resume its rate hikes. Maintaining a sizable primary surplus will likely be necessary to reduce this lofty interest expense and ultimately free up government revenue for more productive uses.

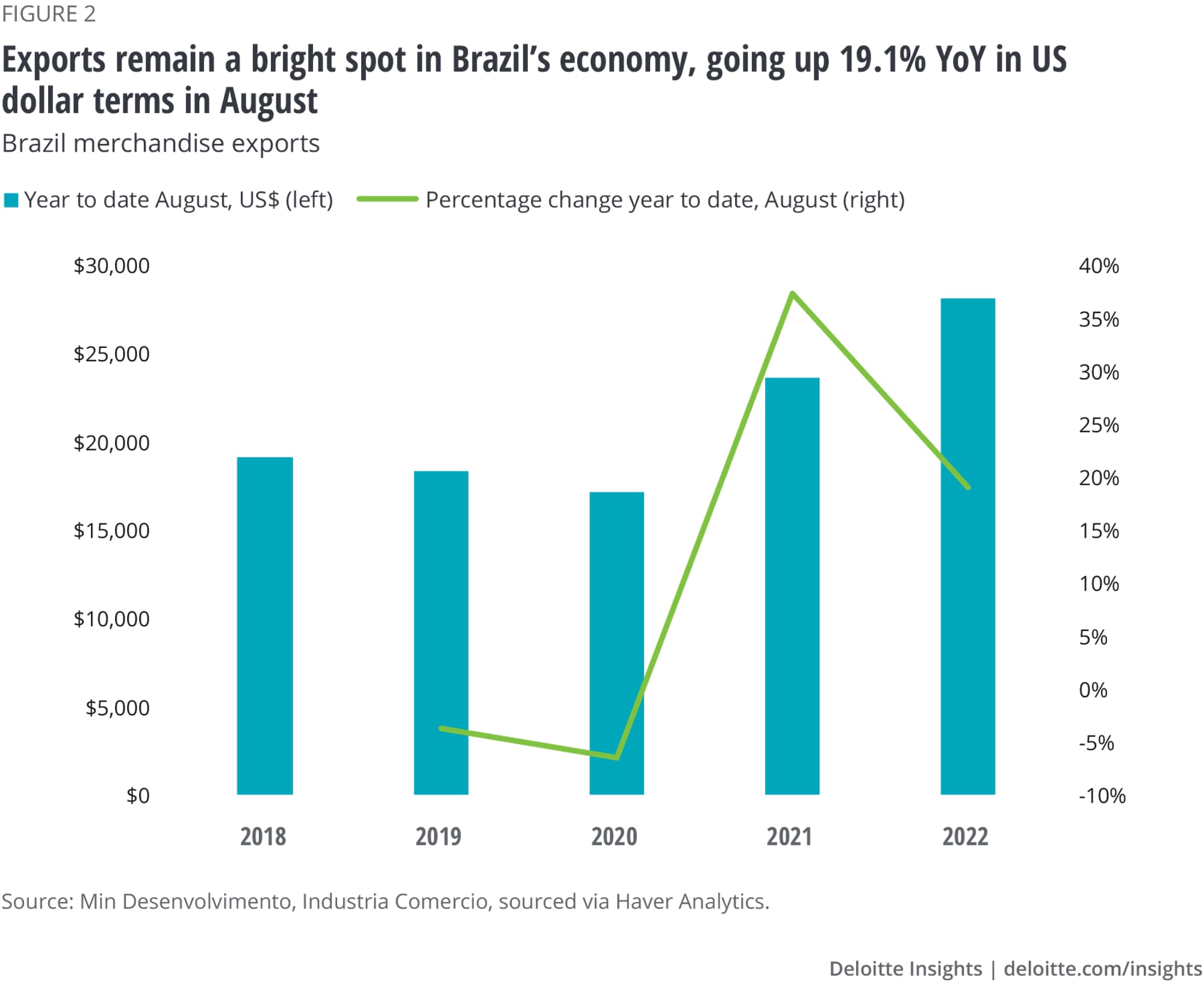

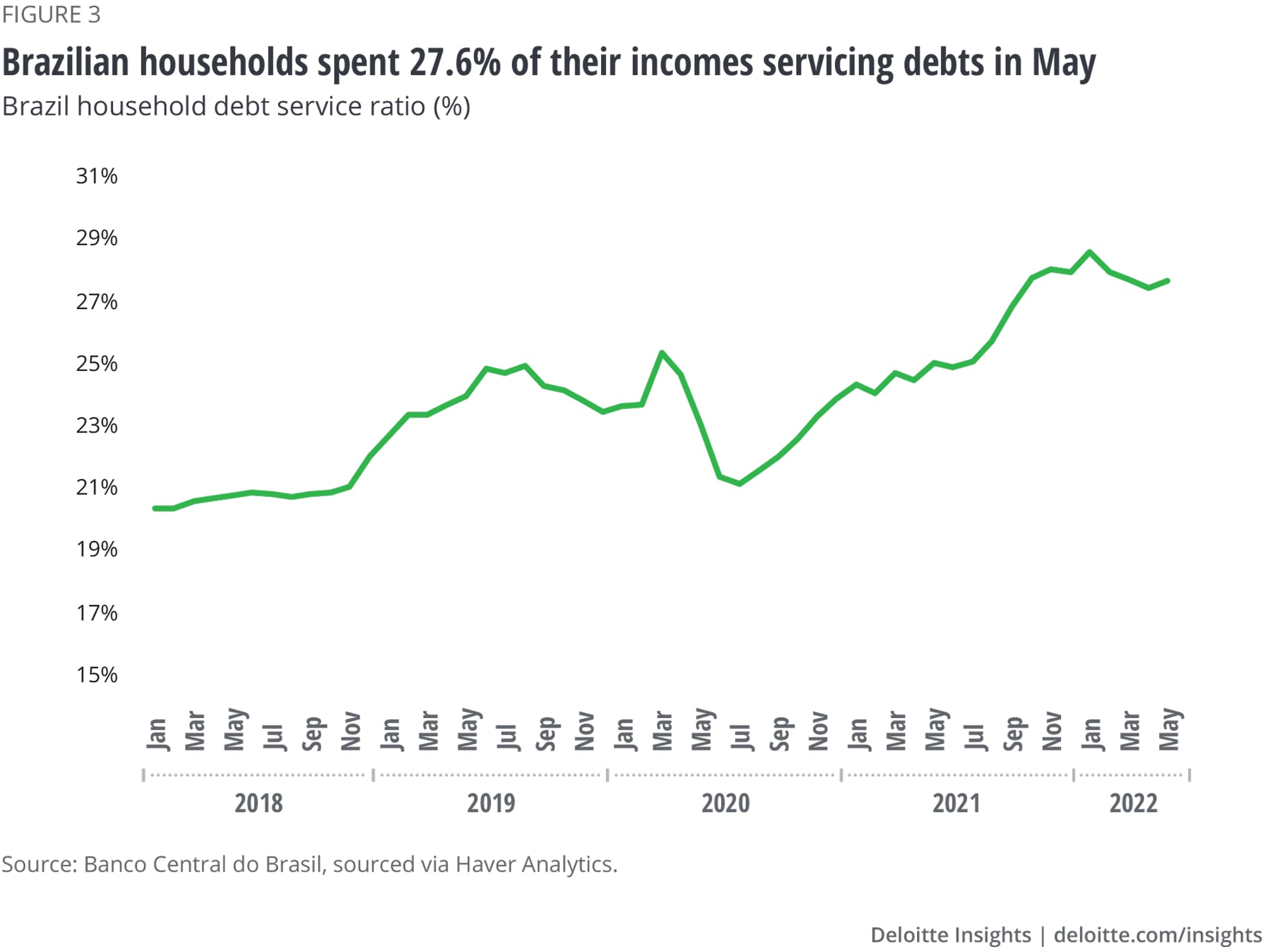

Governments are not the only ones struggling with their debt burdens. Households spent 27.6% of their incomes servicing debts in May (figure 3). Although this is down slightly from the January peak of 28.5%, it remains well above historical norms. For example, as recently as 2018, the household debt service ratio was 20.8%.15 Fortunately, conditions for households have improved. The unemployment rate dropped to 9.1%, the lowest reading since 2015, and total employment is well above its prepandemic peak.16 As unemployment has come down, wages are beginning to pick up. Even inflation-adjusted average earnings began to rise this year. As a result, consumer confidence has improved, suggesting that real consumer spending could strengthen into the end of the year.

In closing, with inflation finally waning, Brazil’s economy should be well positioned for stronger real growth. Improvement in the labor market, higher consumer confidence, and a pause in interest rate hikes should support domestic demand. However, the external environment is deteriorating. A global recession would zap exports, which had been an engine of growth since the pandemic hit. Plus, fiscal belt tightening, although necessary, will ultimately restrain GDP growth next year. Government support to the economy will be difficult to come by given the large sum of money it has to spend to service its existing debts.

{kind=link}

{kind=link}

{kind=link}