India economic outlook, April 2023 has been saved

Cover image by: Jaime Austin

Policymakers the world over are currently facing a predicament. The last two years have seen the global economy struggling to deal with overlapping crises, the latest being the liquidity troubles after a series of global bank crises. While the impact appears to have been contained, these uncertainties continue to undermine the confidence among consumers and businesses to spend, therefore impacting economic growth.

The World Bank now fears that the ongoing slump in global economic growth will likely result in a “lost decade.”1 Despite this gloom, many market analysts believe that this could well be India’s decade.2 And there are enough reasons and data to back this claim. Recent data revisions by India suggest the economy has fared better than previously believed despite continuing global uncertainties. The International Monetary Fund (IMF) expects India to grow by 5.9% in FY 2023–24 and by an average rate of 6.1% over the next five years.3

While betting on consumption-driven growth is obvious given India’s large, young, and rising share of the upper middle–income population (with a high propensity to spend), we believe that investment will play an important role over the next two years. It is investments that will provide India with necessary momentum to take off on a path of sustained domestic demand–led growth for decades to come.

However, capital investment, especially in the private sector, has lagged so far. India is an attractive investment destination is a point well emphasized. The question is, why has private investment not yet picked up sustainably, and what can policymakers do to take advantage of this window of opportunity?

In this outlook, we focus on answering these questions. It’s true that there’s no prescribed policy intervention for policymakers to follow because of imprecise and volatile information available to them, thanks to constantly changing economic dynamics. That said, the government must continue calibrating policies and trying out new approaches to boost investments, as it has done in the past. A three-pronged approach will persuade investors to invest in capacity-building.

Our overall outlook for the Indian economy remains positive: We expect investments to see a turnaround and thrust the economy into sustainable growth. India will likely grow at a moderate pace of 6.0%–6.5% in FY 2023–24, as the global economy continues to struggle. Growth in the next year will likely pick up as investments kickstart the virtuous circle of job creation, income, productivity, demand, and exports supported by favorable demographics in the medium term.

It looks like the world has come out of the shadow of the pandemic and has, in fact, learned to live with it. However, geopolitical crises, supply chain reorientations, global inflation, and tight monetary policy conditions will weigh on the outlook. We have delved into these challenges in detail in our previous outlooks.4

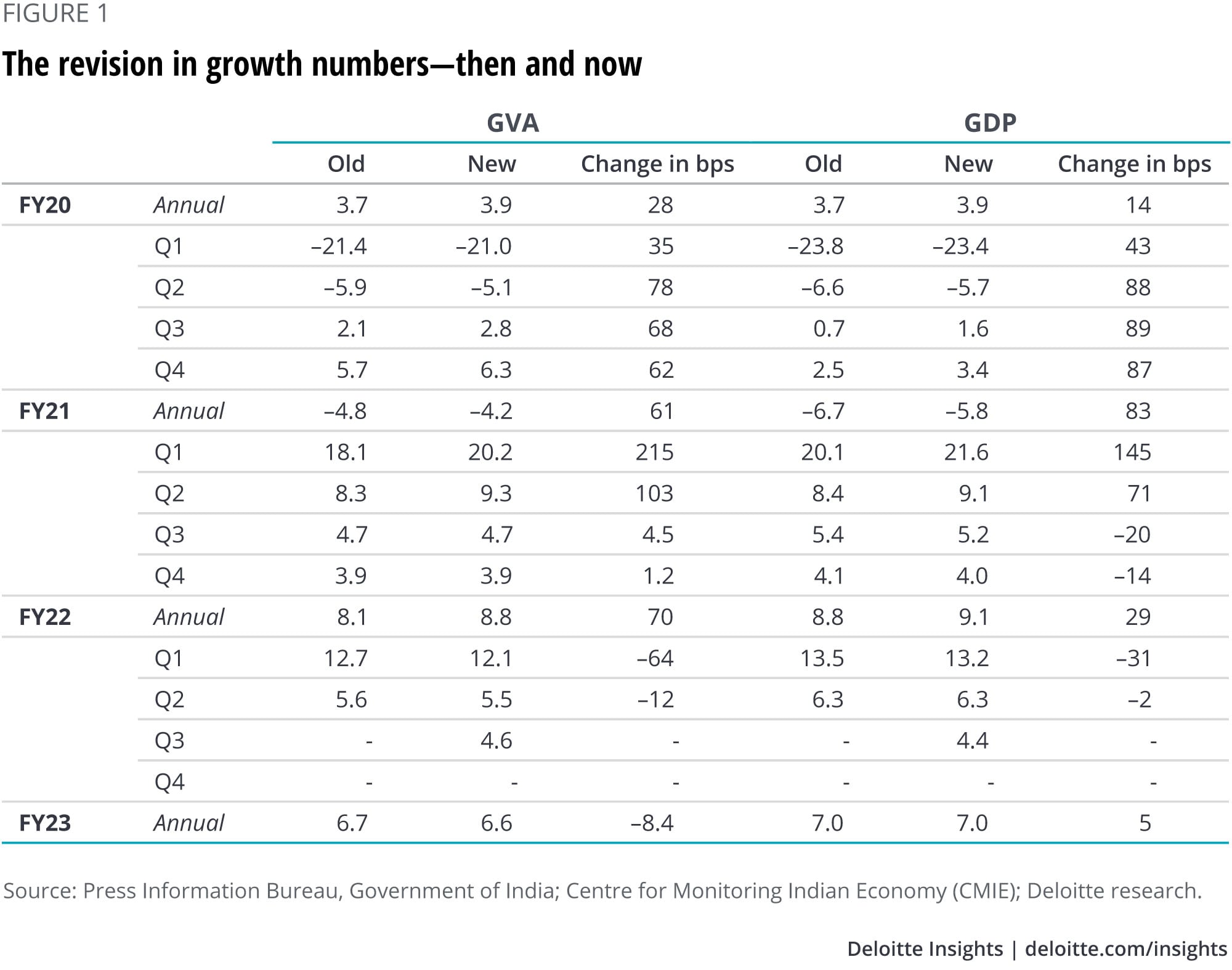

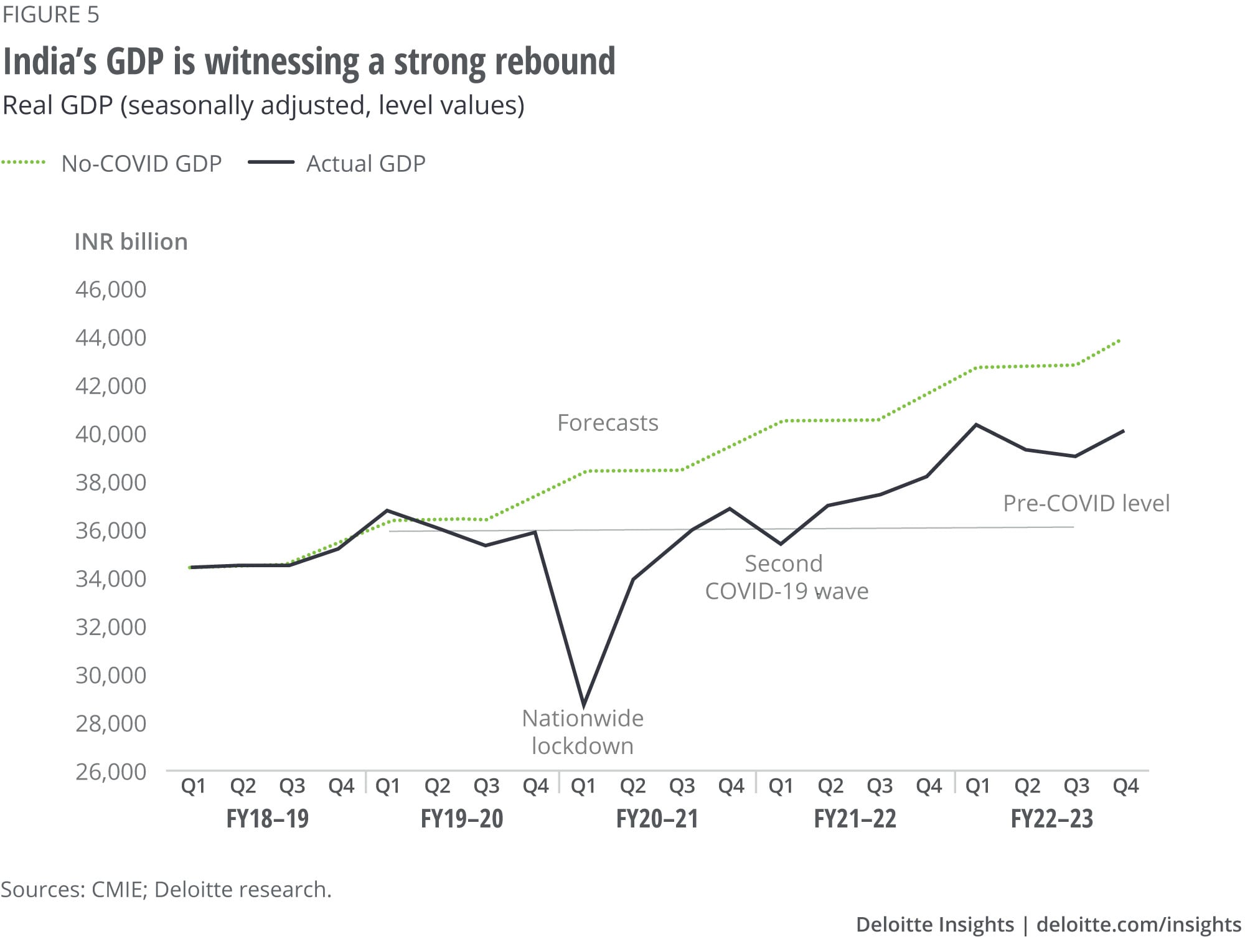

India recently released GDP estimates for the October–December quarter of FY 2022–23 (Q3) along with revisions of the past three years’ data. GDP data suggests that India emerged stronger from the pandemic than initially assumed, with growth gathering steady momentum since FY 2022–23 (figure 1). GDP growth for FY 2020–21 was revised up by 0.77 percentage points, implying the recession was not as deep as previously thought. For FY 2021–22, meanwhile, growth was revised up from 8.7% to 9.1%, suggesting stronger rebound. This upward revision was primarily because of the stronger-than-anticipated growth in manufacturing and construction.

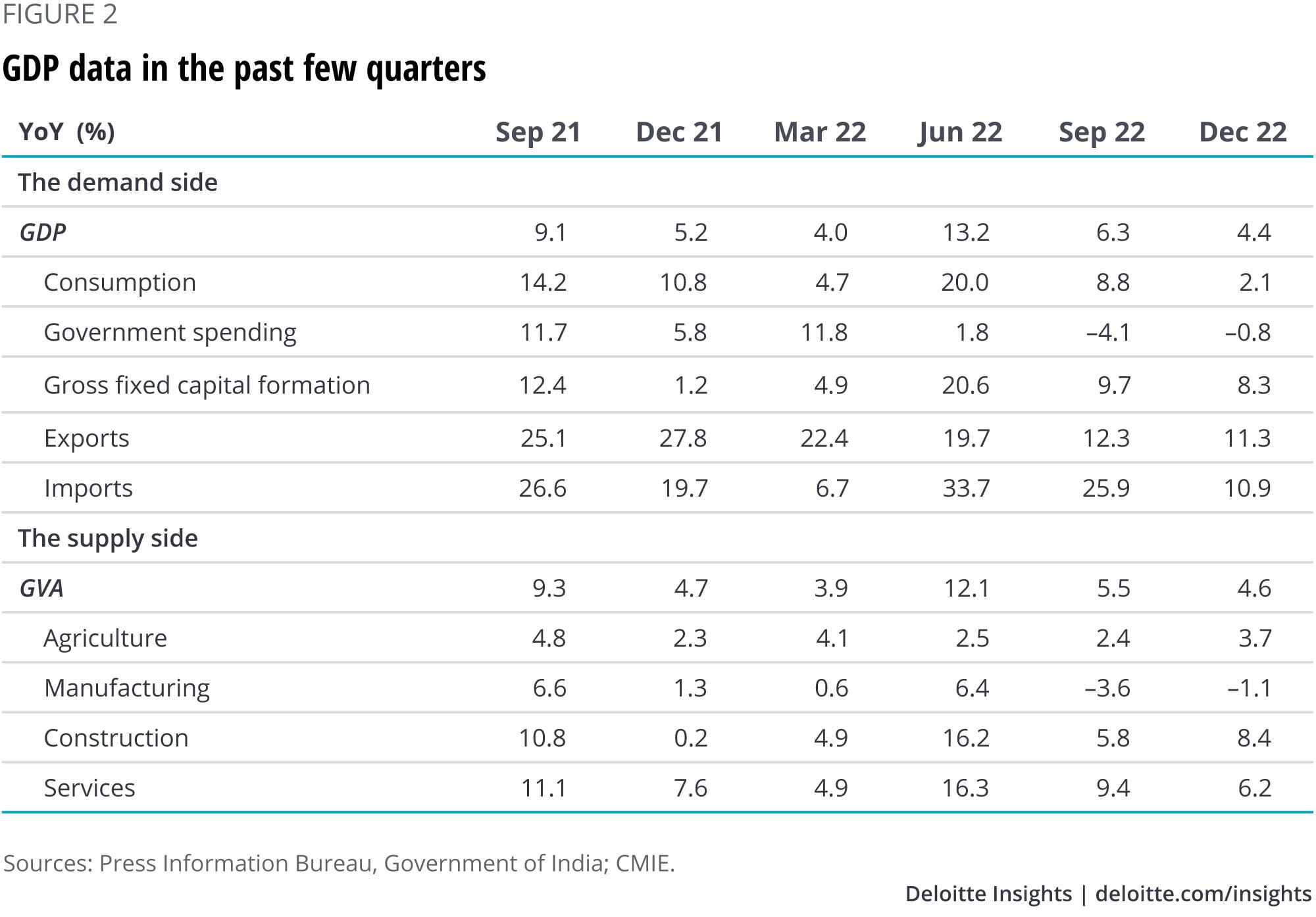

Data for the latest quarter (Q3) points to 4.4% year-over-year (YoY) growth in Q3, which is close to what we had estimated (4.5% YoY) in January (figure 2). Although it appears to be the weakest quarter of this fiscal, the significant upward revision of last year’s data increased the base for this year’s growth estimates.

Two observations are worth noting: Despite the global slowdown, exports performed well, probably because of the depreciated currency against the dollar. While goods exports remained modest, India’s services exports skyrocketed by 30% between April and February. A strong digitization drive the world over, cost-cutting measures by businesses to deal with the impending slowdown, and the growing trend of remote working increased demand for exports of services in technology, where India has a comparative advantage. Interestingly, the share of business and professional services in total services exports also increased as companies globally now prefer outsourcing a wide range of professions, such as accounting, audit, R&D, quality assurance, and after-sales service.

Second, the past few quarters’ data point to fiscal prudence and discipline as government spending contracted for the second consecutive quarter. GVA growth in public administration services also fell. In the first 10 months, the fiscal deficit accounted for 67.8% of the target deficit of this fiscal year. The government’s effort to consolidate its expense instils confidence that it may reduce the fiscal deficit to below 4.5% by 2025–26, with a fairly steady decline over the period as charted in the budget this year.5

Growth in investments will be critical to meet India’s rising demand and ensure noninflationary growth in the long run. The inability to build up capacity would mean that India will have to suppress demand, failing which will result in inflation spiraling up. The challenge is several headwinds have kept investors at bay, and may likely continue doing so, at least in the near term.

We consider three downside risks emerging from:

Rapidly tightening monetary policies across industrial economies have led to a global liquidity freeze and tighter credit conditions, making it expensive and difficult for businesses to borrow. Global uncertainties and geopolitical shifts have restructured supply chains and altered trade flows and relationships. All of these have led to lower visibility of future demand for products and services, thereby deterring investors to incur large expenses on futuristic projects.

Production costs, meanwhile, have escalated because of supply chain issues and rising energy prices, resulting in bearish investor sentiment. The shift toward sustainability and alternate renewable energy sources, albeit gradual in the initial years, is adding to costs. Several nations have accelerated their efforts toward energy transition to reduce dependence on conflicted geographies for energy requirements and carbon footprint. The nature of such transitions is likely to be expensive in the near term. This is because the world’s energy demand will be met with supply constraints as investments in conventional energy sources fall. At the same time, the shift toward renewable sources will be gradual because of the gestation lag of investment and the lack of mass economies.

For India, which has been battling higher prices for years now, sustained pressure on global prices may not bode well for the investment outlook. Recent earning and equity price data suggests that inflationary pressures have impacted profitability and margins.

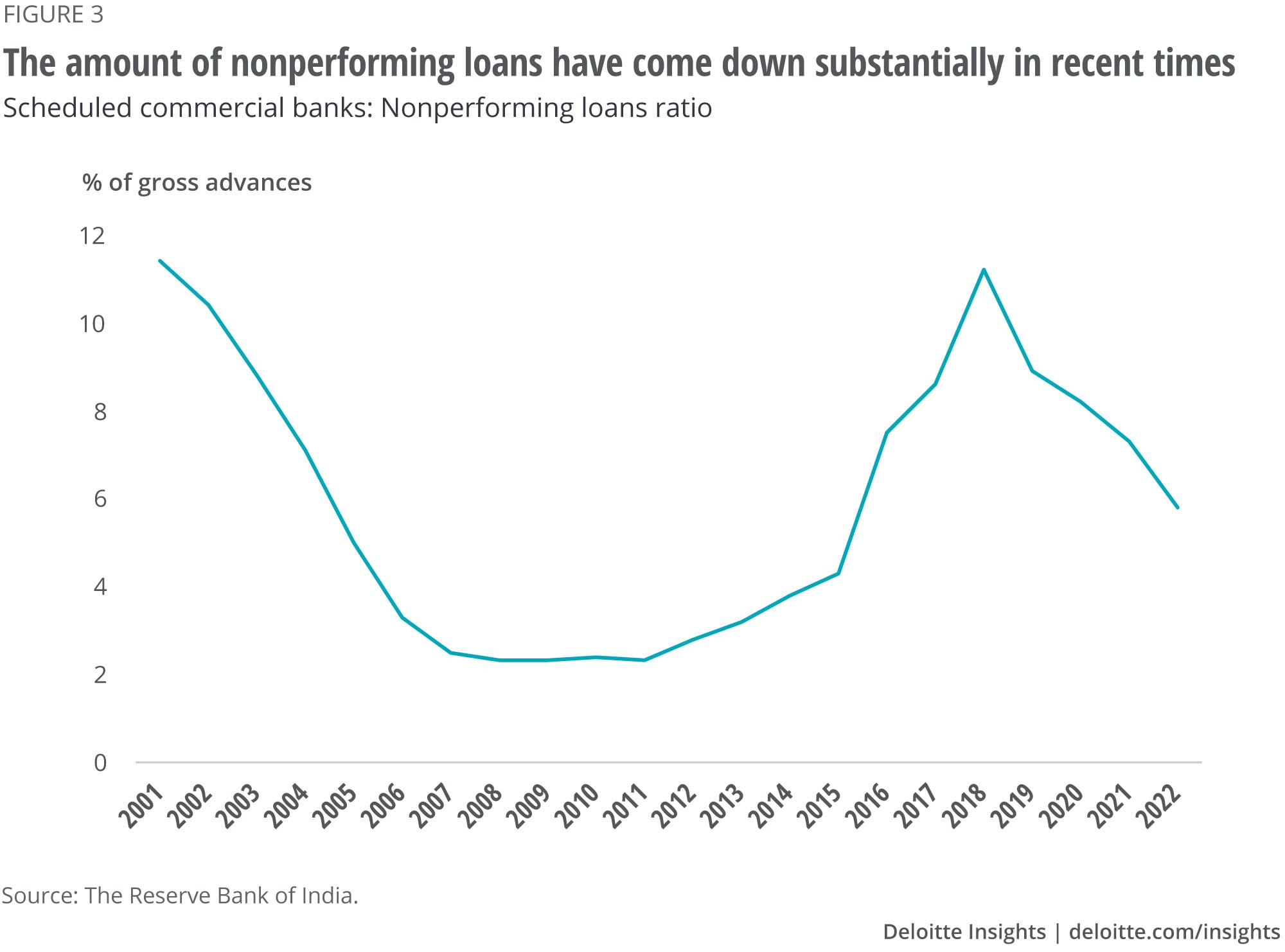

But not all is gloomy. Corporate profits are up because of rising prices. Deleveraged balance sheets have improved businesses’ ability to invest. Even banks have healthy balance sheets: With nonperforming assets coming down and margins witnessing an improvement due to rising policy rates, banks’ willingness to lend has gone up substantially (Figure 3). In fact, there are cues, such as the widening saving-investment gap and the highest capacity utilization of manufacturing firms since prepandemic times, suggesting that India may be at the cusp of private investment revival.

Undoubtedly, the Reserve Bank of India (RBI) has shouldered a major responsibility of cushioning the economy from rising prices and maintaining liquidity. Yet, navigating inflation and preserving financial stability, while boosting growth drivers, have been a tightrope walk for policymakers.

We expect the government to focus on a three-pronged strategy:

A well-balanced monetary policy: Amidst inflation concerns, the RBI is unlikely to let its guard down and will keep the monetary policy tight. The downside of the move is that higher policy rates will raise borrowing costs, which will in turn moderate credit growth (although it is very strong relative to the past five years).

While prioritizing stability is the need of the hour, the government cannot afford to overlook growth. India needs investments to remove supply bottlenecks and meet the rising demand. Low credit availability will impact capacity-building. In short, too much tightening will result in a vicious circle of low credit availability, investment, and supply, thereby causing further inflation. The RBI’s latest move to halt the rate-hike cycle is an indication that the RBI also wants to keep economic growth into consideration as it aligns inflation with the target.

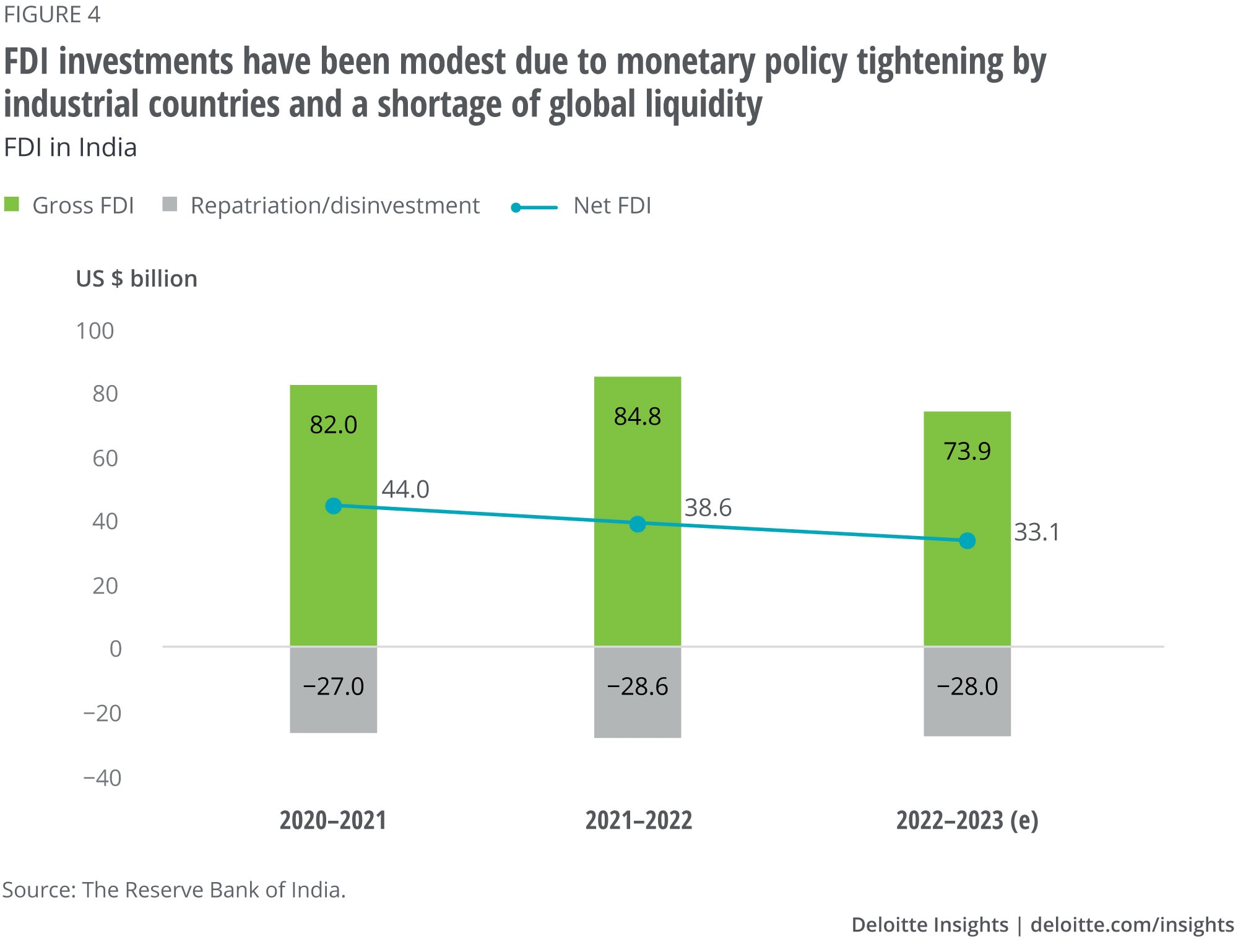

Amplify efforts in spending on infrastructure while consolidating expenses: Over the last year, investment flows from abroad have remained modest. The drying up of global liquidity due to tighter monetary policies in central banks across industrial countries resulted in low gross inward FDI to US$61.5 billion during 2022–23 (April 2022–January 2023) from US$70.5 billion a year ago (figure 4).

The investment gap caused by low private and foreign investment has to be filled by the government through higher spending on infrastructure and improving the logistics ecosystem. Initiatives such as the National Infrastructure Pipeline, PM Gati Shakti, and National Logistics Policy (NLP), among others, are efforts in that direction. These will also improve logistics costs and efficiency and crowd in private investment. Thankfully, a study by the State Bank of India suggests that capital productivity has improved significantly over the last decade, and hence, any incremental investment spending will generate much larger output than it did in the past.6

Capitalize on services as manufacturing ramps up: Emphasis on manufacturing and initiatives such as production-linked incentives will attract investment and those efforts must continue. At the same time, the government must take advantage of the rising demand for services worldwide. The services sector has shown promising growth in exports lately, thanks to global digitization efforts and greater acceptance among multinationals (MNCs) to run operations remotely. India must reap benefits where it has a comparative advantage and build a robust and efficient ecosystem to bring more MNCs to its shore. This will have a spillover on investments in the manufacturing space as well.

We are positive that investments will likely see a turnaround soon. In fact, the next two years will be crucial for investment to gain momentum before the economy takes off on a sustained and rapid growth path. High-frequency data—for example, electricity generation, GST collections (through e-way bills), average fuel consumption per day, sale of two-wheelers and tractors, credit growth across sectors and industry, occupancy rates in hotels, and the purchasing managers’ indices (PMIs)—clearly indicate that growth drivers have maintained a positive momentum despite uncertainties.7

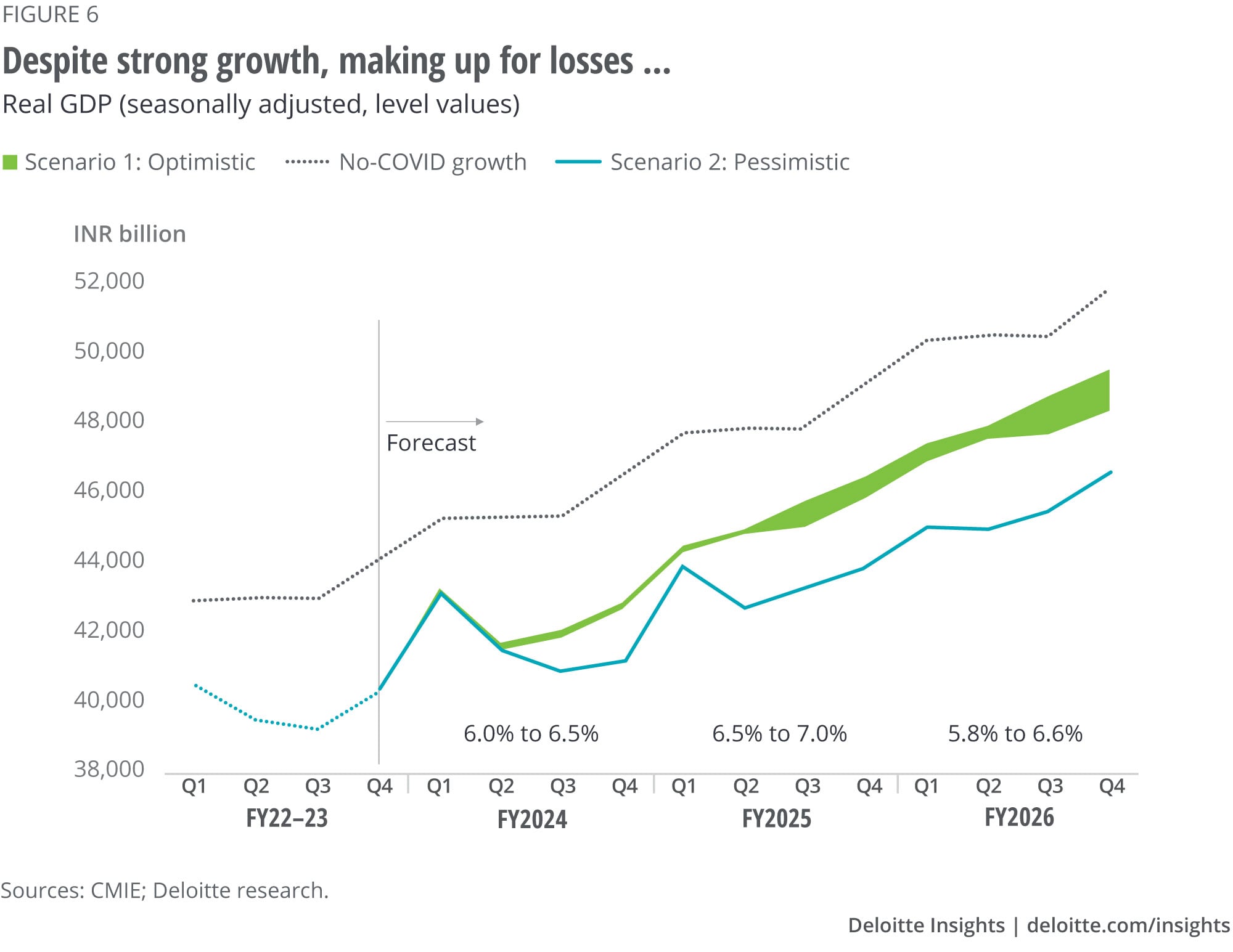

As always, our estimates for GDP growth account for uncertainties. We expect the economy to grow 6.0%–6.5% during FY2022–23 in our baseline estimate followed by growth ranging 6.5%–7.0% the following year. We expect growth to stabilize around 6.5% in the medium term as global economy turns buoyant (figures 5 and 6). Economic activity will likely pick up rapidly later this year, contingent on the revival of the global economy and improving economic fundamentals. However, if downside risks weigh on the economic fundamentals and outlook (listed in the assumptions below), we may see a substantial economic slowdown. (For more on our optimistic and pessimistic scenarios, see “Key assumptions”).

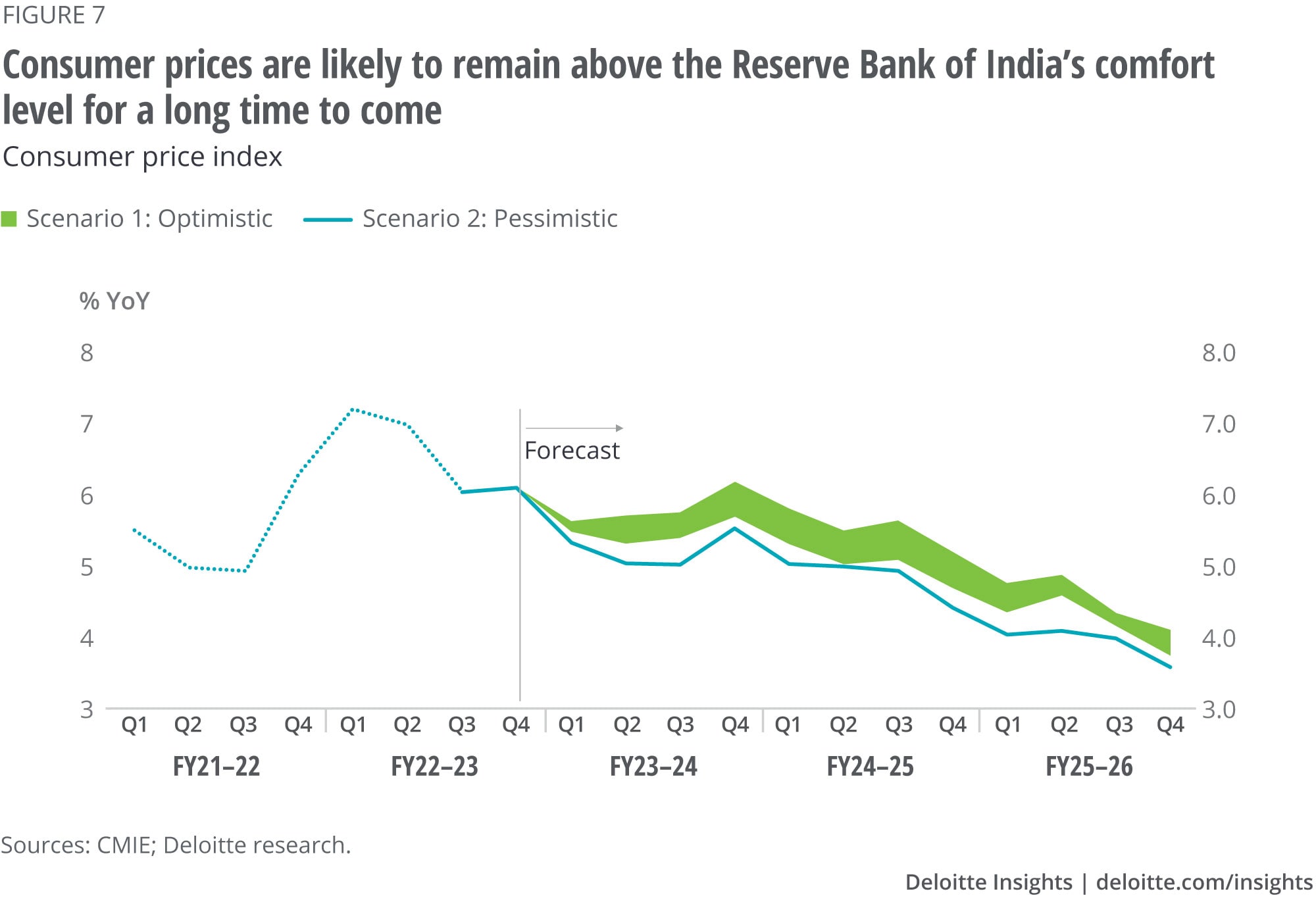

Inflation may peak along with the moderation of the global economy and stability in crude oil and industrial raw material prices. A tighter monetary policy will also help bring down demand and, therefore, cap the price rise. However, the fall in prices may be short-lived as we expect demand to remain high. The recent unseasonal rains (impacting wheat production and its procurement) and the possible impact of El Nino on monsoon rains may further add pressure to food prices in the months ahead. Despite a sooner turnaround in investment, its lagged impact on capacity building will likely constrain supply in the short run. We expect prices to remain in the upper range of the RBI’s target band over the next two years (Figure 7).

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}