India A long, winding, and uncertain road to recovery

8 minute read

18 September 2020

After reporting a steep drop in GDP, can India turn crisis into opportunity and emerge stronger on the other side of the pandemic?

Hit by COVID-19, economies across the globe are discovering that the road to recovery is bumpy. India is no exception. The extent of contraction in its GDP in Q1 FY2021 reflects the severity of the blow to its economy due to the pandemic-induced lockdowns and social distancing norms between March and May. While the staggered reopening of the country over the following months improved economic activity, concerns around the sustainability of this early rebound remain.

Uncertainties around COVID-19 continue to abound. Building a stronger infrastructure and social capital, such as the health of people and industries, will likely drive resilience.

A contraction never seen before

Learn more

Explore the Economics collection

Learn about Deloitte's services

Go straight to smart. Get the Deloitte Insights app

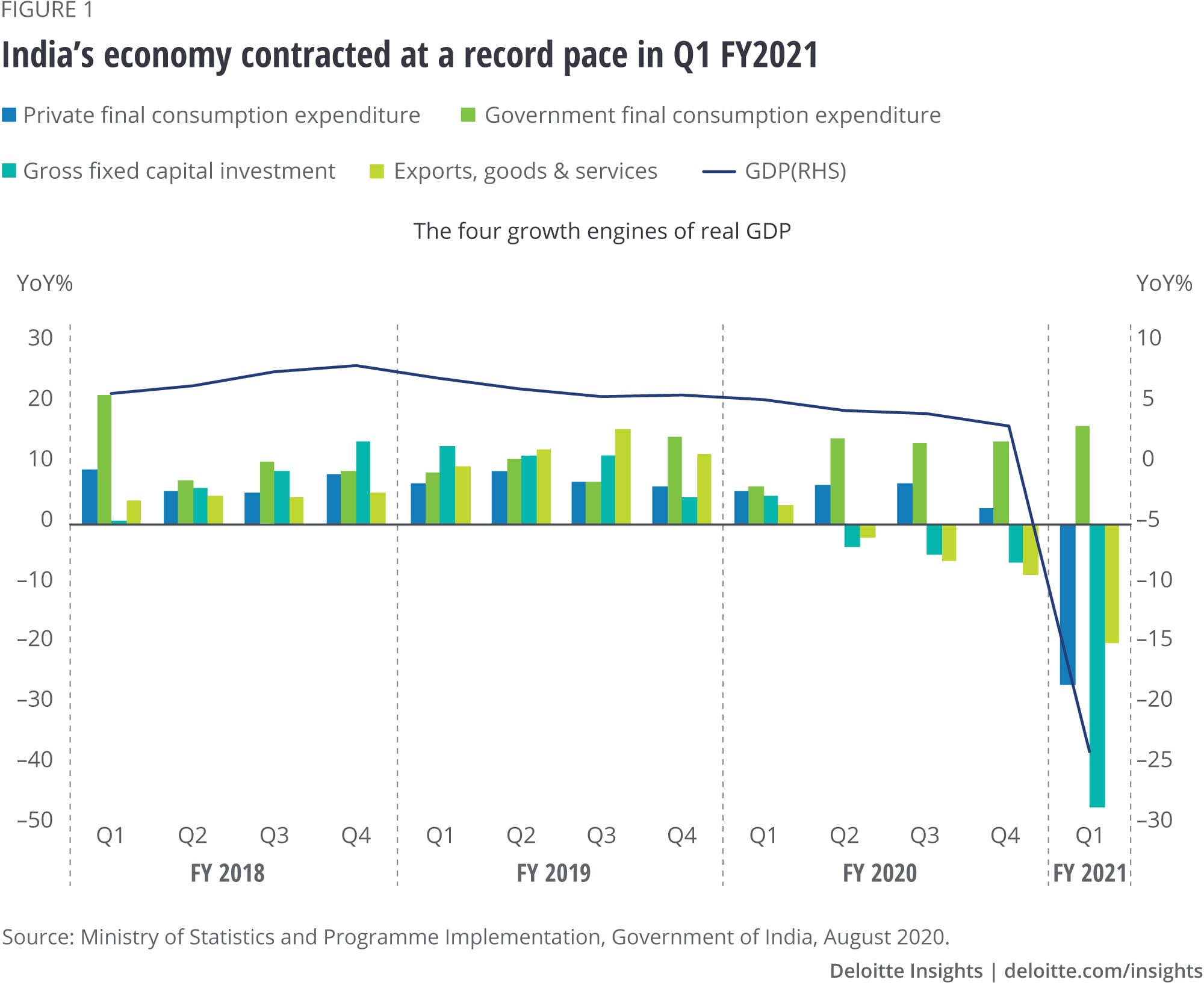

India’s economy had been slowing down for over seven quarters even before the pandemic (figure 1). Investments and exports were contracting and it was government spending that boosted growth to compensate for the declining private sector demand.

And then came COVID-19, causing the GDP to decline by 23.9% year over year1 in the first quarter (April to June) of FY2021 (figure 1)—the largest GDP contraction recorded in a quarter since India began reporting quarterly data (in the mid-1990s). While supply-chain disruptions and closure of factories and industries led to a reduction in gross fixed capital investment by 47.1%, private consumer spending also dropped by 26.7%. The falling volume of global trade reduced exports (by 19.8%), which had been contracting for over four quarters. The drop in imports was even more severe (by 40.4%) compared to exports primarily due to falling domestic demand and oil prices.

The government intensified its effort to cushion the economy from the impact of the pandemic and announced economic stimulus packages.2 Consequently, government’s final consumption expenditure increased by 16.4% as it incurred unplanned spending.

On the industry side, real gross value added fell by 22.8% in Q1 FY2020. All sectors, except for the agriculture, forestry, and fishing sector, were hit hard because of the nationwide lockdown. Growth in the manufacturing and construction sectors plunged by 39.3% and 50.3%, respectively, while the overall services sector contracted by 20.6%. The silver lining was the robust growth in the agriculture sector (by 3.4%), which performed better due to a good monsoon and many migrant workers taking up farming in rural areas upon their return from cities.

Within services, the trade, hotels, transport, communication, and services related to broadcasting sector was hit the hardest and contracted by 47%. The hospitality and transport subsectors were among the first few that felt the immediate impact of the virus and are yet to show signs of revival due to intermittent lockdowns and reduced social interactions. The financial, real estate, and professional services sector declined by 5.3%. Reasons for this drop include supply disruptions across industries spilling into the financial subsector, thereby adding stress on lenders’ balance sheets, and remote work affecting professional services. The impact on the financial sector isn’t usually immediate, so the true impact of the pandemic may reflect in the following quarters. The public administration, defense, and other services sector declined by 10.3% due to higher spending on health care services and support to disadvantaged sections of the population.

The nonfarm private sector GVA (excluding contribution from agriculture and government services) shrunk by 29.6% in Q1 FY2020. The decline in this quarter is so severe that it will take a while for the economy to recover. Sustainable growth is expected to set in motion only in FY2022.3

Events around the global and domestic economy and infection spread are evolving rapidly and high-frequency data suggests the worst is probably over. Supply-side activities are resuming gradually, with every phase of the economic unlock being designed to limit economic disruptions. The initial pent-up demand has also aided the economic rebound as seen in the months following the unlock (figure 2).

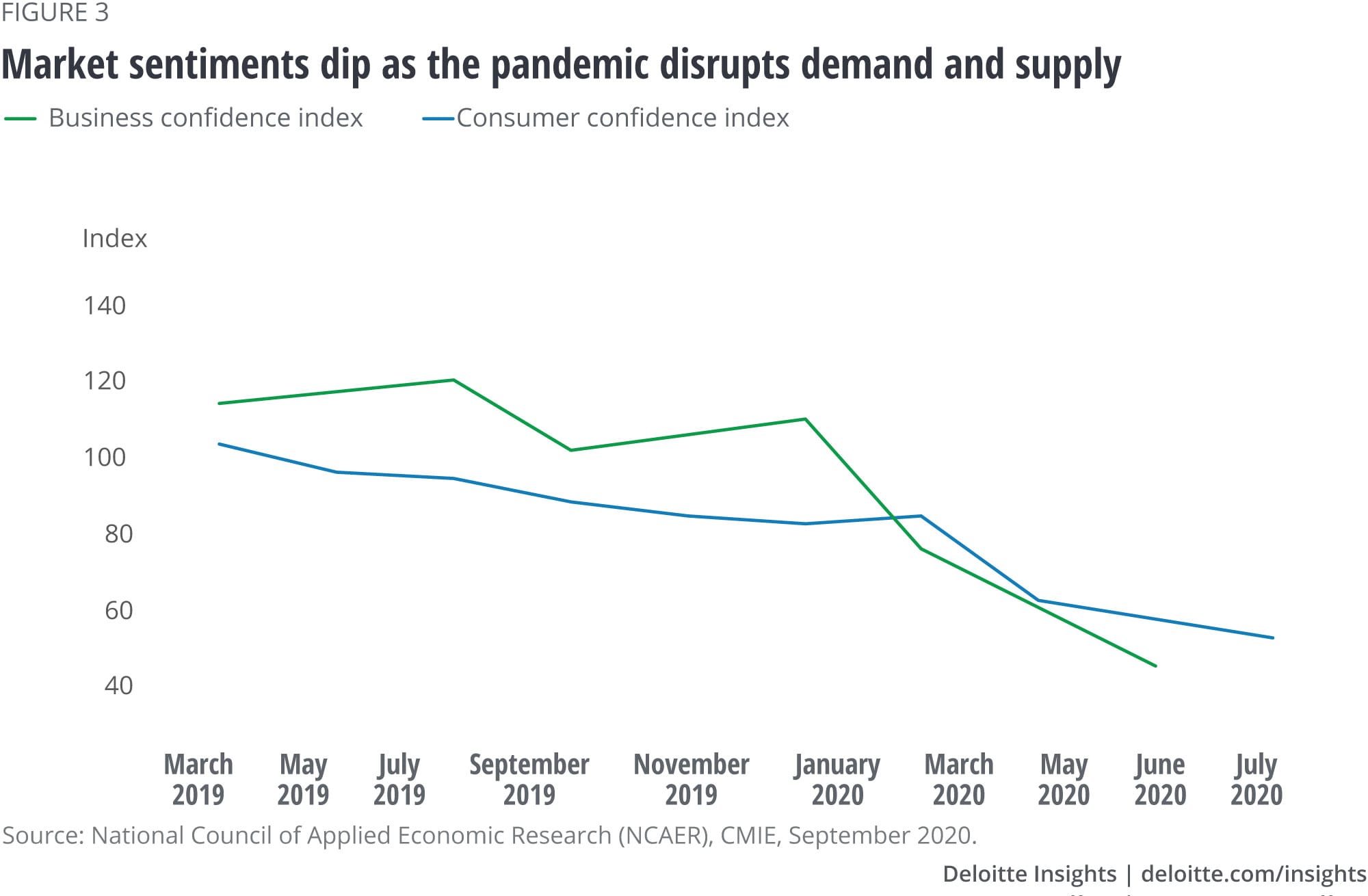

However, activity remains far below the pre-COVID levels (figure 2). The rising number of infections, intermittent regional lockdowns, and social distancing norms have affected domestic demand. According to Deloitte’s consumer behavior survey, uncertainties around employment and financial anxieties have reduced the spending intent among Indian consumers on discretionary goods.4 Lower demand is translating into constrained business investment in capital projects and delay in hiring, thereby creating a vicious circle of low demand and supply. Low confidence among consumers and businesses, as seen in figure 3, will likely keep the economic rebound gradual.

Factors that will ride the economy to recovery

The path to recovery will depend on how long the pandemic lasts. The availability of treatment and vaccines will be key and the sooner people have access to either of these, the quicker will be the economic revival. This is because the rapid spread and longevity of the virus are slowly leading to another contagion—of caution and fear. Anxiety about health, employment, and finances among consumers may change their consumption behaviors and demand patterns, while businesses may modify their practices, leading to rapid automation or business models such as reshoring.

The supply constraints are easing. However, a prolonged pandemic and the possibilities of several outbreaks (as seen in several countries recently) will have implications on the intensity of the supply-chain disruptions (due to intermittent lockdowns), business transformations, productivity, capacity building across industries, and financial sector fragility. These will determine the pace at which industrial production and investment return to normal.

The biggest uncertainty is around private demand recovery. Modest global growth, a lack of coordination among countries to curb the infection from spreading, and the fact that different countries are at different pandemic stages will influence trade and mobility, and therefore, demand. Within India, rural demand may hold up for some time because of a good monsoon and the government’s support to provide employment opportunities in rural areas. In contrast, the increasing levels of infection in urban areas may keep demand subdued. That said, the oncoming festival months may generate enough demand to keep the wheels of the economy moving till the end of the year.

The extent and effectiveness of the fiscal and monetary stimulus by the government will be crucial in reducing the pandemic’s impact on the economy. So far, the government has announced two stimulus packages of over 10% of GDP to help people and businesses respond to the crisis. Fresh measures aimed at improving infrastructure, regulations, and job opportunities and their timeliness will likely aid in sustained economic recovery and rebuilding.

But, how much can the government spend?

Does the government have funds to support the economy continuously? What if the pandemic sustains for over a year? For three reasons, government spending and allocations will likely be prudent going forward. First, India is a resource-constrained nation, so it does not have endless resources to spend. Second, there is evidence that a big bang stimulus may not significantly help the vulnerable population (as seen in the United States) and pull the economy out of a recession (as witnessed in Japan).5 Third, every expense India makes today will come at a cost of higher borrowing, debt, and deficit, which will impact the nation in the long run.

Why is that so? When the pandemic is over, many other peer nations will also see a rapid revival simultaneously. Many Asian nations are much ahead of India in the recovery path. At that time, India’s high deficit and debt with an imprudent consolidation plan may impact investor confidence. This could translate into capital outflows, currency depreciation, a fall in reserves, a spike in inflation (due to imports getting pricier), and higher interest spending by the government on loans borrowed externally. Policymakers may have to raise taxes and reduce capital spending to stem economic instability. In short, a stimulus will help in the short run, but may not in the long run.

Crisis—an opportunity to switch gears?

With adversity, comes opportunity. As policymakers and businesses respond to this crisis, they will require resilience to prepare for uncertainties in the months ahead to recover, and then, thrive. It’s important to understand the emerging new norms and tap into opportunities that these trends present.

For policymakers, this could be the opportunity to increase capital spending to boost productivity, create assets, and monetize those assets to generate revenue. India has to scale up its physical and social infrastructure significantly to compete with its global peers. Spending on infrastructure and health care will likely address the demand uncertainty challenge, thereby generating employment for low-skilled employees, improving private sector performance, and increasing activity among small and medium enterprises. The Indian government has already set the ball rolling by announcing one of the largest and ambitious infrastructure projects earlier this year.6 It is also undertaking many projects planned earlier and reviving a few stalled ones.7 In terms of long-term measures, the government has to maintain the reform momentum that strengthens the institutional structure to improve efficiency and transparency. By addressing structural logjams (related to environmental and other regulatory clearances), complicated tax processes, labor challenges, land acquisition, etc., the government can attract investors who are looking for alternate manufacturing destinations to diversify their supply chains and reduce costs.

At the same time, businesses could invest in improving their skill base and in emerging opportunities such as digitization and consolidation to improve productivity and address new markets. This could also be the time to rethink sourcing plans and reorganize supply chains for many industries to de-risk their businesses. India can build on its reputation in services exports as cost rationalization and diversification to de-risk business decisions among multinationals may lead to greater Global In-house Center (GIC) opportunities. In certain sectors and industries, such as pharma and auto, there are possibilities of GICs moving up the maturity curve through higher research and innovations, and by exploring opportunities for growth in line with policymakers’ self-reliance vision for the country.

With uncertainties around COVID-19 still looming large, the road to economic recovery will remain dotted with challenges. That said, the country has handled trying situations prudently in the past and the government has the necessary mandate to usher in challenging and difficult reforms that can put the economy back on track. Thriving in postpandemic times will require policymakers, businesses, and investors to demonstrate resilience and the ability to convert challenges into opportunities, now.

Deloitte Global Economist Network

The Deloitte Global Economist Network is a diverse group of economists that produce relevant, interesting and thought-provoking content for external and internal audiences. The Network’s industry and economics expertise allows us to bring sophisticated analysis to complex industry-based questions. Publications range from in-depth reports and thought leadership examining critical issues to executive briefs aimed at keeping Deloitte’s top management and partners abreast of topical issues.

Learn more

Get in touch

- Dr. Rumki Majumdar

- Associate director and economist

- Deloitte India

- rumajumdar@deloitte.com

- +91 80 6188 5684

More from the economics collection

-

Economic impact of epidemics and pandemics in Asia since 2000 Article4 years ago

Economic impact of epidemics and pandemics in Asia since 2000 Article4 years ago -

Unlocking the lockdown: Asia Pacific’s road to recovery Article4 years ago

Unlocking the lockdown: Asia Pacific’s road to recovery Article4 years ago -

Japan economic outlook, April 2024 Article2 months ago

Japan economic outlook, April 2024 Article2 months ago -

United States Economic Forecast Q2 2024 Article4 weeks ago

United States Economic Forecast Q2 2024 Article4 weeks ago -

-

The long and short of short-time work amid COVID-19 Article4 years ago

The long and short of short-time work amid COVID-19 Article4 years ago