South Africa has been saved

Cover image by: Tushar Barman

South Africa’s economic climate has presented a number of challenges in the run-up to the 2021 budget. Like many countries, the South African government tabled an emergency budget in mid-2020 in the middle of the COVID-19 pandemic, when it faced an expected budget revenue shortfall of R312 billion since the 2020 budget. The subsequent Medium-Term Budget Policy Statement (MTBPS) had to allocate additional resources towards an economic recovery plan, along with an economic stimulus to ensure that the economy is able to build a sustainable recovery after the estimated 7.2% decline in economic output in 2020.1

As a result, and in line with global trends, South Africa’s debt rose sharply in 2020. So too did debt projections over the next five years to meet the spending needs that arose from the pandemic, including the funding of continuity support measures to households and businesses along with other economic recovery plans.

Since the global financial crisis of 2008–09, South Africa’s debt trajectory has climbed rapidly and is converging with the world average (figure 1). The country’s debt-to-GDP ratio first exceeded the average of emerging and developing economies in 2011, at 38.2% compared with 36.6%. In the past five years, the build-up of debt as a share of GDP has grown substantially, while GDP has not kept pace: Real spending growth has averaged 4.1% per annum, while real GDP growth has lagged at 1.5% per annum. Debt-service costs have outpaced expenditure in health and basic education programmes for 2021–22,2 thereby remaining the fastest-growing line item in the budget.

If this course were to continue, debt-service costs would crowd out more and more spending priorities, which will inevitably adversely affect growth. Furthermore, from 2011 to 2019, emerging and developing economies have averaged 4.8% real GDP growth, compared with South Africa’s stagnant 1.5%.3

The COVID-19 pandemic has brought into sharp focus the limited space South Africa has to stimulate the economy in the event of a global economic shock, and it has been forced to turn to fiscal consolidation to reel in debt. The massive stimulus has also highlighted the country’s desperate need to achieve policy certainty, implement changes at state-owned enterprises and adopt fiscal prudence.

Maintaining fiscal conservatism along the path highlighted in the MTBPS and confirming this in the current and subsequent budgets will be key to ensuring that debt levels remain under control while stimulating growth by addressing South Africa’s short-term structural issues.

The budget has taken strong steps towards addressing rising debt levels. Following the 2020 MTBPS, debt was expected to stabilise at 95.3% of GDP in 2025–26.4 With the pandemic still raging and economic lockdown measures continuing globally, there was speculation that debt may climb even higher to fund the COVID-19 vaccine or additional liabilities, before stabilising later. However, consumption strongly bouncing back at the end of 2020 and an improvement in revenues collected during the latter half of the year have led to a lower-than-expected debt-to-GDP ratio. This ratio is expected to stabilise at 5.4 percentage points below the MTBPS trajectory at 88.9% in 2025–26 before beginning a downward trajectory, with a primary surplus expected in 2024–25.5

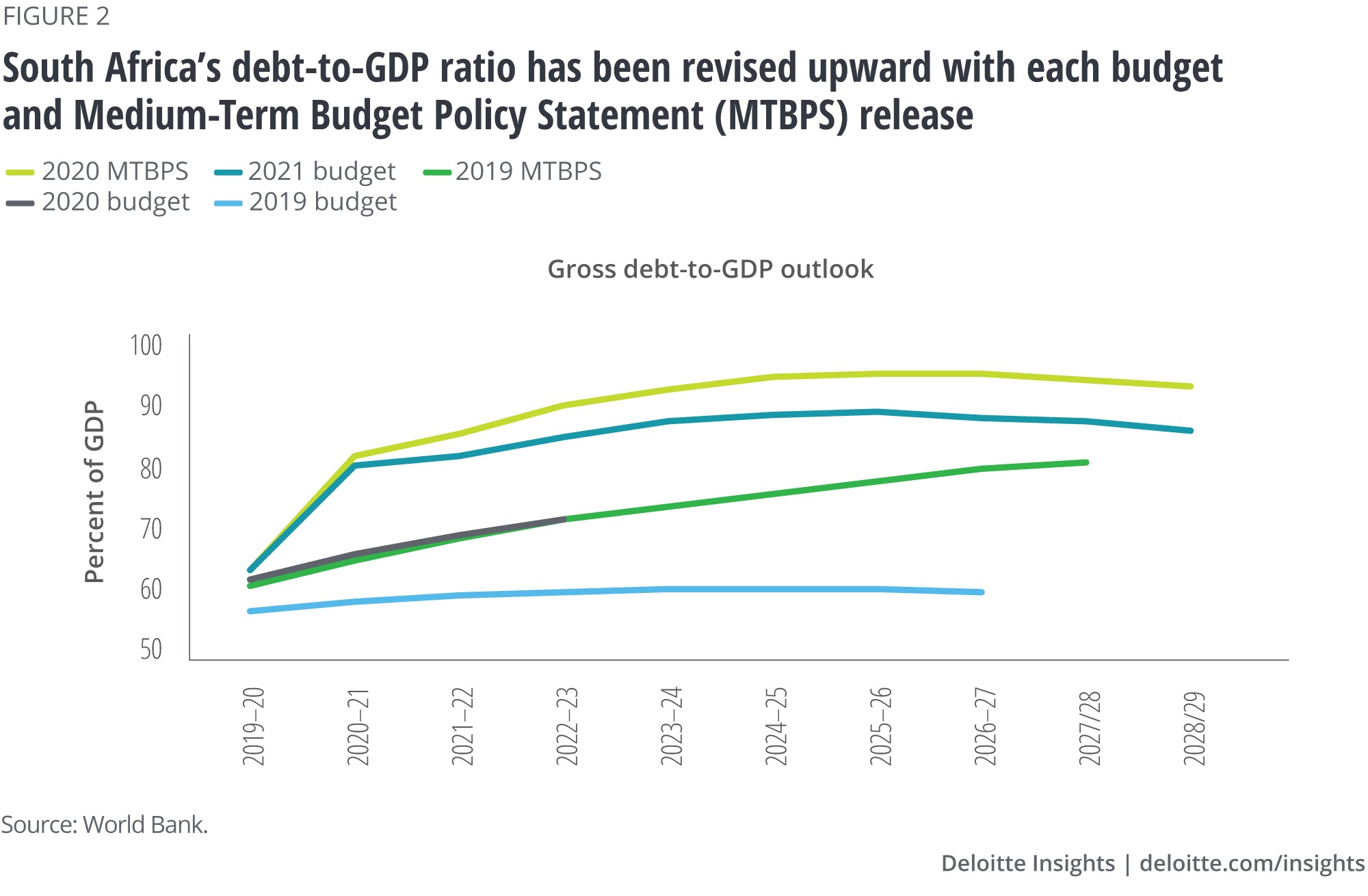

This adjustment in planning marks a distinct pivot from previous budgets, where the focus was on reprioritisation of capital spending to curtail debt levels, which was largely unsuccessful as debt continued to climb through successive budget cycles (figure 2). The debt-to-GDP ratio has been revised upward with each budget and MTBPS release since fiscal consolidation came into focus around 2017, following a countercyclical response to the downturn as described in the 2014 budget.6 This marks the first budget in a number of years where the debt trajectory is lower than seen in the preceding MTBPS.

Although the large jump outlined in the 2020 MTBPS arguably allowed room for a downward revision, this measure should still be commended. Adhering to these projections will go a long way to showing a commitment to fiscal discipline to capital markets. This show of commitment will, in turn, have a positive knock-on effect on borrowing costs, given that South Africa should be able to borrow at lower rates. This will allow government to manage borrowing requirements in coming years without interest costs escalating, as rapidly as seen over the last few years.

Data released in the 2021 budget also showed that tax revenue estimates beat 2020 MTBPS expectations by R99.6 billion, but still fell short of the estimated R213.2 billion that was projected in the 2020 budget, which highlights the precarious position the country’s finances are in.7 However, the surprise upside has allowed the government to limit tax increase measures; it has actually withdrawn previously announced increases of R40 billion.8

Where tax increases have been implemented, they have been focused on tax bracket adjustment and above-inflation increases on alcohol and tobacco excise duties. The government has indicated that a shift away from income taxes and towards value-added tax (VAT) may be the intended direction for future funding requirements, given already-comparatively high rates of taxation on individuals and companies. A much-speculated-over ‘wealth’ or ‘solidarity’ tax was not announced.

South Africa’s economy is expected to rebound in 2021 and 2022 after the dire impact of COVID-19. The sharp contraction in 2020, due to enforced shutdowns and the resulting lack of economic activity, resulted in a high expected growth rate of 3.3% in 2021 due, in part, to base effects.9

World output is expected to grow 5.5% and 4.2% in 2021 and 2022, respectively.10 In comparison, South Africa’s output is expected to grow 3.3% in 2021 and 2.2% in 2022.11 While seemingly impressive compared with the paltry growth rates seen over the last few years, this is still far below the emerging and developing market average of 6.3% in 2021 and 5% in 2022.12

As most of the world picks up pace, South Africa’s growth is expected to moderate to 1.6% in 2023

The public sector wage bill remains one of the highest downside risks to keeping the fiscus in check. The latest budget has taken a hard line on cuts to compensation growth, proposing an effective cut of R300 billion to the wage bill, achieved through a combination of R160 billion worth of cuts from the 2020 budget and R143 billion over the medium term.

Growth in public sector compensation has seen a significant reduction in estimated expenditure. The wage bill has seen revisions to the medium-term estimate fall from 6.8% in the 2019 budget to 3.5% in the 2020 budget; the latest budget estimates annual average growth of 1.2% over the medium term, falling far short of expected inflation over this period. Wage negotiations are set to begin later this year, and the outcome of these will determine whether the debt trajectory will remain on the forecast path. Prebudget tensions between the government and trade unions have been rising, with the latter strongly opposing the proposed wage cuts. The success of keeping spending in check will depend on the ability of the negotiating parties to reach a settlement. However, given the tough economic climate, public sector labour unrest may be on the cards in 2021.

The cuts to the social grant system are likely to cause significant hardship and unrest over the next three years. This is especially relevant given recent employment trends. In the latest Quarterly Labour Force Survey (in Q4 2020), the unemployment rate rose to 32.5%, the highest since 2008. While employment recovered by nearly 900,000 workers in the last two quarters of 2020, this pales in comparison with the 2.2 million jobs that were lost in Q2 2020.13 While the expected economic bounce back in 2021 and 2022 will likely add more jobs, many of the jobs lost in 2020 are unlikely to return.

The budget announced a 2.2% contraction in social grants over the medium term. While the special COVID-19 social relief of distress grant is extended to April 2021, overall grant spending is expected to increase by less than the inflation rate in 2021–22. This is likely to cause hardship, especially in rural areas that often rely on grants and provincial remittances to survive. Over the medium term, as the grant-dependent population finds itself poorer in real terms (with inflation expected to breach 4.5% at the end of 202114), this may lead to civil unrest and increased political pressure to raise spending on social assistance in the 2022 budget.

The 2020 budget has pinned the hopes of a path to recovery on a complex set of reforms. This is driven by a combination of raising public infrastructure spending; committing to exceptional spending cuts, with the aim of bringing about a significant recovery to raise growth; raising tax revenue; and rebuilding a sustainable economic trajectory that allows for job creation and inclusive economic growth.

This is critical to reversing the decline in GDP per capita. Between 2015 and 2019, GDP per capita fell by an annual average of 1% (figure 3). Without a growing economy, the country faces a cycle of constant low growth, fast-growing unemployment and greater reliance on social security, thereby further burdening the fiscus.

To achieve the planned recovery, South Africa will need to enact a complex set of reforms in the short term that will set up the economy for sustainable growth and allow the country to achieve the socioeconomic and development goals detailed in its National Development Plan. These are based on the following goals:

• Increasing investment in infrastructure

• Encouraging private sector investment and private-public partnerships through efficiency reforms.15

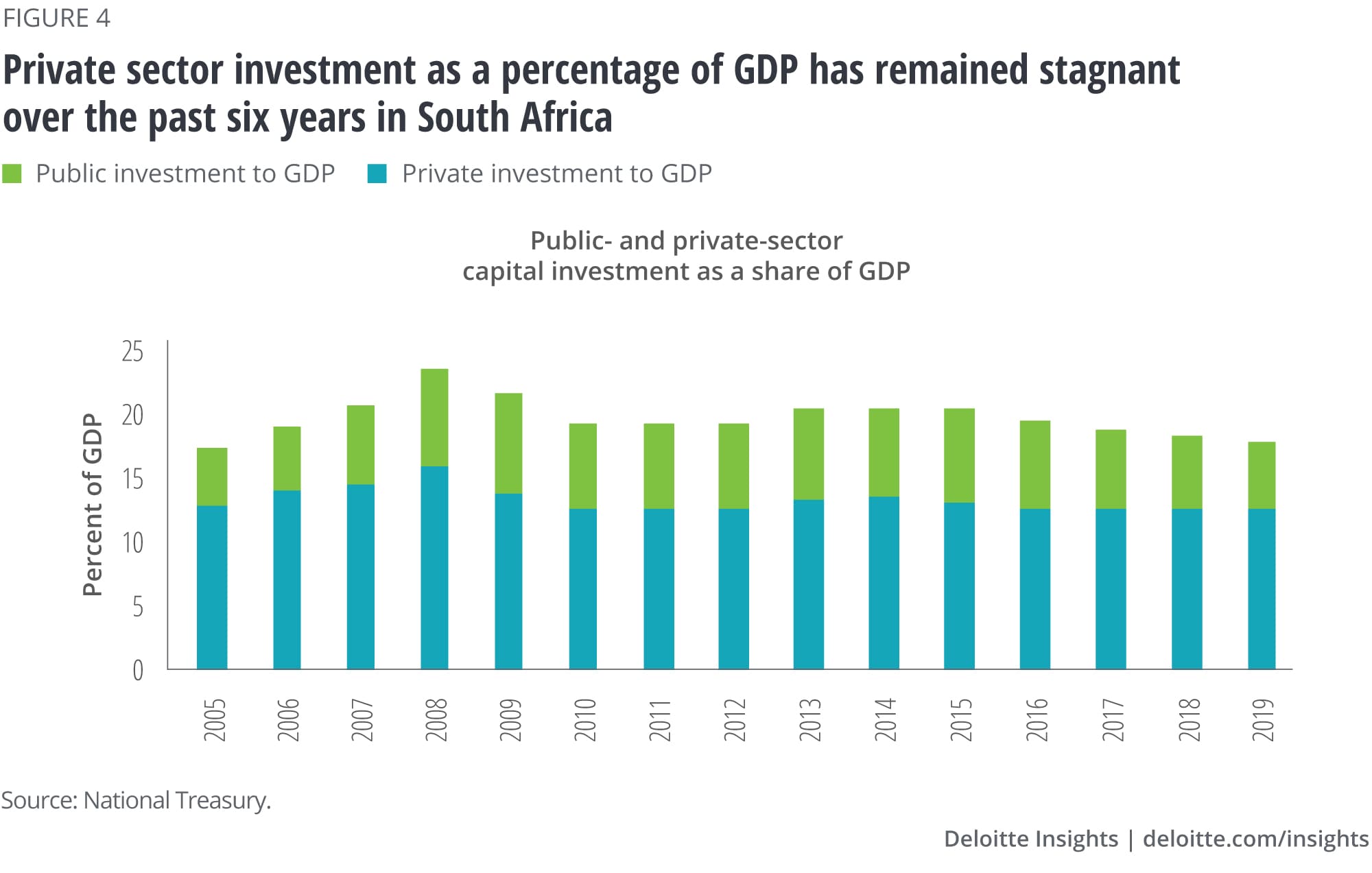

The budget has allocated R791 billion over the medium term to public sector infrastructure spending, the bulk of which is slated to go to transport and logistics (R287 billion) and energy (R149 billion).16 The budget has also noted that government cannot continue to drive investment, given the poor value for money from public spending. Reining in spending while increasing investment forms a major focus of this latest budget, and the fiscal pressures the government is under means that the private sector will have to play a significant role.

As seen in figure 4, private sector investment as a percentage of GDP has remained stagnant over the past six years as a result of low business confidence, lack of policy certainty and infrastructure limitations such as electricity supply. The government aims to solve this by unlocking private-public partnerships in energy, which will raise investment, create jobs, lessen the crippling energy supply constraint and build confidence in the ability to expand operations in the country.

This investment-driven economic recovery does, however, entail further risks. If the desired level of investment to reach the economic growth estimates for 2022 and 2023 is not achieved, the cuts in spending on the public sector wage bill and social security will have a pronounced negative effect on the economy and set back the recovery to 2019 levels far beyond 2023.

The second and even more critical factor to an economic recovery is the rollout and successful vaccination of the population. As seen at the beginning of 2020, the national lockdown saw economic activity plunge, with a resulting fall in growth of 51.7% in Q2 2020 (quarter on quarter in seasonally adjusted and annualised terms).17 The economic recovery is contingent on the economy remaining open, with South Africa ill-equipped to afford another lockdown.

With that in mind, the budget made provision for around R17.3 billion in vaccine-related spending, of which R10.3 billion is to fund a vaccine rollout programme in allocated expenditure, with an increase in the contingency reserve from R5 billion to R12 billion for further vaccine purchases.18

The budget represents a positive shift in thinking to addressing the structural constraints that have kept South Africa in a low growth trap for the past decade. The commitment to the five-year fiscal consolidation pathway outlined in the 2020 MTBPS has been buoyed by a lower debt trajectory, which will certainly be well received in capital markets.

However, the budget does rely on strict fiscal consolidation and discipline in adhering to spending constraints, optimistic expectations of an economic recovery and a bit of luck to ensure the economy remains open through the successful rollout of the vaccination programme. Risks remain high, and should the government fail to hold the line on public sector compensation increases and social spending, this has the potential to severely constrain the budget commitments and economic outlook.

{kind=link}

{kind=link}

{kind=link}

{kind=link}