Eurozone economic outlook has been saved

Cover image by: Tushar Barman

The beginning of the new year was far from perfect for the Eurozone economy. Rising COVID-19 infection rates resulted in continued, new, or tightened lockdowns since autumn, sending the economy into recession in the last quarter of 2020. The new lockdowns are likely to last—in varying degrees—for most of the first quarter of this year. Thus, healing of the Eurozone economy will take more time than most analysts expected after the economy’s rapid rebound in the third quarter. Recovery will be delayed until the virus is brought under control or until vaccinations allow a reopening of the economy.

Nonetheless, the outlook beyond the first quarter seems brighter. If Eurozone countries are able to ensure a quick rollout of vaccinations, a better control of the pandemic and an easing of lockdown measures, the Eurozone economy is likely to rebound from the second quarter, driven by pent-up consumers demand. There are downside risks along the way, however, such as delays in the vaccination campaign or scarring in the economy and labor markets. But there are also upside risks, especially the possibility of a consumer boom in the postpandemic economy, driven by stronger than anticipated pent-up demand due to accumulated savings.

The Eurozone economy experienced a rough ride in 2020. After contracting in the first quarter, it declined by almost 12% when the pandemic fully hit Europe in the second quarter. This was followed by a sharp rebound (up 12.4%) in the third quarter, before a contraction in the fourth quarter (down 0.7%) as new restrictions were put in place. In total, according to provisional estimates, the Eurozone economy shrank by 6.8% in 2020.1 The blow to the Eurozone economy was much harder than to the US economy—the US GDP contracted 3.7%, almost half that of the Eurozone GDP.

Eurozone economies performed substantially differently from each other. According to the OECD, the Spanish economy was the worst hit in 2020, shrinking by almost 12%. In both France and Italy, GDP fell by 9.1%, while Germany saw a contraction of 5.5%. Nonetheless, some European Union (EU) member states weathered the crisis relatively better—Denmark, Finland, Sweden, Poland, and Ireland contracted between 3% and 4%.2

The wide range of economic performance was due to several factors. Some countries, such as Spain and Italy, were hit harder by the pandemic than other countries and, as a result, introduced longer and stricter lockdowns in the first wave. Sectoral factors played an important role too. Countries with a dominant tourism sector suffered more than others, while countries more reliant on manufacturing benefitted from the surprising comeback of world trade.

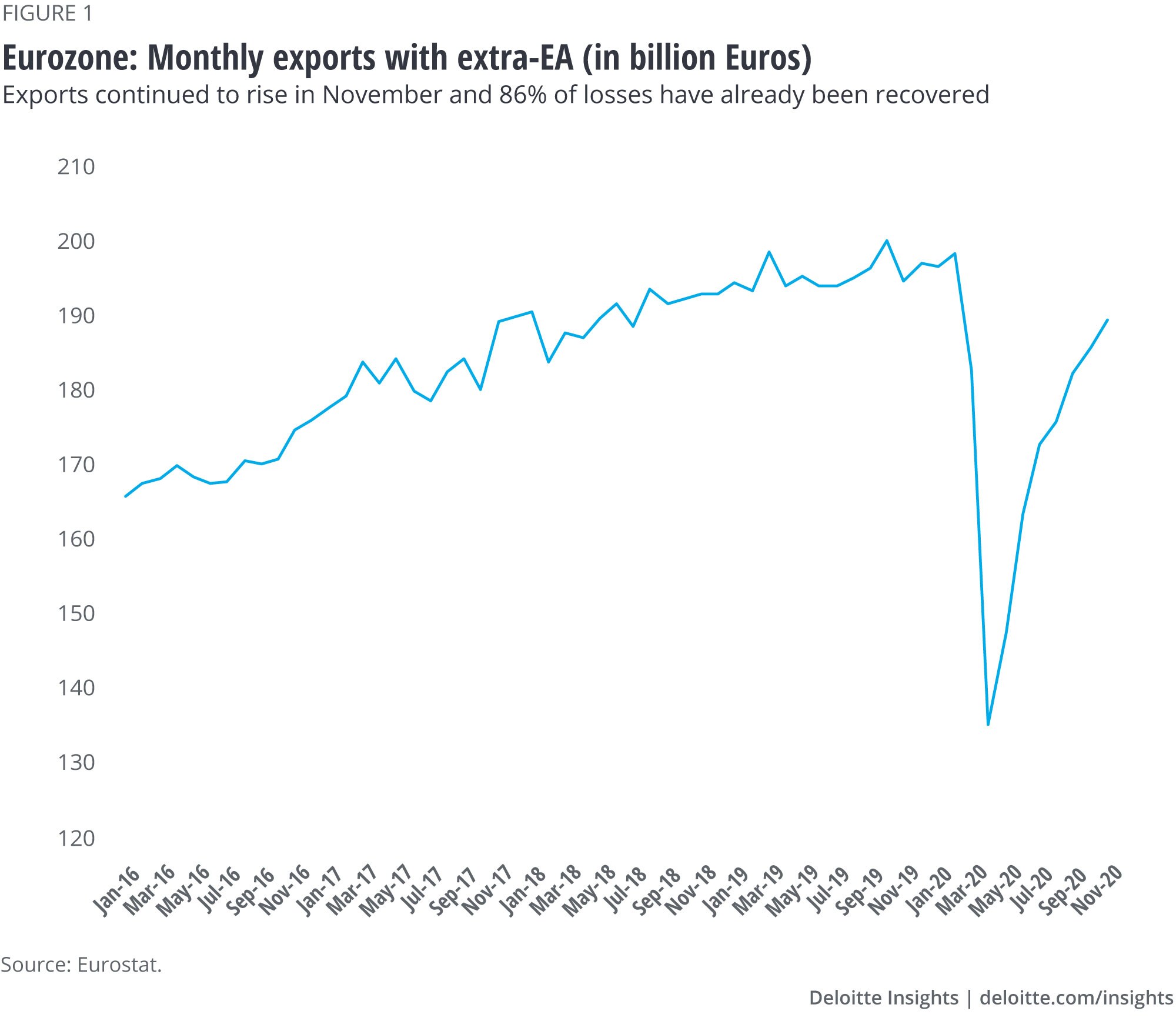

Contrary to gloomy expectations, world trade rebounded very quickly and global supply chains were restored after they were interrupted in the first wave of infections. The rapid comeback of world trade supported the export-oriented Eurozone economy and prevented a worse collapse. In fact, compared to the financial crisis of 2007-08, world trade rebounded far quicker and stronger. According to data from the CPB World trade monitor, after the 2007-08 financial crisis, world trade took almost two years to come close to the precrisis level. In the current crisis, however, world trade took only nine months to recover following an unprecedented fall in spring. China’s rapid economic recovery accounts for a good part of the rebound.3 Eurozone exports, therefore, show a V-shaped recovery and were able to recoup a large part of the earlier contraction (figure 1).

While a revival in global trade provided a welcome boost for the manufacturing sector, the services sector—especially consumer services—did not benefit from the global uplift in trade. This is why we see a bifurcation in the European economy, The Purchasing Managers’ Index (PMI)—an early indicator—for manufacturing remained at high levels in January after having reached an 18-month high in December, while the PMI for the services sector is still in contraction.4 Business confidence in the automotive, electronics, and chemicals sectors has already breached precrisis levels (figure 2).

The effects of the historic drop in GDP on the Eurozone’s labor market have been surprisingly limited. Official unemployment rose only 1 percentage point, from 7.4% in 2019 to 8.4% in 2020.5 This was mainly due to the swift introduction of furlough schemes in many Eurozone countries as well as economic policy measures to help secure corporate liquidity. Taken together, these measures kept employees in employment, companies afloat, and disposable incomes, from a macroeconomic perspective, largely stable.

As for consumer expenditure, consumers generally react to recessions by holding more cash to protect themselves against an uncertain economic future. It was no different in the COVID-19 crisis. Additionally, the lockdowns resulted in a substantial amount of involuntary savings that likely exceed the precautionary savings. With most leisure activities and travel banned, consumers could not spend their money the way they would have otherwise. In fact, a survey conducted by the German central bank in August, after the first lockdown, suggests that the two most important reasons for reduced consumer expenditure were that many goods and services were not available and that some expenses were not necessary any longer. Reduced income or the fear of reduced income in the future was rated much less important.6

As a consequence, consumer savings in the Eurozone are high. According to estimates by Oxford Economics, the savings rate increased to 19% in 2020, up from 13% in 2019. When converted to absolute numbers, this means that Eurozone households saved around €450 billion more than in 2019. Unloading these savings could bring a substantial boost to consumer spending and, therefore, GDP growth in 2021.

The new wave of infections and the new lockdowns in the Eurozone interrupted the recovery that had started in the third quarter. Currently, the recovery in some Eurozone countries is W-shaped and in some others it resembles the shape of the mathematical square root symbol. However, it seems that the recovery is interrupted, but not cancelled. The economic fundamentals suggest that a strong rebound is a likely scenario once the pandemic is under control.

This is due to three reasons. First, the accumulated excess savings could provide strong tailwinds for the recovery once consumers are able to spend their money again. Second, the outlook for corporate investments is cautiously optimistic. A survey by the European Commission suggests that investments in the manufacturing industry will rise by 3% in 2021, after a contraction of 12% in 2020.7 Third, there is reason to assume that world trade will continue to rise. Indices measuring container throughput as a proxy for the development of world trade are at high levels and only slightly below their peaks reached in October 2020.8 Given successful global vaccination rollouts, more countries will recover from the second quarter onwards, which will support the export-oriented economies of the Eurozone. In the baseline scenario, Deloitte expects a growth rate of 4.5% in 2021 for the Eurozone.

There are, of course, risks. The vaccination rate of the continental European countries substantially lags that of the United States, the United Kingdom, and Israel. Further delays in vaccination campaigns would be a serious drag for the recovery. Even worse would be the emergence of vaccine-resistant strains. On the positive side, however, assuming a smooth progression of vaccinations, an accelerating consumption boom is a plausible scenario.9 To prepare for the possible scenarios, developments in the labor markets, consumer confidence, and vaccination rates are the most important indicators to watch out for in the coming quarters.

{kind=link}

{kind=link}