Eurozone economic outlook, June 2023 has been saved

Cover image by: Jaime Austin

The Eurozone’s current economic situation and its outlook are being shaped by economic factors moving in opposite directions. On the positive side, the Eurozone managed to get through the winter without energy shortages and severe recession feared by many analysts. Labor markets have continued to thrive, stabilizing consumer expenditure, and economic sentiment has recovered. On the negative side, inflation remains stubbornly high, the interest-rate hike cycle is still ongoing, and geopolitical uncertainty remains high. As a result of these countervailing forces, very moderate growth in 2023 seems to be the most likely scenario.

According to Organization for Economic Cooperation and Development data, the Eurozone’s GDP grew by 0.1% quarter on quarter in the first quarter of 2023. Among the major Eurozone economies, Spain (preliminary) and Italy both expanded by 0.5%, France by 0.2%, while Germany stagnated.1 All in all, it would be safe to say that the Eurozone economy stagnated.

However, against the background of the gloomy expectations of a severe winter recession, widespread only a short time ago, the Eurozone’s economic performance may be considered good news. Current consumer and business sentiment indicators suggest that a recovery is underway. Both rebounded considerably from the very deep autumn lows and are now close to their long-term average, as the European Commission’s economic and consumer sentiment index shows.2 However, it should be noted that behind the improved corporate sentiment are wide sectoral differences: Consistent with the global picture, the services sector seems to be doing better than the industrial sector.

The industrial sector suffers from weak orders and abating international demand. For example, new orders from the German manufacturing sector collapsed by more than 10% in March,3 the highest drop since the first months of the COVID-19 pandemic. This is especially worrying as the high backlog witnessed during the peak of COVID-19 has largely disappeared. As a consequence, the purchasing manager index (PMI) for the industrial sector in the Eurozone contracted. The PMI for the services sector, on the other hand, is in solidly expansionary territory, indicating an acceleration of the sector at a strong pace.4

Sentiment in the consumer sector is also on the way up. This is likely to be due to the fading energy crisis, even if inflation continues to depress real incomes. In general, consumer expenditure is supported by a robust labor market, which has worked as a stabilizing factor for the overall economic outlook. In fact, at 6%, the Eurozone has reached a record-low unemployment rate.5

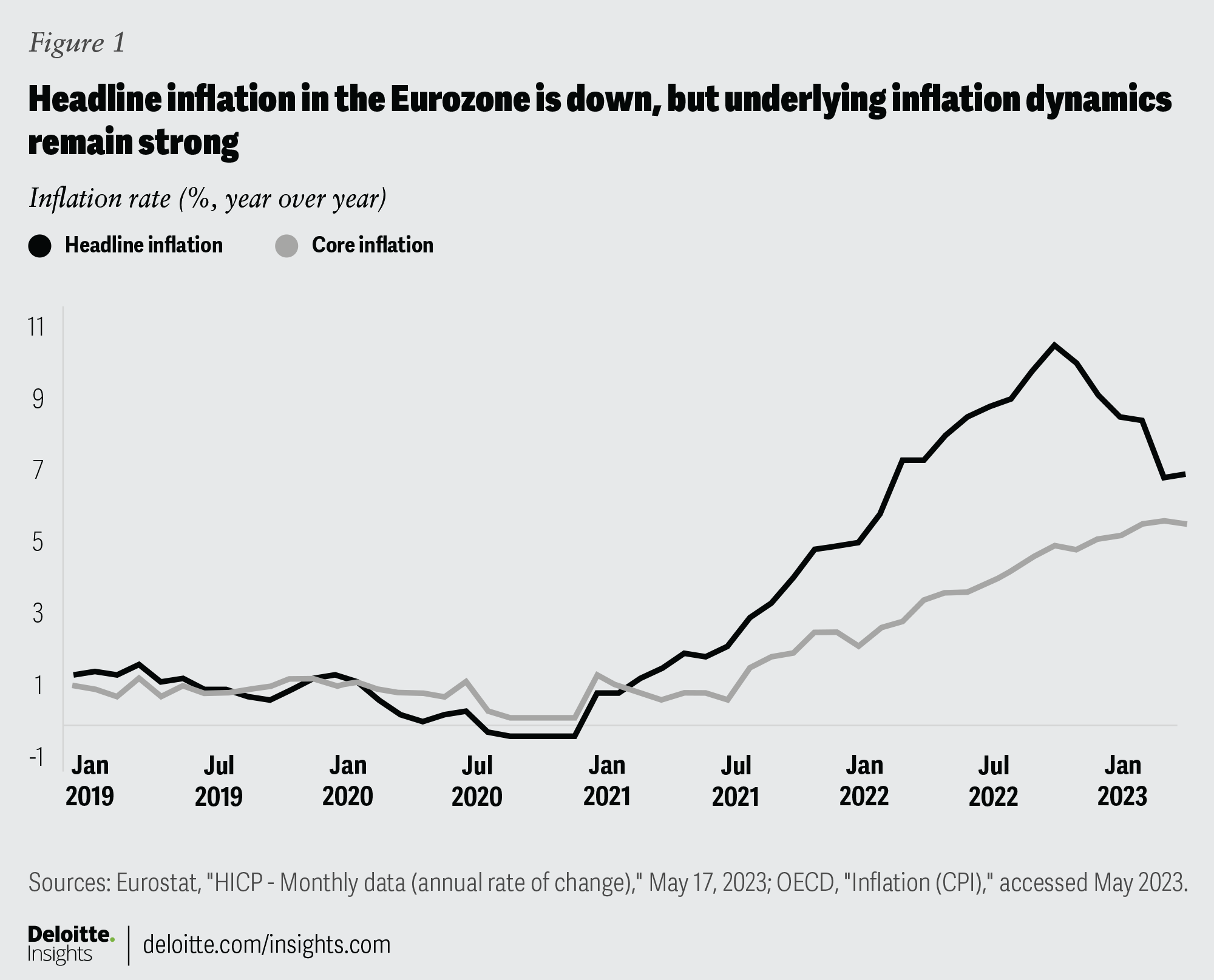

The rate-hike cycle in the Eurozone started last July, and since then, the European Central Bank (ECB) has raised interest rates seven times—the last time in May to 3.75% for its main refinancing operations. Headline inflation has been receding from its peak of 10.6% in October and stood at 7% in April.6 The highest inflation, even if it is receding, is still to be found in the Baltic states (rates of 15% and higher), with wage costs being one key driver. Countries such as Belgium and Spain have inflation rates between 3% and 4%. Inflation in other big Eurozone economies is hovering in between these two extremes—6.9% for France, 7.6% for Germany, and 8.8% for Italy.

The rate-hike cycle is unlikely to be over, as underlying inflation dynamics are still strong. Core inflation (that is, headline inflation without food and energy), which is the key indicator of the spread of inflation across the economy, hardly shows signs of ebbing. In fact, it has been rising constantly. At 5.6% in April, it is only marginally lower than its peak the month before. As long as core inflation is not under control, the ECB’s fight against inflation is not over.

Inflation in the Eurozone has gone through different phases.7 In the first phase, inflation was fueled by price increases resulting from interrupted supply chains during the COVID-19 pandemic. In the second phase, the start of the Ukraine war accelerated inflationary tendencies, especially by surging energy and commodity prices. The question going forward is whether inflation in Eurozone will now enter its third phase, in which wage increases, as a response to the strong price increases, will drive inflation. In this sense, the risk of a wage-price spiral and hardening inflation is real.

With inflationary pressures not showing signs of abating, European companies expect inflation to remain at a high level for the near future. According to the recent Deloitte European CFO Survey, chief financial officers (CFOs) predict an inflation rate of 6.3% for the euro area over the next 12 months. Inflation is also driving up the financing costs of companies: Seventy percent of CFOs rate the present cost of credit as either fairly costly (55%) or very costly (15%).8

The latest, and relatively optimistic, forecasts from the European Commission for the Eurozone assume a growth rate of 1% for 2023 and an inflation rate of almost 6%, with wide differences between countries.9 This meagre growth prospects confirm that the postpandemic recovery was derailed by a series of new crises in 2022 and 2023. Whether or not the recovery continues hinges crucially on three factors: The first is foreign demand, which will depend particularly on the economic growth in the United States and China. The second factor is the trajectory of inflation from this point onward and its effects on real income. The third factor is how rising interest rates impact corporates.

If the fight against inflation, and especially core inflation, were to bear fruit in the near term, we could see rising real incomes and an expansion of private consumption and the economy. It would also make lower interest rates and, therefore, lower credit costs in the medium term much more likely, which will have positive effects on corporate investments. However, if the fight against inflation continues, the predicted current growth forecasts seem to represent the highest level of economic growth achievable in 2023.

{kind=link}