United Kingdom has been saved

Cover image by: Tushar Barman

The United Kingdom weathered two successive waves of the COVID-19 pandemic in the winter months. A new, more contagious variant of the virus has brought about rapid rises in new cases (figure 1) and hospitalizations, forcing authorities to respond with nationwide lockdowns—in November and again in January.

While the January lockdown is slowing new infections, we expect restrictions in movement to remain elevated until early spring, by when the government aims to have vaccinated the most vulnerable and eased pressure on the National Health Service.

Under the current restrictions, consumer-facing services such as retail trade, food- and beverage-serving activities, and travel and recreation are the hardest hit. Latest official data, from November, suggest sharp declines in output in these sectors although not the dramatic collapse they saw during the first wave in April.

Manufacturing activity has held up, supported by Brexit-related stockpiling in the fourth quarter as companies built up inventories to mitigate the risk of a disruptive, no-deal departure from the European Union. But now that a trade deal has been struck, businesses are likely to run down their stockpiles, dampening first-quarter activity.

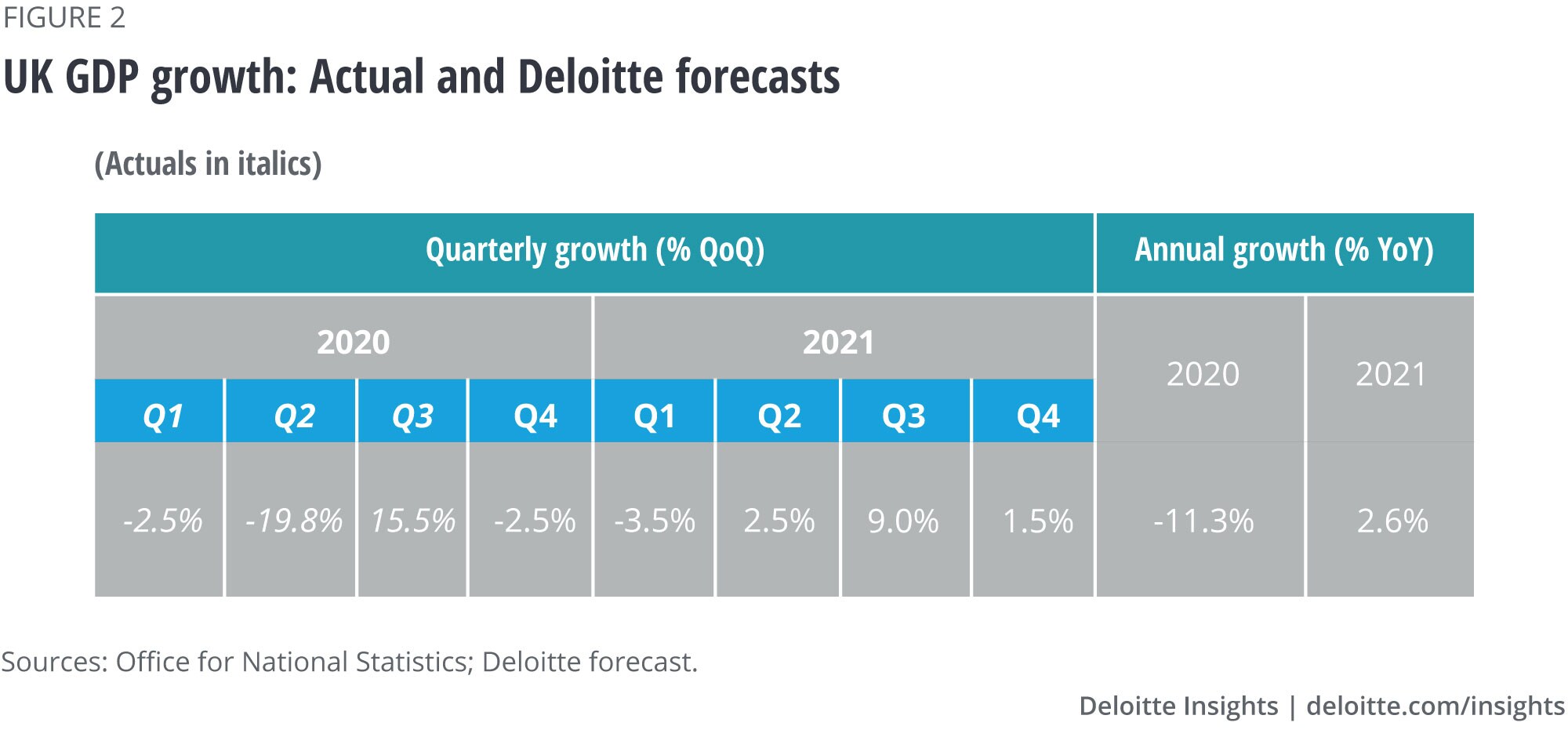

Overall, we expect the economy to have contracted in the fourth quarter (table 1) and to do so again in the first, leading to a double-dip recession. However, with the corporate sector better prepared to respond to tighter restrictions this time, and government support schemes already in place, these contractions are forecast to be much smaller in scale than the one seen in the second quarter of last year.

Growth should bounce back in the summer months as vaccines and better weather provide a route out of the crisis. The government has already made rapid progress in its mass vaccination programme, with 6% of the population having received their first jabs by mid-January—a faster rollout than in the United States or any other European country. With the United Kingdom seemingly on track to meet its target of providing first jabs to 80% of all the over-50s and the most vulnerable by early May, we expect a material easing of restrictions in the summer. This should drive a modest pickup in activity in the second quarter and a strong recovery in the third (figure 3).

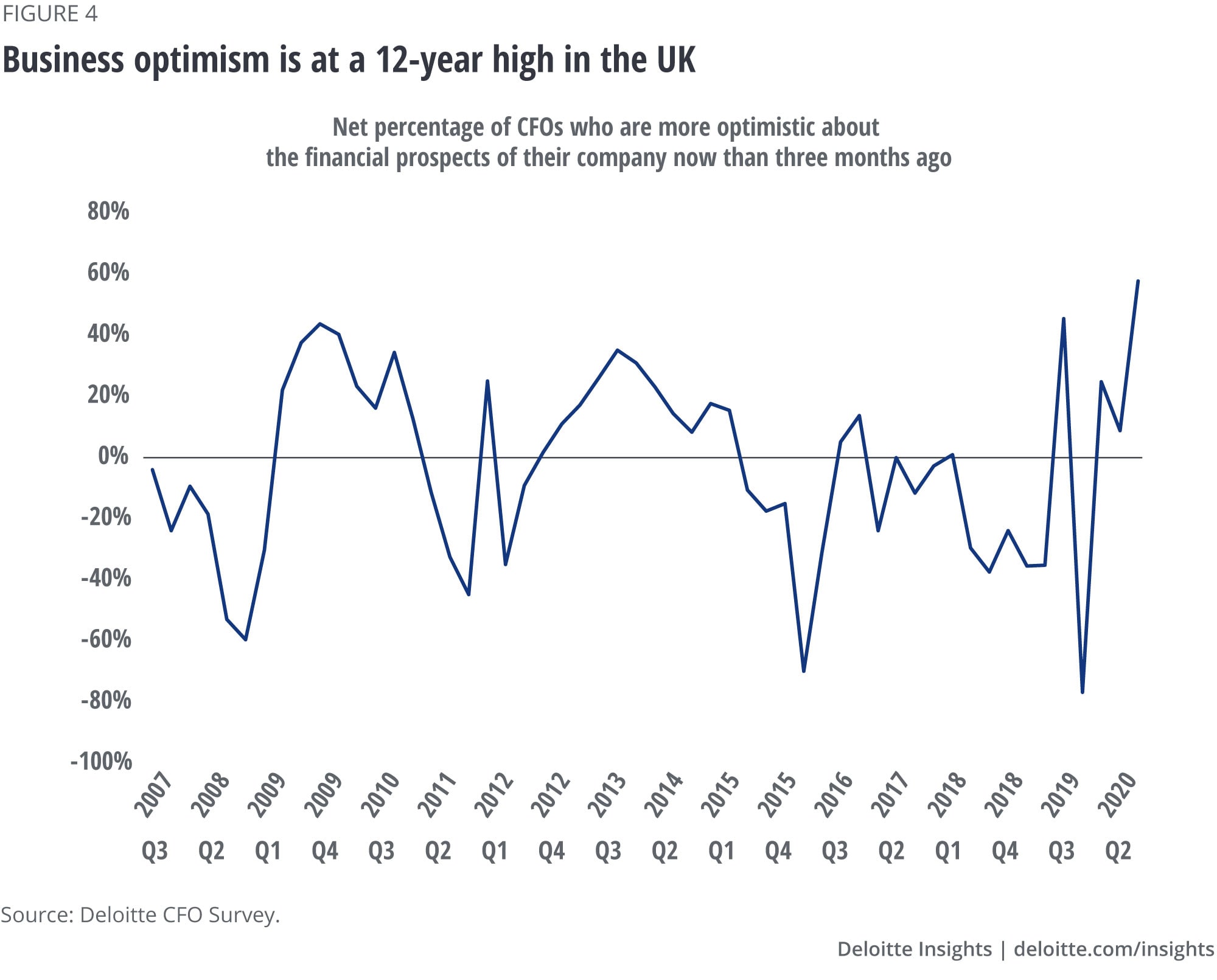

Businesses also seem optimistic about the prospect of mass vaccinations delivering a sustained pickup in activity this year. This is reflected in the findings of our latest CFO Survey, which shows business optimism at a 12-year high despite the surge in cases and new restrictions. Corporates are also relieved at the elimination of the risk of a no-deal Brexit, which had been a major and longstanding source of uncertainty.

Yet, risks remain. Vaccine-resistant mutations of the virus, bottlenecks in the production and supply of vaccines, and challenges in their take-up could significantly slow down any recovery. In addition, a spike in unemployment or corporate insolvencies—in the event of further waves of infections—could put paid to plans for a rapid normalization of activity. In the United Kingdom, the end of the Brexit transition period has brought limited disruption so far, but any extension of friction could act as an additional drag on growth.

2020 was a topsy-turvy year for the UK economy. After the deepest economic downturn on record, a strong rebound was cut short by a surge in COVID-19 infections. This year, we expect vaccines and continued policy support to deliver a more sustainable recovery.

{kind=link}

{kind=link}

{kind=link}

{kind=link}