{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

After the crisis: rapid evolution, not revolution has been saved

The authors would like to thank Ram Sahu for his research support in various stages of the project.

Cover image by: Mark Milward

Germany

Spain

United Kingdom

Germany

“Unprecedented times” – this term, used in the English language since at least 1795,1 has become a cliché since 2020. The COVID-19 pandemic and the measures put in place to address it have required people around the world to rapidly adopt different ways of interacting, working and conducting business.

The pandemic, now in its second year, continues to dominate the global picture. But, with multiple successful vaccines being rolled out, many countries are gradually lifting COVID-19 restrictions and beginning to emerge from the crisis. As the dust settles and life returns to some sort of normality, it is time to take stock and identify the probable long-lasting changes to the business environment. To this end the Spring 2021 edition of the European CFO survey asked almost 1,300 CFOs across 19 European countries to assess which phase of the COVID crisis their company is in, which aspects of their operations are going to change and which key areas they are prioritising as they seek to build resilient organisations.

Since 2015 Deloitte has conducted the European CFO Survey, giving voice twice a year to Chief Financial Officers (CFOs) from across Europe. Besides providing an overview of business sentiment in Europe, each edition focuses on a topical issue. The Spring 2021 edition focused on the long-term consequences of COVID-19. The data was collected in March 2021. The results in this article are based on the answers of 1,296 CFOs. For further details, please visit Deloitte.com.

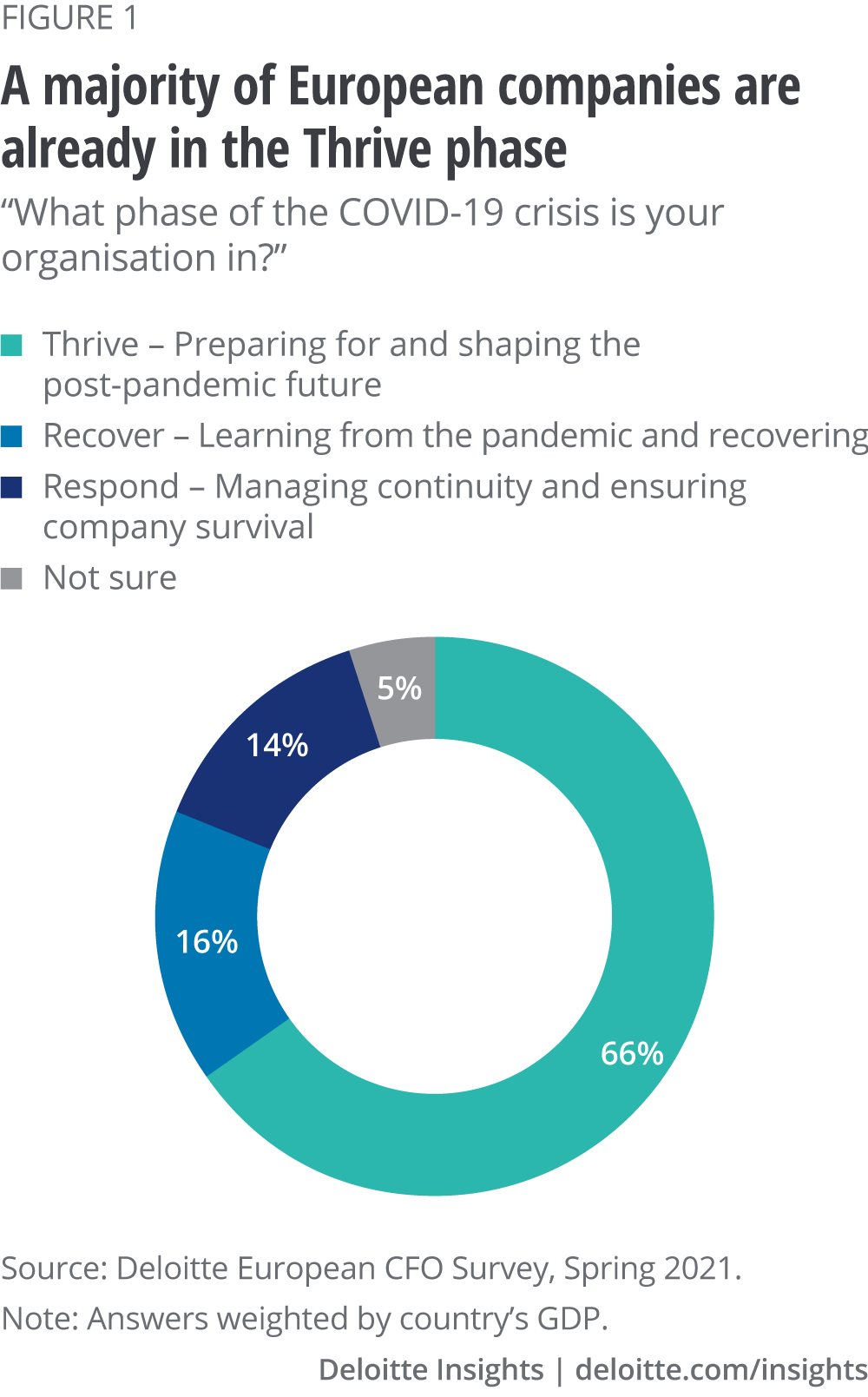

In March 2020, when it became clear that COVID-19 was becoming a global threat, Deloitte laid out a framework defining three critical phases companies must navigate as a crisis unfolds. In the Respond phase, a company deals with the new situation and focuses on managing continuity. In the Recover phase, a company learns from the crisis and begins to emerge stronger. In the Thrive phase, the company prepares for and helps to shape the “next normal”.2

Asked to assess which phase of the COVID crisis their organisation is in, two in three CFOs (66 per cent) report that they are already in the Thrive phase. Only 14 per cent feel they are still in the Respond survival mode.

A typical crisis plays out over three time frames:

Respond, in which a company deals with the present situation and manages continuity

Recover, during which a company learns and emerges stronger

Thrive, where the company prepares for and shapes the “next normal”.

Resilient organisations rapidly and successfully cycle through these phases – not just for COVID-19, but for every crisis.

In general, smaller companies (defined as those with annual revenues of up to €100 million) appear to be at an earlier stage of recovery, with 22 per cent still in the Respond phase. By contrast, only 6 per cent of CFOs in large companies (defined as those with annual revenues of €1 billion or more) are in the same position. Unsurprisingly, the share of executives who say they are in the Respond phase is significantly higher in sectors that have been hit harder by the pandemic. More than half (53 per cent) of the CFOs in tourism and travel declare that they are still managing continuity while that is the case for only 4 per cent of respondents in life sciences and health care. Nonetheless, a positive mood is widespread and suggests that many companies in Europe have turned the page on COVID-19 and have begun to focus on the emerging post-COVID business environment.

If, as seems the case, the world is emerging into the post-pandemic era, it is worth examining what this new environment will look like. COVID-19 has affected how businesses operate in many ways, but especially in three areas: the rise of remote working; the digitisation of business interactions – particularly with clients or customers; and supply chain operations. In this section, we will therefore explore how financial executives in Europe see the future in these three areas and test the extent to which the changes experienced so far (or those expected) will stick.

2020 was the year that remote working went mainstream. According to Deloitte’s estimates, across Europe more than 100 million employees switched to remote working because of lockdown measures, with almost 45 million doing so for the first time.3 This massive experiment worked much better than many had expected. A few companies even announced they would allow remote working to continue indefinitely for workers who prefer it. Others are less sanguine about this prospect.4

But a future where a majority of employees will work remotely on a permanent basis – as was often envisioned early in the pandemic – does not seem to be on the cards. More than 60 per cent of executives in the survey reject this idea. Even in industries with more potential for remote working, such as technology, more than half of CFOs disagree that in the post-pandemic environment the majority of their employees will be working remotely on a permanent basis.

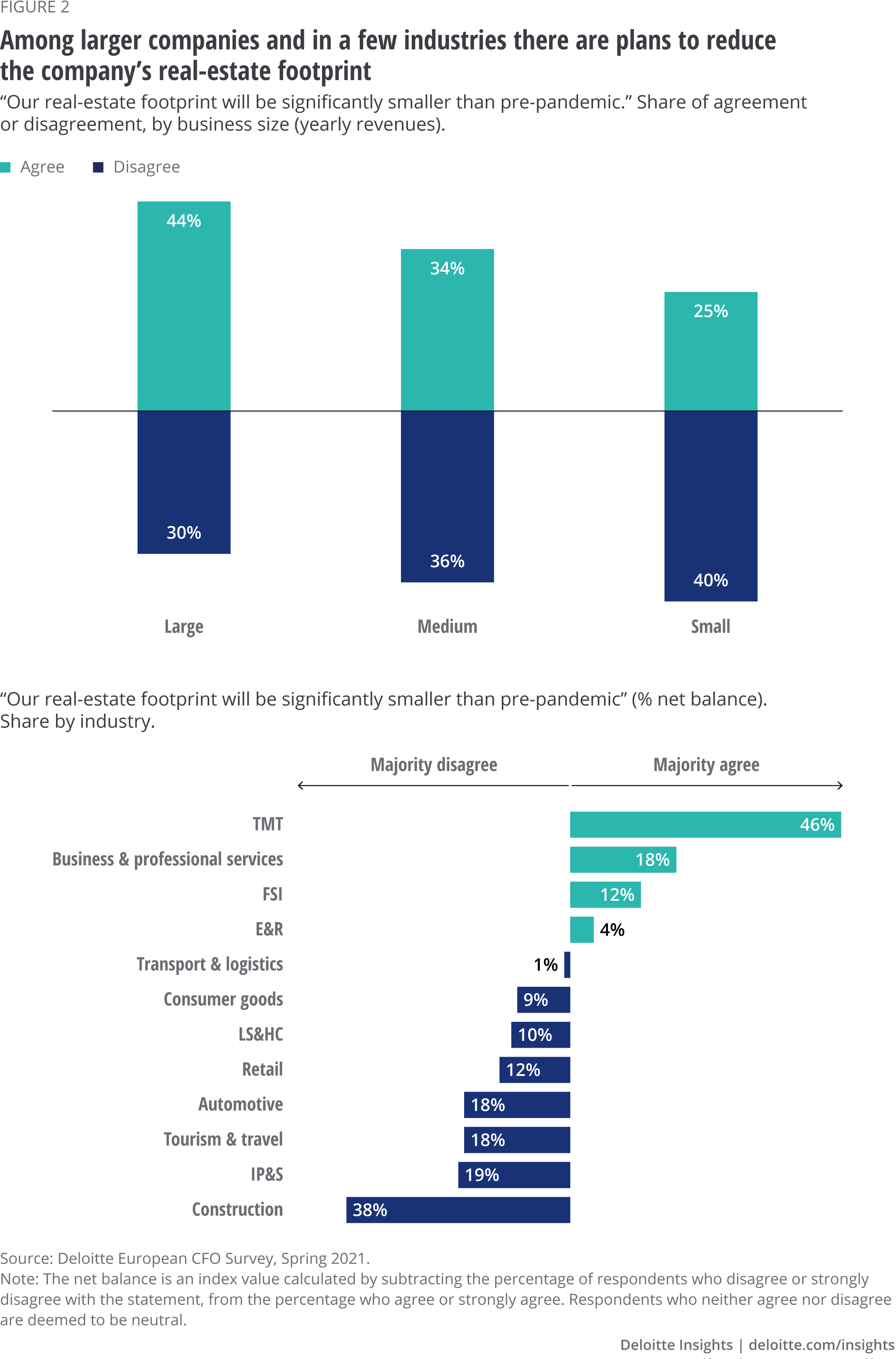

Nevertheless about one-third of respondents agree that the real-estate footprint of their company is going to be significantly smaller than before the pandemic. This is particularly the case among CFOs in technology, media and telecommunications (TMT), as well as in financial services. In general, the share of respondents reporting that they plan to reduce their companies’ real-estate footprint increases with the size of the business (as measured by yearly revenues; figure 2).

Therefore, even if COVID-19 has not put an end to the office, it has certainly sparked deeper reflection on its role and, for some companies, a re-evaluation of their real-estate strategy.

Quarantines, lockdowns and self-imposed isolation have forced companies to interact with their customers through digital channels. According to recent estimates in a United Nations report, online retail’s share of total retail sales increased from 16 per cent to 19 per cent in 2020 – with business-to-business (B2B) sales representing more than 80 per cent of all e-commerce.5 Not only has shopping behaviour changed, the pandemic has also led to a boom in digital products and services.

With the gradual reopening of the economy, many of the activities that had to migrate online can take place again in person. In summer 2020 – as the first wave of the pandemic subsided in Europe and many restrictions were temporarily lifted – the willingness of consumers to order products online or to use digital services declined.6 CFOs across Europe, however, agree that in the post-pandemic business environment, interactions with clients, customers or even prospects will be predominantly digital. Overall, about half the respondents agree with this view against 29 percent who disagree.

There are, however, differences in the extent to which executives in different sectors expect a largely digital future. Perhaps surprisingly given the surge in e-commerce over the past year, 45 per cent of CFOs in retail expect client interactions to be predominantly digital against 39 per cent of CFOs who do not – a difference (net balance) of just 6 percentage points. Only in construction and in tourism and travel is that figure smaller. At the other end of the spectrum, a net balance of 55 per cent of financial executives in TMT expect digital interactions with clients to predominate.

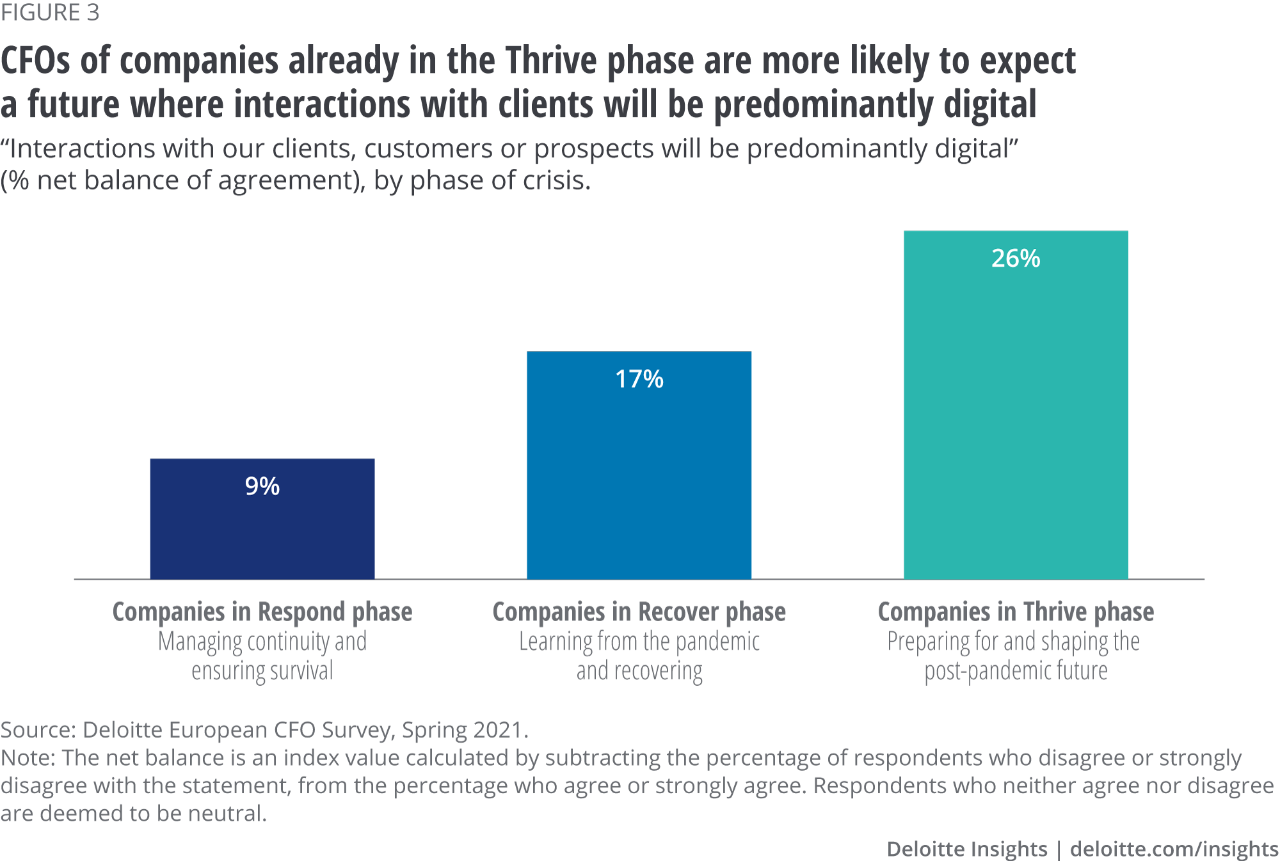

Executives in companies that are already in the Thrive phase are more likely to foresee a future where digital customer interactions prevail, irrespective of the industry in which they operate. A net 26 per cent of them agree with the statement. By contrast, only a net 9 per cent of CFOs whose company is still in the Respond phase do so (figure 3).

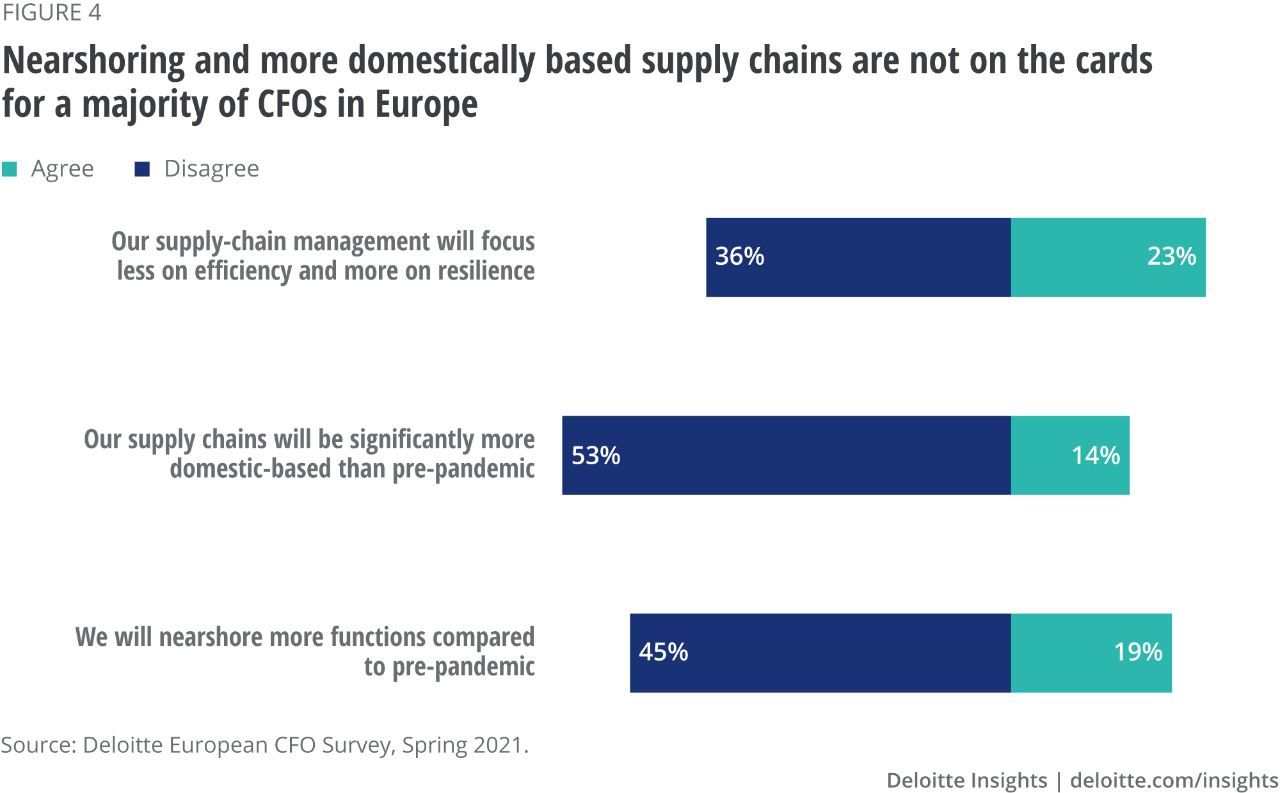

Shocks and disruptions are not a novelty in the supply chains of modern companies, exposed as they are to trade disputes, natural disasters or cyberattacks. But the disruption caused by the pandemic dragged them into the spotlight more than ever before, exposing to the broader public their hidden vulnerabilities. This led to calls for global value chains to shift from a focus on pure efficiency towards consideration of the need for resilience.7 Discussion of geographical diversification in production sites and suppliers has intensified, prompting speculation about a retreat from global supply chains and the rise of more local or regional networks.8

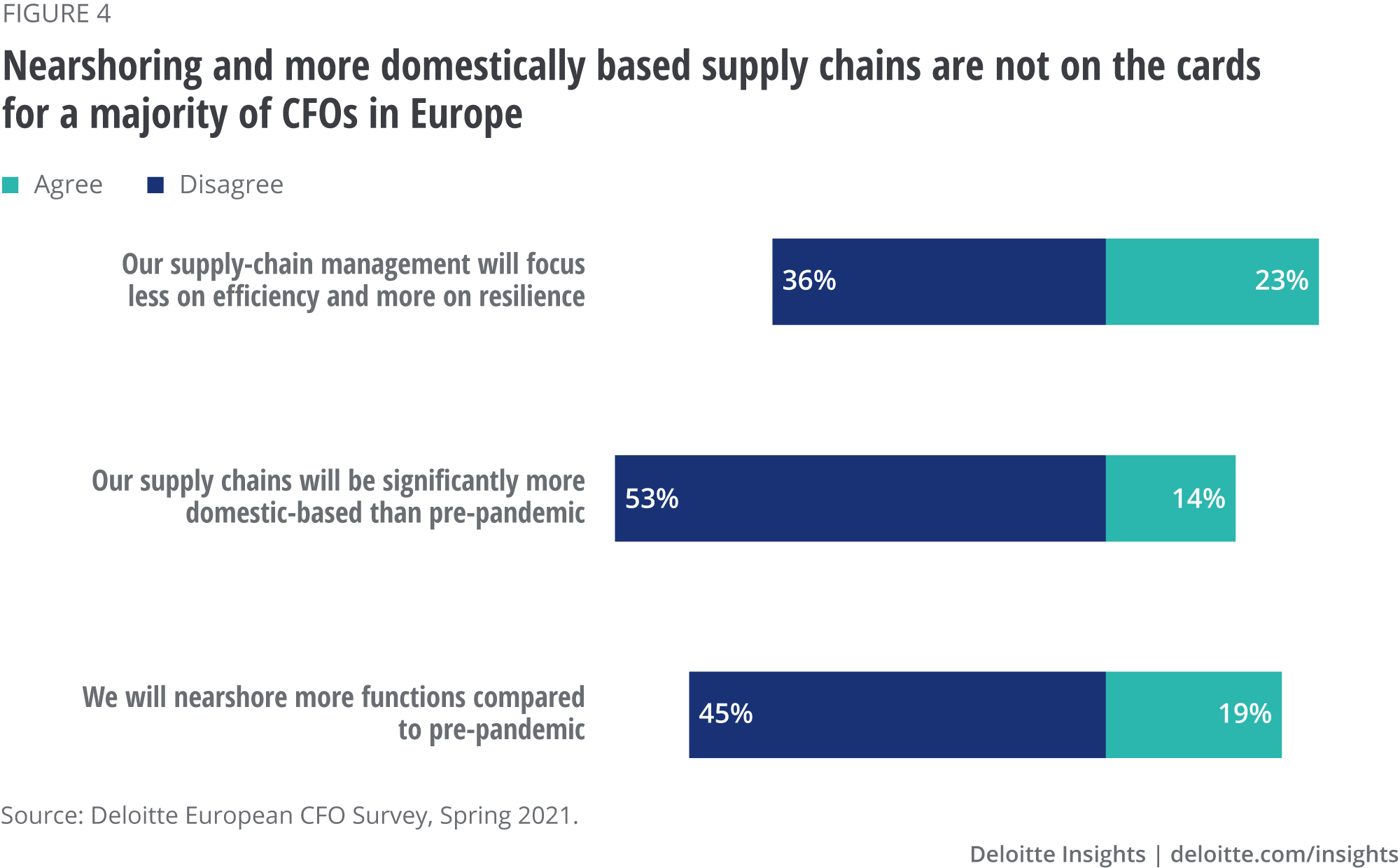

The results of our survey, however, provide only moderate support for the idea that companies are shifting the focus of their supply-chain management towards resilience.

Overall, about one in four CFOs (23 per cent) agree with this view. However, more than a third (36 per cent) soundly reject the idea, and a relative majority (41 per cent) take a neutral stance. And even if the focus of supply management is shifting, that does not mean a post-pandemic world will emerge in which supply chains are shorter and more national. More than half the respondents disagree that compared to pre-pandemic the supply chain of their company will be significantly more domestically based (figure 4). Among CFOs of larger companies the share is even larger, with more than 60 per cent disagreeing. Even among those respondents reporting that the resilience of supply chains is coming more into focus in their company, more than 40 per cent disagree with the idea that supply chains will be more domestic in the post-pandemic environment.

Similarly, more than 40 per cent of CFOs do not expect to ‘nearshore’ more functions in the post-pandemic environment, twice as many as those planning to do so. However, within the group of respondents who are focusing more on the resilience of their supply chains, executives who see a post-pandemic future with more nearshoring do slightly outnumber those who do not.

Altogether, the post-pandemic future financial executives envisage does not look revolutionary. Remote working is going to be more pervasive but still not the prevalent form of work; the real-estate footprint will shrink for about one-third of companies, but not for the majority of them; and relatively few companies seem to have plans to localise or regionalise their supply chains. The only area where there is a clear indication of a major shift relates to the prevalence of digital interactions with clients.

Yet it would be a mistake to underappreciate the extent of the transformation currently taking place in the business environment. In the end, progress is often more evolution than revolution. Thus, even if the majority of employees return to working in offices, companies need to reconsider the role of the workplace, understanding how it adds value and investing in the type of real estate that best supports how work will be conducted in a more hybrid arrangement.9 And even if supply chains remain global and interconnected, the pandemic has highlighted that many organisations are not set up to manage this interconnectivity optimally when adverse events occur.10 Addressing this vulnerability might imply the need for new technologies but also a reassessment of supplier payment terms or of vendors.11

In the end, whether facing a gradual transformation or a sudden shock like the pandemic, organisations need to be able to adapt, endure and rebound – that is, they need to be resilient. In the following, we explore what areas companies in Europe are prioritising to build resilience in their organisations.

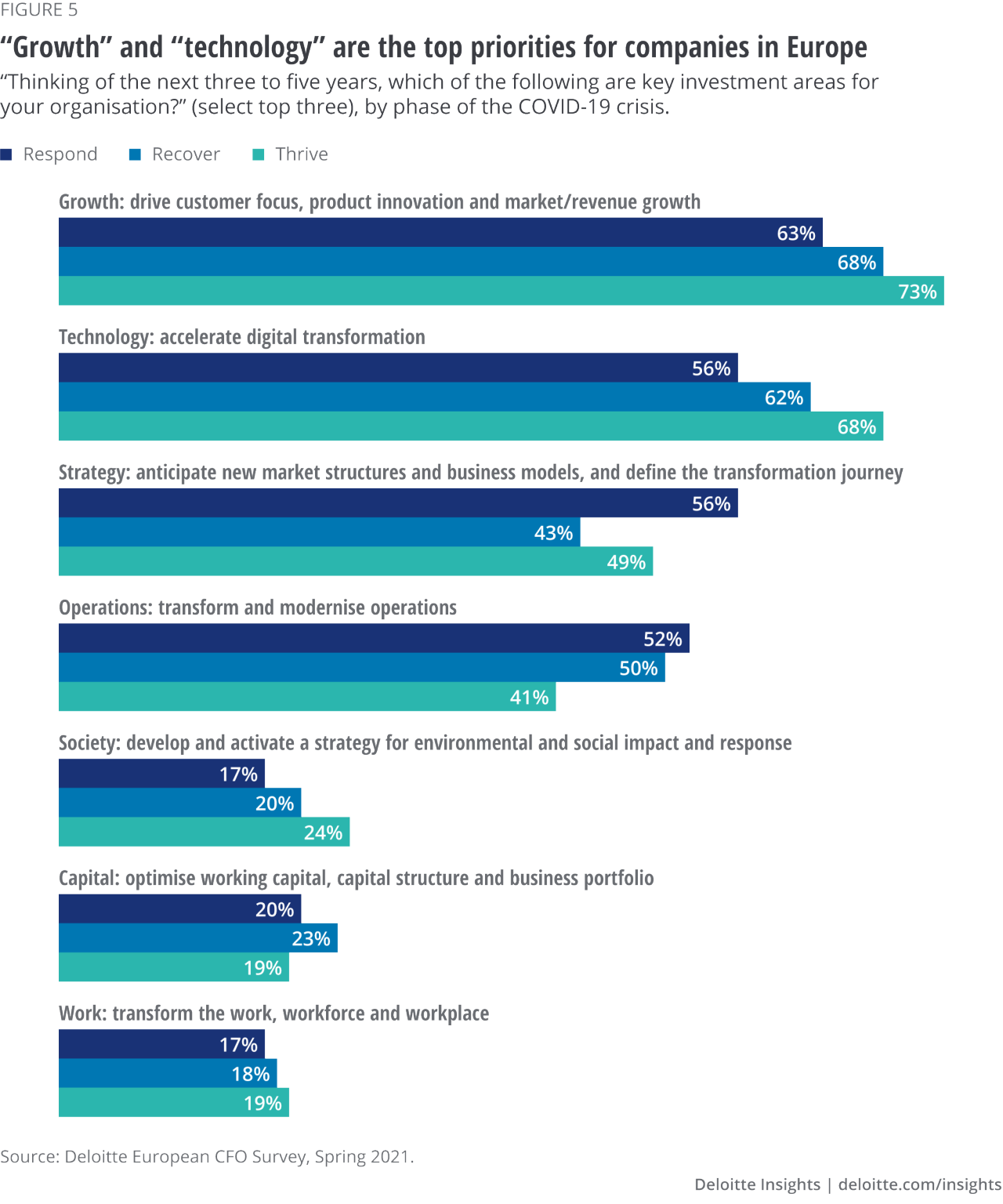

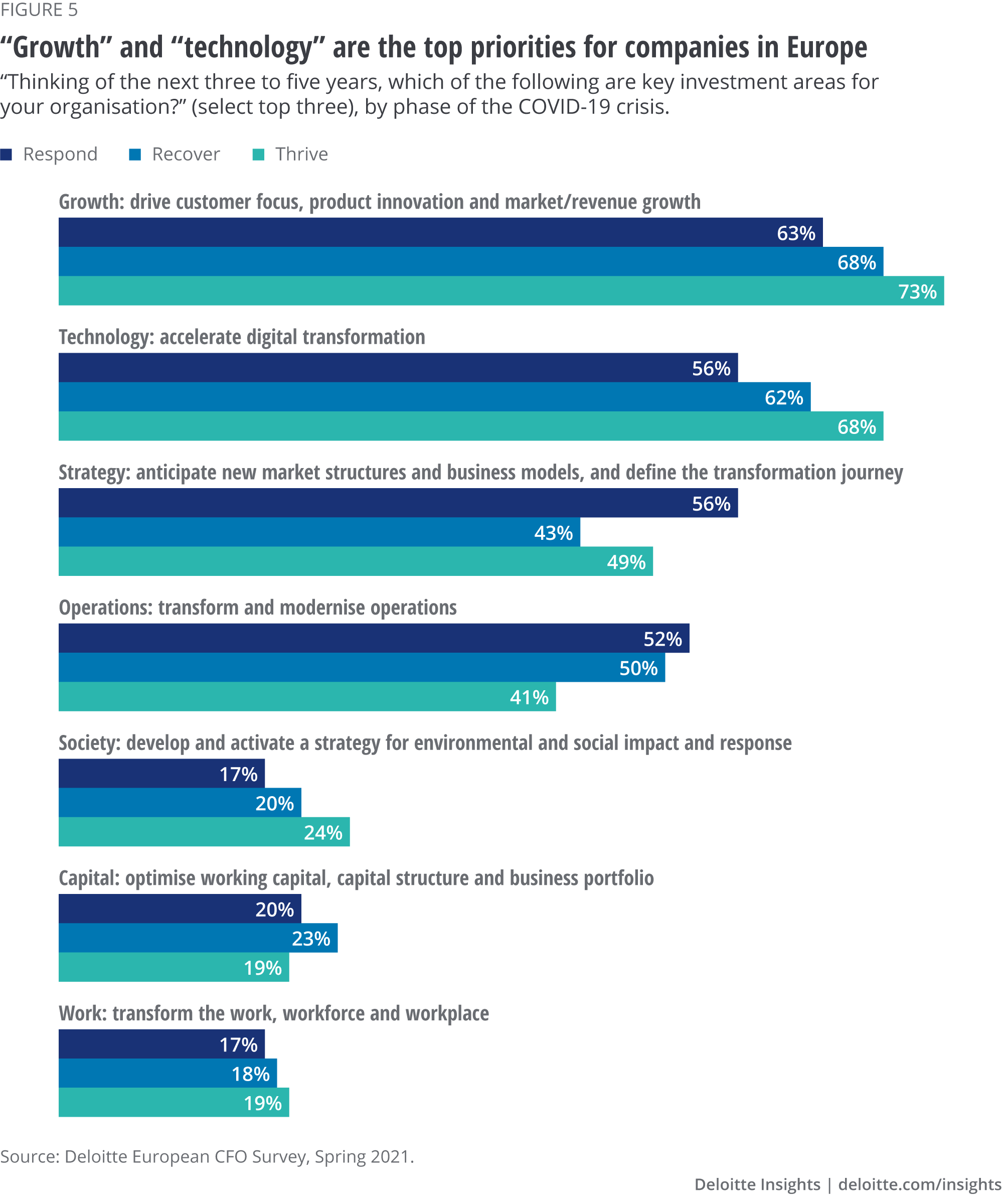

According to previous Deloitte research, a resilient organisation requires seven key elements: strategy, growth, operations, technology, work, capital and society. These elements, while being strong independently, need to operate within a cohesive, interdependent web that reinforces each of the parts and enhances the organisation’s adaptability.12

We asked the survey participants what elements they see as a priority for their company over the next three to five years. For the majority of executives, “growth” and “technology” represent a top priority (figure 5). However, a few differences emerge across companies at different stages of the pandemic crisis cycle. For example, while 52 per cent of CFOs of companies in the Respond phase and 50 per cent of those in the Recover phase consider resilient operations one of their priority areas, that is the case for only 41 per cent of CFOs of companies in the Thrive phase.

What also emerges is that despite the growing pressure on companies to lead on societal and environmental issues and to hold themselves accountable to a wider range of stakeholders,13 overall only 22 per cent of executives consider “society” a priority element. In general, however, the relevance assigned to this element increases the further the company is along the crisis response cycle. Thus, while 17 per cent of companies in the Respond phase select “society” as one of their top three priorities, this is the case for 24 per cent of CFOs in companies already in the Thrive phase. But even for these companies “society” ranks in the lower half of their priority areas.

The optimisation of working capital and of the capital structure does not rank as a high priority either – and least so for companies in the Thrive phase, where “capital” ranks at the very bottom of their list. Record levels of monetary and fiscal stimulus across the major economies worldwide are ensuring favourable conditions on the financial markets – this may be making the reassessment of capital needs a relatively low priority.

As if to reinforce the message that the post-pandemic reality will represent an evolution to more fluid work environments rather than an abrupt transition to fully remote working practices, the element “work” ranks at the very bottom of the priorities. Less than one in five CFOs consider the transformation of the work, workforce and workplace a priority area in the near future.

Taken together, the results reveal a forward-looking attitude across Europe, with a majority of companies focused on the post-pandemic reality. For now, the most extreme predictions about the consequences of COVID-19 on the business environment do not seem to be materialising. However, the increased use of digital technology during the pandemic appears to be here to stay and will have long-lasting consequences for how business is conducted. Accordingly, the vast majority of companies across Europe consider customer focus, product innovation and market growth, as well as acceleration of their digital transformation, as their top priorities. All C-suite members need to be accountable for building up resilience in these areas as the actions needed and their implications reach across all functions.

What companies have learned from the COVID-19 experience and what they will need to do differently varies according to their size and industry. Even if the pace of the recovery has been faster compared to other crises, the pandemic has affected the way people interact with each other and the way individuals think about their interactions. This is a fundamental change with deep impacts across different sectors.

Although there is no magic recipe that applies to all companies, there are three principles that we would like to highlight. Now more than ever companies need adaptable employees, a culture and structures that ensure a collaborative working style and fast decision-making, and transparent and honest communication with the most important stakeholders. Focusing on these three pillars will help companies strengthen the seven elements of resilience and be ready for the next crisis, in whatever form it comes.

The authors would like to thank Ram Sahu for his research support in various stages of the project.

Cover image by: Mark Milward