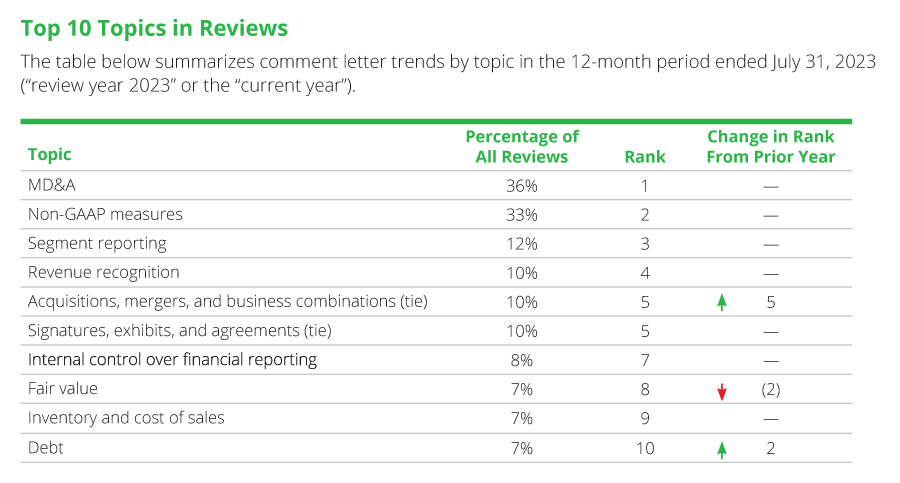

Top 10 topics in reviews

The table below summarizes comment letter trends by topic in the 12-month period ended July 31, 2023 (“review year 2023” or the “current year”).

The topics that constitute the current year’s top 10 list are largely consistent with the prior year’s list, with debt joining the top 10 list and climate change dropping out of the top 10.2 Comments on MD&A and non-GAAP measure disclosures continue to increase in number, and these topics are still the two most significant sources of SEC comments. We also observed an increased number of comments related to acquisitions, mergers, and business combinations, which rose from 10th place in 2022 to 5th place in 2023 (tied for 5th with signatures, exhibits, and agreements) after a rise in merger and acquisition activity over the past several years. In addition, debt moved up two spots to 10th place.

Conversely, climate change (ranked 8th in 2022) fell just outside the top 10 list in 2023. The decrease in rank is largely due to the broad increase in SEC comments issued in the current year from prior years, which led to a decline in reviews with climate-change comments as a percentage of total SEC reviews that resulted in a comment letter. However, the SEC staff continues to issue comments on this topic and issued such comments to a similar number of registrants in both review year 2023 and review year 2022. The staff has begun to release climate-change-related comment letters for reviews conducted in the late summer and fall of 2023 and continues to focus on climate-change disclosures in advance of an expected final rule.

Further, although not identified as a separate top 10 topic, the impacts of higher interest rates, inflation, supply- chain issues, COVID-19, and the Russia-Ukraine war remained a source of SEC comments over the past year. Such comments have focused on disclosures related to the effects of these macroeconomic and geopolitical challenges on a registrant’s (1) risk factors, (2) MD&A, (3) early-warning disclosures about impairments, and (4) adjustments to non-GAAP measures.

A number of the aforementioned trends are likely to continue in years to come since comment letter topics have been largely consistent year over year. While it is difficult to predict what new comment letter trends are on the horizon, we look to the Commission’s priorities to help us predict topics of focus in the coming year. Recent SEC disclosure rules and interpretive guidance related to non-GAAP measures and key performance indicators and metrics may result in increased focus and scrutiny from the SEC staff. Given that the staff often focuses on compliance with new reporting requirements, we expect to see comments on disclosures about cybersecurity risks and share repurchases next year. As the SEC works toward issuing a final rule on climate-change disclosures, we expect the Commission to remain focused on how registrants have complied with the existing interpretive guidance. In addition, we expect the SEC staff to continue monitoring the impacts of higher interest rates, tightening credit, inflation, supply-chain and labor issues, geopolitical conflicts, and concerns about the real estate and banking sectors, as well as other emerging market events, and perhaps focus future comments on accounting and reporting related to these matters. These events, coupled with the staff’s focus on ensuring that MD&A provides useful information to investors, mean that comments on MD&A are likely to stay elevated. The staff may also comment on disclosures about the known trends and uncertainties related to income tax as a result of the Inflation Reduction Act and the implementation of the Pillar Two rules issued by the Organisation of Economic Co-operation and Development.