Enabling energy transition has been saved

Perspectives

Enabling energy transition

Joint ventures in hydrogen, carbon capture, and more

There are incentives for companies to invest in energy transition—due to headwinds in traditional energy and significant subsidies for emerging energy markets. But obstacles exist spanning value chain security, technological uncertainty, and scale. How can joint ventures in markets such as hydrogen help mitigate these risks and gain market share?

Energy transition: A global view

Global investment in the energy transition reached an all-time high in 2022, including a near tripling of investment into emerging markets such as hydrogen and carbon capture and sequestration (CCS). Now with governments around the world injecting significant capital into these fledgling industries (including the multibillion-dollar 45V and 45Q credits for hydrogen and CCS within the Inflation Reduction Act), companies are looking to capitalize on reduced costs to enter these markets of the future.

However, these newer markets bear substantial strategic risk associated with rapid technological innovation and disruption, as well as market ecosystem immaturity and uncertainty. These risks are heightened by the capital-intensive nature of the energy industry and the scale often required to compete without government incentives.

Eighty percent of energy and chemical (E&C) executives believe that their traditional capital investment approach is ill-equipped for the energy transition.1 This push has contributed to a shift in clean energy joint ventures, which now account for one-third of joint ventures and strategic alliances by oil and gas (O&G) companies, the largest share being in hydrogen.2

Accelerating energy transition through joint ventures

Three challenges to energy transition opportunities

Even with government subsidies, new energy markets are inherently capital-intensive, requiring substantial investments in infrastructure, equipment, and research and development (R&D).

Capital requirements heighten strategic risks companies face in selecting and investing in different energy transition growth pathways. As a result, investments can prove to be difficult to justify in the short term. Companies must balance their investment plans while also ensuring their traditional operations remain competitive, as those operations will likely continue to play an important role in the energy mix over the next several decades.

Emerging energy transition markets such as hydrogen and CCS require development throughout the market ecosystem to be commercially successful and sustainable for end markets.

Several energy transition opportunities involve multiple interconnected industries—from renewable energy generation to vehicle manufacturing. The security of value chains and the requirement for co-development for both practical and economic scale are significant challenges for companies looking to enter growth markets—but necessary in many cases for sustainable use in end markets.

Advancements in applicable and competing technology will determine winners and losers.

The industry is characterized by rapid technological innovation, which presents both challenges and opportunities. The fast pace of change and uncertainty of outcomes require companies to continuously evaluate new technologies and employ an agile strategy that allows strategic adjustments and optimizations.

Joint ventures and alliances: Harnessing partnership advantages

Companies must determine where they can create the most value within the ecosystem of an emergent market and what pursuit strategies are suitable for the market segment’s maturity level. In energy transition, these strategies have included the entire corporate toolbox including acquisitions, alliances, joint ventures, long-term partnerships, internal R&D, and organic growth. There has also been an increase in corporate venture capital as companies seek to gain exposure and insight into nascent technologies.

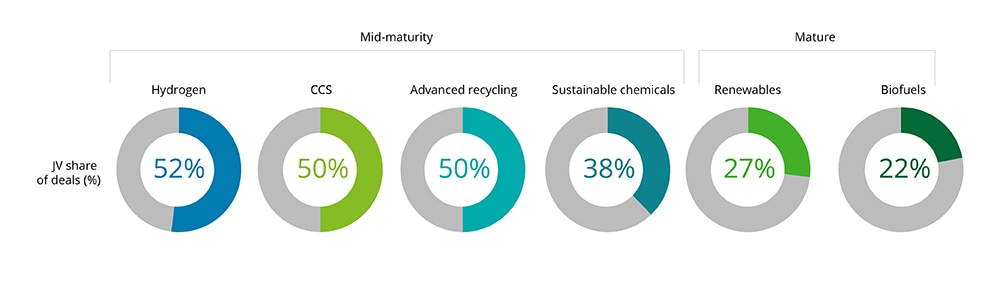

Of these approaches, joint ventures have emerged as an integral part of corporate dealmakers’ strategies to capture growth in mid-maturity markets. This is particularly seen in areas such as green hydrogen, CCS, advanced chemical recycling, and sustainable chemicals where the strategic risk can be significant with traditional investments due to the step-up in capital intensity, high green premiums for acquisitions, and considerable uncertainty of the technology and market winners.

Source: Deloitte analysis of data from PitchBook.com

With the help of government investment and regulation, several energy transition opportunities are moving rapidly into the mid-maturity space where projects are becoming shovel-ready but still possess significant strategic risk. The most notable of such markets for E&C companies are the hydrogen and CCS markets.

Joint ventures offer three major strategic advantages over traditional merger and acquisition (M&A) practices.

Opportunities await

The energy transition is growing rapidly and maturing quickly, and it is unquestionably fraught with strategic risk. The ideal strategy to pursue growth opportunities will ultimately depend on factors such as capital requirements, ecosystem maturity and sustainability, the value of control and market share ownership, and the likelihood of commercial success. As opportunities mature, joint ventures are emerging as an increasingly popular way for companies to pursue energy transition opportunities. To learn how to successfully execute energy transitions, download the full report.

1Shishir Bhargava and James Bamford, “Research: Joint ventures that keep evolving perform better,” Harvard Business Review, April 12, 2021.

2Amy Chronis, Melinda Yee, and Kate Hardin, “2023 oil and gas M&A outlook: Pivoting for change in five strategic moves,” Deloitte Insights, February 20, 2023.

Get in touch