ASU 2018-12: Long-Duration Insurance Contracts has been saved

Perspectives

ASU 2018-12: Long-Duration Insurance Contracts

Targeted financial reporting improvements

The Financial Accounting Standards Board (FASB) recently issued Accounting Standards Update (ASU) 2018-12, which amends the accounting model under the US Generally Accepted Accounting Principles (GAAP) for certain long-duration insurance contracts and requires insurers to provide additional disclosures in annual and interim reporting periods.

Sept 27, 2018

A blog post by Wallace Nuttycombe, principal, Deloitte & Touche LLP

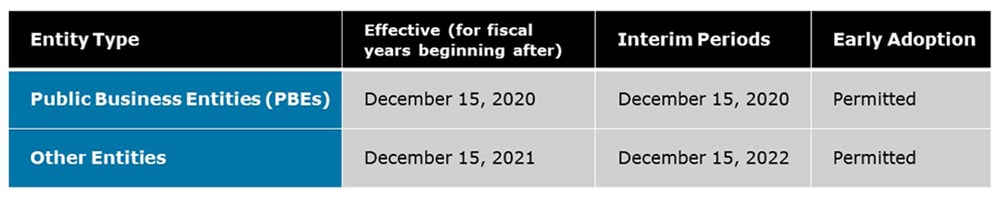

The FASB believes that the targeted improvements of ASU 2018-12 will provide more timely and useful information to financial statement users. The new guidance will have a significant impact on insurers and reinsurers. The table below illustrates when the ASU is effective:

The key objectives of ASU 2018-12

The ASU’s amendments strive to improve the following areas of financial reporting:

- Measurement of the liability for future policy benefits related to nonparticipating traditional and limited-payment contracts

- Measurement and presentation of market risk benefits

- Amortization of deferred acquisition costs (DAC)

- Presentation and disclosures

The FASB has made these changes to provide timely and useful information to financial statement users and to simplify how insurers apply certain aspects of the accounting model for certain long-duration contracts.

Measurement of the liability for future policy benefits

The ASUs’ amendments change the following aspects of how an insurer will measure the liability for future policy benefits for nonparticipating traditional and limited-payment long-duration contracts:

- How frequently the insurer will update its cash flow and discount rate assumptions

- Nature of those assumptions

- The discount rate used for measurements

- How insurer will account for its updated cash flow and discount rate assumptions

Although the changes impact certain aspects of how the liability for future policy benefits is measured, the ASU retained certain aspects of the net premium reserving model and the principle that the liability that should be accrued as premium revenue is recognized. The formula below is used to determine the ratio that will eventually compute the liability for future policy benefits. Interim periods do not generally require updates to the net premium ratio. However, insurers are required to update it annually unless it is necessary to do so in an interim period.

The various assumptions that are incorporated in the revised measurement model are:

- Discount Rate

- A discount rate based on the yield of an “upper-medium-grade (low-credit-risk) fixed-income instrument” (equivalent to an A-rated security in today’s market) will measure the liability for future policy benefits AND reflect the duration characteristics of the liability and reflects the duration characteristics of the liability.

- Mortality/Morbidity

- Terminations/Lapses

- Expenses1 (excluding acquisition costs and costs required to be charged to expense as incurred)

The objective is to maximize the use of relevant observable inputs and minimize the use of unobservable inputs. Current guidance in ASC 944 requires a discount rate that is based on estimates at contract inception of the anticipated investment yield on the underlying asset portfolio over the life of the contract.

Calculating a net premium ratio in interim periods are not required. ASU requires a review and, if necessary, update on an annual basis unless evidence suggests an interim update is needed. The net premium ratio cannot exceed 100 percent and thus if the revised assumptions indicate that it will exceed 100 percent the insurer must recognize an immediate charge to net income for the period so net premiums will equal gross premiums. Because of the updates the premium deficiency test is eliminated for nonparticipating traditional and limited-payment insurance contracts as the new accounting model requires periodic assumption updates.

Contracts or contract features that provide for potential benefits in addition to the account balance

There has been an amendment to the accounting model for certain universal life-type contracts or contracts that contain features that could provide nontraditional contracts benefits in addition to the insured’s account balance. Insurers who write these kinds of contracts must assess if the benefits features meet the definition of market risk benefits. If not, they will need to assess whether they meet the criteria to be accounted for as derivatives or embedded derivatives under ASC 815, or determine whether the potential additional benefits are payable only upon annuitization.

Market Risk Benefits—The Market Risk Benefits is a new concept under the ASU. This new requirement for certain market risk benefits will apply to contracts or contract features contained in both separate account and general account nontraditional products.

Contracts with Annuitization or Death or Other Insurance Benefits—The computation for additional liability for annuitization or death or other insurance benefits has been modified to align with other changes made by the ASU.

Deferred Acquisition Costs (DAC)

The changes here are related to the manner and timing of DAC amortization for all long-duration contracts, including participating contracts. This also applies to other capitalized balances that were previously amortized in proportion to premiums, gross profits, or gross margins.

Revenue recognition for limited-payment contracts

The changes here are related to the manner and timing of DAC amortization for all long-duration contracts, including participating contracts. This also applies to other capitalized balances that were previously amortized in proportion to premiums, gross profits, or gross margins.

Disclosures

The purpose of the enhanced disclosure requirements is to allow users to understand the amount, timing, and uncertainty of future cash flows arising from the (insurance) liabilities. This requirement is fulfilled by obligating insurers to provide both interim and annual financial statements. The insurer should focus on significant categories and include the amounts of insignificant categories in the reconciliations.

While the ASU amendments have impacted certain aspects of the accounting model, it is important to note that the types of entities that are subject to the long-duration insurance contract accounting and disclosure guidance under ASC 944, as well as the accounting models for annuitization and death or other insurance benefits, generally have not changed.

In future posts, we will follow-up with a more specific discussion about the revisions to the discount rate, the introduction of market risk benefits, the complications with a transition and other topics. Notably, how this accounting standard will force significant change within the finance and actuarial departments at insurance companies, and promote more coordination between these core team.

More to come. Stay tuned.

1 Apply to expense portion of Net Premium Ratio

Visit the Controllership Insights blog for additional blog posts.

This publication contains general information only and Deloitte is not, by means of this publication, rendering accounting, business, financial, investment, legal, tax, or other professional advice or services. This publication is not a substitute for such professional advice or services, nor should it be used as a basis for any decision or action that may affect your business. Before making any decision or taking any action that may affect your business, you should consult a qualified professional advisor. Deloitte shall not be responsible for any loss sustained by any person who relies on this publication.

Recommendations

Operationalizing the new lease standard

Lease accounting