Perspectives

The Deloitte Research Monthly Report

Issue XXI

20 December 2016

Economics

Muddling through or a mini big bang?

Sooner or later, exchange rate volatility will invite heavy-handed intervention. According to the Wall Street Journal of November 25th 2016, a joint circular by the State Council, National Development & Reform Commission (NDRC) and Ministry of Commerce (MOFCOM) was issued in an effort to control the avalanche of outbound investment that was the effect of a depreciating RMB. This development should not come as a surprise because many signs since last summer (China devalued the RMB by 1.8% on August 11, 2016) have suggested that the Government is becoming uncomfortable with exchange rate volatility, especially when the dollar’s strength is rapidly getting entrenched. Under the new rules, the government will carefully scrutinize any outbound deals worth more than US$1 billion if it does not involve the core business of the acquiring company. In addition, SOEs will not be permitted to invest more than US$1 billion on any overseas property transaction.

However, in practice such reviews are often quite subjective and the application of the ruling somewhat arbitrary. But what is already evident though, is that the tedious review process by various government agencies has already begun to severely constrain Chinese firms’ overseas acquisitions. More often than not, higher bidding prices are required in order to offset the “approval premium”. It is still too early to say that the Government has abandoned its endorsement of China Inc.’s “going abroad” strategy, but what is clear is that exchange rate stability has taken priority. Desperate times call for desperate measures – or so the official thinking goes.

But are the times indeed so desperate? By November this year, despite a continued fall since August 2015, China’s foreign exchange reserves stood at $3.05 trillion, still a hefty amount by any measure (import coverage ratio and ability pay off foreign currency debt which was at negligible level). The reality is that China is by no means in the situation in which such desperate measures are required because its “depleting reserves” are still more than the sum total wealth of the top ten countries with largest foreign reserves.

Chart: Total reserves in months of imports

In general, a country does not need to maintain more than 6 months of reserves in months of imports (developed countries have an even lower ratio)

But is there a threshold level of reserves? In general, any country’s reserves should pay for six months of imports plus servicing interest rate payments on its foreign currency debt (import coverage ratio is a whopping 18 in China). Of course, China would never tolerate reserves to fall to six months of imports worth, which means China could be tempted to engineer a one-off devaluation if reserves come down by another $1trn. (China would have saved over $600bn if it had chosen to have a one-off adjustment, say, 10%, last summer. Instead, China adjusted the exchange rate by 1.8% on August 11, 2015).

So if the reasoning behind such rulings isn’t economic, what is it? The main reason for policymakers to adopt such “desperate measures” is the greater bias towards stability in the run up to the 19th Party Congress. Thus, politics is what makes the authorities so sensitive to the persisting weakness of the RMB (in our view, they should not be) and that is also why we do not think they will undo such draconian controls any time soon. In fact, we expect more implicit and explicit controls to be implemented as China gets closer to the 19th Party Congress (in Oct 2017).

On the other hand, if one takes exposure to international trade as one’s barometer, China is in fact already a very open economy and such controls, draconian though they seem, will in time get gradually eroded by leakages. But, for the near future, tighter capital controls will not mitigate but rather reinforce the bearish sentiment on the RMB and, given the herd mentality of Chinese consumers, will only serve to exert further downward pressure on the RMB. This is how such interventions result in distortions. Yet, despite the fact that we strongly believe that a one-off devaluation is far better than such piecemeal administrative measures, policymakers seem to favour the `muddling-through’ strategy and are hoping that the mighty dollar will correct itself soon so that they do not have to do anything (i.e., to adjust the RMB exchange rate in a meaningful way).

But what if the dollar does not have a correction soon? We do not believe that China will suffer from a Malaysia-type crisis (as in 1998 and 2014) whatever the policymakers may do. That said, if China could draw certain lessons from Malaysia’s introduction of capital controls in an open economy where leakages were pervasive, the right approach would be to introduce capital controls only after the exchange rate is set at a relatively less over-valued level (as Malaysia did in 1998). It is difficult to argue that the RMB is cheap at 6.9 to the dollar when de-leveraging is not in sight and credit growth is likely to remain in double-digits.

The RMB seems weak because in the wake of Trump’s surprising victory and thanks to the bullish reaction of the American stock market, the dollar went up. But actually, if one looks at the RMBs position vis-à-vis IMF’s currency basket, the RMB has in fact been relatively stable. What policymakers do not want to see is a further weakening of sentiment with regard to the RMB as this might derail the stated objective of internationalization of the currency. Yet on this point, it seems that the logic of the policymakers is somewhat flawed. The degree of internationalization, in our view, is about wider usage of the currency rather than the strength of the currency per se. Sterling is still one of the most internationalized currencies, its current weakness only a reflection of fears of a hard `Brexit’ in 2017. The Japanese Yen is actually not as internationalized as the pound although it has been strong (relatively) in recent years. But for various reasons, the dominant thinking in China has been that a strong RMB is a pre-condition for RMB internationalization. A corollary of this argument is that a large fluctuation of the RMB exchange rate may derail the process of RMB internationalization. This is why the oft-repeated mantra that “the RMB does not have any basis of devaluation in the long run” is being seen by the market as an excuse for tighter capital controls.

It goes without saying that 2017 is a critical year in terms of the political calendar of China. Assuming that the top leaders will feel more confident after the 19th Party Congress, will the government shift gear towards economic liberalization? If so, market sentiment could change quickly and the downward pressure on the RMB would cease due to reduced capital outflows. But in the meantime, we should not be surprised by various implicit controls in the name of window guidance from the State Administration of Foreign Exchange. For example, large MNCs may be denied dividend repatriations. Chinese firms may be asked by the SAFE to convert their foreign exchange earnings into RMB (提前结汇) as quickly as possible. As of now, Chinese citizens are entitled to exchange up to $50000 a year but anecdotal evidence indicates that local banks have often used various administrative measures to discourage people from exchanging foreign currency (e.g., ceilings are set for each transaction and individuals are not allowed to transfer dollars to others). Presumably the logic of such control is that people could abuse such quotas by using other peoples’ names or that Chinese consumers could exhibit an even more pronounced herd mentality (as evidenced by those who have flocked to Hong Kong to purchase insurance policies this year) than they already have.

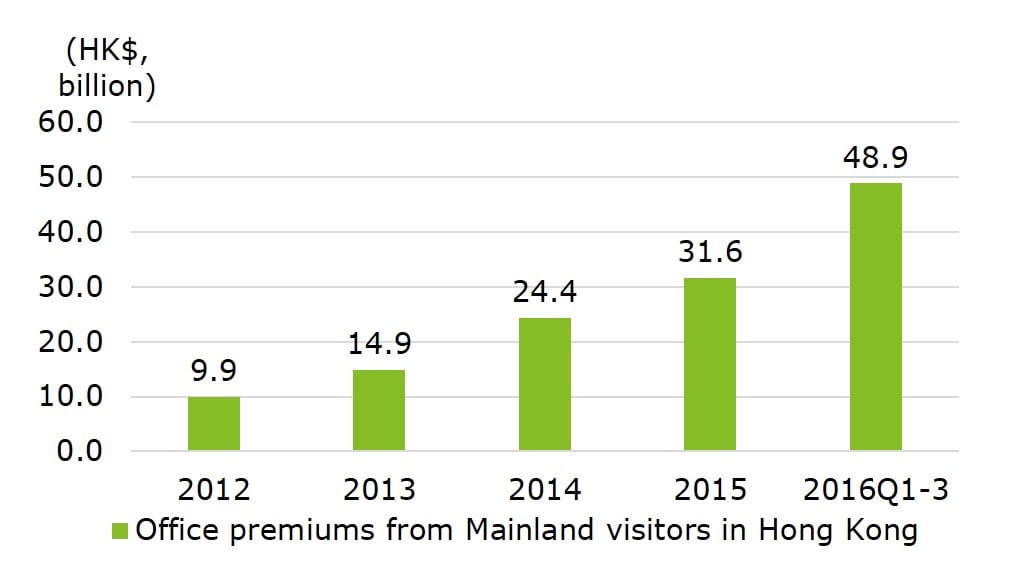

Chart: More Chinese go to Hong Kong to buy insurance

Political factors aside, other challenges also await China in 2017, the toughest one being a sooner-than-expected tightening by the Fed (the credit market has factored in 3-4 times in 2017) which could make the dollar even stronger than it is right now. Secondly, though there is little chance of a full-fledged war between the U.S. and China, trade friction is entirely possible as China has the unenviable task of cutting over-capacities in steel and several other sectors. It is likely that the Trump Administration will increase tariffs in several sectors. Protectionism, in the short term, will boost the dollar and weaken the RMB, assuming that China will make it a tit-for-tat. Another challenge could be recovering prices of commodities and crude oil (it is safe to assume that they have seen the bottom in 2016) which would reduce China’s trade surplus. As a result there could be rising inflation caused by having to pay higher prices for imports and the PBOC will be further constrained in terms of its ability to lower interest rates. This will in turn put more pressure on policymakers to use the RMB exchange rate as a monetary lever.

But coming back to capital controls. Even if these were used only as a stop gap measure, the question is moot as to whether they would work. For, in an economy like the Chinese one where the external sector is over 40% of GDP there will be no way to avoid leakages. But the message that gets sent is likely to result in more dollar hoarding as more individuals will rush to banks in order to exchange RMB for dollars. I expect that by early next year many more individuals will be using their annual quota of $50000 per person. Some people are speculating that the PBOC might even cut personal quotas next year. In which case, a black market may come into being where USD/CNY will surely be quoted at higher prices. So the bottom line remains that China is better off to adjust the RMB in a meaningful way because, on the one hand, fear of the RMB’s “weakness” is unwarranted and on the other, as we have shown, capital control could only be achieved at great cost. The experiences of many countries have shown that where there are such controls there is corruption and thus vested interests get created which make these controls difficult to phase out even after sentiment has improved. Moreover, capital controls might setback the RMB’s nascent internationalization (according to Financial Times, international trade which is denominated in the RMB has come down sharply in 2016, from 26% to 16%). The objective of including the RMB in the SDR basket (Oct 2016) was to accelerate the role of the RMB in global transactions. If China must implement capital controls in order to maintain a stable RMB exchange rate, our recommendations are to set the exchange rate at a slightly lower level and to have a clear timetable for phasing out such controls by the time the mighty dollar loses its shine.

Though muddling through has proven to be the optimal strategy in the past thirty years, where the RMB exchange rate is concerned, we feel the current situation may call for something bolder. Despite various policy confusions in China in the run up to the party congress, China today is in a far stronger position than Malaysia when it suddenly introduced forex controls in 1998, setting the ringgit at 3.8. Ample reserves aside, China today has a relatively dynamic economy in transition where demand is not being met (look no further than auto, housing, leasing, and healthcare). Though there are no figures for it yet, many firms have repaid their foreign currency debt this year, and this was in fact one of the prime reasons why the dollar reserves continued to be depleted, taxing the strength of the RMB. Since China runs a healthy trade surplus and does not face a risk of runaway inflation, engineering a one-off exchange rate adjustment while at the same time unveiling genuine supply-side reforms (e.g., doing away with the foreign investment catalogue) could quickly put a floor to the fall of the RMB whereas on the other hand, the price of muddling through could become much more costly in 2017.

Financial Services

Market live

Energy

China's overseas energy market share set to expand further

China's presence in the global power market will continue to grow as Chinese companies are increasingly looking to overseas markets for stable revenue sources and technological capability enhancement on the one hand, and exporting power plant construction expertise and services on the other. The main reason for this thrust overseas is to offset the impact of a slowing domestic market. Thus, in 2017 we expect to see the emergence of some new trends.

The power sector's overseas investment targets are expanding beyond traditional markets, with a growing focus on “Belt and Road” countries and developed markets. In addition to sustaining and even increasing capital allocation in their traditional markets of Africa and Latin America, Chinese power sector players, we expect, will expand overseas energy investments in Asia and Europe. China will proactively participate in the construction of power plants in emerging Asian countries many of which are facing severe energy supply shortages. Several companies have already mapped out promising plans for future power infrastructure development projects in these regions. Where the European market is concerned, China will continue to target European energy assets as a key route to expand its influence in the region. SOEs have competitive advantages given their easy access to low-cost capital in contrast to many other companies or countries where debt reduction is the top priority. For example, China State Grid has been very active in acquiring a stake in the power grids of Portugal and Italy.

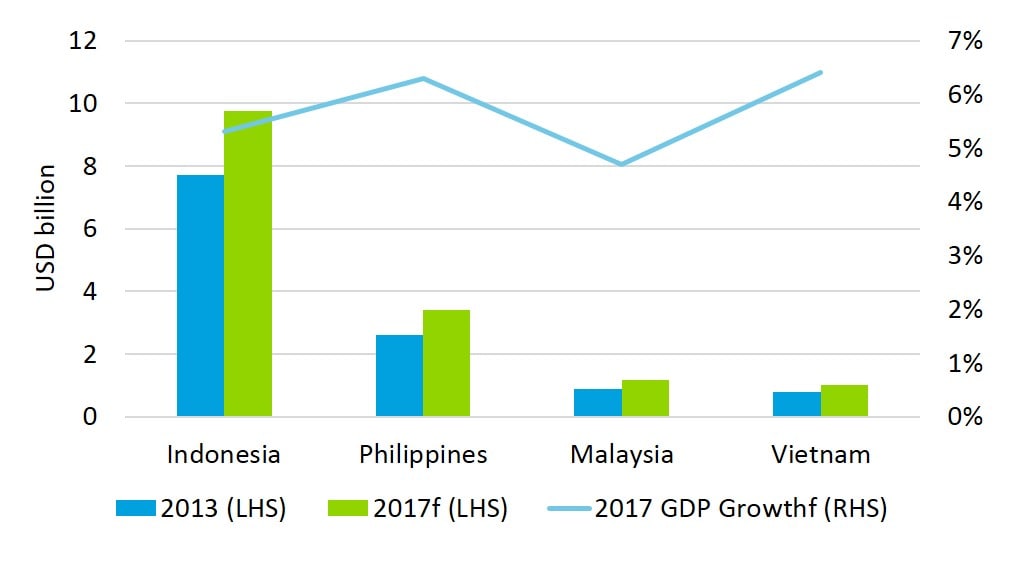

Chart: Power Generation & Transmission infrastructure Industry Value of Selected ASEAN Countries

Aggressive renewable energy capacity targets of emerging markets will drive Chinese companies to expand their footprint in renewable energy technologies. Driven by the rising costs of fossil fuels many emerging countries in Asia, Latin America and Africa have set themselves ambitious renewable energy capacity expansion targets with attractive financial incentives for energy companies. These targets will be a driver of demand for Chinese project operators and EPC (Engineering Procurement Construction) contractors. Although hydro and solar power will dominate in terms of new capacity, Chinese companies are also exploring opportunities for developing other renewable energy technologies. For example, KS ORKA Renewable of Singapore, a JV between China Zhejiang Kaishan Compressor and Icelandic Hugar Orka, acquired a 95% stake in an Indonesian geothermal power company in August 2016.

Chinese power plant contractors will need to enhance their overseas expansion model beyond the traditional EPC (Engineering Procurement Construction) approach. An increasing number of overseas project owners (most of them backed by their governments) will require traditional EPC contractors to expand their business scope to include other support services such as financing, public-private partnership etc. This means that Chinese companies will need to explore new business models such as EPC+ Financing or EPC+PPP (Public Private Partnership). For example, in the Hai Duong thermal power project, the largest Chinese investment in Vietnam so far, China Power Engineering Consulting Group is not just the EPC contractor but also the owner of 70% of the investment.

Competition from Japan in the overseas energy market will become more intense, especially in the ASEAN region. Both China and Japan have adopted aggressive infrastructure export strategies and have become the largest national sources of financing for development projects. Competition in the ASEAN region will become increasingly intense as both countries have announced more initiatives to promote investment in 2017. China pledged in November 2015 additional USD 10 billion in loans for the ASEAN region while Japan launched the Japan-Mekong Connectivity Initiative in May 2016, pledging USD 7 billion for the development of Japan-Mekong Connectivity Program infrastructure projects in the region in the next three years.

Automotive

Auto market to slow as future demand is brought forward

On Dec 15th, the Chinese government announced it will extend the tax break policy to 2017, with the tax rate raised from the current 5% to 7.5%, allowing it still below the normal rate of 10%. Given the size and contribution to GDP growth of the automotive industry, the Chinese government is highly anticipated to continue the purchase tax reduction policy to avoid any significant swings in the sector. In this regard, we forecast auto sales to grow at a clipping 4-5% in 2017 as consumers rush to take advantage of tax breaks, advancing purchases that would otherwise have been made a few years down the line. Tax breaks on vehicles with 1.6L and smaller engines, effective since Oct 2015, has brought forward China’s demand for automobiles at the expense of future sales growth in 2017. The tax rate will climb back to the normal rate of 10% in 2018.

Chart: Auto sales growth and forecast

We believe that government policy has become the single most important factor that drives auto demand in China as the fear of an end to tax incentives has resulted in strong advance purchases in Q4 2016. Large OEMs warned that a flat growth or even a contraction in auto sales will take place in 2017 without an extension of the current policy or the introduction of alternative incentives. A neutral outlook for 2017 is for auto sales to grow at 4-5% on the assumption that purchase tax reduction is set at 7.5% whereas a bearish outlook is a 1-2% annual sales growth with purchase tax climbing back to 10%.

- Domestic automakers’ gain in SUV will expand as the SUV fever continues

The growing popularity of their inexpensive SUV line-ups has helped fuel the increase in sales of domestic brands. In the first 10 months of 2016, the market share for domestic SUV brands skyroctered to 57% and domestic brands recorded cumulative sales of 3.93 million units. The outperformance in SUVs also helped domestic automakers gain market share in passenger vehicle sales, taking their market share in this segment to 43 percent, up 1.7 percentage points from last year. Domestic auto companies’ gain came at the expense of weaker foreign auto brands, especially the French and South Korean automakers which have been losing ground steadily to their local rivals.

Chart: SUV market share breakdown

SUV sales are expected to continue growing at a substantial pace in 2017. From the demand perspective, SUVs have overtaken compact sedans as the prevailing choice for first-time buyers as well as for trade-in buyers who are inclined to purchase SUVs due growing family size and a greater appetite for premium goods. The introduction of more compact SUV line-ups also paved the way for a stronger sales growth in 2017.

- New Energy Vehicle market will experience a slowdown

We expect a major shift in the upcoming new financial subsidy policy for the NEV sector. In a significant policy shift, the Chinese government will cut subsidies more than what is expected on the one hand and will raise the threshold for automakers that are eligible to receive subsidies on the other. As a result, we anticipate the NEV market will experience a slight fall in sales growth in 2017.

The crackdown on subsidy fraud and a policy vacuum combined to make this a hard year for NEV manufacturers which sold a total of 337,000 NEVs in the first 10 months of 2016, far behind the year’s target of 700,000 set by the CAAM. Meanwhile, MIIT recently issued a draft notice, stipulating that NEV makers won't be eligible to receive subsidies unless they use battery manufacturers whose products are on the MIIT’s catalogue. Such a stipulation largely favours domestic companies, further limiting the prospects of the New Energy Vehicle market.

- Tertiary (3rd and 4th tier) cities will lead future growth

We expect that 3rd and 4th tiered cities will play a more significant role in bolstering future auto demand in China. Given the rising household incomes and expanding national roadway networks, tier-3 and 4 cities represent a huge, largely untapped potential market. Mega cities, especially cities that have imposed vehicle purchase restrictions will mainly be driven by trade-in purchases. Based on our analysis of vehicles per 1000 persons across the country, we find that central, northwest and southwest regions achieved the fastest growth in car parc1 in the past three years, and we believe these regions will continue to be the most important source of growth for new car sales in the coming years.

1 Car parc: total number of cars on the road

Logistics

Supply chain will become the core of competition

In 2016, the major domestic express delivery companies accelerated their capital accumulation operations by investing in 'intelligent' logistics system, and improving the efficacy of their parcel delivery services. Deloitte Research forecasts that China’s express delivery volume and business revenue for the entire year of 2016 will increase 53.5% and 42.7%, respectively.

Chart: Growth rates of China’s express delivery volume and industry revenue

- In 2016, because of fiercer competition, mergers & acquisitions and industry integration have increased. In 2017, large express delivery companies will continue to turn themselves into integrated logistics service providers through M&A and diversification of their existing business. After large scale integration of existing companies, a highly concentrated oligopoly pattern will emerge. The supply chain management capability is the core competitiveness for such major logistics companies. In China’s supply chain sector, the most competitive three companies are Jingdong logistics, SF express and Ali Cainiao network which are champions in information technology and intelligent control.

- The top echelons of the express delivery industry have embraced the "going out" strategy. "The Belt and Road Initiatives" will promote the development of international logistics as more favourable cross-border logistics policy initiatives have been released over the last two years, leading to new business opportunities. Leading companies in the field, with their already considerable financing and branding advantages, will accelerate overseas deployment through building overseas storage systems either independently or through cooperating with existing international logistics giants.

- Professional logistics and intelligent logistics will usher in more development opportunities. Industry differentiation requires the express companies to provide more specialized and intelligent solutions to their client’s needs. With the swift development of new services such as cross-border e-commerce, cold chain delivery and instant distribution, professionally managed, intelligent express delivery companies will be able to take advantage of the new opportunities.