Perspectives

The Deloitte Research Monthly Outlook and Perspectives

Issue XXXVIII

27 June 2018

Economy

Embrace the US private sector in order to avoid a trade war

On June 15 the Trump Administration dropped a bombshell on US-China trade relations with its decision to levy tariffs of 25% on $50bn worth of China's exports. Moreover, tariffs on $34bn out of the $50bn worth of Chinese goods will come into effect as early as July 6. The Chinese Government reacted immediately by imposing a reciprocal tariff on US exports (mainly agricultural produce, vehicles and seafood), effectively excluding US exports from tariff reductions on automobiles etc. Undeterred, President Trump warned of fresh tariffs on an additional $200 billion worth of Chinese imports unless China made further concessions. Spooked by the possibility of trade tension escalation, financial markets slumped, with Shanghai A shares losing nearly 4% on June 19, hitting another multi-year low, underscoring investors' fears over pains of de-leveraging heightened by Fed's tightening and trade tensions. In the US, the DOW closed almost 300 points lower the same day. Meanwhile, the dollar strengthened, mainly on fears that such a standoff between the US and China would result in shocks and disruptions to the global economy. The RMB weakened against the dollar to 6.50, based on the assumption that such a trade war would certainly give an inflationary shock to the Chinese economy.

Chart: De-leveraging and trade tension led to Shanghai A share slump

In China there has been much shock and confusion regarding Trump's flip-flops on tariff imposition as many pundits had taken the view that China's pledges of greater imports from the US would keep Trump's trade war at bay. In our view, the chief reason behind the US-China trade talk impasse is that the US and Chinese governments hold very different views on the cause of the trade imbalance. From the US's perspective, China's efforts to reduce the bilateral trade imbalance are too timid and are therefore unlikely to bring about immediate results. From China's perspective, the trade imbalance is not under their control for it is a reflection of complicated global supply chains. The trade deficit is also being widened by ill-considered tax cuts by the Trump administration in the face of a strong US economy. Despite Beijing's efforts and three rounds of talks, the divergence in terms of perspective remains great. China has rebalanced its economy significantly in the past decade or so, as evidenced by a steadily falling current account surplus/GDP ratio. Yet from the US perspective, if China enjoys such a large trade surplus (roughly $350bn a year), the US ought to have more bargaining chips. As we have said earlier, trade, which is supposed to be an economic matter, has somehow become linked to the geopolitical issue of North Korea. The Singapore Trump-Kim summit on June 12 has, at least in the short run, probably made President Trump feel that less help from China is needed in stabilizing the Korean Peninsula. As an eventual denuclearized North Korea looks more promising (the premise to reach this goal without pressure from China may no longer be deemed illusory by President Trump), the US has now decided to prioritize and push harder on trade issues with China.

Assuming the diverging views on trade remain intact, what should be China's policy responses? Again, assuming that domestic politics in the US (midterm elections are around the corner) may make China-bashing popular, how should policymaking in China be framed in order to reduce the risks of trade tension escalation? One response (a tried and tested one) is that of targeted imports. However, this tactic could upset China’s other important trading partners whose exports would be adversely affected. This is exactly why the EU expressed concern over the potential substitution effect of its exports to China if trade tensions between China and the US led to a Chinese 'shopping spree' of US products.

According to the newly released Business Confidence Survey 2018 by the EU-China Chamber of Commerce, market access or a lack of it, remains a critical issue. Industrial policy is also a source of discontent and fingers have been pointed specifically at Made in China 2025 program. But, let us not forget that most newly industrialized countries have relied on government guidance and subsidies during their economic take-off. It would be unthinkable for China to scrap Made in China 2025, as demanded by the US and echoed by the EU, because the program provides a goal to Chinese companies and gives them a nudge in the right direction through the promise of subsidies. But it is also in China's best interest to avoid excessive distortions resulting from overgenerous support by local governments and to counter firms' herd mentality (e.g., the creation of excess capacity induced by government subsidies). So how to strike a balance between a gentle nudge by policymakers and a set of blatantly unfavourable industrial policies? There are no easy answers. However, if the initiative of Made in China 2025 could be made more inclusive in such a way that MNCs have foot in the game, it would be more politically difficult for the West to undertake protectionist policies towards China.

Higher tariffs by the US, in the short term, will prop up the already strengthening dollar. But the greenback's added strength is unlikely to postpone the Fed's course of tightening, presenting a challenge for some emerging markets including China. In China's case, de-leveraging has been identified as the top policy goal of this year but economic deceleration contraction that is an inevitable part of the deleveraging process is testing policymakers' resolve. US-China trade tensions have aggravated people’s fears, rightly so, creating greater uncertainty and thus making it more difficult for policy-makers to stick to their guns. For example, the drastic sell-off of A shares in mid-June was prompted by fears of a full-blown US-China trade war. Luckily the real economy is relatively detached from capital markets, so the stock market turmoil did not result in systemic risk. But it would be unwise to underestimate the lobbying efforts of retail investors who have dominated the volatile A share market. The PBOC's focused easing via reduction of the reserve requirement rate was a clear response to the bearish sentiment in the stock market.

Against such a backdrop, what should China do? We would like to reiterate our long-held views – to use the US private sector as leverage. In practice, this means significant improvement of market access to MNCs (not just the US firms). For example, in the auto sector, the relaxing of the joint venture requirement could well be viewed as an acid test of China's commitment to improving market access. If the PBOC could clearly signal its easing bias as a necessary relief to the corporate sector, as evidenced by its cut of reserve requirement rate to major financial institutions over the weekend, a managed depreciation of the RMB will be a small price to pay for keeping the real interest rates low. Rightly so, the view that the Chinese interest rate has to deviate from the global interest rate is taking hold, and a minor RMB depreciation has nothing to do with competitiveness but in fact necessary monetary easing.

Retail

Vertical e-commerce at the crossroads

Vertical e-commerce companies specializing in online retail targets specific consumer groups with specific needs. Over time, they create tailor made products and services to meet the specialized needs of their customers. This is one of the reasons behind the phenomenal growth of online retailing. The rapid growth of the online retail market has given birth to a number of high-growth vertical e-commerce companies such as Netease Kaola which primarily focuses on cross-border e-commerce and Xiaohongshu which operates on a model that combines social networking and e-commerce. Both companies have, so far, racked up billions of yuan worth of sales. However, given the continuous evolution of consumer groups and consumption patterns and amidst fierce competition from major e-commerce platforms, sustainable growth has become the key concern for these companies.

Transformation of vertical e-commerce key to breakthrough

In order to get out of the growth bottleneck, vertical e-commerce companies are trying different strategies by teaming up with BAT or embracing merchandise synergies.

Two leading social e-commerce giants, Babytree and Xiaohongshu, have completed a new round of financing and Alibaba, the e-commerce juggernaut, appeared on the investor list for both companies. As a large-scale parenting website community, Babytree has reached a valuation of around RMB 14 billion after obtaining a new round of financing from Alibaba. In addition to the injection of new capital, both sides will also deepen cooperation by tapping into their respective core competences and competitive advantages in such fields as e-commerce, C2M, advertising and marketing, knowledge payment, new retail, online and offline maternal and infant scenes and the like.

Xiaohongshu, a life-style information sharing community which is predominantly made up of female consumers operating under the "social + e-commerce" mode, secured investments from both Alibaba and Tencent. On May 31, Xiaohongshu received $300 million in a new round of financing. In the lead was Alibaba, followed by its existing shareholder Tencent, pushing up Xiaohingshu’s valuation to $3 billion. Cooperation with Tencent can help Xiaohongshu continue to strengthen its social attributes. For example, in the first half of 2018, a TV show entitled "Creation 101", which was sponsored by Xiaohongshu and released by Tencent Video, helped bring remarkable brand exposure and user growth to Xiaohongshu. The caveats however, are Xiaohongshu’s less-than-perfect e-commerce functions and limited array of product offerings. But since Xiaohongshu is facing some of the same problems that have troubled traditional e-commerce companies in the past such as supply chain and product quality issues, Alibaba, as the lead investor in the new financing round, could play an important role in guiding the development of Xiaohongshu’s future e-commerce business.

Special sale e-commerce company Vipshop also decided to partner with the giants in order to break through the growth bottleneck. At the end of 2017, Tencent and Jingdong together invested $863 million in Vipshop. The partnership with Tencent will help broaden Vipshop’s consumption scenarios and data capabilities and build up its "e-commerce + social" model. On the other hand, its cooperation with Jingdong in overseas storage will no doubt expand its cross-border e-commerce territory. Thus it becomes clear that the vast resources of China’s internet giants are being increasingly tapped into to aid some vertical e-commerce companies in their further development.

However, not all companies have taken the partnership route. Some have preferred to go it alone. As China’s No.1 cross-border e-commerce company, Netease, on June 6 changed its name to Netease Kaola and announced an across-the-board expansion to boost further growth. In addition, it also changed its slogan from “imported goods, local price” which emphasized “overseas shopping” as its main attribute, to “My Wonderful World” which emphasizes a holistic consumer experience. Though Netease Kaola is trying to become a general merchandise e-commerce company, it continues to further entrench itself in the cross-border business having successfully established partnerships with Umbra, a Canadian designed home goods brand, and Lidl, a leading European supermarket chain with more than 10,000 stores worldwide. This proves that with competitive advantage at the core of the business, horizontal expansion is also a viable choice for vertical e-commerce companies.

Possible choices for the future

In the world of e-commerce, vertical e-commerce companies which are operating at the crossroads of retail and e-commerce need to be vigilant to counter the powerful competition coming from major e-commerce giants and cope with the rapid changes within the e-commerce market. In addition to increasing capital investment and strengthening their competitive advantage in vertical e-commerce areas, existing model optimization is also a powerful way to sharpen one’s competitive edge. There are three potential ways forward for vertical e-commerce companies:

- Team up with a super platform. The super platform can provide not only solid capital support but also technological support in terms of basic technologies, application scenarios, traffic introduction and so on. Super platforms can also take advantages of the resources of vertical e-commerce companies and serve more consumers through integration.

- Stick to the specifics. Because of the rise of a new generation of consumers and constant upgrades in consumption, new or changing consumer groups and consumption patterns as well as changing consumer preferences, specific demands need to be continuously and carefully satisfied and technologies upgraded. At present and in the near future, market capacity in specific areas is to a certain extent enough for supporting the sustainable development of vertical e-commerce. Therefore, vertical e-commerce companies can achieve sustainable growth simply by sticking to specific fields and improving their comprehensive competitiveness.

- Expand business models and seek new growth drivers. As their business models mature, expansion into new areas while strengthening original areas may also be a viable choice for vertical e-commerce companies. By developing new segments of business based on their intimate knowledge of their customers and their experience in satisfying consumer needs, vertical e-commerce companies are likely to open up new growth space. In the process of transformation, vertical e-commerce companies should not only pay close attention to short- and medium-term gains but also focus on long-term benefits and sustainable development.

Tech

Short video frenzy

Douyin (also known as Tik Tok), which allows users to make, edit and broadcast short video clips, has taken China's young generation by storm. It became the world’s most downloaded non-game app in the iOS App Store. The short video app was downloaded 45.8 million times during the first three months of 2018, exceeding Facebook, Instagram, and YouTube downloads. Douyin is owned by Beijing-based ByteDance, the company behind China’s news aggregation platform Toutiao. In the last year, the short video industry has seen an unprecedented increase in competition as over 170 million new installations of video Apps and 460 million monthly active users were recorded in the same three-month period. But this is just the beginning as industry watchers predict that it will grow at a much faster rate once the commercialization of 5G technology kicks in.

The recent explosive growth in the short video sector can be attributed to three factors – an influx of capital, the entry into the sector by BAT (Baidu, Alibaba, Tencent), and lastly, the lowering of content creation barriers. In 2017 the short video industry was inundated by an influx of capital totaling RMB 5.4 billion. This is in part due to the fact that the Internet "giants" (Baidu, Alibaba, Tencent) having finally woken up to potential of this market realized that they had a long way to go before they would be able to challenge established players like Douyin. It is conservatively estimated that over one third of short video traffic eludes the big three (Baidu, Alibaba, Tencent) in spite of the fact that they have all launched their own short video apps.

In order to challenge the predominance of Douyin, Tencent paid out RMB 3 billion to lure `influencers’ to use an upgraded version of its short video streaming app, Weishi while Baidu is going to use most of its budget this year to bolster its own short-video ecosystem. This will include supporting `Nani’, a Baidu-owned app launched last December.

On the other hand, the barrier to content creation has been continuously getting smaller. Anyone with a smart phone can now immediately record and upload a 15-second short video clip, the quality of which may rival the work of a professional.

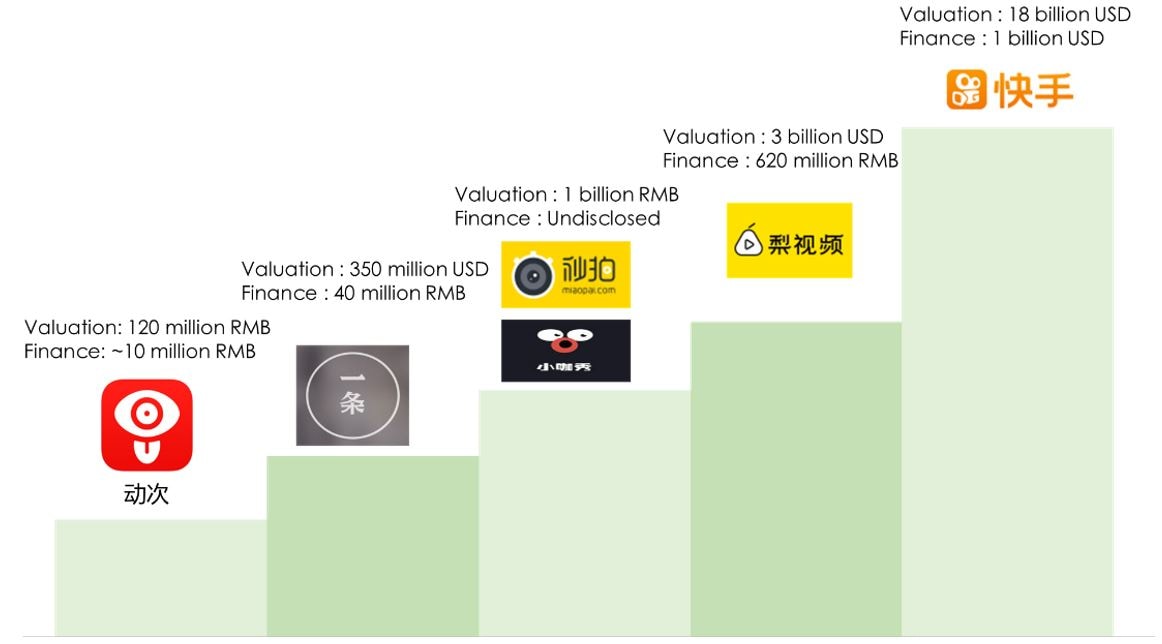

Valuation and financing of short video apps

The real battle, though, is the fight for China’s next social and entertainment powerhouse. Currently those born after 2000 use these short video platforms as the primary means of social interaction. These Apps take up a large chunk of daily user time (give the statistic, a 522% increase from last year) and has even cut into gaming time. More importantly, the short video is luring users away from posting on social media apps such as Wechat's 'Moments' board.

In the future we predict that the short video industry will evolve in the following ways:

1. Content upgrade - As these platforms continue to attract users at an extremely rapid rate, the demand for high quality content is expected to grow rapidly.

2. Consolidation - The industry is expected to go through phases of consolidation as there is not enough room for all the existing players. M&As and market consolidation is inevitable.

3. Trans-boundary - Short videos can be integrated seamlessly into other platforms such as social network and e-commerce, allowing for further development and even faster growth.

4. Going overseas - Fierce competition within the sector will force some players to go abroad in order to allocate excess capacity. Douyin's parent company has already purchased Musical.ly and Flipagram to expand its reach globally and take a bigger slice of what could become a multi-billion dollar industry.

5. Emerging technology - The most influential technology for the short video industry includes AI, AR, 5G and blockchain. AI has already had a subversive impact on content, as well as algorithm recommendation and precise recommendation engines. The advent of AR has brought many immersive experiences to the transmission of content and will lead to potential breakthroughs in content enhancement including advertising. The proliferation of 5G will make video more socially possible while copyright issues could be addressed by blockchain technology.

Logistics

Champions in Logistics

After e-commerce, internet finance, and cloud computing, logistics is the next big arena of development, providing opportunities for companies operating in China and globally. In recognition of the potential in this area, competition among the three industry giants, Cainiao Network, JD Logistics, and SF Express, has escalated to a new level.

Cainiao Network has decided to become the 'brain' of logistics through intelligent logistics hubs. On June 6, in partnership with Air China and YTO Express, it announced that they would build a world-class logistics hub at the Hong Kong International Airport in order to support a global logistics network that guarantees arrival within 72 hours at the latest. The combined investment by the three companies is around HK$12 billion, with Cainiao contributing 51% of the investment, Air China 35%, and YTO 14%. The Smart Logistics Network designed by Cainiao Network is comprised of two parts: one is to create a domestic logistics network that guarantees a maximum arrival time of 24 hours while the other is to create a global logistics network that guarantees a latest arrival within 72 hours. Cainiao has made it clear that its mission is not to become a courier company but to support courier companies in their pursuit of improving efficiency through Cainiao's `intelligent’ logistics network.

JD Logistics has decided to go public in five years, generating revenues of over RMB 100 billion with orders outside the JD system accounting for more than half. To achieve this five-year goal, JD Logistics needs to build more connections externally and develop innovative technologies internally. At the beginning of 2018, JD Logistics completed a capital increase agreement and has raised $2.5 billion since. The capital will go to the further development of its smart supply chain, the exploration and application of advanced technologies, talent acquisition and training as well as logistics value-added services.

SF Express has been involved in multiple industries to expand its industrial chain. According to SF Express's financial report in 2017, the new business of SF includes supply chain management services (under development), heavy cargo business, cold chain transportation service, international express service, and same city express service.

The different development paths of the three logistics giants will determine the future shape of China's logistics industry. But the challenges facing the three companies vary. For Cainiao Network, the main challenge is how to work with other logistics companies for better coordination and increased efficiency. JD Logistics needs to control costs under the direct operating model. In comparison, the environment that SF Express finds itself in is much more complex. There is not only intense competition within the express delivery industry but also cross-border competition in the e-commerce logistics market. Therefore, SF needs to be more ecologically oriented throughout its industrial chain and strengthen investment in new elements such as data and technology upgrade.

Whoever comes out ahead in the end, what is certain is that China's logistics industry will be rapidly improved in the process and will become even more competitive.