Perspectives

The Deloitte Research Monthly Outlook and Perspectives

Issue XL

22 August 2018

Economy

Fiscal stimulus - Déjà vu all over again

The latest tariff salvos between China and the US don’t seem to have manifested themselves in the data on trade yet. In fact, recent trade data show that both Chinese exports and imports rose by 12.2% and 27.3% respectively in July 2018. But a surge in the import of vehicles in July (up 72% YoY) suggests that the business community anticipates high tariffs and a weaker RMB in the near future (depreciated by almost 8% against the dollar this year from its high point).

In order to offset potential external shocks, policymakers have mostly made up their minds to resort to counter-cyclical fiscal policies but with the caveat of doing it in such a way as to avoid creating the same side effects as in the controversial "4trn RMB" stimulus package rolled out in late 2008. In official media, policy makers have pledged not to engage in an all-out fiscal expansion as in 2008-2010, when firms were flooded with loans they did not even want.

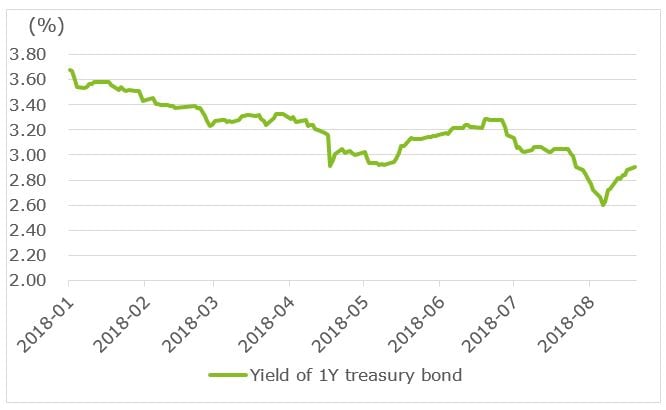

But before we address the question of what concrete measures would work best to protect the economy from such "flood irrigation", we need first to look at the root cause of weakness in the economy. If the Chinese economy indeed suffers from inadequate demand, then there is no doubt that such a fiscal expansion would be warranted - especially when borrowing costs are relatively low (China 10-year bond yield at 3.5%). However, if deleveraging remains a top priority in the medium or even long term, any large fiscal outlays ought to be strictly temporary and target consumption. This is because, if the growth rate comes down to 4% (a scenario not inconceivable in the medium term), pump priming can well hit a binding budget constraint against the backdrop of rising global interest rates. In reality, given that both the housing and auto sectors (in which restrictive policies were introduced a few years ago) remain buoyant, it is clear that demand has not been met. So wouldn't it be more logical to slowly ease such restrictions before turning on the fiscal tap?

The implicit logic behind the preference for strong fiscal policy over consumption is that policymakers would like to kill two birds with one stone, reflating the economy immediately and stabilizing housing prices at the same time. Perhaps it would work - if it weren’t for the desire to invest in infrastructure that manifests itself whenever the fiscal taps are turned on. This is because, first of all, infrastructure investment is easier to execute. Second, unlike banks in the West who are less willing to play ball, Chinese banks are often asked to and do support the real economy. Third, the preference for infrastructure projects alludes to a seemingly perennial argument that their social benefits beyond financial returns ought to be measured (e.g., high-speed rail). So, if infrastructure investment is going to be a part of the fiscal stimulus, it should be made in a more prudent and focused manner. In our view, at least two conditions must be met: 1) only a moderate amount is to be earmarked; 2) budget constraints faced by local governments should be gradually hardened. The ongoing debate between the PBOC and Ministry of Finance over the role of fiscal levers boils down to this fundamental question —- to what extent will the former end up paying for domestic debt? If the PBOC wants to maintain a relatively stable RMB exchange rate (say, capping USD/CNY around 7.0 this year), credit growth needs to be kept roughly in line with nominal GDP growth. But again, if President Trump follows through on his threat to increase tariffs (which seems likely as long as the US equity market holds up), the RMB could face downward pressure. Meanwhile, an external environment characterized by a cyclical global recovery and continued tightening by central banks is, and will be, increasingly hostile to economies that fail to rein in credit booms. Türkiye is a case in point, for the Lira has hit one low because of capital flight. Türkiye's crisis unfolds as business morale ebbs, demonstrating that investors can be easily spooked when the country's current account deficit gets out of control. The threshold of current account deficit in relation to GDP is 6%, judged by previous emerging market crises (e.g., the Asian Financial Crisis in 1997). The point made by Paul Krugman in his article (Partying like it's 1998, August 11, 2018, New York Times) on Türkiye's crisis is that large short-term credit denominated in foreign currencies can be the catalyst for a big financial crisis when market sentiment worsens.

Chart: Spooked by potential inflation shock

It is perhaps far-fetched to draw comparisons between Türkiye today, Asia yesterday (in 1997), and China. But, nevertheless, the lessons to be drawn from both are similar. China needs to avoid too high an economic growth target and a strong RMB exchange rate when the external environment is not so favorable. And finally, on fiscal expansion, we think the government will be able to avoid a "flood irrigation" type of fiscal stimulus but long-awaited tax cuts may fall short of expectations. In conclusion, if tax cuts are not the center-piece of the fiscal stimulus, we hope the bulk of spending will be in education and healthcare.

Retail

The arrival of "Fast Retail"

In the consumer-centric retail market, competition over consumers by major market players is transforming the sector. The most recent development is the integration of food delivery and online retail systems. Two of the main food delivery platforms in China have launched new schemes that aim to meet consumer’s needs more quickly and directly. In July, Meituan launched its “flash purchase” service which focused on the delivery of retail goods to consumers in the same amount of time it takes for food to be delivered to the home. Recently acquired by Alibaba, Eleme, another major food delivery service, is also fast integrating into the Ali retail ecosystem. The merging of food delivery and retail services will change the manner of interaction between consumers and retailers.

The escalation of competition

The food delivery market has been enjoying rapid growth as this service offers consumers a wide array of food choices with a minimum of effort. According to iResearch, a market research firm, between 2017 and 2023 the food delivery market is expected to grow at a compound annual rate of 31%. It is worth noting that this 31% compound annual growth rate expectation is based upon the projection that the amount of delivery transactions in 2023 will be five times that of 2017. Such is the core driving force of online food consumption. The popularity of the internet, coupled with the convenience and the cost-effectiveness of online food purchasing, has changed consumer behaviour to the extent that today people are much less likely to cook at home or purchase pre-made food at shops than simply `ordering out’. In China, in the gradually maturing food delivery market, the two major market players, MeiTuan and Eleme, have amassed strong operational capabilities and service resources. In order to expand their consumer base and increase the size of the market, the extension of service capabilities to other kinds of goods becomes inevitable.

Hence, in July this year MeiTuan launched its online “flash purchase” service which promises a 30-minute delivery of certain retail goods backed by a 24-hour multi-category online store. The service is a pioneer in the upcoming “fast retail” market. After being acquired by and incorporated into the Ali group, Eleme, the other major player in the food delivery sector, is poised to expand its delivery categories to such items as fresh fruits and vegetables, flowers and daily-use products to increase revenue and reduce transportation costs through economies of scale. Thus these two companies have expanded the market by creating a new kind of service – the retail instant delivery service. Consequently, competition between these two players will heat up, but in an expanded market.

In terms of technology innovation, both companies continue to experiment on unmanned delivery service to improve efficiency and reduce costs, moving a step closer toward “future logistics”. What is even more noteworthy is that after its Eleme acquisition, Alibaba clinched a partnership with Starbucks. Alibaba has also incorporated `Eleme’ delivery channels into Taobao, and has taken measures to encourage users to link the two accounts. For example, after linking their Taobao and Eleme accounts, non-member users of Eleme are eligible to purchase prime memberships at 0.01 yuan and enjoy 15 free deliveries. Alibaba intends to integrate resources even more deeply in the near future by opening up the membership and marketing systems.

The rapid growth of the food delivery industry makes it easier for the two platforms to break into the retail market. For Alibaba, full access to Eleme will ramp up its capacity to meet the last-mile demands of its consumers. For MeiTuan, its “MeiTuan app”, “Dianping app” and “MeiTuan food delivery app” form a powerful service matrix, in addition to the support from “Wechat” that has 900 million daily active users and QQ that has 500 million daily active users. The new business of retail goods delivery also reflects its expansion ambitions into the retail market.

Implications for retail industry

The essence of retail is to meet the demands of consumers. Express retail goods delivery will bring about a transformation in the relationship between consumers, commodities and retailers. Because consumers can get products more conveniently and quickly by using a delivery platform, the interaction between retailers and consumers will rapidly shift from physical stores to online platforms. This will result in the following changes to the retail industry.

- Consumer experience will be reshaped. The way in which consumers buy products will change as more and more transactions will be conducted online instead of in physical stores. Consequently, instead of consumers going to the place where the goods are, the goods will come to the consumer – either at home or at the office -in about half an hour. Shopping will be faster, easier and more convenient.

- Transaction medium will change. Due to the involvement of third-party distribution platforms, the ways consumers interact with retailers may also change. Platforms may become the integrators of resources, responsible for matching supply with demand. For retailers, consumers will no longer be limited only to physical stores and online access will play an increasingly important role. Traditional retailers face a major dilemma and need to decide whether to cooperate with a platform and better leverage the resources the platform offers or to take control of their own portals and the consumers they serve.

- Industry landscape will change. For internet giants like Alibaba, breaking into the retail market with express delivery capabilities can be viewed as another way to penetrate the offline market. While Alibaba is quickly improving offline penetration through capital operations, its service matrix, such as payment and delivery, is also powerful to accomplish the same goal. Other industry players such as Meituan, Dianping, Tencent and Jingdong Group also share similar development logic which is to occupy more of consumers’ time through a more comprehensive and broader service coverage. Under the tutelage of the internet, the landscape of the retail industry will experience more profound changes.

Logistics

A new direction for high-speed rail freight

The explosive growth in e-commerce has led to a concomitant growth in the express delivery industry. This has resulted in a gradual change and reassessment of the business models of related industries such as aviation and railways.

Express delivery companies are actively deploying in the air cargo field

Air freight is an important part of the modern logistics business as it is safe, convenient and fast. As a result, it has become the preferred mode of transport for valuable or fragile commodities such as fresh produce or precision instruments. Judging from the development trajectory of international logistics giants, aviation logistics is going to be the next major area of investment for Chinese logistics companies. Recently, a number of express delivery companies have announced plans to invest heavily in the aviation logistics market.

In April 2018, SF Express, the pioneer of Chinese air transportation, opened a number of international cargo routes and invested in international shipping logistics service platforms. On June 11th, ZTO Express also announced a joint venture with Turkish Airlines and Pacific Airlines to provide package collection, freight forwarding, express transportation and “last-mile” distribution services for global customers while on July 30, YTO Express (Logistics) signed a strategic investment agreement with the Jiaxing Municipal Government, investing RMB 12.2 billion to build a global aviation logistics hub at Jiaxing Airport and plans to create a shared intermodal trade distribution center that covers the globe. However, since China's logistics industry has just started to move into the air cargo business, Chinese express delivery companies have a long way to go before they can adequately compete with international logistics giants.

Railway freight transport actively explores new paths for development

With the speedy construction of China's railway network, a rapid growth of freight volumes is expected in the next three years. The railway cold chain in particular has a high growth potential. In July, China's first cold chain train began operation in the Yangtze River Delta region and Sichuan province. The train mainly carried imported frozen meat shipped into Chinese ports via ocean liners into the hinterland. This opened the railway transportation route for frozen and fresh goods.

On July 18th, Jingdong Logistics and China Railway Express jointly announced the official launch of the “High-speed Rail Transportation Freshness” project which aims to tap into the high-speed rail capability to provide better, more efficient and stable support for delivery of fresh goods. Currently, the railway department has signed agreements with a number of enterprises to jointly develop the railway cold chain logistics transportation network.

The impact of the US-China trade spat on China's logistics industry.

Overall, China's logistics industry has a bright future, but the recent US-China trade conflict has and will affect the cross-border logistics industry in the following ways:

- Tariffs will have a negative impact on bulk trade and will therefore affect container shipping logistics. In the short run, transhipment trade to the US could increase as companies try to avoid high tariffs.

- China's cross-border logistics business through the overseas warehouse model could also be affected. Chinese overseas warehouses will face more stringent inspections and they need to exercise more caution with bulk stocking.

- As trade sanctions against China specifically mentioned intellectual property issues, it is very probable that the US Customs will enhance inspection of cargos and come down harshly on any infringement of rules. As a result, customs clearance of goods could become slower and more burdensome. Tariff and trade protection measures will most definitely affect the competitiveness of Chinese logistics companies in the US.