Perspectives

The Deloitte Research Monthly Outlook and Perspectives

Issue XLI

25 September 2018

Economy

Stand foursquare behind the domestic reform agenda

How to quantify the impact of a trade war is the `$64,000 question’ today. One such attempt was made by the former PBOC Governor, who claims to have “used a mathematical model to calculate the negative impact of the trade war”. He concluded that the negative effect of a trade war on the economy is “not very large, and not significant…. less than half a percent." This statement was made on September 7, and to us it appears somewhat optimistic (Zhou's later comments in Switzerland recalibrated that higher tariffs could result in 0.8% of reduction in GDP growth).

We have long held the view that the adverse effects on the Chinese economy, because it is so heavily export-dependent and entrenched in global supply chains, lie mainly in three areas: 1) inflation, 2) investor sentiment, and 3) disruption of supply chains. Despite Beijing's measured reaction to higher tariffs imposed by the Trump Administration (who plans to announce within days new 10% tariffs on $200 billion worth of Chinese goods), the inflationary impact of tariffs is already visible in China, particularly as it has come on top of the rise in oil prices caused by the turmoil in the Middle East and President Trump’s sanctions against Iran. Anecdotal evidence suggests that 2018 has seen significant increases in rents and furnishings, prices at restaurants, and manual labor in major cities. A further escalation of trade tensions between China and the US is bound to create fresh inflationary pressure on China. This will, in turn, hurt investor sentiment, already shaky amidst economic deceleration and regulatory tightening (investors' subdued sentiment also helps explain under-performance this year of both equities and bonds of China.) The impact on supply chains is almost impossible to quantify but one can get a sense of how these get disrupted if one understands the mechanisms of decision making in global companies. In these enterprises, major decisions on strategic investment have to be made with a time horizon of at least 10 years. Therefore, the lack of a clearly foreseeable end to the US-China trade war is deterring private investment and making investors risk-averse.

In light of the Trump Administration's threat to impose an additional $200bn worth of tariffs, will the next round of trade talks initiated by the US yield any concrete results? The short answer is: very unlikely. But to understand why we need to look at some of the underlying assumptions VI’s-a-vis China that are being brought to the table.

Assumption 1: China must be seen as being serious about addressing the question of trade imbalance.

It is unrealistic for the Trump Administration to expect any meaningful bilateral trade surplus reductions in the short run for the following reasons: a strong US economy coupled with the strength of the greenback will very probably widen bilateral trade imbalances unless China undertakes voluntary export restraint (VER) as Japan did in the mid-80s with the US. To get around the VER, the Japanese automobile industry established assembly plants or "transplants" in the US to make up for the reduction in quotas. But this route is not open to Chinese companies today as the US Government is determined to make it difficult for Chinese companies to invest in the U.S. economy.

Assumption 2: China could use the exchange rate as a monetary tool

It is hard to fault China if the RMB exchange rate is used as a necessary monetary tool when major central banks are shrinking their balance sheets. China's monetary policy is likely to be somewhat accommodating with credit growing at the rate of 8-10% (YoY) but if this changes, monetary tools will have to be used as regulators have been left with little leeway.

Assumption 3: China can and should open up the domestic market further to foreign investors

It is unrealistic for China to open up the domestic market in a Big-Bang manner. In fact, China's proven success of economic reforms over the past 40 years has been built on gradualism. If history is any guide, for any country, a drastic restructuring of the domestic economy can only take place after a major crisis.

Hence it comes down to one question: if the US believes these assumptions to be true, could Beijing and Washington still find ways to avoid an escalation of trade tensions?

We are of the view that an all out trade war will result in a situation where everyone loses out. For the US, despite a roaring economy and a strong stock market, higher tariffs will eventually undo the positive effects of tax cuts. In the short run, consumers will bear the cost because it takes time for firms to adjust their supply chains and even if the firms could do so, such revised supply chains will be less than optimal. Again, it means higher prices in both countries. If both parties have to compromise, China should let it be seen that it is the one making the larger concessions. But such concessions should be appraised on the ground that improved market access or progress made in intellectual property right protection must be in line with China's domestic reform agenda. Having chosen gradualism over the Big-Bang approach at the time of its accession to the WTO in 2001, China now has to do several small but important things simultaneously to defuse the accusation of protectionism. For example, it could perhaps broaden its Made in China 2025 in such a way that MNCs including US companies could participate in the program which is aimed at upgrading China's manufacturing anyway. This would be a solid rebuttal to the assertion that Made in China 2025 would cause enormous distortions in emerging industries through government subsidies. China could also provide MNCs' China businesses with access to China's large pool of savings as a means to encourage stronger commitment to the economy. The "international board" scheme which would allow MNC’s China businesses to be listed on the A share market was floated some years ago but has unfortunately fizzled out. The policy intention back then was to attract better quality companies to the domestic stock market. Today the scheme would kill two birds with one stone, improving the quality of the domestic stock market on the one hand and at the same time allowing MNCs to lobby on China's behalf. And ultimately, their increasing investment in the domestic market enabled by improved market access for private business and foreigners would make lobbying itself unnecessary.

And finally, on China's inflation, which is on the rise but remains under control compared to most emerging markets, the PBOC can afford not to hike interest rates despite a hawkish Fed. This means China does not face an acute trade-off as many emerging economies do between currency plunges and unemployment spikes. However, it would be important to avoid any policy initiatives that could hurt private investment. From this standpoint, the policy of having firms pay social security contributions "in arrears", may well cause dislocation in the labor market because some SMEs would have to lay off workers in order to meet their obligations. In this, some lessons can be drawn from the past. At the height of the Asian Financial Crisis, the HKSAR Government rolled out a Mandatory Provident Fund (MPF), a forced retirement saving scheme. Most employees and their employers are required to contribute monthly to MPF schemes provided by approved private organizations based upon their wages and the length of their employment. Such a scheme, though helpful in the long run as it also addressed the challenges of population ageing, didn’t really tally with HKSAR’s economic recovery. In fact, MPF's introduction in the late 1990s probably worsened the unemployment situation since many SMEs then could not afford to hire new employees. It is important that such mistakes not be repeated.

Chart: Tax and social security contributions/corporate profits (global top 10)

In conclusion, what China could do to end the tariff stand-off is as follows. It could 1) allow President Trump to claim some headline wins (as Mexico has done in its recent trade agreement with the US), 2) make concrete progress in terms of better market access for foreign enterprises and 3) provide relief measures for domestic firms on lower costs as an incentive for future investment.

Financial Services

Crisis and Rebirth in P2P industry

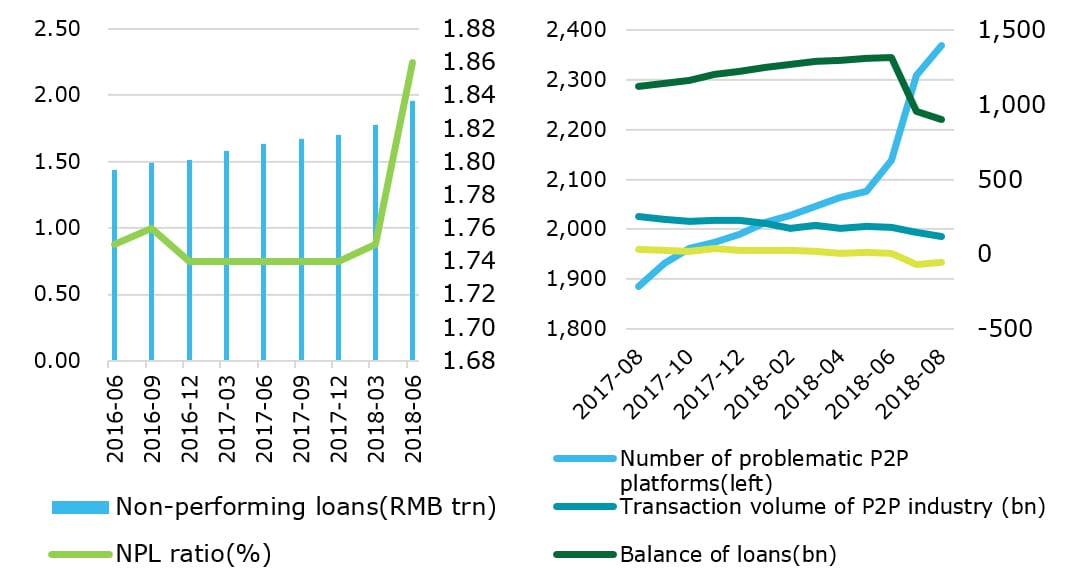

Over the recent months the P2P (peer-to-peer) online lending industry has experienced an increasing array of challenges and issues ranging from default to outright fraud, all of which have garnered a great deal of negative publicity. Wang Dai Zhi Jia (WDZJ), China's leading online lending news and information portal, reported that to date there have seen something in the order of 2,369 `problem’ P2P platforms (with difficulties such as withdrawal, executive disappearances and deferred payments), and only 1,589 platforms were still considered to be operating in a 'normal' mode by the end of August. Investor confidence has plummeted and with recorded loan balances at RMB 903.29 billion, they are 31.4% lower than the June 2018 peak. Moreover, the net inflow of funds continued to be negative in July and August.

Such a precipitous decline in investment has got the regulators worried and they have recently introduced a series of new policies aimed at steering the industry towards greater compliance and standardization in their operations. As a result, the problem platforms are gradually either getting `cleaned up’ or `cleared out’ of the system, and the whole P2P industry is undergoing a process of adjustment and transformation. But, in the short term, as investor confidence has been seriously dented, a wait-and-see mood is now prevalent. It will take some time for the industry to return to health.

Wave of defaults have burst the bubble

P2P lending platforms are ideally placed to provide investment and lending opportunities through focusing on micro enterprises and individuals whose borrowing needs cannot be properly met by traditional commercial banks. So, in essence, P2P is an intermediary among related parties. China's first online lending platform was founded in 2006 and thereafter the industry grew like wildfire. Some companies have become well established, trusted and highly successful. Yirendai and PPDai, for example, are two such lending platforms that started at that time and are still in normal operation today. Others have not been so fortunate.

Without wanting to over-simplify the explanation, it could be said that the recent problems are mainly attributable to two factors, one internal and one external to the P2P ecosystem. First, the threshold for entrance into the P2P ecosystem has been very low due to the initial absence of a rigid and comprehensive compliance regimen. To start a platform only registration or filing for record purposes is required in place of any regulatory licensing or approval. This led to a chaotic environment where there existed a plethora of platforms, some of which engaged in boiler-room operations under the disguise of "FinTech" firms, whilst others more blatantly and openly defrauded investors with some even running age old "Ponzi" type schemes. As a result, over the past few years, the P2P industry has accumulated an increasing level of moral hazard and credit risk. Secondly, external factors such as the economic downturn, financial risk prevention, corporate default and tightening in the credit cycle have all contributed to accelerate the concentration of risk exposures and eventually triggering the crisis. As new regulations are being implemented, China's asset management industry is undergoing a complete transformation and the P2P sector is just one piece of the larger puzzle. The non-performing loan (NPL) ratio at commercial banks in Q1, after staying constant for 5 consecutive quarters, rose to 1.75%, and quickly climbed to 1.86% in Q2. This was seen even more extremely in the P2P sector and consequently, overdue loans and defaults have increased and payment pressures have resulted in cracks in the funding chain which finally created major problems such as difficulties in meeting increased withdrawal demand, the disappearance of some very high profile executives and an increasing deferral of payment obligations.

To add further to the industry's woes, when the original deadline for regulatory filings under the new regime of June 30 2018 was extended, a barrage of negative media coverage, widespread panic struck and investor confidence crashed. In August, the P2P industry had something in the order of 2.61 million investors, with 3.02 million borrowers, representing a massive decrease of 42.6% and 42.1% respectively from the peak months of 2017.

Chart 1: The first rise of Banks' NPL ratio since end of 2016 |

Chart 2: A spate of P2P platform breakdown |

Financial Literacy is critical

As a general principle one should expect that achieving high returns would ordinarily equate to taking a higher level of risk. Through the recently amended asset management regulations, financial products that guarantee the return of investment capital and income can no longer be offered. Moreover, in the current environment of weaker bond and stock markets, high-yield investment and financial opportunities should be relatively rare. Investors should continue to be educated such that they have the ability to detect ecosystems, platforms and other investment opportunities that have a higher potential for financial fraud and abuse through the use of a myriad variants of Ponzi schemes. To this end, Mr. Guo Shuqing, Chairman of China Banking and Insurance Regulatory Commission (CBIRC), has, on several occasions, publicly reminded investors to pay special attention to financial products and investment companies touting high returns – devising a simple rule of thumb for advising investors - regard any product yielding 8% or more as dangerous and to be prepared to lose all of their principal if the yield is touted at 10% or more. Currently, the rise of P2P debt transfer cases (transferring claims to secure cash) has resulted in a rise in yield (annualized yield stands at 10.02%). Investors, however, should be cognizant of the qualifications of the platforms and have strong risk identification capability.

Regulation to promote P2P compliance capability

A new round of nationwide online lending supervision has begun. In August, authorities of both the national online lending risk management group and the National Internet Finance Association respectively released self-examination question lists for P2P lenders which must be completed by the end of 2018. Areas of self-examination include analyzing the very nature of P2P lending - is it illegal financing in disguise, full disclosure of risks, compliance with the principle of small amount lending and lending dispersion. But ultimately the government can only give guidelines. It is up to P2P platforms to strengthen self-discipline, enhance their own risk control ability, improve information disclosure, make public the list of dishonest people with bad credit and promote the construction of a credit database for P2P lending.

Digital inclusive finance is the future

Online lending is the natural demand of a diversified financial system. Globally, P2P platforms have been actively absorbing capital for development, such as Xiaomi's investment in ZestMoney in India and UK's Funding Circle who recently announced their IPO plan.

As a direct financing channel in China, P2P lending has in part satisfied the demand of individual consumption, micro enterprises and even farmer's operational loans, and to a certain extent, enriched the choice of public wealth management tools. For these reasons, it could be said that the ecosystem's development prospects are sound. After the implementation of guidelines and with some industry self-discipline, P2P lending platforms should increasingly become an important part of the digital inclusive finance as an effective complement to traditional banks' indirect financing.

Today the Chinese P2P industry is experiencing a very painful and public adjustment period. As this period draws to an end and is combined with the establishment of rules and regulations aimed at stabilizing the ecosystem and its participants - it should be increasingly possible to identify and subsequently weed out the problem platforms. Eventually, the combination of P2P platforms with demonstrable and comprehensive risk and compliance capabilities and increasingly qualified investors with risk differentiating capabilities will jointly drive the industry towards maturity and longer term success.

Energy

LNG tariff casts a long shadow

Trade tensions between China and the U.S. continue to escalate as China announced a 25% import tariff on a further USD60 billion worth of US goods including LNG in August in response to Trump administration's announcement of proposed tariffs on an additional USD 200 billion of Chinese imports.

Paradoxically, LNG has been high on the agenda of both countries since the first meeting between presidents Xi Jinping and Donald Trump last year. In 2017, driven by its robust domestic demand and stagnant domestic production, China became the world’s second largest LNG importer. The U.S., for its part, plans to become the 3rd largest LNG exporter by 2020 by bringing on line new LNG capacity and increasing exports by 50% in the next five years. The imposition of tariffs on LNG will weigh on both countries.

A tightening global LNG market

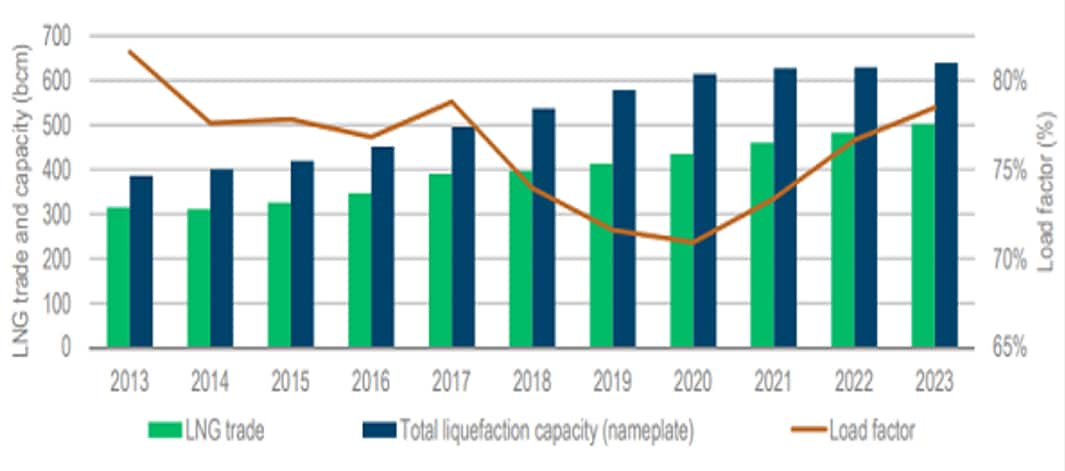

Global LNG imports increased by 10% in 2017, the highest growth since 2010. This was mainly driven by rising Asian demand. China imported 24 million tons of LNG in the first half of 2018, up over 50% from a year ago and there are clear signs that demand will only continue to grow in the coming years. However, according to OECD/IEA, a lack of projects post-2020 could lead to a market tightening beginning in 2021. For, while nearly all the new liquefaction capacity should be in operation by 2020, without new investment, the average utilisation rate of liquefaction is likely to return to its pre-2017 level by 2023. Due to the long lead time of such projects, investment decisions need to be made in the next few years to ensure adequate supply of LNG.

Figure 1: LNG liquefaction capacity and utilisation, 2013-23

Competing for LNG supply

Although U.S. LNG exports to China represent only 5% of China's total LNG imports, in terms of volume they represent a 200-fold increase from what they were two years ago. But the U.S. LNG price advantage over Australian gas will be chipped away by the recent 25% tariff on top of the original 10% VAT. Higher tariffs will drive up the cost of China's gasification program, increasing the risk of gas shortage especially in winter when the demand for gas hits its peak. Given this, China will be forced to find other suppliers and compete with other Asian countries for LNG supplies.

Will China be able to easily secure a new supplier of LNG? Perhaps, but it is not going to be easy, especially in the face of a likely global LNG shortfall in 2021. On the supply side, China’s major sources of LNG are Australia, followed by Qatar, Malaysia, Indonesia, New Guinea and the US. However, most of these countries are facing internal problems which could hamper exports to China. Australia is suffering from a domestic gas shortage and surging prices, forcing it to consider importing the fuel. ExxonMobil, Australia’s top gas supplier, said it plans to import some super-cooled fuel to help offset an anticipated gas shortage from 2021 onwards as well as in order to protect its market share. Qatar lifted its moratorium on prospecting in the North Field in 2017 but it takes time to ramp up production and export capacity. Indonesia is expecting a robust internal consumption to reach its 100% electrification goal. On the demand side, both Japan and South Korea, the number one and the 3rd largest LNG importer respectively, are faced with domestic power shortages. As a result, China may find itself in competition for Asia-bound LNG cargoes if supply and demand problems worsen.

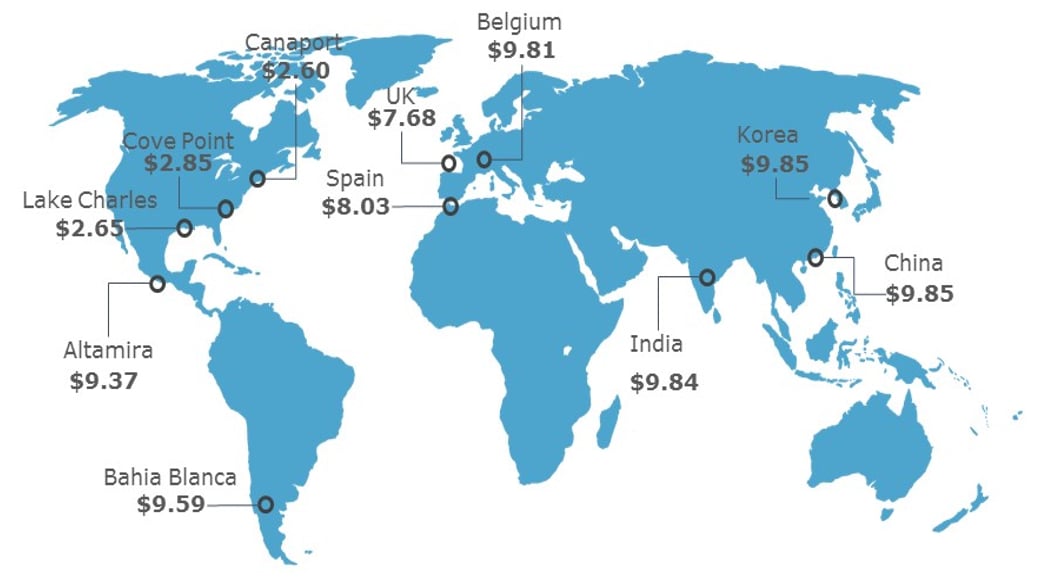

Figure 2: World LNG estimated CIF prices, July 2018

Missing out on the demand boom

For the U.S., perhaps the most significant impact of the tariff war with China will be the increased risk of LNG project delays. China is considered a promising buyer bringing in long-term contracts, which is the foundation of financing for export terminal projects. In February, Texas-based Cheniere Energy signed two long-term contracts to supply LNG to CNPC over the next 25 years. They were the first such deals for a US LNG company with China, and the agreements were directly or indirectly responsible for financiers finally committing to invest in Cheniere’s Corpus Christi LNG export facility. Similar long-term contracts are required for several LNG terminal projects that have received approval from the federal government but await a final investment decision from investors. Export terminal project delays may cause the U.S. to fall behind its competitors and miss out on the global demand boom in a tightening market.

The imposition of tariffs would significantly affect both China and the US. While China must assume the risks of exposure to gas shortage and competition for Asian LNG supply, the US faces having to make decisions to expand export capacity or not in the near future. The perspective of losing the China market because of tariffs, however, could possibly hold investors back. A trade war is always a double-edged sword, and neither party gets off without bleeding. The energy trade between the U.S. and China will certainly be no exception.

Automotive

Auto leasing: the silver lining in China’s waning car market

China’s auto market has a speed bump yet again as sales of passenger cars slipped for the second straight month in August, extending the weakness which might persist in the rest of 2018. There are multiple forces at play. First and foremost is the concern of a spiralling slowdown in China’s economy. The second major problem is that given the volatile external environment, consumers tend to spend less.

As depressed as the auto market may have become, auto financing, on the other hand, is flourishing as more and more consumers are financing their car purchases instead of paying outright with cash. Research has shown that financing (including auto financing, bank loans, leasing) accounted for more than 40 percent of new car purchases at some car dealerships in the first half of 2018. Although there is no detailed breakdown of data, car leasing on its own made up for more than 10% of new car purchases last year, and has at least three times the penetration rate of 2014.

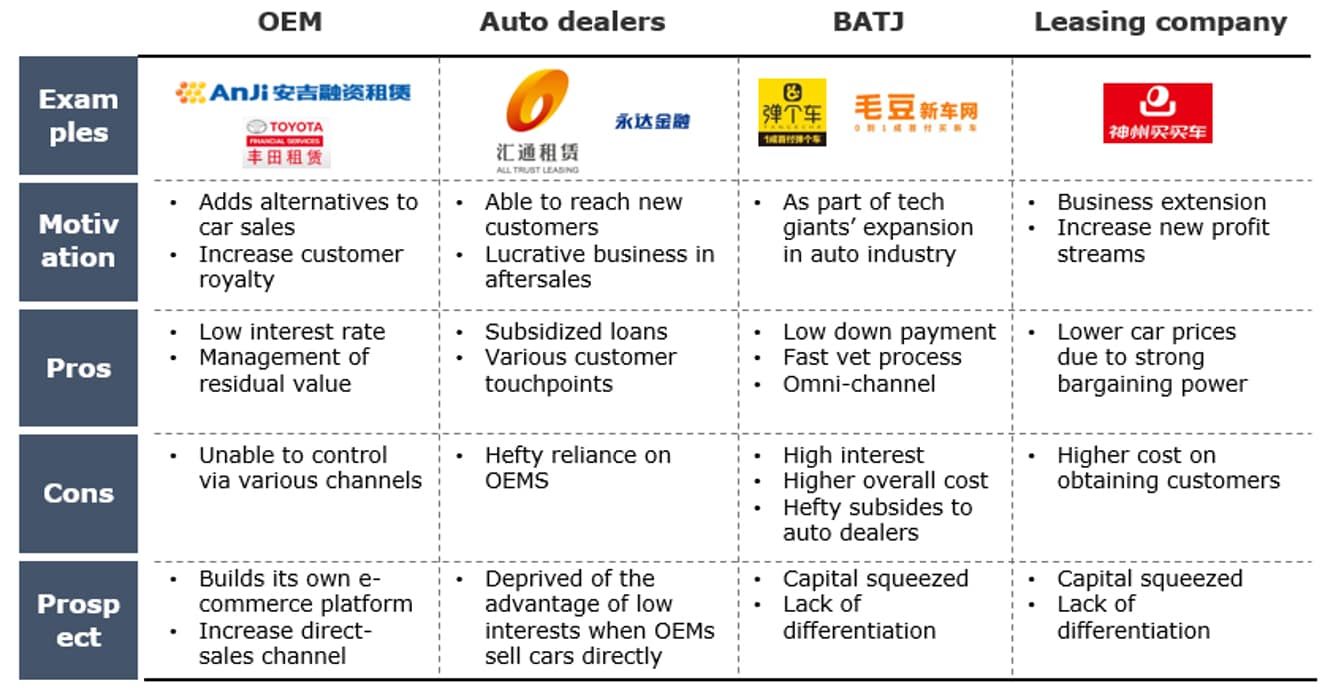

Chart: Comparison of different car leasing platforms

In contrast to car loans that normally require at least 50 percent of initial payment and have a rigid list of loan qualification requirements, car leasing offers minimal down payment and reasonable monthly payments. But it wasn’t until 2017 that the car leasing business really started to take off in China. There are three main reasons for this.

First, tech giants (BATJ) have become more interested than ever in backing auto sales-related start-ups. These newly founded companies allow consumers to drive away with their new car after a minimal down payment and a one-year leasing contract. After the contract expires, buyers can either return the car to the dealership or purchase the car at the residual value established by the company at the beginning of the lease. The BATJ entry has shaken up a market that used to be dominated by OEMs and AFCs (auto financing companies).

Secondly, these new online leasing platforms have been widely hailed as pioneers in reinventing the auto retail model by offering a seamless online and offline customer experience. Although these start-ups initially only identified and acquired customers who demonstrated willingness to buy and then sold these sales leads to dealerships, they opened up their own physical stores after a few months. Compared with 4S stores that normally take up acres of floor space and cost tens of millions of RMB of initial investment, the online leasing platform’s stores typically costs no more than a million RMB to set up and operates more like a centre for test drives and deliveries, saving customers the trouble of driving to 4S stores and haggling with salespersons. This new way of car selling has helped increase sales efficiency.

Lastly, these leasing platforms have managed to zero in on young consumers in the lower-tier cities and counties who are believed to have the biggest purchasing power potential in the near future. In addition, consumer loans have expanded rapidly in recent years as the younger generation is growing more willing to finance their purchases, irrespective of the high interest rates.

But capital and regulation remain the biggest obstacles to future growth for the new leasing firms. The largest expense is vehicle procurement fees as they have to pay for the cars themselves before leasing them to consumers. In addition, they have spent heavily on marketing and promotion to increase public awareness and to collaborate with dealers. As their sources of income are limited, revenue from the sale of asset backed securities and rental income make up the largest revenue stream. Prospects for future growth have become a little more murky recently as a change in regulation could subject the relentlessly-expanding leasing platforms to tighter scrutiny.

Life Science & Healthcare

A new phase of AI-assisted diagnosis

The Medical Device Classification Catalogue of China went into effect on August 1. The most important part of this new version of the catalogue is that the definition of Artificial Intelligence-assisted diagnosis software was added, which implies that this market segment is going to enter a new phase.

Investment is hot but still quite preliminary

From 2015 to 2017, the volume of investment coming to medical AI has significantly increased and focus of that investment has shifted from the systemic level to the applications level. Many medical AI startups have emerged since 2016, most of which focus on AI-assisted diagnosis of cancer, neurological diseases, ophthalmic diseases and vascular diseases. These have drawn the attention of institutional investors, especially since 2017, and money has been pumped into them.

Figure: Trends of investment toward medical AI

However, an effective profit model remains difficult to find in this sector, and competition is fierce as tech giants such as BAT, Iflytek, Wining Health and Fosun Group are also entering the space. Today, only a very few AI-assisted diagnosis startups will be able to make it to the `B’ and `C’ rounds of financing, most of the others remaining at the Angel or `A round’. Moreover, investors have become very cautious on follow-on investment.

Getting licensed is the basis of commercialization

The implementation of this new catalogue will be a significant milestone in this sector as it will enable start ups to apply for licenses. These licenses will help them get investors. However, obtaining a license is not easy. Licenses for new technologies are normally issued on a very limited basis at the beginning, especially in the healthcare sector. Products that can secure the license early will be able to have the first-mover advantage in the market. It will also enable them to explore different billing models in hospitals and develop a long-term profit model.

On the other hand, if a product fails to progress in securing a license, it will disappoint investors and lose chances of growing. Predictably, many startups in this sector will go broke in the near future.

"Data" might will be the key to win

The obtaining of licenses is complicated by the fact that it is really difficult for companies to differentiate themselves from their competition in this sector because the deep learning algorithms of the different AI assisted products are very similar or the same. Hence, though the review methodology of CFDA on AI-assisted diagnosis products is still not clear, it will certainly take into account data quantity and quality.

Currently, although deep learning algorithms of different AI-assisted diagnosis products are similar but the data they use to learn from varies. Since accessibility to healthcare data is always relatively low in China, players should build data sharing relationships with health institutions and third-party imaging centers as early as possible to secure sufficient high quality data to develop their product advantages, which will, in turn, help them accelerate the licensing process.