Perspectives

The Deloitte Research Monthly Outlook and Perspectives

Issue XLIII

29 November 2018

Economy

G20 summit: the stakes are high

Will there be a deal at the November G20 meeting between President Xi and President Trump? If so, financial markets in both mainland China and Hong Kong will be granted a respite, and downward pressures on the RMB exchange rate will probably ease off for a while. If not, it is almost certain that the promised 25% tariff will be imposed on $200 billion worth of Chinese exports starting January 2019.

In the medium term, the stakes of the upcoming G-20 summit are high for China as Trump has hinted at more tariffs should trade talks be stalled. The outcome of the US midterm elections, in our view, is unlikely to affect the ongoing trade talks (the US Treasury Secretary Steven Mnuchin has just resumed discussions with the Chinese Vice Premier Liu He) because both Democrats and Republicans do not have major differences on the current US policy toward China. We have been of the view that concessions by China in the form of improved market access and progress in IPR protection are in line with China's reform agenda (in the long run). The real issue lies in the pace of reform where the views of Washington and Beijing diverged vastly. However, if Beijing could accelerate the liberalization process in financial services and key sectors such as the automobile industry, there is a strong likelihood that Trump may not impose the entire 25% tariff as declared. Vice President Wang Qishan's statement in Singapore last week that both sides would address "shared concerns" is a positive sign. In essence, if 25% tariffs on $200 billion worth of Chinese exports are only implemented partially, then we could perhaps view this round of trade talks as being closer to a "skirmish" or even a temporary truce rather than outright war. For China, a mild RMB depreciation and some export tax rebates could well be used to offset any loss of competitiveness.

On the economic front, signs of deceleration are evident. October auto sales data reveal a -11.7% YoY drop and industrial production growth has also slowed (up only 5.9% YoY). So the question arises: will policymakers unveil a further stimulus package to spur on growth? Recent policy directives of more bank lending to private enterprises have been viewed quite negatively by the equity markets of both Shanghai and Hong Kong. The rationale behind this is that against a backdrop of economic slowdown, investors would prefer to see tax cuts rather than any quasi-fiscal stimulus through bank lending as in 2008, as the latter would most probably lead to over-capacity and asset depreciation in the banking sector.

In a way, nothing has changed. Policymakers have faced the very same fundamental issue for years: the cost of achieving a targeted economic growth. The cost of doing so was extremely high in late 2008 as the short term boost to economic growth came with lasting side effects — a consensus arrived at by most of those in policy circles. The cost of such actions will be much higher today for the following reasons: 1) a far less favorable external environment (trade tensions and rising interest rates), and 2) domestic challenges (leverage and social costs of a relatively high growth rate).

Even if the outcome of the long-awaited Xi-Trump meeting is no more than a "skirmish", there will remain some unresolved issues in the US-China trade relationship. Should there be breakthroughs on sensitive areas of IPR protection and/or alleged forced technology transfers in China, and if so, how to monitor the progress would be “the $64,000 question”. If China pledges to liberalize the financial sector, would it even be possible to implement it in the short run? In the absence of compromise on both sides, 25% tariffs could lead to an escalation of the trade conflict, and global companies will be forced to change or adjust supply chains accordingly. The Financial Times recently reported that A.P. Moller-Maersk, the world’s largest shipping company, said that higher tariffs between China and the US could reduce global trade growth by 0.5% to 2% in the next two years. Moreover, the pace of growth of the US economy, the key locomotive engine of the global economy, is likely to moderate within the next two years as the Fed seems unlikely to stop tightening. In fact, in December it is expected to raise short-term interest rates in the US for the ninth time in three years. Short-term interest rates may not peak until they reach 3.5%, which could translate into mortgage rates no less than 6% in China next year. Given such unfavorable external conditions, China's best policy mix would be to lower the GDP growth target while unveiling concrete measures to improve the business environment. As such, tax cuts will have the most direct impact on this.

On the domestic front, the continuing weakness of the auto sector provides another compelling argument for significantly slashing import duties. Such actions were supposed to transpire in the summer but have not yet been realized. If Beijing makes a bold move in opening up the domestic market, the risk of stalled trade talks will be reduced.

Lastly, on the question of the RMB exchange rate, we would like to reiterate our long-held forecast of 6.95 and 7.3 in 2018 and 2019 respectively, even though the People's Bank of China still believes in maintaining the stability of the RMB exchange rate. The reduction of foreign reserves indicates that the PBOC has been allowing reserves to run down in order to defend the RMB. The cost of teaching the market a lesson (the PBOC reiterated its intention of keeping the RMB exchange rate above 7 and warned RMB short-sellers not to bet on a weakening Yuan) also means that the PBOC will have much less policy leeway in an environment of rising interest rates.

Financial Services

New issues of asset management under the bail-out measures

The continued downward pressure on the A-share market has exposed the increasing risk from listed companies pledging equities as collateral for their financing arrangements. It is believed that for some listed companies, controlling shareholders had already pledged as much as 80% of their holdings. In these circumstances there is a real risk that companies may face forced liquidation with losses even greater than those incorporated in through the trading margin mechanism.

In October, several Chinese government agencies and regulators came together to develop mechanisms to support private-sector enterprises listed on the A-share market. They have followed up with relevant policies in major financial sectors to establish a systematic form of "bail-out fund" like plans, aimed at reducing the risk of market instability. The bail-out fund arrangements will have at least two immediate positive consequences: 1) financial institutions will be able to directly participate in equity markets which should promote the development of their asset management (AM) businesses and capabilities and 2) companies should get a much needed infusion of liquidity.

The bail-out funds focus on the support of high-quality private-sector listed companies with a high proportion of equity pledged by major shareholders. The fund helps these A-listed companies restructure their financing arrangements and at the same time they take proportionate possession of the equities originally pledged to the financiers in order to effectively alleviate the risk of market instability as a result of a further decline in their stock prices. This has the added potential of reducing the cost of financing for listed companies.

Chart: Operating Principles for support initiatives

Chart: Various support initiatives

Area |

Policies and key points |

Amount (RMB) |

Banking |

Guideline of banks' wealth management subsidiaries: Funds will enter stock market, collaborating with private equity (PE) firms |

28 trn |

Securities |

Pool asset management plans support private-sector enterprises by establishing relevant asset management (AM ) plans |

100 bn |

Insurance |

Introduction of establishing special products by insurance fund: - such special products will invest in listed companies |

38 bn implemented |

Fund |

Encouraging fund institutions to support private-sector enterprises development by establishing AM plans to resolve stock pledge risk |

/ |

Local governments |

Beijing, Shanghai and various provincial governments have announced to establish bail-out funds led by State-owned companies |

10 bn per fund |

Source: public information, Deloitte Research

Direct investment channels open, benefiting the market

It is expected that the Banking sectors' financial asset management subsidiaries will take the lead in accelerating the development of each banks' AM portfolio. Following the release of a general framework of AM guidelines for the WMP business of banks, a more detailed `Guideline for Commercial Banks Subsidiaries for WMP Business’ will be officially issued in late November. All three major regulatory documents open up an investment path for banks' WMP capital which can now be tapped to purchase shares of listed companies directly (but no more than 15% of the total shares outstanding), collaborating with PE firms and no restriction on threshold amounts in sales. So far, 19 Chinese banks have announced plans to set up such subsidiaries, including the big five stated- owned banks, China Merchants Bank, Ping An Bank and China Minsheng Bank etc.

Supporting the involvement of insurance funds has further benefits. In principle, the longer term investment horizon and the current levels of liquidity could be considered to provide a more stable platform for market support. Currently, banks’ WMP units and insurance funds would appear to be the two main sources of capital that will be allowed (by regulators) to inject liquidity into the A-share market. In the short run, the scale of these funds may be limited, but in the long run, this move should gradually improve the capital supply. The arrival of the banks’ wealth management subsidiaries as institutional investors should boost market confidence, and help in controlling volatility.

For securities firms, it would appear that they intend to work directly with private-sector listed enterprises, not only to alleviate liquidity risk in the face of market instability, but also to iron out the difficulties of their own. Although securities firms need to tread cautiously amidst the numerous land-mines in the market, the bail-out fund also presents business opportunities for themselves.

The new requirements of risk management

The bailout fund is a market support mechanism driven `at the behest of government regulators’ and hence should be viewed with a little caution. Firstly, with market support funds moving into the market in large quantities, how one "irrigates" the drought-ravaged private-sector enterprises to avoid loss of profit is a challenge. Secondly, how does one enhance risk management processes to balance changes in the market dynamics. Put simply, 1) financial institutions should continue to assess corporate fundamentals and future development prospects of enterprises to identify promising high-quality prospects as well as limiting moral hazards, as was the perceived outcomes of some of the debt-to-equity operations that shunned rescuing zombie enterprises. 2) Banks' WMP subsidiaries and Insurance AM institutions should carefully navigate the new scope of any change in their business coverage, clarifying the differential positioning (with public funds) and enhancing their risk management frameworks.

Continued strengthening of the oversight of the IPO market, enhanced supervision and focus by regulatory authorities has continued to expose potential credit default and challenge the confidence of the market. Loopholes in the real economy have also become more evident and the increasing fragility of the market has been exposed. With this in mind, we believe it is fair to say that market volatility is likely to remain at a high level, with continued uncertainty over the pressure on the financial services industry and the real economy. The future direction of the market still depends, in large part, upon the regulatory environment, commitment to policy directives, and the sentiment in the stock market itself.

Automotive

Will China’s car market remain in the doldrums?

China’s auto sales plummeted by 11.7 percent in October, the second straight month of double-digit decline, making it the longest period of contraction the world’s largest auto market has ever experienced. Furthermore, the China Association of Automobile Manufacturers (CAAM), a government-sanctioned industry association, has confirmed that vehicle sales are on track to record the first annual decline since 1990.

Chart 1: Auto monthly sales Chart 2: Inventory alert index

The most commonly-cited culprit is the weakening economy. But many people argue that the contraction in car sales is internally driven and external headwinds have only helped amplify the market slump. For example, the expiration of the purchase tax cut and the absence of alternative policies has saturated the market with advance sales while demand has waned.

Automotive institutions have been blaming the booming property market for the weakening car sales as Chinese consumers have preferred to purchase real estate assets over cars. We hold a different view on this. When prices in the property market are rising steadily, property owners are more willing to spend as they are confident that the price of real estate will keep rising. But, when property prices peak or show only moderate growth, consumers tend to tighten their purse strings. In addition, Chinese households who have seen a rapid rise in borrowing are less inclined to borrow or to spend.

Third, China has put a cap on the fast-expanding but risky peer-to-peer lending business as part of its financial deleveraging campaign. This has hit private consumption hard. Although auto financing in China is not as prevalent as in developed countries, it has grown rapidly, fuelled in part by the booming consumer credit platforms.

US-China trade tension remains the largest external factor affecting the Chinese economy (as evidenced by the falling RMB and a stock market which is unable to lift itself out of bear-market territory). Although financial assets only account for 15 percent of household wealth, the uncertainty and lack of consumer confidence has weighed on car sales.

In addition, it is worth pointing out that China’s auto market is undergoing a major structural shift. The last two rounds of policy stimulus weakened the business cycle and exacerbated the volatility of the auto market. This is clearly reflected in the data: sales in the lower-end segment (TP<100k RMB) have slumped dramatically whereas in the higher-end (especially luxury) segment there has been a 13% growth in the first nine months. This is in stark contrast to the popular belief that there exists a so-called “consumption downgrade” across China. The shrinking demand for low-price, entry-level cars not only indicates that car buyers have become more quality conscious and rational about their purchases but also shows that China’s car market has matured. As for the buoyant luxury segment, it only underscores the irreversible trend of consumption up-gradation among the rising middle class population (the cut in import tariffs also helped fuel this growth).

Car companies are worried that the slump indicates a prolonged downwards trajectory for China’s car sales rather than a normal cyclical adjustment. We believe that the latter is the case and the automotive market will bottom out in mid-2019 and then slowly start regaining strength when external headwinds fade and large-scale tax cuts are rolled out nationwide with a view to boost consumer confidence (especially of the lower-to-mid level income earners who have higher marginal propensity to consume).

Energy

Place your bet on China's shale gas

Bolder steps taken in unconventional hydrocarbons

Earlier this month, the Ministry of Natural Resources is said to have reviewed shale gas development with a view to taking back the blocks where operators failed to make the promised investment before offering them again in a fresh round of public tenders.

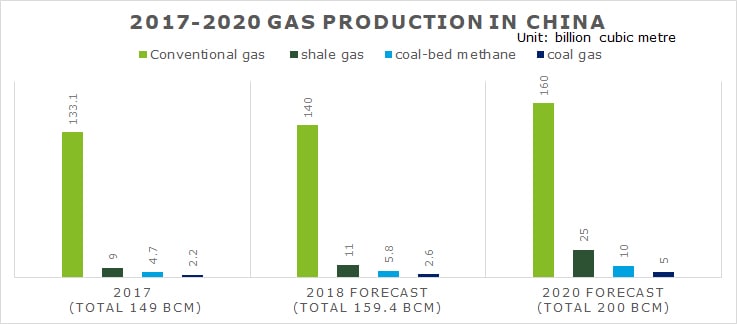

The objective of this upstream reform is to invite fresh investment from private and foreign companies and thus re-invigorate China's lackluster upstream exploration and curb the decline in the nation's oil reserves base (oil reserves hit a 10-yr low of 6.4 bn barrels last year). Compared to the cautious opening up of conventional oil and gas sectors to international companies, the Chinese government has made far bolder strides in unconventional hydrocarbons, launching several rounds of tenders in shale gas since 2011 and offering coal-bed methane (CBM) blocks starting 2017. This coincides with the recent shift in focus from oil to gas, especially to shale and CBM. The CAGR of Chinese oil production in the past decade is a mere 0.3%, dwarfed by that of gas production which is 8%. From 2011-2017, the cumulative growth of China's natural gas production is 7%, in which conventional gas grows at 6%, CBM at 14% and shale gas at a stellar 82%.

With the mature basins in the east facing a rapid depletion of reserves, the new blocks (which will be offered via licensing rounds) are to be found in the north-west and south-west of China and are mainly unconventional resources. These remain under-explored due to technical and logistical challenges. Hence, technological breakthroughs (including enhanced oil recovery, geophysical prospecting, well drilling and other services) are the key to tapping the potential of these areas. As foreign companies have better technology, this plays to their advantage.

Foreign investment in shale

Formerly, foreign oil companies that wanted access to Chinese oil and gas reserves had to enter into a Production Sharing Contract Agreement with the state-owned giants through private negotiation. Now they will probably be able to form joint ventures with Chinese partners to bid for onshore acreage. BP's presence in China's shale gas exploration is a case in point.

Currently, BP is the only foreign operator in China's shale gas reserves. It moved quickly after signing a production-sharing contract in 2016 with CNPC in what was at the time a very bold move given the withdrawal of Hess, Chevron, Shell and ConocoPhillips from China. Cost was the major concern as there were doubts about the viability of shale gas in China without government subsidies. So what does BP know that its predecessors didn’t know?

Technology is indeed the answer. In the Sichuan Basin, BP is backing its new-found technology of "multilateral drilling" that it has been developing at its Lower 48 onshore business in US. Multilateral wells feature many horizontal wells connected to a single vertical drilling hole—or "well bore"—that allows it to access more oil and gas in a single reservoir, but with fewer drilling sites, hence deliver premium returns at lower cost. This technology enables BP to unlock pockets of oil and gas in China's complex mountainous terrain that would have otherwise probably gone untapped.

Looking ahead

Demand for natural gas is set to grow at a significant pace, given China's firm pledge to move to a low carbon economy and replace coal with gas for heating. As the International Energy Agency reports, "the outlook for China's gas production is more upbeat than oil", noting that the projected increase from the current 140m barrels/day to 340m barrels/day in 2040 is "due almost entirely to an expected expansion in unconventional production, largely from shale." Second, policy support is implied in setting production targets. The paper entitled "Opinions on sustained and coordinated development of natural gas", newly issued by the State Council on 5 September, lays out the target for gas production as 200 bcm/y by 2020, and considers extending government subsidies for unconventional hydrocarbons to the 14th five year plan as well. As outlined in an earlier version of the "shale gas development masterplan (2016-2020)" by China’s National Energy Administration, Beijing had set the shale gas production target at 30 bcm/y by 2020 and 80-100 bcm/y by 2030.

Global oil prices have gone back into an upswing (despite recent corrections) with the US’s sanctions on Iran, and Venezuelan oil production in a "free fall". According to Fitch Solutions, the Brent is likely to settle at the $70-90/barrel range in 2019. High oil prices provide an incentive for independents to take on new ventures.

Figure 1: Policy-induced expansion of unconventional gas

However, there are certain pitfalls. Foreign operators have no choice other than to work with nationally-owned giants such as Three Barrels, as they control more than 70% of total shale gas resources in the existing acreages. Second, there remains significant uncertainties about the quality of China's shale resources as well as the eventual cost of production. This is because while the most prolific fields in America are tapping shale gas from only 1,600 metres beneath the earth’s surface, in the Sichuan basin shale gas is being tapped at depths of up to 4,800 metres. China's deposits also present technical difficulties not experienced in US shale fields, one of which is a high population density that makes access to land difficult. Third, policy uncertainty remains, since many of the measures announced are still only guidelines and detailed plans are yet to be rolled out.

Seen in this light, BP's collaborative venture with CNPC in China's shale gas may end up working as a pilot program., For if the group can land gas at viable costs, it will quite possibly trigger a scramble by foreign operators that would, in fact, be welcomed by Beijing. But in practice, Beijing is more likely to resort to a gradualist approach to maintain its energy independence. Meanwhile, foreign companies should strive to negotiate for better terms in this evolving game. That said, the easing up of regulations on joint ventures with foreign companies (and even foreign direct investment) in the upstream business may not be as far-fetched as it sounds.

Life Science & Healthcare

A new page in clinical trial regulation

On November 5, 2018, the Center for Drug Evaluation (CDE) under CFDA started to implement the new "registration-based" clinical trial approval process. This is a step forward from the old "approve-and-go" review and approval process. In the new process, a company can proceed clinical trial if CFDA has no comments on the application within a given period of time. Although the new process only applies to new drugs, it can be seen as an important part of the overall "simplification" strategy of China's drug administration and will definitely have significant impact on the R&D value chain in China.

New process will benefit innovative drugs and solve backlog issue

China has been plagued by backlogs on drug review and approval for the last several years. Project backlogs exceeded 22,000 cases in 2015. One of the major tasks of China's drug administration in the past three years has been to tackle the backlog issue head on. According to a CDE annual report, the time for review and approval of new drugs in 2017 averaged about 120 workdays. The new process, however, requires the CDE to start the approval process within 5 working days of receipt of all the required documents. Furthermore, they must grant the go-ahead for clinical trials if there are no negative comments from the evaluation committee within the following 60 workdays. Thus the new process saves a lot of time, something that will be of great benefit to innovative drug manufacturers.

Market demand & supply will change

Current CFDA data shows that by the end of October 2018, there were 825 certified clinical trial institutions in China. However, many of these institutions are newcomers and could lack the capacity and experience required for testing. Once the new ‘time-bound’ approvals process is fully implemented, demand for clinical trials will significantly outstrip supply, which will cause the overall cost of clinical trials to rise.

This will change the clinical trial market, making it go from a "regulation-focused" approach to a "market-focused" one. Hence, while the new approvals process will accelerate China's new drug development, it will also push up the prices of clinical trials which means that the development budget for new drugs will also need to be increased.

Risk management is becoming more important

The reform of the drug review and approval process will raise the bar on drug administration as well. The safety of clinical trial subjects has always been, and will continue to be, a priority. But Chinese institutions lack a good track record on ethical review and lag behind their western counterparts.

To sum up, drug makers should develop well-established protocol and management mechanisms to avoid unnecessary increases in cost and risk. Otherwise it will be hard for them to benefit from the new approvals process.