Perspectives

The Deloitte Research Monthly Outlook and Perspectives

Issue L

9 August 2019

Economy

Heightened uncertainty ahead of trade deal

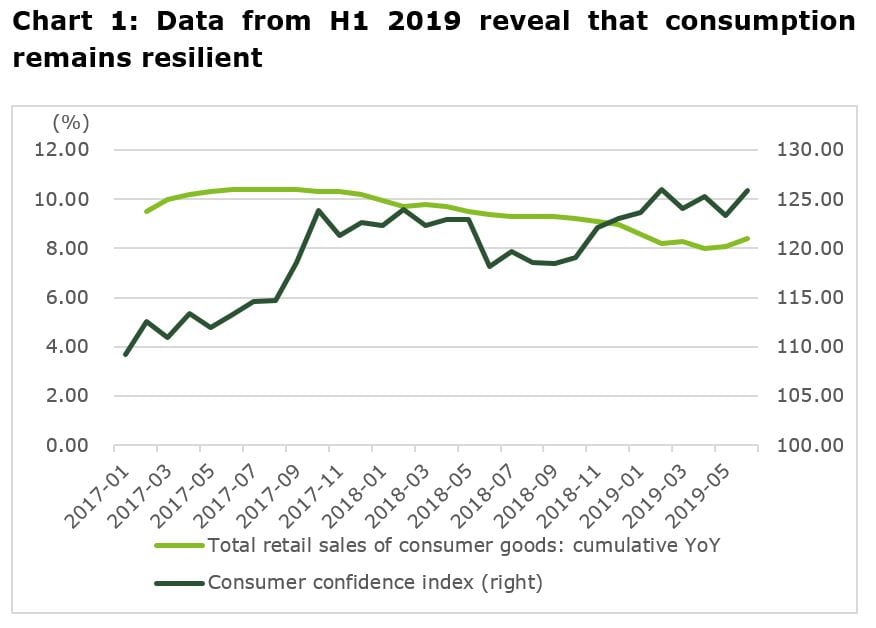

Consumption resilient despite external shocks

It may sound like a cliché but the fact remains that data for the first half of 2019 (GDP growth of 6.3%) have clearly revealed the resilience of the Chinese economy. If we dissect major economic data of H1, consumption remains the brightest sector with retail sales showing an increase of 8.4%. However, it is our firm belief that retail sales would better reflect the real state of the economy if auto sales (down over 12% in H1) were not taken into account. Investment has also held up, growing by more than 5% in the first half of the year. In particular, investment in property has risen by almost 11% - and this is in spite of the fact that most major developers have reported having great difficulty in funding their projects.

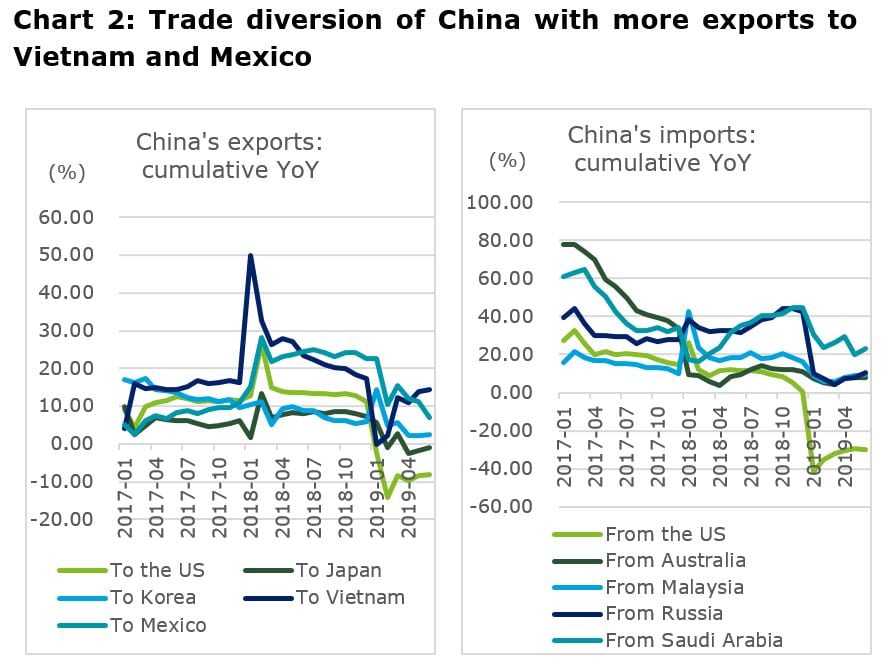

As was expected, the external sector has been the most affected by the trade war. US exports to China fell by almost 30% in H1, and China's exports to the US, China's largest market, has dropped by 8.1% disappointingly due to 25% of tariffs on over $200bn of China's exports. It seems that trade diversion is happening with more exports to Vietnam and Mexico. Besides, China's exports to Japan and Korea, No. 3 and No. 4 overseas market for China, held relatively steady with the change of -1.1% and 2.5% in H1 respectively.

RMB revaluation in face of global monetary easing and trade war salvos

On August 5, USD/CNY broke 7.0, a key psychological threshold, and continued to edge higher on PBOC's eased control and latest trade war salvos (the US Treasury has designated China as a currency manipulator on the same day). As more central banks have slashed rates, China is in the position to ease, therefore, this RMB revaluation could be seen as an immediate boost of liquidity when short-term interest rates' movement could be floored. A mild currency depreciation and a cut of short interest rate have the same effect from the standpoint of loosening monetary conditions.

Despite the cut of 25bps on July 31, the US Federal Reserve is likely to slash the Federal Fund Rate by another 25bps in the second half of 2019 (could be as early as in mid-September, at next FOMC meeting). In fact, treasuries have staged ferocious rally in the past week with 10-year treasury yields plummeting to 1.75% from above 2% a week ago. The Fed's dovish stance, which was initially prompted by a potential economic slowdown in the US and trade tensions, was later reinforced by the European Central Bank's return to quantitative easing. Severe corrections of equities could lead to monetary easing by the Fed. So should the PBOC lower interest rates as what some of the region’s central banks (e.g., Bank of Korea and Bank Indonesia) have done? The short answer is not yet. Lowering interest rates won't address the fundament issue - lack of access to credit by private sector and SMEs who are suffering from a severe credit crunch due to ongoing economic and financial restructuring. Moreover, if the PBOC joins other central banks in their easing exercise, instead of guiding money to SMEs, it could end up leading to renewed speculation in the property sector—exactly what policymakers have been striving to avoid.

Alternatively, the PBOC should move to a slightly more flexible rate regime, a managed float (not a free float by any means). The market of course is expecting further weakness of the RMB because forex market is more prone to momentum trading in the short run. So it is more important for China to open up domestic market in order to ease concerns of China's trading partners. But one cannot rule out the possibility of black swan or grey rhino events occurring. What if, for example, tit-for-tat moves by China (state firms were asked to stop buying US agricultural products according to CNBC) and the US (10% tariffs on $300bn of Chinese exports could arise) bring about global stock markets crash, in turn leading to a recession of the US economy? The fixed income market (the Fed has been indeed led by the market) has even discounted two more rate cuts, in addition to 25bps in July, in 2019. Against this backdrop, there will be more pressure for the PBOC to join monetary easing chorus.

China's stance after latest "constructive" trade talks

The latest round of trade talks in Shanghai (July 30 and 31) ended early with a mutual acknowledgment of "having had constructive talks" and a clearly stated commitment on China's side to purchase more US agricultural products. However, on August 2, President Trump announced a new set of tariffs, of 10%, on $300 billion worth of Chinese exports (to come into force on September 1st), on the grounds that China did not live up to its promises. Immediately US asset markets reacted negatively – stock values went down, bond yields fell, and oil prices also fell sharply. All of this contributing to an even dimmer economic outlook for the remainder of the year. More significantly, while China's A shares also reacted negatively, share prices of rare earth went up, bucking the trend and reflecting investors' expectation of retaliatory tariffs from China.

But there is still a little space for optimism. The fact that both parties have used the word "constructive" to describe the last round of trade talks, which at least did not collapse, demonstrates that both sides are aware that they cannot ignore ground realities. It would be unrealistic for the US to imagine that China can fundamentally alter its economic model even in the medium term. But China also needs to understand and address certain grievances of its major trading partners - especially as some of the requests from the US such as more effective protection of intellectual property and better access for foreign goods and services to the vast domestic market are very much in line with China's own reform objectives. Hence, we are confident that a trade deal can be struck before 2020 since an escalation of trade tension is not in either party's interest. Of course, such trade deal or "truce" cannot be taken for granted. A resolution with Huawei would be seen positively by China. And on its side, China can easily, if it wants to, step up its purchase of US agricultural products. But even if the US could achieve a so-called fairer trade or balanced trade with China, it may not be the optimal outcome for both countries. If Washington and Beijing engage in a grand managed trade, in which China guaranteed to buy certain US products in exchange for access to the largest consumer market, the end result would create more frictions with other trading partners (i.e. substitution of trade in agricultural and energy products) and be detrimental to the global trading system.

Therefore, it is still in China's best interest to cut tariffs close to the level of developed countries. In the short run, global companies are likely to take a wait-and-see approach when it comes to changes of supply chains (over 60% US companies in China don't have plan to relocate manufacturing facilities, according to an Amcham survey). But if trade talks drag on, average tariffs of China's exports to the US could conceivably force many global companies to reevaluate their supply chains. What could China do to mitigate such disruptions? Local governments are expected to roll out various relief measures such as subsidies and tax rebates. However, from central government's standpoint, agonizing trade talk may have raised a deeper questions – how to entice global companies to invest more into China's domestic market where there is ample demand unmet.

In conclusion, Fed's dovish stance is indeed a respite to most emerging markets including China but the PBOC is expected to maintain its neutral monetary stance in view of a relatively resilient economy. But a truce of trade war is needed so that wounded investment sentiment could gradually heal.

Retail

3rd and 4th tier cities become China's E-commerce new battlefield

In this year’s June 18 Mid-Year Shopping Festival, 3rd and 4th tier cities and towns were heavily targeted by Chinese e-commerce players who launched several promotional campaigns such as group buying platforms and flash sales specifically targeting these areas. In these markets, e-commerce players with a strong presence on social media networks such as Pinduoduo saw a clear spike in growth through the launch of promotion campaigns such as flash sales and group buying platforms. Thereafter, major traditional e-commerce platforms including Alibaba, Jingdong, Sunning, seeing the potential in these 3rd and 4th tier cities, also started their own flash-sale and group-buying platforms. All in all, there are three reasons for this sudden spurt in interest in lower tier cities and rural areas.

As on-line shopping slows down nationwide, and especially in the first and second tier cities, there has been a gradual realization that lower-tier cities will become the main growth driver for e-commerce platforms as more than 70% of the Chinese population resides in these areas. The cumulative consumption demand in this market is therefore huge and consumption growth in these areas is increasing steadily. According to Alibaba’s annual report, their e-commerce platform signed up 120 million new monthly active users in 2018, 70% of which came from Tier 3 cities and below.

Rising disposable incomes in rural towns and cities has unleashed consumer demand. Thanks to some timely tax reductions and wage increases as well as shelter reform and poverty alleviation policies, the incomes of residents in 3rd tier and 4th tier cities and rural areas have been increasing each year. In contrast to consumers in 1st and 2nd tier cities, the residents of 3rd and 4th tier cities face less cost-of-living pressure in terms of mortgages, rents, eating out, schooling, and entertainment. Hence, rising incomes have boosted consumption for the middle and lower income families in these fast growing urban centers in the hinterland of China, an area once considered to be of little importance to the retail market. Data on the June 18 Mid-Year Shopping Festival released by Juhuasuan (an Alibaba’s group-buying brand targeting lower-tier cities) showed that the growth in sales of inexpensive goods such as small household appliances and furniture supplies in 3rd tier or 4th tier areas was twice as high as the growth of similar products in 1st and 2nd tier cities.

The continuous increase in Internet penetration at the 3rd and 4th tier city level has widened the reach of e-commerce platforms and retail brands. According to quarter-on-quarter data provided by QuestMobile, a third-party data provider, while the total number of mobile users in China dropped by nearly 2 million in the second quarter of 2019, 3rd and 4th tier cities saw an increase of active mobile users. In addition, monthly active users in 3rd and 4th tier cities grew by 59.4% yoy in June 2019.

Future trends of e-commerce in lower-tiered cities

In the near future, E-commerce giants and retail brands will remain focused upon the 3rd and 4th tier city market as sales in the 1st and 2nd tier cities slow. With more e-commerce giants and emerging social e-commerce players entering the market, competition will intensify.

As incomes in rural areas rise and wealth grows in the 3rd and 4th tier cities, so will the demand for higher quality goods and services. When this digitally-fuelled maximizing lifestyle goes mainstream, consumers in these markets will seek to purchase premium brands and the latest products.

Thanks to their extensive use of social networks, the market penetration of Pinduoduo in 3rd and 4th tier cities will continue to grow. However, social e-commerce platforms are hindered by the presence of counterfeit goods on their sites and a weak brand image. To counter this problem, social e-commerce platforms like Pinduoduo recently implemented more stringent rules to remove counterfeit goods from their platforms and partner with more reliable manufacturers and premium brands.

Media

Is Chinese cinema losing its shine?

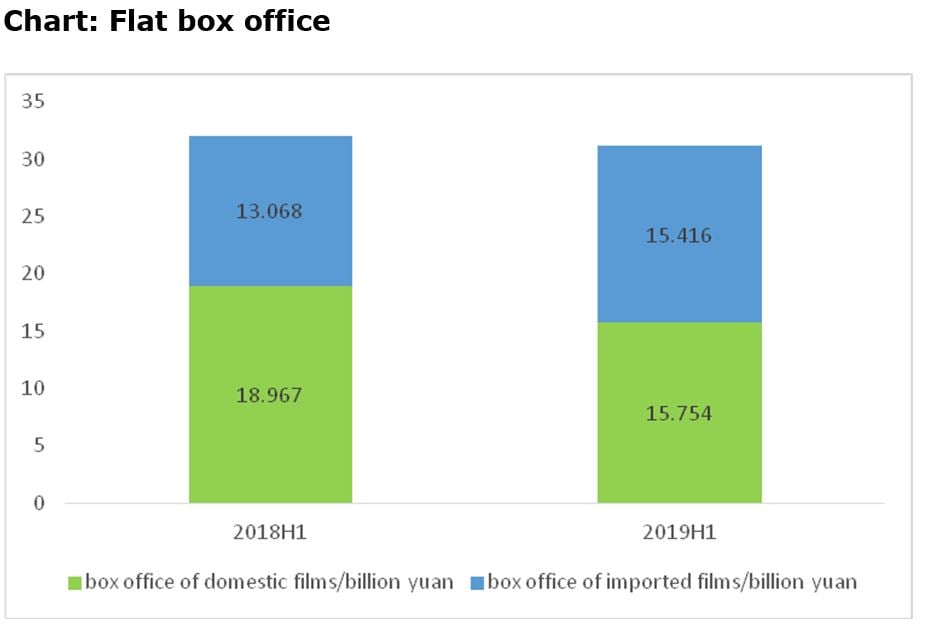

In the first half of 2019, the Chinese box office netted a little over RMB 31 billion, down 2.7% from the RMB32 billion of the comparable period of the previous year. Moreover, in the first six months of the year, only 806 million tickets were sold, down 10% from the 901 million tickets that were sold in the first half of 2018. This is the first ever decline in box office takings in nine years. The only exception being the recently released "Nezha", which became the 10th highest grosser ever in China after two weekends. Should we be concerned? Is this merely a hiccup in sales or is it indicative of the shape of things to come? If indeed interest in the cinema is flagging, what can the industry do to woo moviegoers back?

Lack of blockbusters and ticket price hike

A quick look at past box office data shows that perhaps the decline wasn’t all that unexpected. For, after years of very rapid growth, it is hardly surprising that the Chinese film industry entered a cool-off period in 2018. The decline in the first half of 2019 was mainly due to the poor performance of domestic films which made less than RMB16 billion, a decrease of 16.9% over the same period last year. Foreign films took up the top monthly box office receipt spot for 5 of the 6 months in the first half of the year while the only domestic hit that occupied the much coveted top spot was "The Wandering Earth" released in February. In addition, 8 of the 16 domestic films with over RMB100 million in box-office receipts were released during the Chinese New Year (CNY) holiday this year, resulting in a dearth of new releases in the months that followed. That a large number of domestic films rushed for release during the CNY holiday can also be attributed to two reasons: first, everyone hopes to profit from the time when attendance is highest as during the CNY holiday; second, as many domestic movies are not good enough to compete with imported films during regular release calendars, releasing during the CNY holiday can effectively reduce the risk of competition.

Average ticket prices spiked to RMB38.6 each in the first half of the year as a result of a subsidy reduction on tickets. Between 2014 and 2017 ticket subsidies played an important role in the rapid expansion of the Chinese movie market. In 2015 alone, ticket subsidies reached RMB 4 billion, accounting for 10% of the total box office takings. In 2018, the authorities halted ticket subsidies to third-party and cinema-owned channels, resulting in the elimination of the "9.9 yuan movie ticket" and other attractive discounts. Movie-goers had to pony up 11% more on average for a ticket, putting a dent in their movie-going enthusiasm.

Per screen income also down

Shift in demand has put pressure on all parts of the film industry chain. For cinemas, although new screens are being added across the country on a daily basis, revenue per screen is declining. In the first half of 2019, the number of screens reached 64,944 (China has built 3,492 new screens so far in 2019) along with 691 new cinemas. But revenue per screen was just RMB1 million, down 8.3% year-on-year. The attendance rate of theatre chains also dropped in the first half. The top three theatre chains - Wanda Cinema, Dadi Cinema, and Shanghai Union Cinema - averaged 12.02%, 10.51%, and 11.82%, respectively, in terms of attendance rates.

Distributors adjust screening and promotion strategies

For distributors, adjusting film selection criteria and broadening and enriching promotion channels are both necessary strategies to cope with the downturn.

In terms of selecting film subjects, distributors will need to conduct thorough data analysis to identify the many individualized needs of current consumers while paying closer attention to the ideas that they hope to communicate through their films. Box office hits such as "Dying To Survive" and "The Island" should be studied closely in order to understand what in the films appealed to audiences.

Furthermore, moviegoers today are becoming "pickier than ever”. Not only do they care about the quality of the content, but they also care about the ways in which the films are promoted. Moviegoers have grown tired of being bombarded by advertisements, which means that distributors need to utilize precision marketing to find their target audience and to be innovative in marketing content at the same time. This year's hottest promotional video, "Who is Peggy?" went viral with more than 20 million views on Weibo, attracting a large number of moviegoers for the release of the film "Peppa Celebrates Chinese New Year ".

Competition intensifies amid capital withdrawal

Upstream film production companies are facing serious financing difficulties as funding for films gets more difficult to access. The "tax scandal" of last year not only put filmmakers on edge but also scared off investors, accelerating capital withdrawal. At the same time, relevant authorities have strengthened supervision over the film and television industry and implemented more stringent requirements for the production and promotion of movies, making the entire film industry much more cautious about script creation, copyright usage and artist selection. The simple “IP plus pop stars” model which has been the commonest path to windfall profits in the Chinese film market is losing its luster. This situation of greater scrutiny and tougher financial conditions may, however, actually present an opportunity for the industry to reshape itself, and allow emerging companies capable of producing high-quality movies to rise to the top.

The decline in box office profits simply means that the Chinese film industry has entered a new stage in its development. The explosive growth of low-quality films that relied solely on the size of China's population to be successful has come to an end as short videos, online movies, variety shows and other forms of entertainment vie for the attention of the Chinese viewer. However, one can't ignore the fact that some aspects of cinema are even today, irreplaceable: providing a top-notch entertainment product, for example, while acting as an offline social platform. The most urgent task for film practitioners therefore, is to enrich content, enhance quality, and, at the same time, integrate new technologies and new consumption models into their work.

Logistics

Smart warehousing is the key to logistics real estate market

A quality logistics warehousing market has yet to be developed

The logistics industry has been growing steadily in China over the last decade. Between 2010 and 2018, total logistics expenditure increased from RMB 7.1 trillion to RMB 13.3 trillion, an annual compound growth rate of 8.16%. This hectic rate of growth has been fuelled by the needs of the rapidly expanding Chinese economy. The Chinese Association of Warehouses and Storage reported that by the end of 2018, the number of logistics parks in China had reached 1,638 - a compound growth rate of 10.6% in the 2015-2018 period. Although the quantity of real estate used by the logistics industry in China (approximately 955 million square meters) is exceedingly large, the proportion of high-quality logistics facilities compared to total stock is relatively low (about 5%). This needs to change as, along with the recent boom in E-commerce and high-tech manufacturing industries, demand for high quality logistics facilities will certainly grow exponentially, widening the gap between supply and demand. Thus, there exists a huge opportunity for those willing to step into the breach and develop high-quality warehousing and stockage facilities.

The government, meanwhile, has launched a number of policies in support of the logistics industry. In December 2018, the National Development and Reform Commission and Ministry of Transport released a plan for the construction of 212 national logistics hubs with widespread coverage, high capacity and close links. This will enhance efficiency and promote cooperation within and between regions, thus making possible a more organized development of the logistics industry.

The 'asset-light' strategy goes mainstream in logistics warehousing

The 'asset-heavy' nature of logistics puts constrains on the industry in terms of land and capital. A prolonged investment cycle will put pressure on the later stages of operation after construction is complete. It is therefore a major challenge for corporations to identify a healthy profit strategy in coping with these two crucial factors – land and capital – according to their own growth capacities and capabilities. Considerations on warehousing strategies vary as demands are different. Most companies for now adopt asset-light strategies – going for rental rather than outright purchase.

Rental income from logistics warehousing has been growing steadily in recent years, and return on investment is higher than in other types of real estate investment. The net rate of return for logistics facilities in major cities such as Beijing, Shanghai and Guangzhou ranges between 6%-8%, higher than that of commercial real estate (4%-5%) and residential real estate (2%-3%). The reason behind the high rental returns is that the logistics warehousing industry in China is still in its infancy, and there is a dearth of high-quality facilities.

There are 3 characteristic modes of operation employed by the logistics real estate corporations.

Table: Main operation modes of logistics real estate corporations

Operation modes |

Characteristics |

Examples |

Funding-driven |

This kind of corporation depends on strong capital operation groups. They first establish private funds to purchase the real estate and then recycle the funds to develop new projects, forming a high-speed, high-return, asset-light strategy. |

GLP, Goodman Logistics |

Resource-driven |

These corporations own core warehousing assets and hence adopt asset-heavy strategies. They are mostly traditional real estate companies which are capable of securing land parcels and have an abundant supply of land. |

BLOGIS HOLDING LTD, VX Logistic Properties, Wanke |

Industrial chain-driven |

This kind of corporation has their own industrial chain. The reason for them to develop logistics real estate is in order to strengthen co-operation within the industrial chain, optimize services and reduce operation costs. Many logistics and internet corporations are members of this group. |

Jingdong, Ali Cainiao, SF Express, YTO Express, STO Express |

Source: Deloitte Research

The future of the logistics real estate market

- High-tech smart warehousing facilities will be the next hotspot

There is a rising demand for automatic and precise warehousing management thanks to the rapid growth of e-commerce in China. Consequently, based on technologies such as mobile internet, big data and cloud computing, a certain smart warehousing system has come into being that features intelligent sorting and robot-centred operations. This kind of ‘intelligent’ warehousing system is what is guiding the development of warehousing hardware. Moreover, environmentally-friendly warehousing starts to become a trend. For example, Suning logistics plans to launch its Green City Project in 13 cities in 2019, which includes Green Warehousing. This will force logistics real estate companies to improve their ability to innovate.

- More attention will be paid to the completeness and quality of service

The core competitiveness of logistics real estate depends upon the quality of service rather than actual storage space. In this highly competitive industry, companies will focus more on developing the clients' loyalty by improving value addition to services. To accomplish this goal, companies will design and develop a whole package of services based on the needs of the industrial chain of their customers and then strive to improve the efficiency and quality of their services in terms of location, storage, processing and distribution.

- Exploring more strategies for operation and profit

Traditional operation strategies have a longer cycle of return on investment and therefore cannot meet the needs of rapidly expanding companies. Hence, more and more companies are beginning to explore new strategies for operation and profit: changing from the old `asset-heavy’ strategy to "asset-heavy holding + asset-light operation"; in other words, they are moving from profiting merely by rentals to profiting through "logistics + finance"; and boosting earnings by way of services of investment, capital and distribution management.

- Industry integration is the new trend

On the one hand, the logistics real estate market is intensely competitive and on the other, it is still quite scattered — making horizontal integration among companies not just highly possible but also quite probable. Examples of such integration include GLP's acquisition of Gazeley and GLP's cooperation with Pingan Real Estate. However, vertical integration between operators and developers would offer both sides better resources, which is beneficial to all.