Perspectives

The Deloitte Research Monthly Outlook and Perspectives

Issue LIII

13 December 2019

Economy

PBOC's neutral stance remains intact

The PBOC recently lowered the rate on its one-year medium-term lending facility (MLF) by 5 basis points to 3.25% from 3.30% previously. This adjustment drew wide attention, prompting the question: has the PBOC finally joined the global easing chorus? If so, by how much could we expect short-term interest rates to be cut in 2020? But if the PBOC does not bring down the rate further what message will it be sending? Before we answer these questions, let us briefly examine recent data releases. Rising from October's reading of 49.3, November’s manufacturing PMI broke through the threshold of 50 that divides optimism from pessimism. Non-manufacturing PMI rose from 52.8 in October to 54.4 in November. However, November's trade data, which show a decline in exports of 1.1% and a rise in imports of 0.3%, suggest that the external sector is likely to remain a drag on growth for some more time.

Chart 1: Weak property price will eventually weigh on strong investment

Hence, the rebound in the PMI does suggest that the economy is resilient and stable. But a single swallow does not make a summer. Since October there has been a visible slowing of new investment in the housing market. Thus the surprisingly strong overall growth of 10.3 percent recorded from January to October is unlikely to be sustained in 2020. Over a two-year time horizon, our survey suggests that, barring changes that could be brought about by the conclusion of phase-one of the imminent trade deal, supply chains are likely to remain intact in the coming months. (89% of our respondents said that they did not intend to make any significant change in their supply chain.)

Another indication that the growth of investment in housing was likely to flatten was provided by a recent PBOC report on consumer leverage, which showed that the level of consumer debt in relation to incomes, in China, is now similar to that of some developed countries. According to the report the consumer leverage ratio had reached 60.4% by the end of 2018. The total outstanding mortgages amounted to RMB25.8 trillion by the end of 2018. This was 53.9% of total consumer debt. The report argues that such a high level of debt is bound to constrain consumers' ability to take on fresh consumption commitments. It warns that if housing prices start to decline, banks could well see rising non-performing loans in certain cities.

Against this, however, it can be argued that it is misleading to use the debt leverage ratios of developed countries to gauge paying capacity in the Chinese market. First, growth in the developed countries is now sluggish, which is not the case in China. Second, China's chief strength lies in its strong family ties, which allow seamless wealth transfers across generations. The willingness of frugal parents to finance their children's debt should mitigate some of the concern being expressed in the report over China's relatively high consumer leverage. That being said, however, Chinese consumers could still cut back their investment in housing if they do not expect further capital gains in 2020. Our base line assessment of the housing market in China remains therefore that while the first-tier housing market will remain stable, the second- and third-tier markets will see mixed results.

Chart 2: Chinese consumers' resilience remains intact despite rapidly rising leverage

The way in which the PBOC has cut MLF appears to be more symbolic than substantial: it highlights the Central Bank’s commitment to ease liquidity if necessary but does not herald the beginning of monetary easing. Interestingly, Yi Gang, PBOC's Governor, has penned an article titled Stick to the Goal of Currency Stability and Implement a Prudent Monetary Policy, arguing that it is not the role of the PBOC " to dilute the savings (in RMB) amassed by the people, so it would not to engage in any competitive devaluation". We have interpreted Yi Gang's assurance of price stability as an indicator of the PBOC's bias in favor of a neutral monetary stance. Its pledge to maintain a stable exchange rate for the RMB is also most probably a gesture of goodwill towards Washington before Beijing and Washington sign the long-awaited phase-one trade deal.

The good news is that both sides have been trying to set non-economic issues aside while the not-so-good news is that the so-called phase-one deal is likely to entail a somewhat managed trade between the two largest economies in the world (reminiscent of what the US and Japan practiced in the last decades of the past century). Such managed trade has the potential to create tensions with other economies in the region if China reduces its buying from them to buy more from the US in order to reduce its bilateral trade surplus with the US. This could act as a constraint on the PBOC’s use of monetary levers – interest rates and exchange rate.

Financial Services

Reform of SMS banks to accelerate

China's small and medium-sized (SMS) banks are undergoing a major restructuration and this is about to accelerate. The takeover of Baoshang Bank by the People’s Bank of China and the restructuring of the Bank of Jinzhou as part of the financial supply-side structural reform being implemented since the beginning of this year were groundbreaking events. However, they accentuated the crisis of confidence vis-a-vis SMS Banks in the market, making it more difficult for these banks to meet their financing needs. On the one hand, high-risk financial institutions should not be "too-small-to fail"; on the other, it is important to discover and solve operational problems so that they can get back onto a path of healthy and sustainable development. After all, the ultimate goal is not to kill but to make these vulnerable banks healthy. As painful as reform may be, SMS Banks, as the fountainhead of small- and micro-finance, do indeed have a bright future.

Critical period of risk and pain

SMS Banks, namely urban commercial banks and rural commercial banks, occupy a very important position in China’s banking system. They have a total asset size of about 26% of the total assets of the banking industry and provide 52% of all the inclusive micro-loans.

Since the crisis of Baoshang Bank in May this year, financing costs (the issuing interest rates of interbank negotiable certificates of deposit, NCDs) of urban commercial banks and rural commercial banks have continued to rise, causing an ever increasing crisis of confidence in SMS Banks. The crisis has been aggravated by the increase in the non-performing asset ratio which, at the end of the first three quarters, reached 1.86%. At the same time, growth of social financing continuously decelerated. In October, total social financing increased by RMB 618.9 billion, registering a decrease of RMB 118.5 billion from the same comparable period last year, a level that was below market expectations.

SMS Banks face two serious problems. The first is shadow banking. Some banks, in the past few years, used shadow banking to expand their investment business at the same time allowing their loan businesses to remain weak and their capital adequacy levels insufficient. As a result, they are facing a liquidity crisis. On the other hand, some regional banks have actually become little more than ATM machines for large shareholders or local governments. They are mandated to make loans to poorly-operated entities. As the economy decelerates, some of these loans have become non-performing, negatively affecting the performance of these banks. But behind this lies the root cause of today’s crisis - the lack of corporate governance – which is in fact responsible for the present situation.

Reform accelerates

In response to the crisis of liquidity in SMS Banks, Zhou Liang, vice Chairman of China Banking and Insurance Regulatory Commission (CBIRC), cautioned that we should not mistake the the trees for the forest and that we should rely more on reform and restructuring methods to resolve problems in a smooth and stable manner, minimizing the use of scalpels. Thanks to the high value of bank licenses, most SMS Banks thus far have resorted to mergers and acquisitions (M&As) to introduce strategic investors and establish new management teams so as to strengthen corporate governance and re-introduce vitality. For example, the Bank of Jinzhou, which previously had private enterprises as the majority of its shareholders, recently introduced the Industrial and Commercial Bank of China, Cinda Asset company and Great Wall Asset company to implement its reorganization program.

On November 6, the ninth meeting of the Financial Stability and Development Committee voted to deepen the reform of small and medium sized (SMS) banks, to improve their corporate governance structures and internal risk control systems, and most importantly, to help SMS Banks to replenishing capital through multiple channels. On November 7, the government allowed urban commercial banks to issue perpetual bonds to replenish capital for the first time. However, SMS banks are being much more cautious this time. Huishang Bank and Taizhou Bank announced the issue of no more than RMB 10 billion and RMB 5 billion worth of perpetual bonds on the same day in order to supplement other tier 1 capital. Meanwhile, the listing of SMS Banks has also been expedited. At present, there are 10 rural commercial banks and 8 urban commercial banks on the A-share market. At the end of October, there were 16 A-share SMS Bank IPOs waiting to be listed on the Shanghai and Shenzhen stock markets. However, the number of listed and scheduled IPOs of SMS Banks accounted for only 2% of the total number of SMS Banks.

The continued liberalization of financial institutions will bring more long-term strategic investment for SMS banks, sparking a new round of M&A activity. Though re-financing (by issuing perpetual bonds) is the most direct way to replenish capital, only those institutions which persist in steady operations, service the local areas and have sound corporate governance can secure regulatory approvals and gain investor recognition and public trust.

But at present, downward pressure on the domestic economy and tough business conditions have pushed SMS Banks to a critical “make or break” point. As stated by Guo Shuqing, Chairman of CBIRC, “financial institutions should not always be kept alive without ever facing death, appropriate elimination is imperative.” Although reform is painful, there is light at the end of the tunnel. Though small in size compared to large banks, regional banks need to work on their core strengths and to service the local real economy. Thus, the differentiated competitiveness of SMS Banks will become more marked in the future.

Automotive

What global auto consolidation has meant for China

The announcement of the FCA-PSA (Fiat Chrysler Automobiles -Peugeot S.A) merger as had the effect of a bomb exploding in an open marketplace. The proposed mega-company, a combination of the above two companies, if actualized, will surpass Hyundai-Kia to become the fourth largest auto group in the world. After a series of moves to reduce jobs, wind down factories and form alliances with former rivals in order to survive the current industry-wide recession, global automakers seem to have decided that consolidation is the most effective solution to the low demand conundrum.

The proposed merger also sheds new light on China’s growth problems. This past October marked the 16th consecutive month of negative growth in sales. Yet, even though a growing number of private car companies are now teetering on the verge of bankruptcy, no large-scale merger and acquisition deals were announced since the start of the slowdown. In fact, the last time Chinese automakers embarked on a merger binge was in 2009 when Chang’an acquired Chang’he and Hafei, while Dongfeng invested in Fuqi (all fit into the profile of large State-owned firms merging with their smaller brethren). A look at CR3 (the market share of the top three auto companies) as a measurement of market concentration of the auto industry shows that China, at 25%, lags far behind Japan which is leading the world at 69% market concentration, followed by the United States at 45%. China’s market concentration rate is even behind the global auto market average which stands at 33%.

Chart: Consolidation progress of Japan’s auto industry

Why is consolidation important? Let’s look at Japan. The country agreed to an open and free market in the late 1970s when foreign car companies were allowed to establish fully-owned entities in Japan. As a result, the domestic car industry was forced to embark on its first wave of consolidation. A few of the domestic automakers, Toyota, Hino and Daihatsu, decided to join forces in order to increase manufacturing capacity, thereby warding off competition from foreign players. Others like Mitsubishi and Mazda opted to partner up with foreign counterparts like Chrysler and Ford.

In the 1980s when the economic bubble burst, Japan suffered from diminishing demand and severe overcapacity. The Auto industry, once again, responded to the slowdown by accelerating its consolidation progress. By the late 90s, one mega company (Toyota) along with a few powerful carmakers had emerged to dominate Japan’s auto market. Automakers had been aware since 2010 that global demand was going to peak. At the same time, market expansion had become more complicated due to a number of business and technology related factors such as an increasingly competitive market landscape, a technology revolution and changing business. So, Japanese carmakers decided to follow strategies that privileged sharing – both of technology and capital. An important part of their strategy as the shared platform, as well as sharing of manufacturing capacities and R&D costs on next-gen technologies and the risks thereof. Through these at time loose, and at other times close cooperation frameworks, the auto industry sector in most developed countries grew from a fragmented industry to a highly concentrated one.

Chinese auto giants are mainly State-owned enterprises and while they have been announcing cooperation programs on mobility and R&D, and on connected vehicles, in the last few years, none of the above-mentioned approaches which are generally viewed as pathways to enhanced competitiveness, have really been followed seriously.

With China’s auto sales in a cyclical decline and the clock ticking on limits to foreign ownership, China’s automakers, especially Stated-owned enterprises, will have resort to drastic solutions to revive their competitiveness.

Energy

The big question about natural gas

While the natural gas supply for this winter seems secured, China's gas demand is growing annually as the government tries to move away from its dependence on fossil fuels. Forecasts show that gas demand is expected to grow at 5% annually for the next decade. But despite the current state of demand for natural gas, falling costs for renewable energy generation and more efficient electric battery projects has given rise to further debates on natural gas. At the heart of these debates lies a big question about where China should focus her efforts to meet its energy needs. Can natural gas be considered a lower-carbon "bridge" fuel during the energy transition period or is it simply a continuation of our dependence on fossil fuels?

Alarming signals

Globally, natural gas productions seems to be running into difficulties. Recently the UK government banned fracking for shale gas extraction over earthquake fears and said it will not support future fracking projects until and unless extraction is proven safe.

In America, General Electric (GE) announced that it plans to demolish a 750MW natural-gas-fired power plant it owns in California this year after only one-third of its useful life. The reason they gave for this is the increasing availability of wind and solar energy at reasonable prices.

Does this mean we will be entering a "peak gas" era soon?

Not just about costs

In the near future it is very likely that the cost of power generation from renewable energy sources will continue to fall significantly while the price for natural gas will only see a moderate decline, if not a rise. Hence, in the years to come renewables are more likely to be cost-competitive than natural gas.

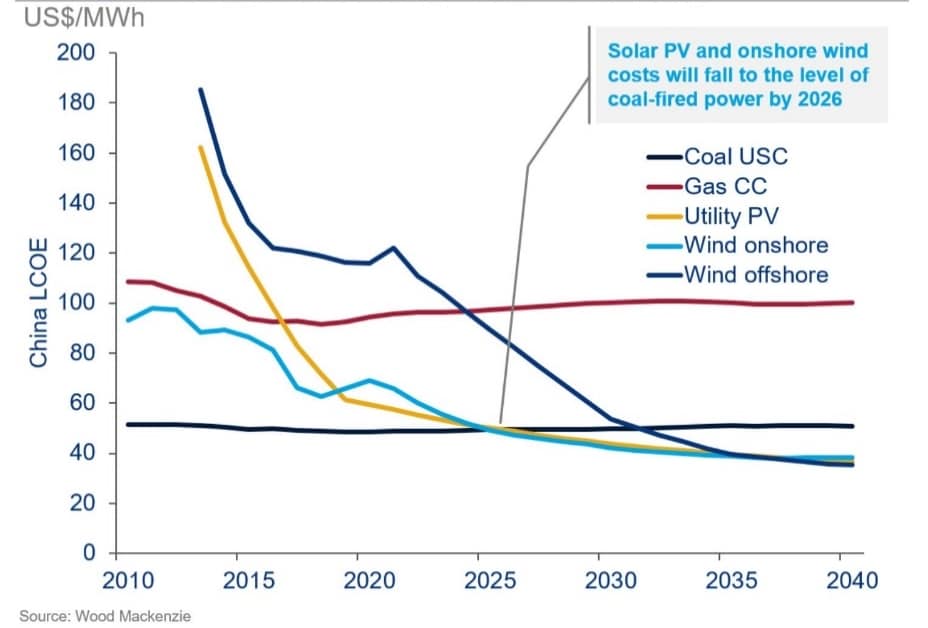

According to the Wood Mackenzie report, the average levelized cost of electricity (LCOE) from solar and wind power is already cheaper than gas-fired power in China. In 2019 the LCOE of China's utility scale solar PV power plants has fallen to $70 per megawatt-hour on an average, while natural gas costs about $90 per megawatt-hour, the second most expensive fuel type after offshore wind.

Chart 1: Average power generation cost (LCOE) trend in China

While renewable energy is the fastest growing segment in the industry, natural gas power plants are needed to provide reliable baseload generation as well as for balancing the grid. For renewable energy to scale up, it’s not just about the cost of the renewable itself, but also the cost of battery storage technology. The cost of “solar + storage” will only be competitive comparing to coal by 2040 when “solar + storage” costs fall to between $33 and $85 per megawatt-hour through declines in battery cost and economies of scale. Before that, solar and wind power generation will continue to require back-up energy sources (and gas turbines remain the cleanest option) for decades to come. In another words, until the time that grid-scale energy storage becomes commercially viable, natural gas will play the key role in providing baseload power and grid balancing.

Also, when considering the likelihood of “peak gas” as a result of competition with wind and solar, we shouldn’t forget that natural gas is not used exclusively for power generation. Natural gas has many more uses than simply providing electricity. It can be used for heating, lighting, cooking, for supplying processing heat in many industries and for propelling vehicles, trains and ships. In China, only 20 percent of gas consumption is power related.

Energy diversity

At present and in the near future, no form of alternative energy can replace coal, given China's huge absolute energy demand. But the need for China to reduce emissions is so urgent that a diversified energy structure which includes fossil fuels, renewables and nuclear energy is bound to emerge soon. This could provide a longer lifespan for natural gas in China's landscape. Most of the analysis and forecasts conducted by international energy organizations do actually foresee at least 20-30 years of rising gas demand in China.