Perspectives

2021 China Outlook

The Deloitte Research Monthly Outlook and Perspectives Issue 61

4 January 2021

Economy

Economy on a roll

2020 will undoubtedly linger long in our collective memories as an annus horribilis of biblical proportions. But as all bad things shall eventually pass, so will the COVID-19 pandemic. As we move into 2021, the Asia-Pacific region can look forward to a better year as the pandemic is brought under control and economic activity gradually revives.

We believe three forces will help shape the regional economic landscape in the coming year:

First, economies will undergo a period of rehabilitation as governments use every policy tool available to get their economies back on track and corporations make the repairs needed to resume normal operations.

Second, we are likely to see a process of rectification across the region. Amid the crisis, some economies outperformed, a testament to their better fundamentals, while other countries that had neglected getting important basics right faltered. Now, there is a greater sense of urgency to address weaknesses that hampered countries’ capacity to absorb and bounce back as fast as possible from unexpected shocks like the pandemic.

Third, several countries in the region are also likely to introduce additional fundamental reforms, directed at producing a new model of economic management and development, to adapt to the substantial changes the post-pandemic world will bring. In Indonesia, for example, this means a more flexible labor market. In China, financial sector liberalization is expected to accelerate as the multi-lateral approach of the Biden Administration will bring heightened urgency.

China: a self-sustaining recovery underway

China's V-shaped recovery after it conquered the pandemic has been nothing short of spectacular. Policymakers got many things right through early and stringent lockdown measures, such as the one in Wuhan on January 23. Contact tracing was highly effective, even compared to star performers such as South Korea, Singapore, and Germany. China also mounted extraordinary campaigns to test people for the virus whenever a new cluster of infections was discovered. A case in point is the mass swab testing campaign of nine million residents within five days in Qingdao.

The government also mobilized resources for the resumption of business. China's strong export performance since Q2 reflects how quickly it was able to resume manufacturing activities and gain from a diversion of export demand from countries whose supply chains remained disrupted. China's almost doubt-digit export growth in September also suggests a global recovery is now gathering pace at a speed sufficient to boost China’s growth. In addition, the strong recovery has boosted consumer confidence, fueled by a buoyant property market.

The US dollar's persistent weakness coupled with interest rate differentials resulted in capital inflows in 2020 (foreign reserves reached USD3.18 trillion in November, up USD63 billion from the start of 2020).

With this success behind it, policymakers are likely to focus on improving the quality of growth, first by addressing the uneven recovery between investment and consumption through more efforts to support SMEs and consumers in 2021. People's Bank of China Governor Yi Gang has also pledged to stabilize leverage after China’s debt-to-GDP ratio rose in 2020, a clear change in Beijing's policy stance of the past two years, which allowed for gradual increases in leverage to generate growth. Yi's remark also suggests there will not be any large fiscal stimulus. Beijing is likely to rely more on the fiscal levers for poverty reduction and other social programs, but stay away from large infrastructure projects.

The biggest potential downsides for China are external, particularly increased frictions with the US. What started as a trade war has since spilled over to other areas, especially technology. Trade will remain a source of friction—the US trade deficit with China did not narrow much over the past two years (shrinking by only 8.5% in 2019 and increasing 5.4% in Jan.-Nov. 2020), virtually eliminating any chance to lower tariffs by a future US administration. Indeed, President-elect Biden has already ruled out reducing tariffs, an implicit gesture that they will be held as leverage. Nevertheless, China has found ways to contain this downside risk. Its policymakers have exercised restraint with the US, for example by limiting the number of American companies covered by Beijing's Unreliable Entity list. Beijing has also wooed US businesses, particularly in financial services. The offer of more progress in market access through licenses and eased ownership restrictions could even be a catalyst for Beijing and Washington to find a new equilibrium in their relationship. If China’s new dual circulation strategy means a wider social safety net and not massive import substitution, China will remain highly attractive to US corporations, who would be a force pressing for better US-China ties. Beijing's efforts to mitigate climate change could also be an area in which the US and China can collaborate.

And finally, simply due to the low base in 2020, we see 2021 GDP growth at about 7.5%. We expect USD to rebound because the three factors that strengthened RMB in 2020 are set to reverse, at least partially. First, relative growth momentum between China and the US will shift. Second, interest rate differentials will narrow. Third, the decline in Chinese outbound tourism, which vastly expanded its current account surplus in 2020, should begin to reverse.

Financial Services

China's open financial sector coming into line with international peers

Since the outbreak of COVID-19 pandemic, the Chinese financial system has provided various support to stabilize the economy and rescue enterprises, which demonstrates its strong ability to withstand pressure.

2021 marks the start of China's 14th Five-year Plan. With the U-shaped recovery of the domestic economy, China's financial system will develop steadily. With the completion of the negative list for foreign investment in the financial sector, the introduction of enhanced governance on China's shadow banking industry and the capital market registration system, as well as the establishment of the regulatory framework for domestic systemically important banks (D-SIBS), we are seeing an open Chinese financial system gradually becoming more international.

Systemically important banking regulation is integrated internationally

Recently, the Measures for The Evaluating Systemically Important Banks was released, which established an evaluation index system of D-SIBs in China from four aspects: size, interconnectedness, substitutability, and complexity.

Since the financial crisis, the concept of "too big to fail" has become the focus of international financial regulatory reform. Since 2011, the Financial Stability Board (FSB) has each year released a list of global systemically important banks (G-SIBs). China's D-SIB regulations have been introduced to prevent systemic risks among banks and to facilitate financial reform and opening up, bringing the financial sector more in line with international regulatory framework and rules. Additional regulatory requirements will later be drawn up and a list of Chinese D-SIBs published. All six State-owned banks and some joint-stock banks are expected to be designated as D-SIBs, and non-D-SIBs (such as urban commercial and rural commercial banks) will receive limited regulatory support in the future. As the non-performing loan ratios of these banks are already high, pressure on their business operations will heighten.

Capital markets boom to accelerate

High-quality development of the capital market is a key task during the 14th Five-year Plan period, which includes comprehensively implementing the stock issuance registration system, establishing a normalized delisting mechanism, and expanding the proportion of direct financing. Backed by the government, China's capital markets are on a fast track of development. On one hand, the government is encouraging outstanding foreign securities and fund institutions to bring their expertise into play in China in the hope of spurring a catfish effect that encourages healthy competition. Holding subsidiaries of investment banks like Goldman Sachs and JP Morgan Chase, and fund manager BlackRock, have been approved. On the other hand, fresh money from China's banking and insurance system, and foreign institutional investors, are continuing to flow into the capital market, which will improve the investor structure and bring Chinese capital market in line with international markets.

When China's capital market matures, it will herald a period of expansion and development for China's securities and asset management industries. Large commercial banks will also support direct financing in the capital market. For its part, regulators will likely issue securities licenses to banks to encourage Chinese commercial banks to improve their competitiveness and compete with international comprehensive banks.

Development of pension’s third pillar expected to accelerate

The Insurance Association's Report on the third Pillar of China's Pension Fund predicts a shortfall of RMB8 – 10 trillion in the next 5 - 10 years. As the aging of the Chinese population accelerates, pension financial reforms are expected to be introduced to ease the pressure on pension insurance expenditure.

China's pension system has three pillars. The first is basic pension insurance, which is dominant and covers nearly a billion Chinese residents. The second pillar, - enterprise and occupational annuities, - has a relatively low coverage of only tens of million of the population. The third pillar, personal pensions including endowment insurance, is still small and has been nascent for some time, developing slowly and providing insufficient support for the elderly. Therefore, China's pension insurance market has huge room for growth.

Authorities are expected to gradually introduce an institutional framework to promote the development of this third pillar, and foreign pension management institutions with good market reputations will be favored by the Chinese government.

Governments are becoming more tolerant of bond defaults

On November 13, 2020, the Baoshang Bank wrote down the principal of its second-tier capital bonds by RMB6.5 billion. Around the same time, some local government SOEs defaulted on their bonds. Both cases reveal that regulators are now amenable to allow bonds to default rather than rescue them.

Baoshang Bank's capital replenishment bonds have incurred losses, and this should enhance risk awareness in China's bond market. The favorable impact on bond pricing thanks to implicit government support is now less certain. Interest rates on capital replenishment bonds issued by small- and medium-sized banks are expected to rise.

Non-financial corporate bond defaults are also expected to increase. Regulators have become more tolerant of defaults, so long as they do not touch the bottom line of systemic risk, and local governments now do not necessarily support financially distressed SOEs unless they are strategic sector players. Investors will be more wary of companies in poor financial shape, especially private sector companies.

Shadow banking supervision continues as new risks are monitored

The COVID-19 epidemic increased the pressure of financial asset defaults, but the overall operations of China's financial system remained relatively stable, and financial markets did not have wild swings. According to the China Banking and Insurance Regulatory Commission (CBIRC), this is mainly due to deleveraging and efforts to reduce the size of shadow banking from 2017 to 2019. By the end of 2019, shadow banking was RMB8.48 billion in its broad sense and RMB3.91 billion in its narrow sense, a significant reduction in China's financial risks.

In early November, regulators halted the Ant Group's IPO and issued a regulation on "online microloans" for public comment. Peer-to-peer online lending falls under the confines of shadow banking. CBIRC Chairman Guo Shuqing said attention should be paid to new risks of "too big to fail", referring to large technology companies with cross-border operations that are involved in various areas of finance and technology. A small number of technology companies dominate China's micro-payment market, which is accessed by the general public and now has all the characteristics of an important financial infrastructure. Attention must be paid to the complexity of related institutional risks to avoid new systemic risks.

Shadow banking and the traditional financial system will continue to coexist. In the current economic and financial environment, every area of shadow banking activity will eventually be brought under supervision, and related risk classifications and provision standards will improve.

Technology

Fast-track development

In the past few decades, emerging technologies have been driving companies to adopt and implement digital transformations. But the COVID-19 pandemic has accelerated the development of technology in unprecedented ways. Video conferencing, for example, has changed from a form of work communication to a daily essential this year. Looking ahead to 2021, we expect Sino-US tech disputes to ease somewhat on the political side, but commercial competition and the fight for tech supremacy will continue. The technology industry will continue to flourish and foster digitalization in every industry. Cloud and intelligent edge computing will become a critical infrastructure and virtual reality development by enterprises and in education will accelerate. We also expect digitization in emerging industries, including the commercialization of sports data.

Gaining an intelligent edge

We predict that in 2021, global market for intelligent edge will expand to USD12 billion, growing at a CAGR of about 35%. Expansion in 2021 will be driven primarily by telecoms providers using intelligent edge in their 5G networks, and by hyperscale cloud providers optimizing their infrastructure and service offerings. Well-capitalized leading companies will establish use cases and best practices that will make it easier for companies across multiple industries to attain intelligent edge capabilities. By 2023, 70% of the enterprises could be running some data processing at the edge.

In China, intelligent edge has gained traction in sectors such as industrial internet, smart city, and connected drives. Smart city construction requires a fusion of many types of computing, and 5G intelligent edge can meet the requirements of smarter city application scenarios due to its larger bandwidth and lower latency than other networks. 5G intelligent edge will also make the connection of vast numbers of low-cost, small sensors possible, facilitating extensive urban data decision makings and governance.

Cloudy with a chance of clouds

It would have been no surprise to see cloud spending drop a few percentage points this year, given spending reductions in multiple areas triggered by the COVID-19 pandemic and the resulting global recession. Yet the cloud market has been remarkably resilient. The likely reason: COVID-19, lockdowns, and work-from-home increased demand. We expect cloud revenue growth to remain at or above the 2019 level (i.e. >30%) from 2021 to 2025 as companies move to the cloud to save money, become more nimble, and drive innovation.

In China, against the dual impact of new infrastructure projects and the pandemic, online office, healthcare, education, and e-commerce cloud use has continued to grow as various industries are moving to the cloud. Cloud computing is also important in China's digital transformation. As data transmission and storage demand rise, enterprises' data calculation requirements will rise, too.

From virtual to reality

The VR market is heating up as immersive technologies gain ground in enterprise and education. In 2021, global sales of VR headsets will double from 2019's level, as will sales of related software and services. Enterprise and education extended reality (XR) headset sales will grow, but for now are likely to continue to represent a minority of overall spending on digital reality projects compared to software, development, content, and services. Over time, however, hardware will grow as a percentage of the project value, as most other costs are upfront whereas headset demand increases as pilot digital reality projects enter full deployment. If enterprise headset sales follow the same trajectory as several other workplace devices did in the past, this would herald an even more substantial boost.

China is now the world's most important producer of VR headsets, and product shipments by companies such as Xiaomi lead the world. The VR consumer market has vast product opportunities across games, entertainment, and film, and its business model is maturing. In 2021, 5G will enable VR technology to be applied in a wider range of sectors.

Technology and the business of sports

From cricket to hockey, and baseball to basketball, the digital transformation of sport is in full swing. Clubs, teams, leagues, broadcasters, venue operators, and athletes increasingly see the value in analytics and are working to realize that value. Technologies such as computer vision, machine learning, advanced wireless connectivity, and wearable sensors are transforming how athletes train, compete, and manage their careers.

The hyper quantification of athletes can provide them with more efficient training, enhance their competitiveness, and increase the likelihood that star athletes stay healthy—benefits that, as sport organizations well know, can lead to higher attendance, more sponsorships, and increased viewership. What is much less clear is how this digital revolution can create new revenue streams for teams, leagues, and players themselves. KOK Pro Boxing in China, for example, has not only launched a new league system, but also formed a communication matrix with its live stream platform, and is using big data as an important support for event development, brand promotion, and marketing interaction.

Although there are innovations in smaller sports, many major sports leagues are just starting to test the water on ways they can monetize players' biometric and positional data, as other leagues even ban the commercialization of player data. There is still much to be done to establish clear data ownership policies, to provide equitable revenue distribution, and to ensure player protection. But the potential for monetizing player performance data is so great that it will likely encourage all parties involved to begin addressing these concerns.

The start of the 8K wave

8K’s core attraction for consumers is an option to the future of video, and it will be appealing to buyers for emotional as well as rational reasons. Owning an 8K screen offers the prospect of enjoying movies and TV programs in the best possible quality in terms of pixel density, color range, screen brightness, and sound. It opens up the possibility of showing the next-generation 8K video games on the best available screen. It also gives consumers the option of using large TV sets in new ways. They will no longer be just for watching video content, but could also be used to display digital wallpaper or, for people working from home, productivity tools.

In China, from a policy perspective, national and local policies for 8K have been introduced gradually. The development of the ultra-high-definition video industry and its application in related fields are being promoted on the basis of "4K first but 8K as well". From a technical perspective, the rapid construction of 5G networks provides larger bandwidth and higher data transmission to support 8K TV video transmission; meanwhile, content conversion through the development of chip technology and AI algorithms provide the content support for 8K TV. On the demand side, as incomes and consumption in China continue to rise, they will drive consumers' acceptance of the higher prices of 8K TVs. In addition, the launch of pilot programs for major sporting events, international conferences, and the broadcasting of 8K videos, will stimulate consumers to buy 8K TVs.

Automotive

Shifting Gears

As the world's largest vehicle market, China will continue to lead the global auto industry's recovery from the pandemic. According to the China Association of Automobile Manufacturers, China's vehicle sales are likely to reach 25.3 million units in 2020, including 20.2 million passenger vehicles and 5.1 million commercial vehicles. In 2021 we expect sales to rise 4% to 26.3 million vehicles as consumers continue to prefer mobility in private vehicles over public transport.

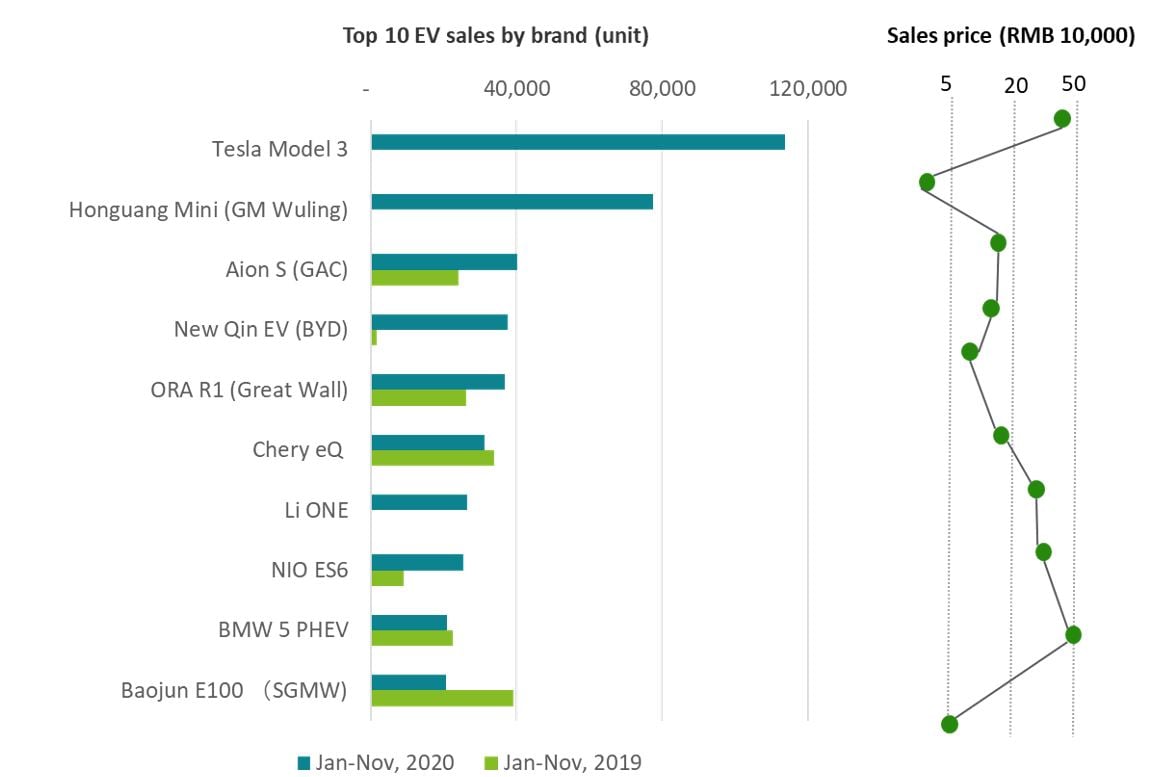

Rise of high-end electric vehicles

Driven by policy support and consumer demand, sales of new energy vehicles (NEVs) surged 105% to 200,000 in November, the fifth consecutive month of growth. NEVs include battery-powered electric vehicles, plug-in petrol-electric hybrids, and hydrogen fuel-cell vehicles.

Two brands top the list. Sales of Tesla's Model 3 reached 113,655 vehicles from January to November, followed by Hongguang Mini with 77,370 cars sold. However, the two brands are adopting very different approaches. Tesla's Model 3 costs about RMB270,000 - 420,000, mainly targeting buyers in wealthier cities. The Hongguang Mini, an EV under GM's local Wuling brand, costs RMB 30,000 - 40,000, designed primarily for consumers in smaller, less affluent cities.

The popularity of Tesla's Model 3 shows the potential for high end EV adoption in China if automakers can produce EVs that inspire confidence in their safety, range, and convenience.

Inspired by Tesla's success, domestic mainstream automakers have started launching high-end EV brands, including BAIC New Energy's ARCFOX, Dongfeng Group's Lantu, and GAC's Aion. SAIC Group and Chang'an Automobile are also planning to build high-end EV brands.

Chart: Potential of high-end EVs

Software defining vehicles

Against the backdrop of electrification, software, AI, and 5G are reshaping the auto industry, from how vehicles are made to how consumers experience them.

The vehicles of the future will include software-defined computing architecture built on AI driving platforms. This means consumers will not only buy the car itself, but also its software functions, including autonomous driving, entertainment, and networking.

Tesla is bringing software functions to its cars, making then extendable platforms. NVIDA is partnering with Mercedes-Benz to make its fleet perpetually upgradeable starting from 2024.

Domestic brands are also promoting software-defined, value-added services. SAIC Motor has set up a software center to accelerate the upgrading of autonomous driving and mobile services by developing a unified data platform. NIO Pilot service is divided into a RMB15,000 select package and RMB39,000 full package. The select package includes common functions such as adaptive cruise and road automatic maintenance while the full package includes additional automatic auxiliary navigation driving and other functions.

The challenges remain for domestic auto makers as their on-board electric architecture are still evolving. Software unlocking services, other than autopilot, are rare and official upgrades remain dominated by hardware tweaks.

We expect EV adoption to continue to grow in 2021 and software-defined vehicles to herald a turning point from which traditional vehicles become high-performance, upgradable computing devices.

Life sciences and healthcare

A year of policy-oriented e-medicine development

Changes in the life sciences and healthcare industry in China are mainly reflected in the industry chain transformation as a result of accelerated digitalization. In 2021, "Internet + Medicine" transformation will become even more important, bringing about increasingly personalized and innovative consultation and treatment. In addition, a series of actions by the Chinese government have shown its desire to deepen and strengthen healthcare system reform, which will benefit innovative biotech and pharmaceutical companies.

Overall, we believe there will be more innovation and consumption upgrading in medical services in 2021.

The key changes in 2020 took place in innovation and digital upgrading, policy reform, a changing external environment, and demand growth in the post-pandemic era.

- Innovation and digital upgrading

The COVID-19 pandemic triggered an acceleration in healthcare digitalization, transforming the whole industrial supply chain, particularly through telemedicine, digital health monitoring, and e-pharmacies. Moreover, "5G + Healthcare" has become a trend and will be an implementation priority in 2021. The combination of 5G technology and healthcare services is expected to help ease the shortage of healthcare professionals through clinical data consolidation, and enhance the user experience, especially after integration with mobile terminals.

- Policy reform: to achieve industrial standardization and normalize volume-based procurement (VBP) program

The healthcare industry in China has been moving towards standardization since 2009, but the practice accelerated in 2020, driven by new policies and the active involvement of government agencies, including the National Health Commission of China, National Medical Products Administration, and National Healthcare Security Administration (NHSA).

Standardization has two main elements:

- Quality management: via a more comprehensive and complex consistency evaluation process to strengthen the supervision of generics and biosimilars, and to direct increased attention to First-in-Class innovative drugs.

- Medical insurance: via the centralized procurement and VBP programs for prescription drugs and medical devices

- External environment a new opportunity for medical export and CXO (CRO/CMO/CDMO) business

China's export trade, including for medical supplies and Active Pharmaceutical Ingredients (APIs), was heavily impacted by China-US trade tensions. With the Regional Comprehensive Economic Partnership (RCEP, hereinafter) trade agreement which was recently signed, we predict China's medical export trade business will have ample space for rapid growth with substantial tariff reductions between China and Japan, and China and ASEAN. Furthermore, as India is now securing internal API demand during the epidemic, more API orders will be transferring from India to China gradually, which will drive China’s API business growth in 2021.

Also, as China emerged out of the pandemic relative unscathed while many countries were still struggling, China has become one of the top choices for medical outsourcing services, creating a boom in China's CXO (CRO/CMO/CDMO) industry in 2020.

- Consumer demand growth due to increased health awareness in the post-pandemic era

As one of the leaders of the COVID-19 pandemic recovery, China has already entered the post-pandemic era in 2020. The increased health awareness on the part of its citizens will boost healthcare industry growth. We predict demand will increase for preventative medical products including vaccines and medical services like early-diagnosis.

Opportunity: Internet + Innovation will bring impetus to healthcare industry in 2021

The COVID-19 pandemic prompted rapid development of digital healthcare in China in 2020, and stable growth is expected in 2021 towards personalized medicine. With 5G technology becoming more mature, it now lays a strong foundation for the informatization and digitalization of China's healthcare industry. The government released two digital healthcare development policies in 2020, which will provide substantial impetus to the development of e-health in 2021.

Table: Comparison of telecomm technology used in the healthcare industry

Performance |

Wired LANs |

Wi-Fi 6 |

4G |

5G |

Terminal speed |

>1 Gbps |

Wi-Fi 6 can reach 9.6 Gbps |

0.05-0.1 Gbps |

0.1-1 Gbps |

Latency |

0 |

≥100ms |

10-100 ms |

<1ms |

Connection density |

Restricted by port and transfer speed |

Wi-Fi 6 has four times the efficiency of previous versions in high-density environments |

<10,000/km² |

<1 million/km² |

Applicable scenarios |

Equipment for in-hospital tests and treatment, etc. |

Wearable, portable medical monitoring equipment |

Online medical consultations |

All applications and 5G ambulances, telemedicine, telesurgery, etc. |

Maturity |

Widely used in daily life and production |

Wi-Fi 6 was finally confirmed in Q3 2019 |

Widely applied in daily life |

Activated in 2019, Release 16 standard confirmed in 2020, to be commercialized in 2021 |

Mobility |

Fixed |

Fixed |

≤350km/h |

≥500km/h |

Source: Ericsson, 3GPP, Huawei, Deloitte Research

Considering many countries are still struggling with the pandemic, we expect further growth in 2021 for China's contract research organizations and contract development and manufacturing organizations, as well as API export businesses.

Based on industry trends in 2020 and the outlook for 2021, companies are set to shift from general innovation to high-value innovation. Additionally, medical services providers will garner increased attention in the post-pandemic era, as digital healthcare platforms, chain-pharmacies, and medical services providers will have room to grow.

Challenge: market is shrinking and prices are tumbling since VBP adoption as barriers remain to e-medicine information integration

The NHSA started to implement the VBP program for prescription drugs in 2019, followed by VBP program for medical devices in 2020. As a result, market for items included in the VBP programs shrank considerably, and in 2021 many companies that fail to win bids will see their market share fall off the cliff. As the NHSA aims to devote more effort to promoting VBP in the next few years, it will be challenging for many pharmaceutical and medical device companies in China to survive and manage their portfolios, making it imperative to transform their business models.

Meanwhile, amid the fast growth in digital healthcare, how to consolidate clinical data across different institutions and parties while safeguarding user privacy and information security will be a challenge for providers. Hence regulatory changes will be the key factor.

Energy

Balancing the post-COVID recovery and low-carbon growth

In 2021, China will strive to balance its recovery from the COVID-19 pandemic with the need to pursue low-carbon growth.

China's energy consumption is estimated to have declined by just 0.1% in 2020 due to COVID-19, but could increase by 3.6% in 2021 driven by the country's post-pandemic recovery efforts. High-carbon sectors such as energy and infrastructure will continue to play an important role in driving the economic recovery.

On the other hand, China has postponed scaling back subsidies for renewable energy. For instance, the government restored the new energy vehicle subsidy that was cancelled in 2019 and extended this to 2022. In September, President Xi Jinping announced that China would target carbon neutrality by 2060 and peak emissions by 2030.

High-carbon energy has an important role in post-COVID recovery

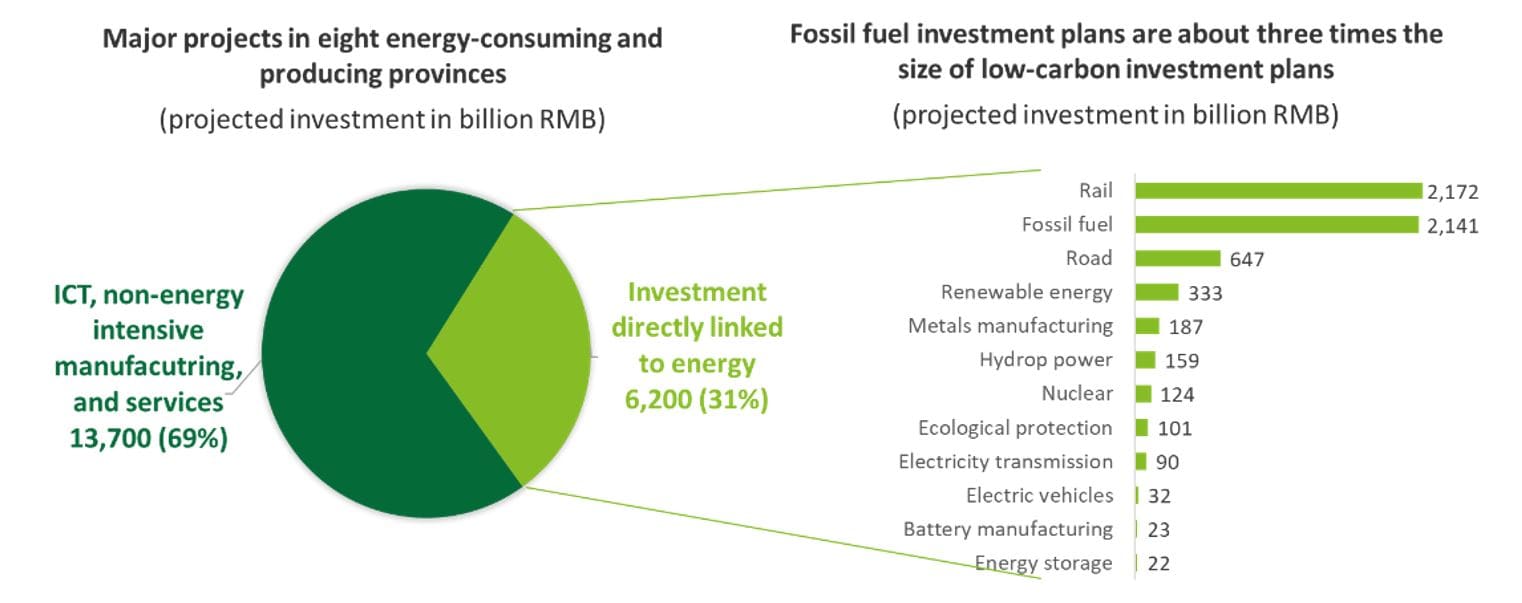

China’s main energy-consuming and producing provinces are directing vast sums of money into fossil fuel projects to stimulate the post-COVID recovery. Although final approval for these projects is not guaranteed, they reveal the priorities of decision makers at provincial governments and SOEs

According to a Carbon Brief analysis of 4,348 listed projects across eight Chinese provinces that account for half of China's CO2 emissions, RMB6,200 billion of investment is directly linked to energy and energy intensive sectors. Of this, RMB2,141 billion is earmarked for fossil fuel projects, but much less is devoted to low-carbon energy, with RMB333bn for renewables, RMB124bn for nuclear, and RMB77bn for electric vehicles, batteries, and energy storage.

Some regions are choosing high-carbon energy and infrastructure as the drivers of their economic recovery. This will make it difficult to reach peak CO2 emissions before 2030 and achieve carbon neutrality by 2060.

Technology innovation tops SOEs' agenda

China needs to balance its post-COVID recovery and low-carbon development. This will be a huge challenge. Fossil fuel will still have an important role, which suggests technology innovation, especially low-carbon solutions, will be the key to this strategy.

Technology innovation is a prominent theme of the 14th Five-year Plan period (2021-2025). The State-owned Assets Supervision and Administration Commission (SASAC), China's state-assets watchdog, regards technology innovation by SOEs as essential.

In April 2020, more than 200 State-owned science and technology enterprises were selected to demonstrate science and technology reform. China's three oil majors, two grid companies, and big five power companies are all on the list. The selected energy SOEs are required to explore innovation, make technological breakthroughs, and build replicable innovation models. SASAC also plans to formulate policy measures to promote innovation among SOEs. All of the above suggests technology innovation will be a KPI for SOEs, affecting everyone from top leadership to employees. Sinopec has already created a six-person new energy office within the group’s planning department and established an R&D center with 48 staff.

Emerging low carbon solutions

For over a decade, China has had the world's most carbon capture, utilization and storage (CCUS) pilot projects. It has an opportunity to deploy CCUS as a priority for its energy sustainability, while boosting other strategic sectors such as electric vehicles, smart grids, and hydrogen.

Chinese oil majors have prioritized CO2-EOR (enhanced oil recovery) development and conducted pilot projects across China. In the power sector, 60% of China’s 3,000 coal-fired power plants are considered young at about 10 years old. Their live spans will extend beyond 2030, making them suitable candidates for CCUS.

While current projects in operation and under construction are small in scale, future projects will be much larger. As CCUS develops from demonstration to application, national policies and carbon trading will be needed to replicate China's success in solar and EVs.

Hydrogen needs to become another pillar of China's green revolution. Wood Mackenzie estimates China's hydrogen production will grow five-fold by 2050, equally distributed between green and the fossil fuel-based production, and paired with CCUS. Given China's large heavy industry and machinery sectors, meeting its pledge to become carbon-neutral would be extremely challenging without these emerging low-carbon solutions.

Logistics

Achieving breakthroughs via innovation, integration and efficiency improvements

The evolution of China's logistics industry is accelerating

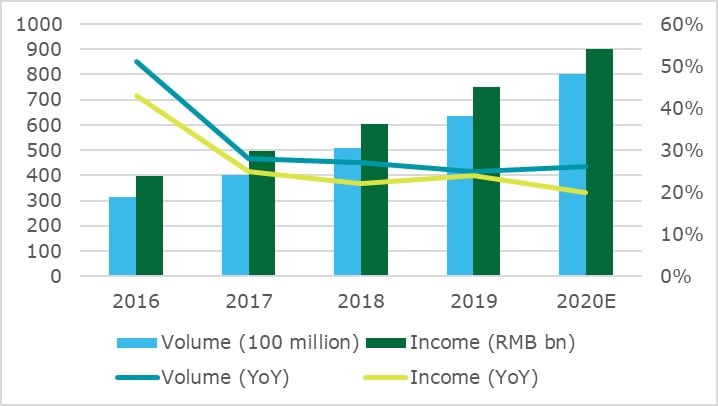

The growth of online consumption has led to an explosive growth in logistics industry. As COVID-19 affected offline operations, consumption has gradually shifted online. According to the National Bureau of Statistics, online retail sales increased 16% year-on-year in January-October 2020 period, accounting for 24% of total consumer goods retail sales. The growth of online consumption has prompted the expansion of the logistics industry.

As of October, the 2020 revenue of express delivery businesses has reached RMB691 billion, with 64.4 billion items delivered, exceeding revenue and volume in the whole of 2019. By the end of this year, express delivery revenue is expected to have reached about RMB900 billion, with delivery volume of about 80 billion items, spotlighting the vitality and huge potential of China's express delivery market.

At the same time, the Chinese government is constantly issuing laws and regulations to strengthen the standardized development of the logistics market, designed to force out some transport enterprises that lack core competitiveness. China's logistics enterprises will continue to move towards scale, technology, and specialization.

The evolution of the express delivery market since 2016

Chinese logistics companies to focus on and implement "two in and one out" strategy

- With increasing international trade, overseas express delivery has become a new challenge for enterprises. In March 2020, the State Post Bureau proposed a "two-in-one-out" strategy (with "two-in" being parcels entering factories and express services entering villages, and "one-out" enterprises delivering overseas) to further improve logistics network service capabilities. Overseas deliveries are now a development priority for express delivery companies. Meanwhile, RCEP agreement signed in November by ASEAN plus countries will abolish trade barriers among ASEAN countries, which will spur the development of export trade and bring massive development opportunities for China's third-party international logistics industry.

- National policy increases logistics coverage; last-mile links the core value of express delivery. In April, the State Post Office announced The three-year action plan for express delivery into villages (2020-2022). With the development of online consumption, demand for rural express service is increasing. Some 96.6% of the country's towns have express stations, and 26 provinces or cities have achieved full coverage. COVID-19 accelerated the development of contactless distribution. As diversified delivery needs continue to emerge, the logistics industry must address the relationship between new delivery models and current service standards, to meet growing service demand.

- From consumption to manufacturing—ToB logistics will develop rapidly. With the increase in high-end manufacturing enterprises, ToC business will largely shift to ToB. The greater dimensional requirements for logistics and transportation of high-tech products will also promote the development of ToB logistics. Central and local governments have increased financial support for the construction of logistics facilities such as dedicated railway lines and multimodal transport stations, and promoted dedicated railway lines entering ports and large industrial and mining enterprises, to speed up the medium and long-distance transportation of bulk cargo. This infrastructure will boost transport capacity for large goods.

Innovation, integration, and efficiency enhancements will become the focus of enterprise development

- Digital upgrading is accelerating, and logistics companies need to accelerate their realization of comprehensive intelligence. Digitalization has been a focus of logistics enterprises in recent years, and is key to seizing future opportunities to drive the complete intelligent transformation of supply chains. The development of logistics enterprises will focus on emerging technologies such as 5G for intelligent logistics reform, promoting new technologies including robots, intelligent warehousing, and automatic sorting, and improving production logistics automation, digitalization, and intelligence.

- Innovation, integration, and efficiency enhancements the new development goals. Logistics enterprises should carefully analyze their own characteristics and those of their industry, build differentiated core competitiveness, and use technology to achieve the key objectives of innovation, integration, and efficiency. This means creating services that meet customer needs through reform and innovation; integrating social resources and using crowdsourcing for mutual benefits; and establishing flat organizational structures to improve the response speed of cold chain logistics platforms.

Retail

Demand side reforms to spur domestic consumption expansion

As 2020 is coming to an end, China is proposing domestic demand side reforms to shift towards consumption-driven demand against the backdrop of “dual circulation” policy. Improving income distribution systems, introducing measures to promote consumption, and improving the consumption environment will be starting points of demand side reforms. For example, to improve income distribution systems, China could reform its tax and social security systems to increase the spending power of low-income groups. Driven by macro policies, new consumer demand and technological innovation, China's consumer market is expected to witness several development opportunities in 2021:

- Post-COVID consumer market driven by traditional Chinese style and culture, healthier lifestyles, and intelligent technology

Domestic products will continue to drive the growth of China's consumer market. In the beauty sector, for example, cosmetics and skincare products have become daily necessities rather than discretionary items. Since April 2020, sales of prominent cosmetics enterprises (annual revenue >RMB5 million) has continued to expand. Three factors have boosted sales of domestic cosmetics brands: thematic trends popular among the post-90s and post-00s generations, the success of livestreaming e-commerce and community influencer recommendation APPs, and high quality products at affordable prices.

In addition, luxury and wellness-themed small household items are becoming a new growth driver in the household appliances segment, thanks to social distancing and consumption upgrading. In 2021, as Chinese consumers’ preferences move towards more premium, greener, and healthier products, demand for higher quality products and services is bound to rise. And amid the further deployment of 5G, artificial intelligence, and Internet of Things applications, premium and smart home appliances will enter a phase of rapid development.

- New business models arising from technology and policy dividend to usher in new era of development

In 2021, e-commerce cross-border trade will grow rapidly riding on the tailwind of the “dual circulation” policy, RCEP, and demand side reforms. In cross-border e-commerce imports which meet domestic consumption upgrading needs and pull demand forward, Chinese consumers will purchase high-quality imported goods including cosmetics and high-end household appliances from Japan and South Korea at more favorable prices under RCEP. For e-commerce exports, RCEP will simplify customs procedures, improve logistics, and reduce production costs. At the same time, relying on the advantages of domestic supply chains, China's e-commerce exports to Southeast Asia will develop rapidly in 2021.

With the rapid implementation of 5G technology, related retail business scenarios will keep evolving. Compared to offline shopping, online shopping lacks immersive experiences due to geographical constraints. With the support of 5G + 8K technology, consumers will be able to obtain, quickly, clearly, and intuitively, product details, getting the same "what you see is what you get" experience that they do offline. With the support of 5G technology, new online sales models, including livestreaming e-commerce and product review platforms, will improve consumers' online shopping experience.

- ‘Last mile’ as the key scenario for brick-and-mortars

In "new normal" of pandemic mitigation measures, physical stores will not only accelerate their omni-channel strategies, but also promote the development of business models that match consumers' spending habits. Apart from supermarket O2O, a fast-growing new model for supermarkets during the pandemic, more types of format at physical retail stores, including convenience stores, specialty stores, exclusive stores, and even shopping malls, will build up customer attraction channels and membership mechanisms with the help of social media platforms such as WeChat, mini program APPs. New omni-channel strategy and last-mile community concepts will create comfortable, efficient, and integrated online and offline shopping experiences.

China's consumer market will also face challenges. First, the pandemic will continue to have an impact. If a resurgence occurs, this would harm China's economy and consumers' enthusiasm for consumption could be hit again. Second, new models of rapid growth need to be regulated and managed. Since the pandemic, new business models have showed some weaknesses, including poor quality products sold via livestreaming e-commerce. In addition, monopolistic behavior such as price discrimination and subsidies will face more stringent policy supervision. That said, China is set to embrace an integrated retail market in a post-COVID new normal.