Perspectives

The Deloitte Research Monthly Outlook and Perspectives

Issue 62

9 February 2021

Economy

Financial risk prevention a higher priority

To say the Chinese economy is on a roll is an understatement. GDP of Q4 of 2020 came in at 6.5% which putting whole year growth rate at 2.3%. This strong growth of recovery which was not just being propelled by investment (up 2.9% in 2020) has been achieved despite PBOC's relatively hawkish stance; by last December, China's exports have posted 7 consecutive growth while imports began to perk up since last September, suggesting both a broadening-out external demand and a rebounding domestic demand.

Long-anticipated cuts of reserve requirement rates for commercial banks have not panned out as long term interest rates started to edge higher from last summer. Meanwhile, the RMB has gone from strength to strength on the back of widening interest rate differentials between China and the US. This means the PBOC has kept its powder dry should the economy face another external shock in 2021. In our view, growth momentum is likely to persist even with recent "surge" of cases in Hebei.

Hebei's proximity to Beijing has naturally made the Central Government wary, especially with the Chinese New Year around the corner. But our sanguine baseline scenario of the economy (not just China) rests on successful rollout of vaccine in both developed countries and most emerging markets, behavioral adaptation of firms and consumers to various forms of lockdown and policymakers' learning. For example, in Shanghai two weeks, it took merely three days for the municipal government to contain cases (22 in total) with minimum disruptions of economic activities. Of course, Shanghai represents a high bar in terms of governance but the society as a whole is gradually taking the virus in stride. That is why we continue to hold the view that Q1 of 2021 GDP growth is likely to be explosive mainly due to base effect. For most people who could not go back to their hometowns for the Chinese New Year, the most important holiday in Chinese culture, impact can't be quantified with dollars and cents. However, such personal sacrifice is widely viewed as necessary for greater good. If growth in 2021 (our forecast is 7.5%) is far above trend growth (say 5%, for argument sake), should China take advantage of this opportunity by phasing out the goal of GDP growth.

Whether to phase out this target or even de-emphasize it has been a perennial debate for over decades. As China is well on its way to a moderately prosperous society and has proclaimed the goal of carbon neutrality by 2060, GDP growth target certainly is less necessary. Chief difficulty, for local governments, at least in the short run, is that there are no viable yardsticks as far as KPI is concerned. So all in all, we expect GDP growth target to be somewhat de-emphasized despite the fact that 2021 will see celebration of the centenary of the Communist Party of China.

In fact, recently resurfaced discussion on GDP growth target within the PBOC has suggested that policymakers are precisely moving to the direction of a better quality growth, a welcome development. Better quality growth also means more vigilant stance taken by policymakers towards financial sector risks. More specifically, policymakers continue to stick to notion of "homes are shelters not tools of speculation". In four first tier cities except Guangzhou, targeted measures of restricting housing demand mainly through stringent loan provisions and tighter quotas have been unveiled this year. Shenzhen's sizzling real estate market has been a headline grabber in recent years while anecdotal evidences have indicated that Shanghai's property market has quietly posted a high double digit gains in terms of prices since last summer. Policymakers' concerns over asset bubbles are warranted given that housing affordability has been an acute social issue for years. In Beijing, firms are prohibited to offer schemes of prepaid rents for a period of longer than three months. The rationale is to prevent Ponzi scheme and fraud. In the long run, the best way for address housing bubbles is to increase land supply in the vicinity of major cities; and ultimately relaxed restrictions of resident registration system will make housing more available and affordable. The dilemma is that policymakers are equally concerned about sudden price declines should interest rates are being hiked due to an inflation shock. So the policy bias is to have rising incomes "deflate" housing "bubbles" in the long run.

A recovering economy also allows China to turn the table on the international front assuming the Biden Administration will be preoccupied by domestic issues (covid reliefs, vaccine rollout and stimulus) for now. On the China strategy, comments so far from key cabinet members of the Biden Administration have indicated that there are no major differences between democrats and republicans but President Biden would prefer to work more closely with allies in dealing with China. However, given that US's return to CPTPP is unlikely to transpire at least in first couple of years of the Biden Administration much due to lack of domestic support, most Asian countries will try their best not to choose sides. In the short run, all eyes will be the likely call between two top leaders of China the US in the run up to the Chinese New Year. On the 4th of February, President Biden has delivered his foreign policy speech in which China was dubbed as a competitor while Russia, as an adversary, suggesting that the Biden Administration is likely to seek collaborations with China amid an entrenched technology rivalry.

Financial Services

Banks' KPI will be broadened

At its annual work conference on 4th January 2021, the People's Bank of China (PBOC) called for "deepening of supply-side structural reform as the cardinal line, and reform and innovation as the fundamental driving force". As regards further regulatory reform for banks, this accords to the Central Economic Work Conference (held in December 2020), and primarily centres on requiring commercial banks to focus on servicing national development goals and promoting the balanced development of the finance and real estate sectors along with the real economy.

The new "performance evaluation measures" for commercial banks will emphasize the “servicing of national strategies” principle.

An updated version of the Ministry of Finance’s ‘Measures for Performance Evaluation of Commercial Banks (new version)’’ went into effect on January 1, 2021. In this, more emphasis is placed on servicing the national macro strategies of both the real economy and the micro economy. Banks and bank personnel will be evaluated on the basis of their capacity to service national macro strategies and their remuneration will be based upon the results of this evaluation. Compared with the previous 2016 version, the new version has three significant differences:

- The new version looks outwards, focusing on how banks should service key areas in the economy and strengthen weak links. It also focuses more on economic benefits, shareholder returns and so on. The old version, in comparison, had a narrower outlook, focusing more on the bank's own performance (such as earnings, operations, assets, and solvency).

- The new index system is more far-reaching. For example, the introduction of economic value added, per capita net profit, per capita taxes paid and other indicators will guide banks to focus on innovation, speed up transformation (of banks), and enhance value creation.

- The compensation level of bank executives, the formulation of total salary and the assessment of the leadership team will be linked to the new system of evaluation. The mechanism of "matching compensation with performance and paying equal attention to incentives and restraints" has also been clarified and elaborated. Violations will result in point deduction and demotion.

Under the new development paradigm of domestic and international dual circulation, the new method of performance evaluation of commercial banks will help strategic emerging industries and the real economy to secure credit and will lead to a decline of the real interest rate.

Regulations on the real estate sector tightened

On November 3, 2020, the 14th Five-Year Plan and the Vision 2035 Proposal promulgated the "promotion of balanced development of finance, real estate and the real economy" - the first time both finance and real estate sectors are simultaneously referenced, indicating that the government will treat future real estate regulation and strong financial supervision on an equal footing. In other words, the government will strengthen efforts to curb real estate bubbles and debt accumulation and real estate supervision will be much more stringent over the next five years.

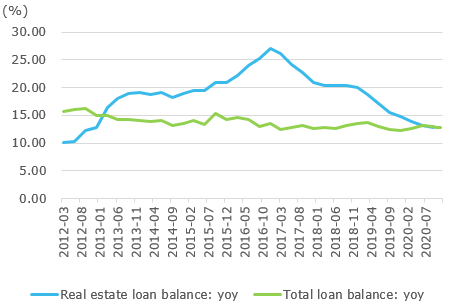

On December 31, 2020, Chinese regulatory authorities formally issued a document establishing the implementation of a unified management system for real estate loans given by Chinese-owned banking and financial institutions, effectively setting a ceiling on the proportion of real estate loans and personal housing loans given by large, medium- and small-sized commercial banks, respectively, and setting up a 2-4-year transition period for banks that currently exceed this ceiling. This brings the Chinese financial sector in line with international standards as on the international regulatory front, the IMF also utilizes such unified management indicators to determine whether the property market is sound.

The substantive supervision on real estate sector financing is expected to affect the sector in several ways. First, real estate loan growth will continue on a downward trajectory. In January 2021, the PBOC stated that the growth rate of real estate loan balances had fallen for 29 consecutive months, and that new real estate loans accounted for only 28% of all loans in 2020, down from 44.8% in 2016. Second, commercial banks' credit funds will be invested more in non-housing related sectors such as national strategic emerging industries and small and micro-enterprises. This shows that credit growth in the non-housing sector will be, at the very least, growing at a faster rate than housing sector credit. Third, the real estate sector will have more supply side reform in the near to medium term, as small- and medium-sized housing companies encounter greater difficulty in maintaining liquidity as debt pressure increases and financing costs rise. The real estate industry will gradually enter a phase of substantial stock integration, and pressure to consolidate will also increase.

To sum up, in 2021, measures related to the supply-side reform of the financial sector will speed up. The performance evaluation of commercial banks and the reform of real estate financing supervision will enable banks to better support the development of key areas of the economy. Under the new paradigm, banks need to actively innovate, accelerate digital transformation and build digital finance platforms in order to optimize their credit structure and enhance their operational efficiency and value creation.

Retail

Potentials of rural markets still to be tapped

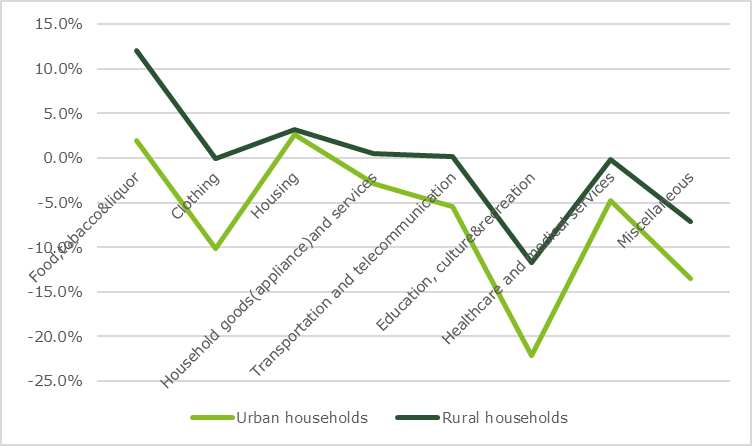

The 2020 annual data of China's consumer market, released by the National Bureau of Statistics in January, showed that consumption became the primary driver of GDP growth in the fourth quarter of 2020. Previously, consumption negatively impacted the GDP in the first half of the year, largely due to the big drop in service consumption caused by the pandemic. In 2020, China's total retail sales of consumer goods reached RMB 3.92 trillion, down 3.8% y-o-y. At the early stage of the pandemic, offline consumer goods and restaurant and catering businesses experienced big drops in sales which dampened the annual growth of total retail sales of consumer goods. However, online sales of consumer goods picked up the slack significantly. By the end of December 2020, the share of online sales of physical goods accounted for 24.9%, up 4 percentage points compared to 2019. In general, the impact of the pandemic on service consumption was significantly greater than that on physical goods consumption. The sales of consumer goods dropped by 2.3% y-o-y while restaurant and catering sales plunged 16.6% y-o-y. In addition, based on the 2020 per capita resident consumption expenditure, residents spending on transportation and communication, education, culture and entertainment, medical and health care and other consumption-related service industries declined to varying extents.

It is worth noting that the impact of the pandemic on the consumption of goods and services in rural areas was significantly lower than in urban areas. The main reasons for this are: first, since rural areas introduced efficient prevention measures at the beginning of the pandemic, infection rates were very low in rural areas. Secondly, unlike city dwellers, the income level of rural residents increased in 2020, with the median per capita disposable income of rural residents going up 5.7% y-o-y. Consumer demand has been going up as a result of this increase in income. Furthermore, with the greater penetration of e-commerce, communication and other infrastructure in rural areas, consumer demand of rural residents can better serviced. IIn 2021, we expect to see greater development of the domestic market in lower-tier cities and rural areas as companies, supported by the government, rush to service the needs of China’s rural residents.

2021 will probably usher in the following trends in China’s retail and consumer goods market:

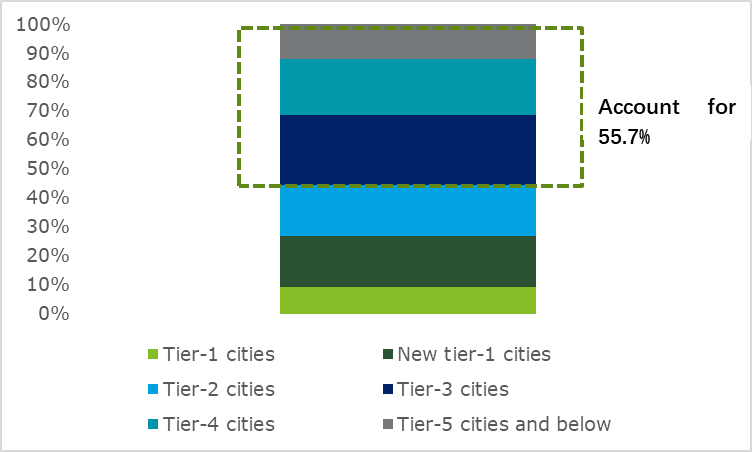

First, young consumers born after 1995 and 2000 will become the main force behind the upgrade of consumption in lower-tier cities. According to Questmobile, by November 2020, 55.7% of mobile Internet users of this age group are residents from third-tier or lower cities. Through mobile Internet and social media touch points, these young digital natives favour personalized services more than the older generations. Furthermore, since the Internet broke the geographical boundaries, consumption preferences of post-95 and post-00 population in cities of all tiers tend to be the same.

In addition to growth in demand in lower-tier cities, online retail and the local lifestyle service sector in Tier 1 cities may experience higher growth in the near term. Due to the high risk of a new outbreak of COVID-19 in winter, local authorities have recommended that people stay put in the cities where they work during the upcoming Spring Festival. Moreover, pandemic prevention and control measures that restrict the size of dinner gatherings and the no-home-cooking lifestyles favoured by young consumers nowadays, will probably ensure that the local lifestyle services in Tier 1 cities will see a large growth in sales. Ready-to-eat meals, food and beverages may also experience a significant sales spurt during the Spring Festival.

In the long run, however, much depends on the success of the vaccine rollout. For example, if vaccines can be rolled out successfully in a short time, China's brick-and-mortar retail sector and discretionary spending will see a quick rebound. However, if the vaccine rollouts slow, new business models such as offshore duty-free and cross-border e-commerce and domestic brands will have larger window of opportunity. At the same time, the new normal under the Covid-19 prevention and control measures will keep accelerating the digital transformation in the retail and consumer market which will enable better servicing of demand and greater penetration of the rural market.

Logistics

Digital transformation is the way ahead

The logistics market continues to grow, and leading companies have built upon their competitive advantages. The COVID-19 epidemic has greatly catalyzed the development of the digital economy and the penetration rate of online retail has shown continuous improvement, giving rise to increased logistics demand. According to the State Post Bureau of China, China's express business volume topped 83 billion pieces in 2020, an increase of 30.8% over 2019 while the business income reached RMB 875 billion, a y-o-y increase of 16.7%. Meanwhile, the penetration rate of domestic and foreign e-commerce increased, as well as cross-border e-commerce transaction volume. Customs statistics show that the import-export revenue of cross-border e-commerce will reach RMB 1.69 trillion in 2020, an increase of 31.1% over 2019. The Covid-19 pandemic triggered a series of chain reactions, including the restructuring of the global supply chain. In addition, the logistics industry is characterized by handling parcels in different sizes and shapes, in small batches, and with high frequency, which set forth higher requirements on their network deployment, inventory turnover and management capabilities during the pandemic. In future, powerful leading logistics companies will benefit from owning a complete logistics network, highlighting their competitive advantages and enhancing their market positions.

The epidemic prevention and control measures have brought new challenges

- At the level of business operations, the continuation of the epidemic in the future may bring about challenges to the development of logistics enterprises in three areas: transportation, personnel control, and cost increases due to COVID-19 related measures such as goods disinfection and personnel safety.

- In terms of transportation, when some COVID -19 medium and high-risk areas are forced to adopt a closed management mode, logistics operations may be suspended in the high-speed roadway off-ramps and airports or controls on cargo flows may be introduced, resulting in a slower cargo delivery cycle. Road traffic restrictions on vehicles will also greatly reduce the delivery rate.

- The second area of concern is personnel control. At present, most deliveries involve in-person contacts, and the health of the distribution personnel is especially important. Although companies have begun to implement a testing-for-work mechanism for delivery personnel, quarantine measures for delivery personnel may cause labor shortages as a large number of employees may prefer to resign.

- Finally, there is the issue of budgeting. The uncertainty of the epidemic has greatly increased the cost of distribution. If it continues for a long time, the high cost of goods disinfection and the rising cost of employee safety may lead to a decline in corporate income and negatively impact further growth.

At the market and industry level, there have been several changes brought about by the implementation of COVID related regulations and these will profoundly affect the development of certain sub-sectors, the cold chain and cross-border e-commerce markets in particular.

- The cold chain market. In the context of the normalization of epidemic prevention measures, cold chain cargo inspection and disinfection are of particular importance. This will have an impact on the newly booming cold chain logistics of fresh food. The cold chain market has grown steadily and rapidly in the past five years. The market in 2020 reached approximately RMB 480 billion, an increase of over 25% from a year earlier. Expansion of cold chain logistics to improve transit and distribution hubs while ensuring safety will be the focus of future development.

- The cross-border e-commerce market. At present, cross-border e-commerce is still facing delays and multiple difficulties in areas such as customs clearance, credit risk, and capital security. The unpredictability of logistics timelines since the start of the epidemic and the impact of order reduction due to economic shocks is also beginning to show. For cross-border e-commerce companies, it is imperative to adjust and optimize the cross-border delivery process to reduce the risk of volatility in export trade.

Digital transformation becomes the ultimate solution.

With the ‘normalization’ of pandemic prevention and control measures, companies must implement a comprehensive digital transformation, and develop new models, new services, and new business formats for the digital economy, in order to obtain digital "immunity" and truly create anti-risk, cross-cycle capabilities. At the same time, huge advancements are being made in digital technology, AI and robotics, and these are constantly being applied (for example low-cost sensors, computer vision, augmented reality, wearable devices, the Internet of Things, robot gripping capabilities, human and robot safety) to the logistics sector. Improving existing digital logistics capabilities, on the other hand, can also create new intelligent functions, which will lead to innovations in the operationality of the logistics industry.

Energy

EU-China agreement comes just in time

The EU-China Comprehensive Agreement of Investment (CAI) creates significant opportunities for the Chinese renewable energy sectors, and, perhaps, a new sweet spot for both parties.

Just in time

A new regulation on the screening of Foreign Direct Investment (FDI) by the EU in place since October 11, 2020 allows Member States to use a national screening mechanism for FDI from outside the EU on grounds of widely defined public order or security.

Under this regulation, Chinese companies, especially State-owned Enterprises (SOEs), are faced with legal and practical challenges when they invest in or acquire European companies in sensitive sectors, including energy production and supply. The regulation followed an intense lobbying effort by Germany, France and Italy, where the majority of China's Europe-bound renewable energy investments are concentrated.

Hence CAI could not have come at a better time. The agreement grants EU better market access and fairer investment in China (i.e. no forced technology transfer, comprehensive transparency rules). In return, the EU allows Chinese renewable investments in the EU, with a 5% cap for each EU member country and a reciprocity mechanism.

How does China's renewable energy sector benefit from CAI? We believe that they will benefit though the expansion of renewable investment opportunities in the EU, through gaining greater access to cutting edge hydrogen-based technology, and by learning from the success and mistakes of EU's policy and technology models.

Expanding renewable investment opportunities

The European Commission launched the European Green Deal with a set of policy initiatives to make Europe climate neutral by 2050. To achieve the goal, the EU needs to mobilise at least 1 trillion Euros in sustainable investment over the next decade.

Given EU's ambitious emission reduction goal and massive investment needs, and with more EU market access for Chinese companies in renewable energy, the Chinese renewable sector is bound to benefit.

Take, for example, the solar energy value chain. Europe is already China's largest export market for solar PV modules and the trajectory is likely to continue. According to PVinfolink data, in the first half of 2020, the Netherlands bought 21% of Chinese photovoltaic module exports while the remaining EU members accounted for less than 10%. With CAI, mainstream manufacturers will have greater access to the EU market.

Prior to the agreement, Chinese wind turbine manufacturers had problems accessing the EU market as local European wind turbine companies already had a solid market share and there were many restrictions in place. After the agreement comes into effect, Chinese companies may be able to enjoy an ease of restrictions in terms of polices, financing and transportation thresholds.

Renewable power generation companies are also looking for investment opportunities in Europe as currently domestic competition is becoming fierce for new energy projects.

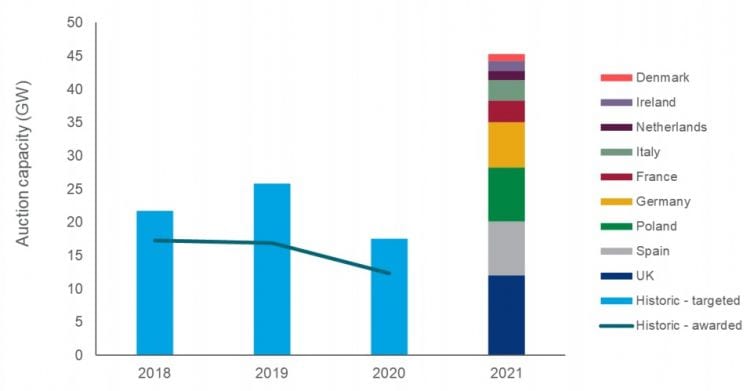

In fact, renewables were the only energy source that grew in Europe last year - despite the pandemic. According to Wood Mackenzie, Europe has 45 GW renewable power capacity slated for public auction in 2021, a significantly higher total than in recent years. Moreover, as Europe's power pipeline projects tend to benefit from the priority dispatch and Regulatory Asset Base (RAB) system for secured return on investment, Chinese companies will encounter less risk and greater success in the long run. Furthermore, various stimulus plans and regulatory initiatives both by EU and at national levels favor a green transition in power infrastructure.

By investing in Europe, Chinese companies will also improve the country’s image as a reliable and responsible partner in driving decarbonisation.

Hydrogen, a new sweet spot

European Commission launched its Hydrogen Strategy in July of last year, with a long-term objective of using green hydrogen produced 100% from renewables. The strategy contains a three-step plan, as shown below.

European hydrogen technology is leading the way when it comes to reliability and quality. On the other hand, Chinese manufacturers are ahead of Europe in the low-cost manufacturing of hydrogen production equipment (for example, electrolysers) as Chinese producers benefit from economies of scale and automation.

China currently is a major importer of European hydrogen technology. There are already about 50 OEMs working on new models for fuel cell vehicles in China, and where China is lagging behind technologically, European companies can help - through technology transfers and promoting innovation in electrolysis and liquefaction technologies.

Europe has historically been ahead of China in terms of renewable energy technologies and policy models. China can take this opportunity to learn from Europe's successes and mistakes.