Perspectives

The Deloitte Research Monthly Outlook and Perspectives

Issue 63

25 March 2021

Economy

China's policy choices: Recovery and Inflation

Each year, as the time comes around for China's ´Two Sessions’ conferences, uppermost in all observers’ minds is the GDP growth target. The economic disruption caused by COVID-19 has given birth to a vibrant debate domestically as to whether China should set a GDP target for 2021 or not, given that 2021 GDP growth will be much higher than China's growth trend (our forecast is 7.5%) anyway. However, as some sectors of the economy are still affected by COVID-19 (notwithstanding the fact that the virus has been practically eliminated in China) the key question is whether or not China should provide additional fiscal relief to SMEs and consumers. This question has become more pertinent than ever as global economic recovery received a shot in the arm with the passage of the Biden administration's $1.9 trillion stimulus package.

While the majority of policymakers feared a loss of momentum if no concrete GDP target was to be announced, they were also aware that with growth at 2.3% in 2020 (the highest among the major world economies), a growth target for 2021 would only serve as a benchmark, nothing more. Yet, a GDP target of 6% was announced during Premier Li's Government Work Report. This is quite conservative in the light of apparent base effects. So why such a low target?

As the government aims to restructure the economy to focus on more 'high-quality' growth and manage expectations around the ongoing structural slowdown, this year's Two Sessions should have been the ideal opportunity for the government to phase out growth targets. There is a chance, however, that such a low target this year has paved the way towards their complete removal in future years. Assuming that the vigorous pace of the global economic recovery continues into 2022 – a rather plausible scenario considering that the vaccine rollout in developing countries will lag behind developed countries by roughly six months – the extent to which policymakers de-emphasize GDP growth in 2022 will come under much closer scrutiny. There are several good reasons to simultaneously deemphasize the importance of GDP targets and restore fiscal discipline a year down the road. Unless slowing growth can be offset by technological innovation and improving demographics, sustaining or even raising China's long-term growth trajectory will require both supply side (further economic liberalisation) and demand side reform (increasing consumption's share of GDP). Relaxing China's birth control restrictions will also be part of a broader overall reform initiative. Debate on birth controls began to heat up in the run up to this year's Two Sessions and will have a significant bearing on China's future economic prospects as China has already followed a pattern similar to many of its Asian neighbors. As incomes have risen, couples have been marrying later and having fewer children, thus dragging down the domestic birth rate. Relaxations on China's birth control measures that currently restrict couples to two children are expected to be announced after the Two Sessions, although such easing may not actually succeed in raising birth rates.

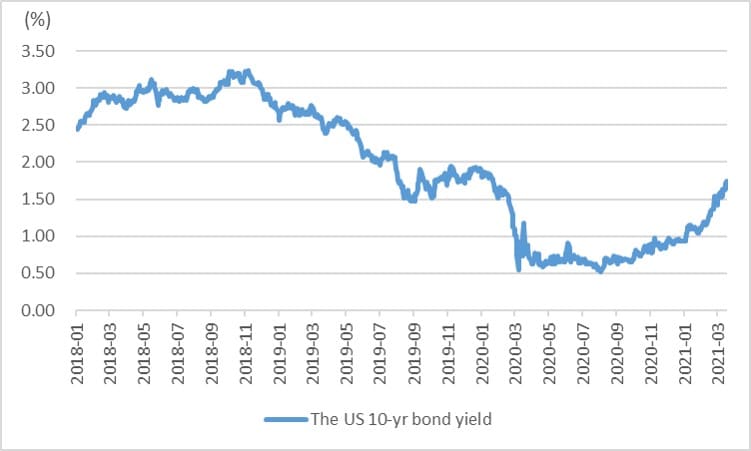

All things considered, China's economic outlook over the next couple of years is nonetheless positive. This year will be marked by a strong rebound from COVID-19 and 2022 will likely prove to be a continuation of this trend. In 2021, the US should see a better than expected recovery (some well-known institutional investors have forecast GDP growth of 6-7% in 2021), creating a much more favourable global backdrop, and European economies will join the cyclical recovery in 2022. The biggest risk will come from inflation, driven by a global recovery and surging commodity prices (not limited to just crude oil and iron ore). Asset inflation will also be of increasing concern to Chinese policymakers who will have to factor it into their decision making. In the US, by contrast, the Fed is likely to hold short term interest rates unchanged this year. The central question therefore is not whether to tighten monetary policy, but how – raising the reserve requirement ratio, increasing short term interest rates, strengthening the RMB exchange rate or taking other, more unconventional, measures. Our view is that short term interest rates will not rise, but we can expect to see more ‘persuasion tactics’ being employed by the Chinese authorities to stabilize property prices. Of course, asset inflation is as much a global phenomenon as it is a national one. In the current global environment of low interest rates, the RMB remains a high-yielding currency and therefore could very well continue to attract capital inflows as it did in 2020. Can China afford to allow the RMB exchange rate to appreciate in the face of substantial capital inflows? The answer is yes, but if the economy has to be restructured owing to various constraints such as environmental considerations or global protectionism, would it not be better to avoid an overly strong RMB especially when the greenback regains some lustre this year? From this perspective, the recommendation from SAFE (State Administration of Foreign Exchange) of allowing individuals to use their annual quota of $50,000 to purchase overseas financial products such as insurance and securities could provide timely relief.

To insert a relief valve in a relatively closed capital account is a novel idea, but implementation will take time. Meanwhile, investors are quite literally hanging onto the Fed's every word as long term interest rates edge ever higher on a strong cyclical recovery and rallying commodity prices. For China, higher commodity prices (especially crude oil) will mean a reduced trade surplus and a potential squeeze on industrial profits. So far, based on the performance of sub-sector A shares, manufacturers have performed strongly, suggesting that the market is banking on an uninterrupted recovery. However, central banks need to be ahead of the curve and so we expect the PBOC to exercise more caution if property markets in certain cities (e.g. Shanghai and Shenzhen) overheat. As we alluded to earlier, raising interest rates or the reserve requirement ratio is not an option given the current strength of the dollar. If 10-year US Treasury yields approach 2%, the dollar could conceivably sustain its rebound which has already surprised many people this year. All in all, concrete steps to implement capital account relaxation, if needed, in conjunction with policies aimed at boosting consumer incomes are more preferable policy choices.

Chart: Emerging inflation risk

As expected, the high-level dialogue between senior US and Chinese officials in Alaska has done little to cool existing bilateral tensions. However, despite the accusations levelled by both sides, each party was able to lay down their red lines, and there appears to be appetite at least to cooperate on tackling global issues of mutual interest such as climate change and the pandemic.

Technology

Caught up in a 'perfect storm'

The digital world as we know it today runs on semiconductor chips. Almost all electronic devices such as smartphones, televisions, and air purifiers, contain chips, and every car has dozens of chips. Semiconductor chips also play an important role in Internet optical fiber, digital factory management, artificial intelligence as well as power transmission. The current global semiconductor chip crisis, which has forced automobile companies to reduce production and has pushed up prices of many electronic devices, stems from a convergence of several factors last year:

- Unprecedented demand - The Covid-19 pandemic has spurred unprecedented demand for consumer electronics as consumers bought PCs, monitors and other electronics peripherals for remote learning and working from home. The stay-at-home era also spurred sales of home appliances from TVs to air purifiers, all of which now come with smart chips. A boom in the new breed of 5G-compatible devices further exacerbated the shortage.

- Manufacturing and logistics bottleneck - Top chip designers across the globe rely on Asian companies for manufacturing, foremost among which are TSMC and Samsung. Due to the high cost of setting up semiconductor plants, these two companies have, in recent years, become the only sources for producing the most advanced kinds of semiconductors. Increasing semiconductor capacity takes years to plan and billions of dollars to build in tandem with customers. COVID-19 has also created logistics and cargo choke points. For example, the cost of moving a shipping container is now considerably more expensive than it was 18 months ago.

- Excessive stockpiling - Major Chinese smartphone and networking gear makers began stockpiling components to safeguard against U.S. sanctions. Hence Chinese imports of semiconductor chips reached almost $300 billion in 2020 - a fifth of the country’s overall imports. Other multinationals have also been accumulating more inventory than normal to hedge against uncertainties. All this hording has dried up supplies, leaving little room for smaller-volume buyers such as the car and gaming console makers to get what they need.

- Vaccine distribution - Large-scale mass vaccination efforts could also be adding to the stress on semiconductor supply chains. This is because vaccine vials use the same silicon that is needed to manufacture consumer electronics.

Semiconductor shortage creates a ripple effect across industries.

The global semiconductor chip shortage has affected almost all electronics-based industries, from consumer electronics to automotive. Auto makers have been hit the hardest, as they are likely to lose around $61 billion of expected sales. This has spurred governments in the U.S. and Germany to take action. But the electronics industry may well end up being worse off. Qualcomm and AMD, which sell chips to electronics firms, have noted a shortage in recent weeks while Sony is unable to ship its flagship PlayStation 5 game console to consumers. Apple, which recently reported a record $111 billion quarter, could not meet the demand for its new iPhones because it didn’t have enough semiconductor chips.

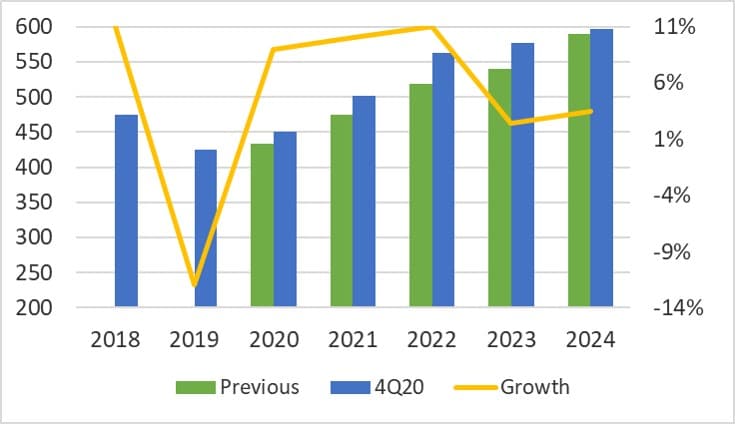

Figure: Semiconductor Revenue Forecast ($billion)

Industry to be transformed by the shortage

From remote work and distance learning to the daily commute in computer-powered automobiles, the ongoing product shortages have clearly illustrated the extent to which the modern economy hinges on semiconductor supply. There are 3 trends that will play out in the near term:

First, we may see more in-house chip design and, possibly, production. The current semiconductor chip shortage could spur companies to begin designing and manufacturing their own chips. For example, last year, Apple started designing its own chips, although the manufacturing of these chips is still being outsourced. This is because chip manufacturing is capital intensive and requires large up-front investment as well as proper expertise and manufacturing experience. In addition, a chip fab has to reach a certain scale and utilization rate to be financially viable.

Second, businesses need to better plan its logistics. In previous "black swan" disruptions such as typhoons or floods, the industry adjusted, arriving at a new normal. But, the only new normal during the Covid-19 pandemic seems to be change. Alternatively, companies could source from other suppliers. But since most suppliers are at present based in Asia and remain dependent on air and shipping lanes to supply their customers, this will potentially create choke points, amplifying the need for proper supply chain planning and collaboration. Companies need to adjust their capacity and sourcing patterns with suppliers. In the short term, industry-wide collaboration can help reduce the impact of shortages. But in the long run, businesses with mature supply chain planning processes will perform better.

Third, semiconductor chips have become strategic assets. Rising overall demand for semiconductors and their ever-increasing importance throughout the global economy has captured the attention of policymakers around the world. For example, the U.S. Congress enacted legislation earlier this year calling for federal incentives to encourage domestic chip manufacturing and investments in semiconductor research in order to make semiconductor supply chains more resilient to future crises. On February 24, the U.S. President signed an Executive Order to address the global semiconductor chip shortage. China, on the other hand, aims to domestically produce 70% of its semiconductors by 2025 as part of its broader plan to attain global leadership in high-tech industries such as artificial intelligence and information technology. The Chinese goal was made against the backdrop of the US tightening restrictions on American and overseas chipmakers that hope to ship to Chinese tech firms. But only time will tell whether this goal will be achievable since China spent almost $300 billion in chip imports last year.

Public Sector

Moving steadily into a new stage of development

The 2021 National People's Congress and the Chinese People's Political Consultative Conference (Two Sessions) were held on time this year from March 4 to March 11, with more than 2,000 CPPCC members and nearly 3,000 NPC deputies from all over the country gathering in Beijing. (Last year was the first time that, due to the pandemic, the ‘Two Sessions’ conferences were delayed.)

Having successfully brought the coronavirus under control, China emerged as the only major economy in the world to achieve positive economic growth in 2020 last year with an annual GDP growth rate of 2.3% and a GDP exceeding RMB100 trillion for the first time.

This year’s ‘Two sessions’ meetings are especially significant because 2021 marks the start of China's 14th Five-Year Plan, the beginning of a new stage of development in the construction of a modern socialist country, and the 100th anniversary of the founding of the Communist Party of China. Hence the Two Sessions meeting began by summarizing the experiences and lessons of China's economic and social development in recent years and then went on to discuss the implementation of the ‘dual circulation’ development concept. Significantly, the blueprints for China's development in the next year, the next five years and even the next 15 years, were described as being characterized by “steady progress”.

The coming year: a return to normal policy measures

Despite getting hit by the COVID-19 pandemic in 2020, China's economy grew by 2.3% and the targets outlined in the 2020 Government Work Report were accomplished according to schedule (see table 1). At the same time, with the normalization of epidemic prevention and control measures, 2021’s macro-control policies will only begin to veer towards a return to normal, while still maintaining the necessary support for economic recovery and adhering to the overall tone of “steady progress” adopted during the Central Economic Work Conference at the end of 2020.

Table 1 Objectives in 2021 Government Work Report

Unlike 2020, the Government Work Report presented this year set a growth target of more than 6% for 2021. Taking into account the underlying base period of the economic downturn in 2020, the target is relatively conservative and highlights the Chinese government's “bottom line thinking”. On the other hand, in view of the actual economic recovery, this fairly modest target is tantamount to telling all parties concerned to concentrate on promoting reform and innovation, as well as high-quality development. At the same time, this will ensure that when the economy returns to normal growth after the pandemic, wild swings can be avoided, thereby maintaining the stability of market operations.

Given that the global economic recovery remains slow and domestic economic growth has still to gather momentum, the fiscal deficit target has been set at around 3.2% for 2021. The expected targets and statements on price level, monetary policy and fiscal policy all reflect the need to keep the economy running within a reasonable range and maintaining the bottom line in the face of possible systemic risk while at the same time moving towards future goals.

The report also supports the strengthening of employment-over-growth policies and states that “the effective enhancement of people's livelihood and well-being remains of the highest importance”. The target for new employment generation in cities has not been changed much from the 2020 figure. It remains at the level of around 11 million. In addition, topics of concern to Chinese society such as education, wellness and health, housing, basic social security, spiritual satisfaction and social governance were also addressed in the report.

In order to accelerate the formation of a new development pattern of domestic and international ‘dual-circulation’, the report states that the government will continue to focus on a combination of supply-side structural reform and expansion of domestic demand, as well as industrial chain and supply chain optimization and stabilization. The government is to ensure that the same standards will be applied to both domestic and foreign products and that various approaches to increase people incomes while tapping into the potential of the domestic consumer market will be adopted. At the same time, the Chinese government will continue to promote the steady development of imports and exports, utilize foreign capital actively and effectively while reducing the negative list for foreign investment, and widen the opening up of the service industry.

An analysis of the keywords in Government Work Reports since 2018 (see table 2) shows that "development" and "economy" have been the most popular words followed by "reform" and "openness". With China's economy entering a new stage of development, "high-quality" has also become an increasingly visible term. In order to achieve high-quality development, key words like "domestic demand", "industry chain", "scientific and technological innovation" have also appeared more and more frequently in Government Work Reports. In addition, acknowledging the challenges of sustainable development, the word "carbon" was mentioned for the first time in 2021. All of this is indicative of the future direction of China’s development.

Table 2 key words in Government Work Report

14th Five-Year Plan: a good start to building a modern socialist country

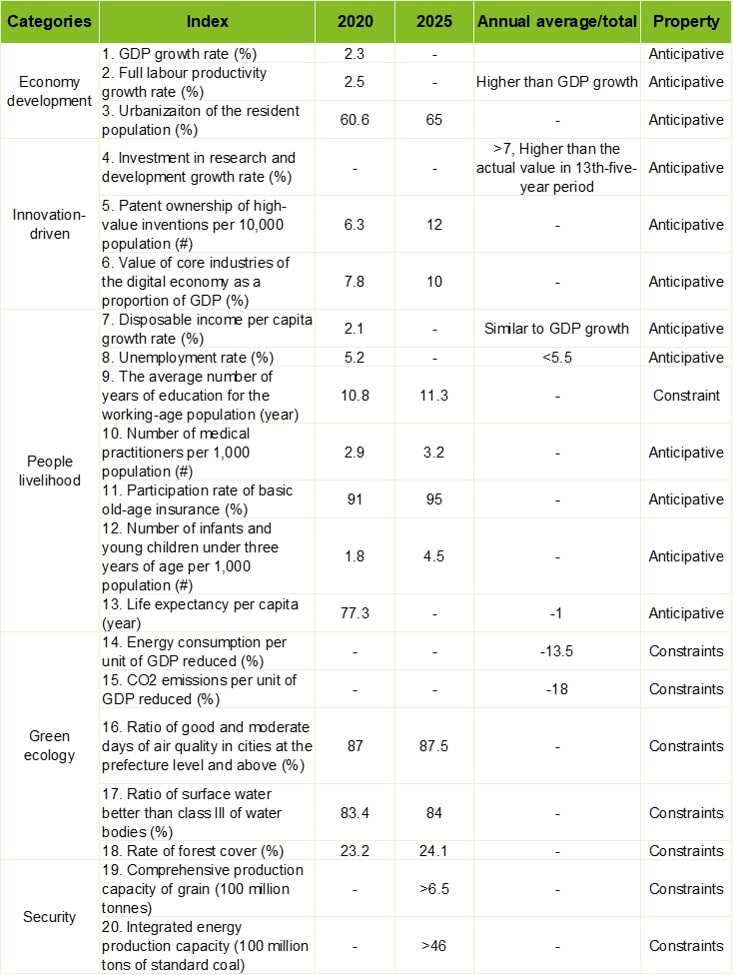

The most important item on the agenda of the Two Sessions meetings is the Outline of the 14th Five-Year Plan for National Economic and Social Development and the (Draft) Vision Goals for 2035. The current outline strictly follows the recommendations of the CPC Central Committee on the Development of the 14th Five-Year Plan for National Economic and Social Development and the Vision Goals for 2035, and formulates the main objectives and major tasks for economic and social development during the 14th Five-Year Plan period (see Table 3) in appropriate, realistic and quantifiable terms. It highlights the strong commitment of the Chinese government to steadily build a new development model during the next five years.

Table 3 Objectives of the 14th Five-Year Plan

Economic development, innovation, people's well-being, green ecology and security are the most important objectives of the 14th Five-Year Plan period, with a more detailed listing of priorities and targets under each heading.

Economic development: With the domestic market as the base, implementation of the strategy to expand domestic demand is integrated with the deepening of supply-side structural reform to lead and create new demand through innovation-driven and high-quality supply. This requires the removal of choke points, connecting production, distribution, circulation and consumption, achieving a dynamic balance between supply and demand, and allowing final consumption to account for a higher proportion of GDP growth. At the same time, through continued reform and opening up, foreign capital can benefit more from China's vast markets. Constructing a more open economic system and promoting greater international cooperation will mutually benefit China and its foreign partners.

Innovation driven: Scientific and technological innovation lies at the core of the new development plan. During the 14th Five-Year Plan period, China will adhere to innovation-driven development and put scientific and technological self-reliance at the center of its national development strategy with the aim of achieving industrial autonomy and self-reliance. At the same time, China will promote the position that enterprises must take the lead in scientific and technological innovation with the government merely providing support to industry. In addition to the research and development investment intensity target, it also proposed that the proportion of investment in basic research should be raised to over 8% at the end of the 14th Five-Year Plan Period. The implementation of the ten-year action plan for basic research, as well as the "science and technology innovation-2030" projects should achieve new breakthroughs in key technologies. It is worth noting that the new target of adding value as a share of GDP to the core industries of the digital economy underscores the Chinese government’s commitment to digital transformation.

People’s Livelihood: The 14th Five-Year Plan contains seven targets relating to people's livelihood and well-being, more than any previous Five-Year Plan. This shows that in congruence with the new development pattern, the 14th Five-Year Plan will focus on promoting equality and strengthening the construction of inclusive, basic and minimum welfare. At the same time, it will focus on coordinated development, promoting rural revitalization in order to combat poverty. It will also further improve the new urbanization strategy and promote coordinated regional development, focusing on solving problems of uneven development between urban and rural areas and regions.

Green Ecology: The draft states clearly that promoting green development is vital to implementing the new development concept and constructing a new development paradigm. The draft proposes to accelerate green development, improve the dual control of total energy consumption and intensity, and implement the 2030 national self-initiated contribution target to combat climate change. In addition, ensuring food security and energy security remains a prerequisite for development.

Summary: How to enter a new stage of development steadily

The draft retains the 2035 vision set out in the 14th Five-Year Development Plan Proposal and depicts China in 2035 from nine points of view: national strength, economic system, national governance, and social civilization, ecological environment, opening up, social construction, national security and people's livelihoods.

With the conclusion of the Two Sessions of the National People's Congress in 2021, China has officially entered a new stage of development of comprehensively building a modern socialist economy, and the 14th Five-Year Plan, a pragmatic document, will also be officially released to the public. With the blueprint outlined in this strategy, China will steadily move forward towards realizing the country's second centenary goal.

Life science and healthcare

New reforms shake up the industry

Many changes have taken place within the pharma industry after the recent 4th round of Volume-Based Procurement (VBP) and the publication of the latest National Reimbursement Drug List (NRDL). One of the significant trends to emerge is the increase in standardization and centralization in the pharma market. The new trend will profoundly transform the industry, creating a new landscape that benefits the enterprises which have a high-quality pipeline portfolio, strong R&D and strong sales capabilities. These will be the leading enterprises in the future with the largest market share. Innovation will also play a big role in the future as market players try to stand out from the crowd.

The 4th VBP – standardization is the new normal

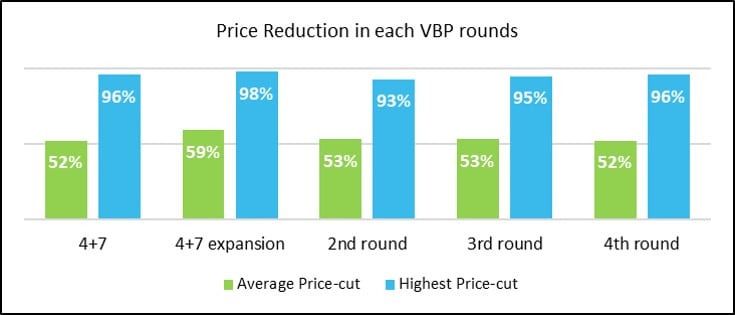

On December 25, 2020, the tender for the 4th round of VBP was issued and the tender result was published on February 3, 2021. A total of 152 companies won bids for 45 product varieties with 80 specifications. The average price reduction was 52% less than the market price with the highest price reduction hitting 96%. According to the National Healthcare Security Administration (NHSA), it is expected that the 4th VBP round will reduce China's annual drug expenditure by RMB 12.4 billion (USD1.9 billion). New prices will go into effect by May 2021.

Meanwhile, the State Council has issued an opinion paper entitled "The Opinion on the Normalization and Standardization of the VBP Development" which lays out its commitment to extend the centralized drug procurement program and to emphasize transparency and a level playing field for all players while continuing to emphasize quality control and the smooth production, supply and distribution of drugs. With this Opinion paper, it is highly likely that the VBP program will expand to include more drugs with high clinical demand.

Although there were 34 varieties of drugs open to foreign players in the tender process, only 5 varieties had foreign winners. From the previous VBP rounds, we have observed that more and more generics manufacturers are replacing their brand-name counterparts. As the VBP implementation becomes more widespread, the mature product market for foreign companies in China will shrink as foreign companies usually have a higher cost base and are constrained by their global price consistency policies. In such a climate, cost control and pricing strategies become very important. As the generics market becomes more centralized, products that are unable to offer a lower price could get pushed out of the market. On the other hand, companies with products that have passed the consistency assessment are likely to become leading players in future VBP rounds.

What is becoming increasingly clear is that with the implementation of the VBP system, local companies that had small market shares, but which managed to win VBP bids, have now been able to reach scale and build or upgrade their own research and innovation capabilities. With the normalization of the VBP program, we foresee that there will be more local players coming to the fore in the near future.

In general, with the introduction of the VBP program, the mature product market is getting more centralized. We foresee that in the coming years, centralized procurement will become the new normal across the board at both national and province levels. Biologics and TCMs may become the next battlefield of the centralized procurement system. As a result, foreign pharmaceutical companies will find it more difficult to sustain their presence in the mature brand-name drug market in China. Hence, for such companies, innovation and differentiation will become more critical than ever before.

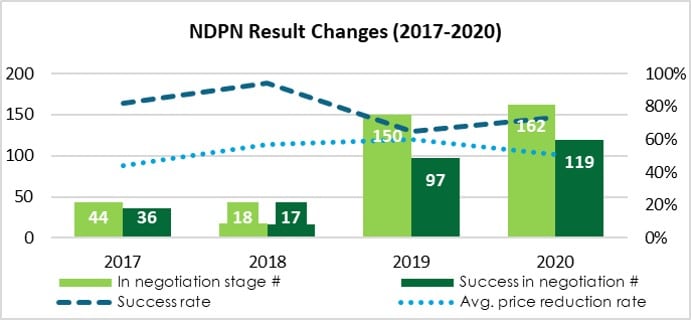

The new market landscape created by the latest round of National Reimbursement Drug List (NRDL) updates and National Drug Price Negotiation (NDPN)

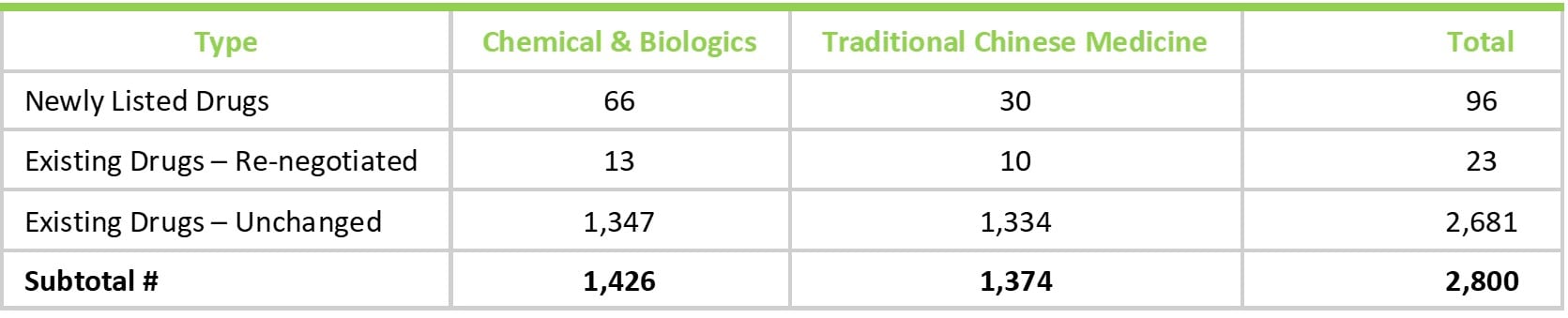

To achieve higher efficiency in the usage of National Health Insurance (NHI) funds, the National Healthcare Security Association (NHSA) has made "secure the essentials" its core policy objective, whilst downgrading other objectives such as "removing products with low clinical value" and "accelerating the listing of more new drugs”. Hence, 2020's National Reimbursement Drug List (NRDL) which was released by the NHSA on December 28, 2020 revealed that a total of 119 drugs successfully entered the 2020 NRDL– 96 newly listed, 23 renegotiated, while only 29 drugs were removed from the list. The new NRDL contains a total of 2,800 drugs and will take effect on March 1.

Additionally, NHSA has also announced three major accomplishments in this round of the NRDL negotiations:

- The average price reduction for renegotiated drugs reached 43.5%.

- All covid-19 treatment drugs are included in the covid-19 treatment guideline to support the covid-19 treatment and prevention.

- The new list includes 16 innovative drugs which were newly approved by National Medical Product Administration (NMPA) in 2020 (as of August 17th, 2020)

The current NRDL update has also set the price ceiling for many products currently in clinical trials such as PD-1/PD-L1 products. While drugs included in the NRDL averaged almost 78% in price reductions, those failed to be included in the NRDL then amended their Patient Assistance Program (PAP) as the alternative solution for the price reduction in order to compete with newly listed NRDL drugs in the market. Either way, the price ceiling for future PD-1/PD-L1 products has been set. In addition, as NRDL updates and NDPN become more frequent, the NRDL access for all drugs has been accelerated, giving rise to a phenomenon of drugs getting onto the “NRDL listing right after NMPA approval". Hence, for pharma companies in China, indication selection, pricing strategy, and pharma economics studies will become extremely important as they will have to be more precise in their product portfolio design and pricing strategy in order to secure profits.

A change in the pharmaceuticals landscape

With the on-going medical reform, the pharma market is becoming more centralized. We predict there will be two major trends emerging in the industry in the next few years:

- Locals poised to replace foreign counterparts. As more and more local generics and biosimilars have passed the consistency assessment, it will become harder for foreign pharma companies to sustain their brand-name business in China, especially when more domestic companies are coming up with locally developed, innovative products. We expect to see more domestic companies coming up with competitively priced new products that are able to compete with those of the foreign players, thus ending the old status quo where imported drugs were heavily relied on.

- Radical overhaul of pharma strategies with a focus on innovation in order to remain in the game. As the VBP program becomes ‘normalized’ across China, pharma companies which rely heavily upon their generic business will feel the squeeze. And if they fail to make headway under the Volume Based Procurement system, their products might be forced to exit the market. Furthermore, with the speed-up of the regulatory approval mechanism and the shortening of the NRDL access period, we have seen 16 new drugs get onto the NRDL list in the same year of getting regulatory approval. This could herald a new situation where new drugs can get onto the "NRDL listing right after NMPA approval". In order to adapt to the new changes, pharma companies in China will have to undertake a major overhaul of their operating systems, enhancing their R&D facilities in order to produce more innovative new drugs so as to differentiate themselves from the pack.