Perspectives

China's economic and industry outlook for 2022

Issue 70

30 December 2021

Economy

Property holds the key to growth in 2022

The key question for 2022 remains what will be the right level of economic growth, assuming that policymakers won't have to resort to a massive fiscal stimulus as in 2008. Can this be done? If so, what tools will be utilized? Uncertainties brought about by the new Omicron variant have clearly reinforced the existing tough policy on Covid-19 protocols in China with zero tolerance of any cases. Needless to say, the economic cost (e.g., travel and restaurants, to name a few) is high, but in the grand scheme of things, the majority of Chinese citizens support such strict measures because normal life has ensued amid some inconveniences. Such strict protocols may well go up a notch soon as China prepares to host the Winter Olympic Games in February. Industrial activities will certainly be affected in Beijing and Hebei province over the next two to three months, and the National Bureau of Statistics has even acknowledged that factories will be shut down in order to improve air quality in Beijing during the games, although its overall impact will be limited. Tighter Covid-19 mitigation measures might prompt certain restaurants to close operations for a longer period than normal (the Winter Olympics coincides with Chinese New Year) due to rising costs associated with Covid-19 tests. Meanwhile, the impact of the Evergrande fallout is likely to be felt by the broader property sector. Judging from economic performance from H2 of 2021, a greater dose of stimulus is indeed warranted should 2022 GDP growth be maintained around 5%, an implicit target.

Recent cuts to the reserve requirement ratio on December 10 2021 has sent two signals: 1) the PBOC will undertake a different direction from that of other major central banks in developed countries (e.g., the Fed and Bank of England); 2) the PBOC would like to stabilize the property market. The most recent reduction of the lending rate (from 3.85% to 3.80%) by the PBOC on December 20 2021 has underscored policymakers' commitment to reflate the economy amid more hawkish stances by the Fed. So the divergence between the PBOC and the Fed could therefore be more pronounced in 2022. Would such a divergence be a significant factor causing the RMB to give back its immense gains in 2021 against the dollar and most other currencies? In our view, the answer is yes, but that should hardly be a concern. Why? If the PBOC continues on its course of improving liquidity with the main goal of revitalizing investment in the property sector whose growth will clearly be a determining factor of GDP growth for 2022 which is projected at around 5%, interest rate differentials between the RMB and the dollar will surely be widened. A slightly more competitive RMB would bring down interest rates in real term because additional demand for the RMB. Again, such a calibrated change to the exchange rate will be aimed at making the intended monetary policy more potent, but a weaker RMB would serve as an insurance for China's export machine in the medium term. Given that inflation is not expected to be a problem, a slightly weaker RMB will be necessary to compensate for the limited room of rate cuts from the standpoint of monetary easing. On fiscal policy, China will have to ramp up its fiscal deficit in areas of fiscal reliefs and potentially increase fiscal transfers to those local governments who may experience difficulties (local governments' finance has been linked to land auctions). So Beijing does have tools for reflating the economy. However, policy mixes matter in the post-Covid era for several reasons. First, supply chains in China have proven to be more resilient. Second, Omicron has compounded challenges faced by SMEs who may not benefit much from monetary easing. Third, consumers will be expected to carry growth if property investment does not rebound. So the policy implication is that tax cuts and subsidies should be targeting to SMEs and those enterprises who are more vulnerable to travel restrictions and social distancing.

In an almost unprecedented manner, the widely watched Central Economic Work Conference flagged six stabilities (employment, finance, trade, foreign and domestic investment, and expectations). Employment should naturally be given top priority for social stability. Exports have been doing well despite a strong RMB and therefore trade should not be a concern. Stability of expectations is linked to the finance and investment. The key to ensure stability around expectations is policy clarity. As such, a stronger signal of preventing spillovers from Evergande to the real economy will be the first step in stabilizing expectations.

Energy

Re-focusing on energy transition

China's energy sector experienced a volatile year in 2021, with the fastest growth in energy consumption on record in the first half of the year followed by massive power cuts across the country in the second half. As supply chain disruptions wane and most countries return to pre-pandemic levels of energy consumption, China's energy industry will have to re-focus on energy transition as the problems of the past come back into play. Here are five trends to watch for in 2022.

- Growth in energy consumption will slow, but with a rise in clean energy consumption

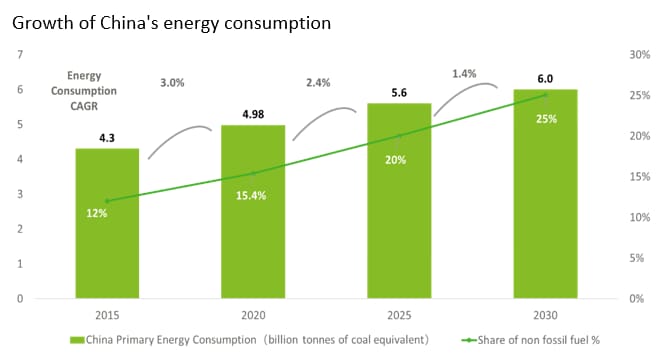

China’s total primary energy consumption is expected to reach 5.2 billion tonnes of coal equivalent (tce) in 2021, a 4.4% increase compared to the previous year. This relatively high growth rate is mainly driven by the recovery of the industrial sector in China while the rest of world still struggles to expand curbed production capability due to the pandemic. In 2022, we expect to see a mild increase in energy consumption to about 5.3 billion tce, as we move away from seasonal energy demands and the push to energy saving intensifies. In the long-term, China's energy consumption will slow down, while clean energy consumption will increase as China is determined to reach the goal of 20% of non-fossil fuels in the energy mix by 2025 and 35% by 2030.

Source: China Statistics Bureau, China 2030 Energy Development Planning and 2060 Outlook, Deloitte Research

- Energy supply will diversify, incorporating clean energy sources into the system with renewable pairing policy support

China still has a carbon based energy structure dominated by coal. Energy infrastructures are usually large-scale and centralized, with limited flexibility. However, there is no doubt that China's energy supply will transform from a high-carbon structure to a diversified, clean and integrated one, allowing for the coordination of various energy formats including electricity, heating, cooling, gas, water, and hydrogen. So far, more than 20 provinces have released policies to encourage or enforce the deployment of renewables-plus-storage projects, with an energy storage capacity ratio at 5-20% of renewable energy generation capacity. - Changes in energy service models and consumer roles

During the process of energy transition, the diversified and integrated development of energy services will provide consumers with various energy options. The relationship between energy consumers and suppliers has gradually changed from a one-way supply-demand relationship to a two-way interactive model. Increasingly, energy consumers will also become energy producers, dealers and storage providers. Energy consumer's buying decisions will not only depend on price, but also on factors such as energy quality, ease of use, environmental impact, and technological change. - Improvements in the overall efficiency and safety of the energy system through digitization and smart technologies

The transition to an integrated energy system will be accompanied by greater coordination among various energy sources. Digitization and smart technologies will further enhance data collection and utilization in energy production, transmission and consumption. The extensive application of information technologies such as big data, cloud computing, IoT, and artificial intelligence will fully tap into and utilize the data generated by different kinds of energy systems throughout the life cycle: 5G provides energy systems with ultra-wideband and ultra-low latency; IoT enables online access and data collection of massive devices; and cloud computing and artificial intelligence enhance the efficiency of calculation, processing and analysis of big data. Energy enterprises may optimize decision-making through data analysis, thereby improving the operational efficiency of energy production, transmission, trading and consumption, and ultimately boosting the overall efficiency and safety of the energy system. Take the power system for example. This will inevitably become more efficient, interactive and intelligent, driven by the large-scale integration of clean energy, combined with the utilization of interactive facilities such as distributed energy, energy storage, electric vehicles, and smart electricity equipment. - Zero-carbon transition, energy transition and digital transition jointly promote the development of new business and new profit models

The new energy landscape that is coming into being through the integration of multiple energy sources, energy providers, distributors, consumers, big data and smart technologies is driving profound changes in the energy supply-demand model and business ecosystem, as well as giving birth to new business and profit models. For example, energy enterprises may provide one-stop smart energy services by consolidating capabilities in energy consulting, green energy substitution, multi-energy synergies, integration of investment, construction and operation, energy efficiency management, carbon asset management, digital platforms and so forth, resulting in the two-way interaction with users and the sharing of ecosystem data. Non-traditional energy enterprises such as digital technology and internet companies have entered the market, forming a business ecosystem centering on the coexistence of traditional energy enterprises and emerging service providers.

Logistics

Deeply exploring the intensive and efficient logistics

China's logistics industry is expected to grow by 8%

2021 is the opening year of China's 14th Five-year Plan. Under the new development framework, the continued integration of China into global markets will be accelerated through improving and expanding logistics networks. In the last few years, the logistics industry, especially the level and capacity of supply chain services associated with international trade, has been rapidly improved. This trend will continue as expanding logistics networks in international markets has become a mainstay in the future development of China's logistics industry. In the domestic market, it is urgent for the logistics industry to upgrade from traditional commercial logistics to integrated supply chain management services, under the stimulation of the gradual saturation of the industry scale and the increasing diversity of demand.

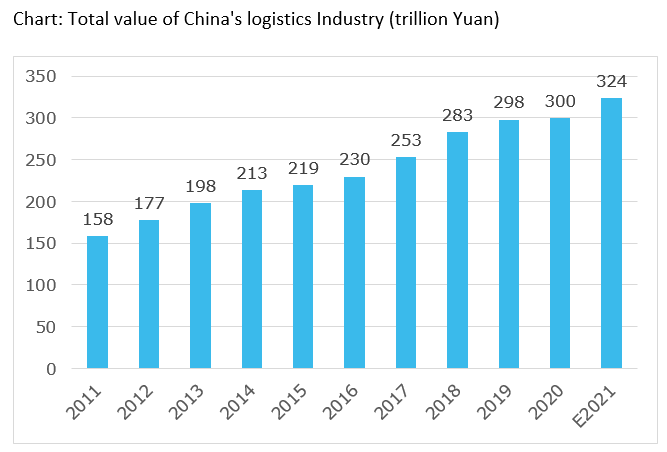

China's logistics industry could not have made such rapid strides without the continuous improvement of laws and regulations, physical infrastructure, supply chains, and the application of science and technology to logistics. According to the China Federation of Logistics and Purchasing (CFLP), the total value of the logistics industry was RMB 261.8 trillion from January to October 2021. We conservatively predict that the total value of China's logistics industry will increase about 8% to reach at least RMB 324 trillion by the end of 2021.

Source:Wind, Deloitte Research

On the 18th of November 2021 the Ministry of Transport issued the ‘Development Plan for Integrated Transport Services during the 14th Five-year Plan’. This stipulated higher requirements for the development of the logistics industry in light of the post-pandemic economic situation: “We should pay more attention to quality, efficiency and innovation-driven development, and follow the basic principles of deepening reform, safe development, green and low-carbon development. By 2025, a full-chain and integrated freight and logistics service system should basically be established, with transport service management system and management ability modernization significantly increased, and service capability further enhanced to support economic and social development.” With this in mind, we can expect to see some of the following developments in 2022 in the logistics industry.

In 2022 the logistics industry will focus on intensive and efficient in-depth exploration

- Build an intensive and efficient freight and logistics service system

The construction and development of multi-modal transport will enable the logistics industry to improve transport efficiency and reduce transportation costs. At present, domestic multimodal transportation is relatively small in scale and lags behind developed countries, especially need to strengthen bulk goods in "road to rail" and "road to water" links. Next, to further promote the construction and the operation level of multimodal transport systems remains an important task in China's transportation and logistics field during the "14th Five-year Plan" period. - Build a safe and smooth international logistics supply chain service system

Where smooth transportation is concerned, China needs to rely more on the existing international train system, promote intensive organization, platform operation, product service and market operation of the rail channel, and actively and steadily expand the overseas coverage capacity of aviation logistics. From the perspective of public health in the context of repeated outbreaks during the pandemic, safety of logistics personnel is crucial for the smooth running of international logistics operations. - Develop a clean and low-carbon transport service system

At present, low energy consumption, high efficiency, energy saving and environmental protection have become the norm for the logistics industry. At the government level, this means accelerating the construction of a logistics standardization system, promoting the integrated development of green logistics-related industries and gradually pushing the carbon asset management of the logistics industry. At the enterprise level, leading technologies such as artificial intelligence (AI), big data and Internet of Things (IoT) can be deployed to realize low-carbon and intelligent operations and reduce carbon emissions through the application of carbon reduction technologies. This will not only help logistics enterprises control costs, but also provide a great opportunity for them to improve their competitiveness.

Takeaways for Chinese logistics enterprises

- The deep integration of manufacturing and logistics industry puts forward higher requirements for logistics enterprises.

As the manufacturing industry moves towards the 4.0 mode, intelligent logistics as a partner to intelligent manufacturing will continue to benefit. China's manufacturing industry is at a critical moment, upgrading to a flexible production stage. This raises the bar for the degree of division of labor, automation rate, coordination within the industry chain, and production efficiency. All these upgrade also urges China's logistics enterprises to upgrade accordingly. - Combination of digital and intelligent logistics supply chain will continue to benefit logistics technology companies.

In the next two years, the intelligent warehousing will usher in a golden period of development in the logistics industry. At present, it is mainly used in industrial production logistics and commercial distribution logistics. Through the coordination of "digital trade and digital freight", procurement and transportation systems will be able to seamlessly connect, so as to create a full life cycle supply chain management system. As investment and financing of logistics technology is picking up, logistics technology enterprises will get more capital infusion, fuelling this digital transformation. - As the integration of the logistics industry continues, more leading international logistics enterprises will be born in China.

On December 6, the China Logistics Group Co. Ltd., a new State-owned enterprise with integrated logistics as its core business, was officially established. The purpose of the reorganization of several State-owned enterprises into a single conglomerate was to create a world-class comprehensive logistics enterprise group with global competitiveness. History shows us that international logistics enterprises basically upgraded from a single business to a comprehensive logistics service provider through mergers and acquisitions. The active mergers of major logistics companies in 2021 prove that mergers and acquisitions are an inevitable step in the process of growing into a global logistics enterprise. With the upgrading of technology and a concomitant increase in market size, China will also see the birth of more companies that are capable of rivaling international logistics giants.

TMT

Technology development accelerating despite headwinds

Digital technology is rapidly reshaping the way people live and work as artificial intelligence, cloud computing and 5G technologies are already entrenching themselves in the daily lives of people across the globe. Going into 2022, we expect the digitization of industries to accelerate, coupled with advancements of innovations in disruptive technologies, while focusing on sustainability. However, the industry as a whole will continue to face regulatory and supply chain challenges in the near term, as well as competition between the U.S. and China for technological supremacy.

Semiconductor chip shortage to continue: By 2022, more digital products will have semiconductor chips built into them. Demand for chips is increasing from consumers, industry and government, and the semiconductor industry is ramping up its production capacity. We expect chip shortages to continue well into 2022, with some deliveries delayed until 2023. This means that the shortage will last for at least 24 months, with a cumulative economic impact of more than $500 billion. For example, if a $30,000 car is missing a critical $1 chip, that carmaker won't be able to sell his car to consumers. As a result, chip companies are spending over $200 billion for building new fabs while governments are spending over $100 billion to invest in chip manufacturing. The real problem is that it takes years to build a fab. So the shortage of semiconductor chips will continue.

Semiconductor ecosystem is poised to be a winner: Since the world needs innovative energy-efficient, secure and smart, as well as cheap chips, billions of dollars of venture capital is indispensable. We expect global venture capital investment in semiconductor companies to exceed $6 billion in 2022, down slightly from 2021, but well above the $1-2 billion average of the past 20 years. Much of this investment is likely to go to companies in China. High valuations are making investment in chip start-up companies more attractive than ever, with dollars per deal tripling in the last two years. As venture capital firms continue to invest in start-ups, the semiconductor ecosystem will come out on top.

Smartphones to reduce carbon footprint: : We expect the world's 4.5 billion smartphones to generate 146 million tonnes of CO2 or equivalent emissions in 2022. Most (83%) of these emissions will come from the manufacturing, transporting and first-year use of the 1.4 billion new smartphones expected to be shipped in 2022. As manufacturing accounts for almost the entire carbon footprint of smartphones, the biggest factor that can reduce their carbon footprint is to extend their life expectancy. This will depend on a thriving market for trading and refurbishment, and as much optimization software as possible plus regular security updates.

Wi-Fi 6 will play a pivotal role: 5G may be getting hyped right now, but Wi-Fi 6 devices are quietly outpacing 5G devices by a wide margin. We expect Wi-Fi 6 to ship more devices than 5G devices in 2022 - at least 2.5 billion Wi-Fi 6 devices compared to around 1.5 billion 5G devices. Like 5G, Wi-Fi 6 has a major role to play in the future of wireless connectivity - not only for consumers, but for businesses as well. As a key partner of 5G in advanced wireless solutions, Wi-Fi 6 will be increasingly important in realizing the benefits that enterprises are seeking through next-generation connectivity.

Increased competition for quantum computing: Quantum computing (QC) should begin to make inroads by 2022, although the market will remain a niche one for a while. Investments in quantum computing by governments including China, India, Japan, Germany, the Netherlands, Canada and the United States could bring the combined total this year to north of $5 billion. Within a decade, quantum computers will become useful and generate billions of dollars in annual revenue. Companies should now start thinking about the impact of QC. What impact will quantum computing have on their own industry and on adjacent industries? What does this mean from a strategic, operational and competitive point of view?

Everything ‘Metaverse’: The metaverse is a digital reality that fuses social media, gaming, augmented reality/virtual reality (AR/VR), and cryptocurrencies to allow users to interact in a virtual world. The Metaverse is currently conceptual and may become the next generation of the Internet. Apart from Facebook which has changed its name (to Meta) this year, several tech giants such as Microsoft, Google and Apple have also announced that they will enter ‘Metaverse’ space. Compared to the traditional Internet, the 'Metaverse' will have higher requirements in terms of immersion, engagement and sustainability, and will therefore be supported by many independent digital tools, platforms and infrastructure. As technologies such as AR, VR, 5G and cloud computing reach maturity, the 'Metaverse' is expected to gradually move from concept to reality, with a number of new products as well as business models emerging in the near future. In addition, the underlying architecture of the 'Metaverse' is built across software and hardware devices, so even the tech giants can't cover it all. Start-ups can hope to get a share of this huge market in terms of breakthroughs from single-point technologies.

AI regulation gets tougher: AI in 2022 will face increasing regulatory scrutiny and its impact will be felt across industries. AI in 2022 will be much more powerful than it was five years ago, but regulators are concerned about the impact of AI on fairness, bias, discrimination and privacy. In 2022, the EU, China, the US, and other countries will propose to regulate AI more systematically, although implementation is not likely to happen until 2023 or later. Some regulations may attempt to ban entire subfields of AI altogether. Regulating AI is necessary because AI will make decisions, but regulating AI is also very difficult.

Data security a hot button: Against the backdrop of the ubiquity of big data, data security has risen to the status of strategic national security. In China, we expect stricter regulations on cross-border data transfers in 2022. Chinese companies with overseas operations and multinational companies in China should carefully assess whether they fall under the scope of critical information infrastructure operators before transferring data to overseas parties. They should also closely monitor future legislative developments to avoid compliance risks and potential penalties. In addition, companies engaged in data trading, information matching, software development and other related activities should conduct social ethics surveys and do an ethical review of their data analysis and products before going to the market.

Automotive

Investing in long-term transformation despite short-term troubles

Despite short-term vicissitudes, China’s auto market will remain resilient in the mid-to-long term. The pandemic along with supply chain problems has taken a heavy toll on car sales. The shortage in automotive chips has led to an industry-wide production halt, which to a great extent deterred consumers’ car purchase intentions due to months-long waits and limited price discounts. It is estimated that the chip shortage has caused a reduction of about 2 million in car production, or about 8% of China’s annual vehicle output. We expect that chip shortage woes will extend through 2022 given the uncertainty of the pandemic but may start to ease during the second half of 2022. By then, depressed auto demand will also begin to ease. A low single digit growth rate of 3% in sales is anticipated for the whole year. However, there are some exciting trends developing across different segments of the auto market. First, China’s car market is becoming a mature market where second/third buyers (52%) for the first time have replaced first-time buyers to become the largest contributors to car sales. Second, the market share of vehicles costing below RMB 150,000 has gone down by 3.3ppts to 25.9% in the first seven months of 2021, whilst vehicles with price ranges of RMB100,000-200,000, 200,000-300,000 and 300,000 and above have inched up by 0.8ppts, 0.8ppts and 1.6ppts respectively, in line with China’s continuous consumption upgrade.

The changing consumer preference of Generation Z will usher in the transformation of vehicles growing from pure mobility tools to large complex digital terminals. Generation Z will soon take over the Millennials to become the largest group of first-time car buyers in China. Compared with their millennial peers, the tech-savvy Generation Z is much more interested in personality and lifestyle, and their buying decisions are less influenced by price considerations than consumer satisfaction. They care more about experiences and involvement and demonstrate a higher willingness to pay a premium for new and smart features. This trend in demand is matched on the supply side by the ongoing revolution that is transforming automobiles from a mechanical device to an ever-changing and upgradable digital product.

The new energy vehicle (NEV) sector is expected to compete neck to neck with its ICE (internal combustion engine) vehicle peers. 2021 marks a critical juncture for China’s new energy vehicle industry. It has taken nearly a decade for the EV sector to grow from nothing to 5% of total new car sales in China. However, it took less than ten months for EV penetration to surpass 10%. Sales of electric vehicles is poised for double-digit growth over the next five years. We expect the growth momentum will be primarily driven by the following four factors:

- Growing number of new models to be launched and enhanced product competitiveness. More than 20 new EV models covering a much wider spectrum of price segmentation will be launched in 2022, compensating the current product offerings that are mainly entry-level mini EVs and premium EVs. There has been a visible increase in product competitiveness in electric vehicles in the past two years. Most of this comes from EV start-ups which tend to have a competitive edge in connectivity, software-led experience and innovative services.

- Achieving price parity with ICE vehicles will play a big role in speeding up EV adoption. As the largest contributor of EV cost, batteries have seen a remarkable decline in prices thanks to economies of scale and technological advances in the manufacturing process.

- There have been some noticeable changes in consumer’s attitudes toward EVs. Some of the barriers to EV adoption have been removed. For instance, driving range is no longer perceived as the top concern for Chinese consumers. On the contrary, consumers are more concerned about the charging times and battery safety as they are considering EVs as a viable alternative to gasoline vehicles.

- Investment in EV Infrastructure continues to expand in China. In addition to meeting the challenge of insufficient charging ports, the new round of investment targets emerging demands such as shortening the charge time and other hurdles faced by EV consumers.

Funding for autonomous driving vehicles will continue to gain traction in 2022 as commercialization accelerates. Competition to produce Level 2.5+autonomous driving vehicles will heat up in 2022. Autonomous driving is no longer being seen as a key differentiator in new cars but, instead, a must-have feature in today’s intelligent vehicle. To reinforce their positions as technology leaders, some auto OEMs have been developing full-stack capabilities on autonomous driving whilst majority carmakers are partnering with autonomous driving start-ups through equity investment. Meanwhile, in their bid to fully commercialize first, China’ domestic carmakers have partnered up with tech giants Huawei and Baidu which have deployed application of L4 autonomous driving to L2+vehicles. This has led to a funding boom in autonomous driving related areas, which is expected to continue in 2022.

Software has become a key competitive edge for car companies. But the magnitude of this software-led revolution has been greatly overlooked. Software is playing a vital role in the auto industry today. At the product level, for instance, human-machine interaction in the cockpit, neural network algorithms that power autonomous driving and battery management systems for increasing battery efficiency will all have been enabled and supported by software. The application of software has widespread and far-reaching ramifications for the auto industry in that it will lead to a major change in the whole R&D process, supply chain and business model.

First, leading auto OEMs have been changing their product development method to adapt to the new normal that cars will be updated as frequently as smart phones. Second, there will be some fundamental shifts in their sourcing approach or partnership strategy in the auto industry. Auto OEMs are no longer satisfied with the embedded sourcing approach, under which they have little visibility and knowledge of codes. They have ramped up investment in in-house software capabilities to gain control of key touch points of product and consumer experience. The new trend has also given rise to a series of new software tier-1 companies, especially in chips and system software areas, which have bypassed traditional tier-1 players and forged strategic relationships with OEMs directly. Lastly, software is becoming an important new stream of revenue for OEMs. For instance, EV companies, such as Tesla and Xpeng, have been exploring subscription models, paid OTA updates and other data monetization services such as user-based insurance, remote diagnosis and maintenance. Unlike hardware manufacturing and sales, software provides recurring revenues throughout the entire vehicle lifecycle, providing a rather sustainable source of revenue for the car industry in the future.

Retail

Product upgrading and retail format innovation create resilience

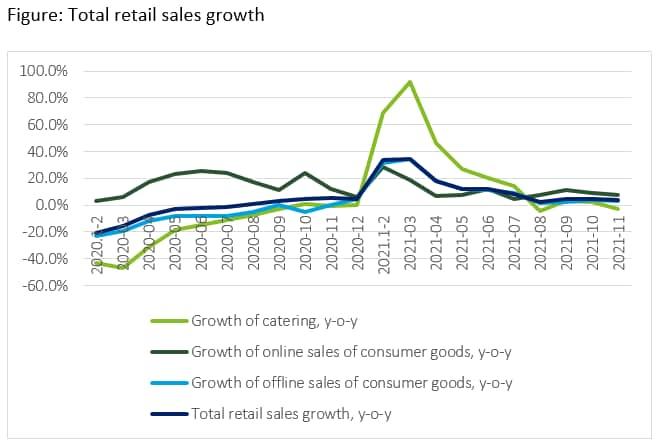

As 2021 is coming to an end, the consumer goods and retail industries are gradually recovering from repeated outbreaks of the Covid-19 pandemic. The year-on-year growth rate of China's total retail sales of consumer goods has turned positive since August 2020, and sales have gradually recovered. Although August 2021 recorded slower growth because of bad weather and repeated outbreaks, the overall recovery trend remains fundamentally unchanged. From January to November 2021, sales of consumer goods rose 13.7%, and the cumulative growth rate reached 8.2% when compared with the same period in 2019. We are confident that the industry will remain resilient in the face of product upgrading and retail format innovation driven by digitization.

Although the consumer industry is expected to be strongly resilient in 2022, it will still face many challenges. First of all, faced with repeated outbreaks of the pandemic and strict real estate control policies, consumers’ willingness to spend may further weaken, and the industry, as a whole, faces the risk of a slowdown. Secondly, information technology based retail models will be the ‘new normal’ of business model innovation. The traditional ‘brick and mortar’ business model will also face challenges coming from new market participants. Moreover, the increasingly stringent national regulatory policies on antitrust, data security and low-carbon emission reduction will increase compliance costs for enterprises, making it difficult for enterprises to further optimize their operations. In the coming year, the development of online and offline retail and consumer goods may show the following new trends:

E-commerce platforms will continue to expand the scale and proportion of domestic online sales, despite high customer acquisition costs that have slowed the growth of online sales. As "digital natives" represented by Generation Z have gained greater consumption power, and with a significant increase in the number of middle-aged and elderly Internet users during the pandemic, consumer goods companies further accelerated the penetration of various goods onto online channels targeted at consumers of all ages. According to CNNIC, by June 2021, the number of domestic Internet users over the age of 50 had increased 5.2% year-on-year to account for 28% of total users. In addition, rapid business models driven by digitization have further reduced the capital and technical threshold for online goods and services operations across different categories, city tiers and price levels. This not only solves the problem of high online costs of consumer acquisitions, but also helps brands target consumers and their wallets more accurately and efficiently.

Source: National Bureau of Statistics

The impact of the pandemic on offline retail formats will gradually weaken thanks to the increasing portion of online sales, community-based formats and continuously refined pandemic prevention measures.

From the perspective of offline retail, with the impact of the pandemic on consumers' offline purchase habits, new trends are also emerging for offline formats. First, the pandemic has accelerated retail in catering and other services. For example, online catering and delivery have freed the offline service industry from previous restrictions in providing offline services, while improving efficiency and sales. Secondly, the pandemic has further shrunk the physical radius of consumers’ daily lives. At the same time, competition in fresh produce e-commerce and community-group purchases has also gradually encouraged companies to develop their offline business activities, including supermarkets, convenience stores and even shopping malls. These retailers are now opting to set up new stores within and around small communities rather than city centers in order to be closer to consumers, while also accelerating the digital transformation of their own business models. For example, promoting the implementation of home delivery models. In addition, offline retail accelerated the deployment of entertainment, social and leisure service attributes of business formats. For example, in the post pandemic period, the newly-opened shopping malls have gradually changed from traditional retail spaces to spaces with leisure, entertainment and social functions. Meanwhile, we see the convenience store has become a popular place for new product testing and socializing.

Source: National Bureau of Statistics

From the perspective of consumer goods, digitization and consumption upgrading will be the key factors affecting the growth of consumer goods in the post pandemic period.

As far as consumer essentials are concerned, these are less affected by external factors since they are necessities and hence have fairly inelastic demand. However, repeated outbreaks of COVID will push up demand rapidly for some categories of goods such as agricultural products, processed grain and oil, paper, household products and the like. At the same time, with the accelerated digital transformation of enterprises and the increasing demand of consumers for high-end, healthy and high-quality goods, leading companies are speeding up the development of premium brands. In addition, they also increase consumers' awareness and upgrade the brand by opening offline brand experience stores (such as brand coffee shops, beer bars, and snack stores). These measures will promote the rapid growth of essentials categories, including beverages, leisure food, pet food and fast food. And these categories will be favoured by more capital due to their "certainty" in terms of return on investment. According to Wind Data, the number of food and beverage enterprises account for the largest portion of consumer goods companies which have been newly listed on A-shares since 2020.

In terms of optional consumption, because it is non-essential demand, it will be greatly affected by external factors such as pandemics, changes in demographics, consumer preferences and fashions. In the future, for brands and businesses involved in the optional consumption category, a few factors will be key in determining the development of their enterprises: their digital insight into diversified, personalized and dynamic consumer needs, the operation ability of digital channels, and the category innovation, brand upgrading and product R&D ability around changes in consumer demand. Take apparel and footwear as an example. As this sector has matured, sales of major categories other than sportswear have been weak. With the acceleration of the digital transformation of leading sportswear companies, and the rise of Generation Z's preference for domestic brands, some leading enterprises quickly caught up with consumer demand through digital tools, identified a new breakthrough in the mature market, seized the trend of segmented market attributes of sportswear and accelerated their product R&D and digital promotion, which enabled them to achieve rapid growth during the pandemic.

Government and Public Sector

Urban renewal, smart city tech and green infrastructure

2021 is the first year of China's 14th Five-Year Plan period. "High-quality Development" has become the long-term development goal. As local governments will announce new leadership for the next five years before the 20th National Congress of the Communist Party of China, which will be held in Beijing in the second half of 2022, China's leadership expects a stable economic environment, as the long-term reform target might be rebalanced with a short-term demand for stable growth. The Central Economic Work Conference in December proposed "to maintain fiscal spending and accelerate the progress of spending", hence it is reasonable to expect a more proactive fiscal policy in 2022 given that the central government adopted a relatively conservative fiscal policy in 2021.

Under a proactive fiscal policy, infrastructure investment will continue to increase in 2022 with central, provincial and local governments investing more in urban renewal and green infrastructure.

Urban renewal is a systematic project in the 14th Five-Year Plan for many cities in China. It aims to improve the quality and efficiency of the existing outdoor space resources in urban built-up areas and improve urban functions. There will be investments in municipal infrastructure, including roads, corridors, parking lots, safety facilities and public spaces. Large-scale and mid-scale cities are likely to deploy more new infrastructure such as 5G, while shanty-town and old residential areas are also being pulled into the scope of urban renewal. Newly-established urban renewal platform companies are tasked to provide financing channels for infrastructure construction and to avoid the implicit debt problem.

Information technology is at the heart of the new plan for urban renewal. The Digital Twin program is driving smart city development to a new stage. Digital Twin city refers to the use of digital twinning technology to build a virtual city in cyberspace that mirrors the one in the physical world, to help the governments make decisions in a more accurate way. Smart city has been widely valued by the central and local governments in the last ten years. Since 2020, new applications in smart cities such as health codes and travel cards have played an extremely important role in epidemic prevention and control. Digital Twin city is clearly proposed in the outline of China's 14th Five-year Plan, with more than 20 provinces and cities regarding Digital Twin city technology as the key measure to improve city governance. In 2022, with more cities claiming to become a part of the Twin city action, the path to digital twin city construction will become clearer.

The other plank of urban renewal is cleaning up the environment through transformation of the energy generation and distribution within urban areas. In this regard, the government will promote green infrastructure investment, in and around urban areas. The State Council has issued the Carbon Peak Action Plan by 2030 to promote investment in green power and related infrastructures, including photovoltaic power, wind power, hydropower, nuclear power, and power grids and energy storage facilities. At the same time, the Plan stipulates the energy saving requirements and carbon reduction of municipal infrastructures.

In order to achieve the "carbon peak and carbon neutrality" goal, hydrogen energy, as a clean and low-carbon energy, is strongly supported by national policies. Since 2020, China has issued a series of hydrogen-related policies, further improving the policy framework for the development of China's hydrogen energy industry. It is expected that the State will release the top-level design of the hydrogen industry as soon as possible, and the development of the industry will continue to accelerate under the supporting policies of local governments.

As they require large investment and have a rather long gestation cycle, the clean energy projects require diversified financing. Both the central government and local governments are making a series of arrangements to increase investment and financing support for green industries, and government policy support is expected to expand in 2022. In November 2021, the People's Bank of China launched the carbon emission reduction support tool to encourage commercial banks to make loans to business in the field of clean energy, environmental protection, and carbon emission reduction technologies. And we expect to see more incremental financial support provided to the green sector in the following year.

Concomitantly, the government will continue its efforts to build a better business environment. More reforms will be launched in the fields of taxation, international trade, and the awarding of construction permits so as to bring domestic rules and regulations in line with international leading practices. With continuous improvement of laws and regulations, the Chinese government is committed to create a fair, honest and free market environment. Besides, the government will accelerate administrative reform through digital transformation to provide a one-station service to enterprises and individual users on basis of the interconnection between national, provincial and municipal government data platforms.

The State-owned enterprises (SOEs) will focus on strategic emerging industries. With scientific and technological innovation as an increasingly important goal, SOEs are being encouraged to invest more into the national basic research and applied basic research innovation system, especially in the areas of semi-conductors, new materials and new energy vehicles. The total revenue of SOEs for the first ten months in 2021 was RMB 60,386 billion, with a year-on-year growth of 22.1% and 9.7% on average over the past two years. Their total profit was RMB 3,825 billion, with a year-on-year growth of 47.6% and 14.1% on average over the past two years. Playing an increasingly more important role in the economy, SOEs are expected to foster a sustainable growth to resist the uncertainty.

Life Sciences & Health Care

Accelerating the construction of a ‘Healthy China’

Since the release of the Healthy China 2030 Plan in 2016, China's medical system has continued to improve, moving from "disease treatment" to "disease prevention". The pace has been further accelerated after the COVID-19 outbreak in 2020. 2021 is the first year of the 14th Five-Year Plan period, and the entire life sciences and healthcare (LSHC) industry has once again ushered in new changes. As of the end of 2021, China's LSHC industry has continued to develop in the three directions of "innovation", "digitalization" and "standardization", as well as supporting the evolution from “disease treatment” to “disease prevention”.

Health care reform and the acceleration of the construction of a ‘Healthy China’

As one of the key development industries in the country, China's LSHC industry has undergone massive changes and new achievements in 2021 resulted from various policies and guidelines from different dimensions. At the moment, government agencies are promoting medical pricing reform to increase the coverage of the National Reimbursement Drug List (NRDL) and Volume-based Procurement (VBP) scheme to eventually achieve ‘the home-growns to replace the imports’ goal, to control price rises in drugs and medical consumables, and increase the efficiency of medical insurance fund usage. Key milestones for health care reform in 2021 include:

- The clarification and implementation of the hierarchical medical treatment system in public hospitals: this was responsible for improving the utilization rate of limited medical resources, expanding the coverage of treatment, using digital technology to break through geographical constraints, and gradually achieving more efficient and broader coverage of medical services.

- Reform and innovation of payment model: The establishment and promotion of innovative payment models such as DRG/DIP payments, online medical insurance reimbursement, and off-site settlement made rapid progress in 2021, profoundly changing the medical insurance payment landscape in China.

- Technology to improve the system and promote healthcare equity: The process of digital healthcare development continues to advance with the reform of medical insurance payments, the construction and development of IoT, 5G, AI and so forth.

On the other hand, under the influence of factors including domestic substitution of imported drugs, VBP normalization, and industrial upgrade through digitization and information technology, LSHC enterprises are also implementing an upgrade of the entire industrial chain, from R&D to marketing. This has led to some profound changes in the Health Care and Life Sciences landscape:

- Foreign-owned enterprises strengthen local deployment and localization

In 2021, human genetic resources (HGR) related requirements are officially incorporated into Biosafety Law and are in the process of being added to PRC Criminal Law. To foreign enterprises, the localization of R&D capabilities has become increasingly important over recent years. Some foreign enterprises have built local R&D centers in China for ‘in China, for China’ purposes, while others are using localized vendors, including global vendors based in China or domestic vendors, for local data analysis. - Local enterprises - innovation breakthrough and China-export

Ushering in the innovation harvest period and policy support, local pharma, and medical devices enterprises have achieved domestic substitution acceleration in 2021. The proportion of innovative drugs produced locally and approved by the authorities has increased from 26% in 2019 to 72% in 2021 YTD1, surpassing imported ones in 2021. Meanwhile, as of Nov. 2021, a total of around 48 license-out deals have been announced with a disclosed value of around RMB 43.6 billion2, double the disclosed deal value in 2020. This shows that domestic innovation strength has started to become recognized globally.

Data-manage pain points and talent shortages magnified under the rapid development

With the rapid upgrading and development of the whole industry, a few issues have gradually come to the fore, such as digital technology applications, the management model of enterprises and institutions in response to the new mechanism and market, and the shortage of industry talents.

- Difficulty in storing and sharing clinical data in the era of digital intelligence

Unlike other industries, clinical data come with higher requirements in relation to storage and security. Proper data storage and washing of data has become particularly important from enterprises to medical institutions in the face of greater penetration of the information infrastructure. To efficiently use clinical data in innovative product development and in the upgrade of medical services, the protection of patient privacy has now become a big priority for all parties in the market. - Challenges in forming new management models to adapt the medical reform and new system

For all enterprises and institutions in China's LSHC industry, the reforms have meant that new management models have to be developed quickly and many barriers must be overcome, such as hospital cost management under the diversification of payment channels, R&D and marketing for innovative products under the VBP normalization, and digitization. - The shortage of multifunctional talents in cross-industry cooperation is an obstacle to development and transformation

The issue of multifunctional talent shortage has become magnified with the development of ‘internet +’. In the transitional stage of hardwiring the internet into healthcare services and R&D, it is important to have talents with deep knowledge of the LSHC industry while having a solid understanding of internet technology at the same time. The competition for limited talents in the market has caused some obstacles to development and transformation.

Innovation brings in new doctor-patient interaction models and product offerings. Digitization brings in breakthroughs in development bottlenecks and geographical restrictions. Standardization ushers in changes in the market and a revamp, resulting in a healthy new market landscape. We foresee that China’s LSHC industry will witness another round of reform in both the medical system and the LSHC market in the upcoming years.

As one of the few industries that has grown during and after the outbreaks, the development of a ‘Healthy China’ has further accelerated in terms of technological breakthroughs in the upgrading of the entire industrial chain as well as the improvement of policies and regulations. Along with China’s demographics moving towards an aging population, there will be further growth in demand for more personalized and technological medical services. Elderly care services and commercial insurance will become one of the key fields to develop in the next few years. In addition, AI applications and industry-university-research cooperation, which is facilitating the R&D innovation breakthroughs we have witnessed this year, will also continue to be developed. New industrial models, formed by the integration of digital technology, will also become one of the key directions of future transformation for LSHC players.

Climate change & sustainability

Improving emissions reduction mechanisms, accelerating green competition

2021 has been marked by unprecedentedly high degree of attention being paid by the private sector to decarbonisation. The Chinese government announced a pledge to ‘hit the carbon peak by 2030 and achieve carbon neutrality by 2060,’ and has since released a slew of policies to further this aim. Regardless of the varied speed and extent of responses from different industries, businesses are being encouraged to adopt a multi-dimensional performance matrix due to the increasing regulations, competition in low-carbon business models, and green consumption demand. In addition, the refining of emissions reduction policies, accelerated construction of renewable energy sources, and the greater synergy with market-oriented approaches, will accelerate ‘green competition’, reshaping companies' competitiveness.

Strengthening of emission reduction policies accelerates phasing out energy- and carbon-intensive industries

The 14th Five Year Plan period is critical for carbon peaking, raising energy efficiency, lowering energy intensity and carbon intensity. In the coming year, action plans of certain key industries, such as coal power, steel, chemicals, construction materials, nonferrous metals are expected to be published. Green standards will be perfected and regulatory pressure will increase accordingly.

In 2021, the State Council released Chinese government's guiding document on carbon peaking and carbon neutrality, as the lead of its "1+N" decarbonisation policies. "1+N" policies include "1", the guiding document, and "N", action plans of particular industries to decarbonisation. Meanwhile, the coverage of the national ETS will be enlarged to include industries such as nonferrous metals, construction materials, steel, and the like. The quota distribution and trading mechanism will be upgraded to further unleash the financial nature of the ETS. Companies with lower emission reduction maturity will be faced with increasing compliance pressure due to the uncertainty of the price of carbon. Besides, China starts to institutionalize methane reduction. Technological readiness will increase the competition between industries and businesses. Last, the advancement of carbon emission MRV (monitor, report, verify) methods and mechanisms will have a deep impact on the whole industrial chain, speeding up the phase out of energy- and carbon-intensive entities.

Accelerating renewable energy construction keeps the balance between development and emission reduction

The Central Economic Work Conference in early December pointed out that to transit the "double control" from energy side to carbon emission side, and the energy "double control" mechanism will no longer include energy consumption from newly-installed renewables and fossil fuels used as raw materials for manufacturing. It implies a pathway towards increasing renewables supply like solar PV, and utilizing fossil fuels in a clean and resource-oriented way, which to some extent alleviates the emission reduction pressure faced by petrochemical industries. Renewables is placed at a strategic position to secure the dynamic equilibrium between economic development and emission reduction.

The change of focus from energy consumption and intensity, to carbon emission and intensity, is inevitable. Increasing the supply of renewables is circumscribed by limited land availability and cost, therefore it is crucial to guarantee that the renewables are installed and consumed in an efficient manner. Under the guise of "Prioritize Saving" and lifting energy efficiency, it is expected that the government will speed up the introduction of comprehensive regulations on renewables.

Improving market-driven mechanisms, carbon asset management becomes a key to success

Carbon emissions are being translated into credit and assets. China is building and connecting its national ETS, power consumption credit market and electricity trading market. Globally, it has kicked off the set up of an international ETS. More diverse carbon credit products such as voluntary emission reduction (VER) and inclusive emission reduction (PHER) are being mainstreamed. Linkage between an emission entity's cost-effectiveness and its carbon asset management capability is being strengthened. Leading companies have already taken actions, not only to focus on energy saving and emission reduction of their own facilities but also checking its full lifecycle emission inventory, cooperating with eco-chain partners, and empowering themselves by adopting a set of tools to realize the value of emission reduction.

Glasgow Financial Alliance for Net Zero, including financial institutions which manage nearly USD 130 trillion (40% of the world's private capital) has announced that they will align their investments with the Paris Agreement goals. China's financial regulatory authorities are accelerating the introduction of pro-emissions reduction financial instruments. International communities are uniting behind the sustainable finance standards. Sustainability within the company’s activities will be further linked to its capacity to garner financing. Under this trend, it is particularly important for companies to maintain their competitiveness by both technological and market-oriented approaches, and to improve their carbon asset management capability.

MNC Pulse

Foreign businesses staying the course

Multinationals will go into 2022 with a cautiously optimistic outlook on China's business environment. As firms in China are gradually returning to pre-pandemic levels of revenue growth after a better than expected economic recovery, multinationals will look to increase the level of investment in their China operations. According to a survey by HSBC of more than 2000 multinationals, 97% will continue to invest in China in 2022, 42% of which will invest between 11% and 25% of their operating profits domestically. The lure of China's sizable market and its favorable economic prospects, in addition to domestic innovation and sophisticated supply chains, are the primary factors behind their planned investment.

Following on from previous years, foreign companies will double down on their China operations next year. Only 9% of European firms have any plans to move operations out of China, which, according to the European Chamber of Commerce, represents a record low in the survey's history. Instead, companies will continue localizing their operations by onshoring production and bringing more of their value chains over to China, while also looking to expand their market share. The exception here is companies which have sensitive technologies related to national security. Among such Japanese businesses, 42% either have considered or are considering plans to diversify supply chains out of China.

Market openings also present an opportunity for MNCs to scale up. As equity restrictions have been lifted in several sectors, a number of European businesses in joint ventures (JVs) have taken controlling stakes or bought out their Chinese partners entirely in response. With new market openings on the horizon, such as a revised Negative List for Foreign Investment and complete removal of equity investment caps on passenger vehicle makers in the automotive sector in 2022, it is reasonable to expect that increased investment will be welcomed wherever possible. However, as has long been the case, lagging implementation and structural barriers will likely remain an obstacle preventing many businesses from fully capitalizing on new openings.

Moving into next year, multinationals will increasingly look to tap into opportunities arising from two underlying trends: China’s domestic technological innovation and climate ambitions. China's lead in the adoption of advanced technologies such as AI, cloud solutions, 5G and IoT, in addition to a thriving digital economy, will afford new opportunities for foreign businesses across all industries. MNCs also look favorably on the Chinese government's net zero agenda. Among European firms with their own carbon neutrality target, approximately half aim to reach net zero before 2030, largely by decarbonizing energy use and decreasing energy demand. With already high environmental standards, many MNCs will play pivotal roles in leveraging their expertise and technologies in helping China realize its national carbon reduction targets.

Source: British Chamber of Commerce in China

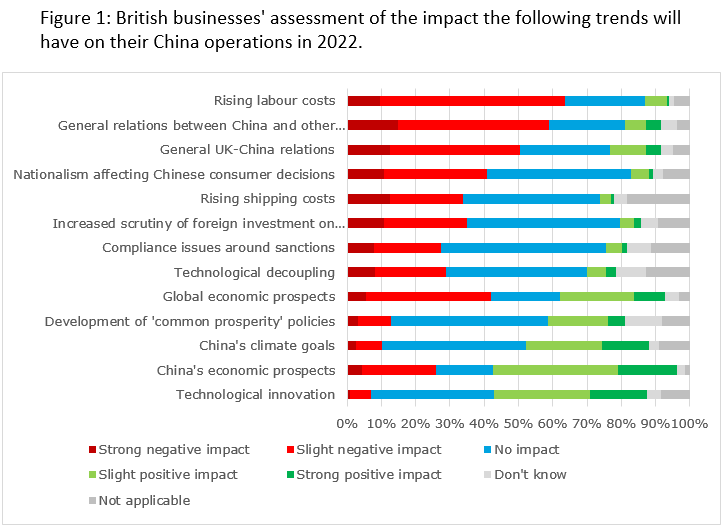

Despite considerable media speculation, businesses will maintain a pragmatic approach to government actions surrounding common prosperity, and they will wait and see if any detailed policies emerge from what currently represents a lofty policy strategy. Currently, 42% of British companies don't expect this to have an impact on their operations in 2022, according to the British Chamber of Commerce in China. Another 23% in fact predict that common prosperity will have a positive effect on their business, with the likelihood of related policies helping to boost incomes and add to an already growing middle class.

Some of the most prevalent challenges MNCs will have to navigate in 2022 come down to talent. An exodus of foreign employees and executives out of China is likely in the coming year due to travel restrictions remaining in place and changes to the preferential individual income tax regime for expatriates. Despite speculation that China's border restrictions could be eased after the 20th Party Congress in November, the sudden emergence of the highly transmissible Omicron variant now makes it unlikely. China's borders will remain closed into the new year. This will further accelerate broader localization trends among multinationals that are already underway. MNCs will also have to grapple with rising labor costs, as well as a high turnover of local staff as a growing tide of employees leave for Chinese competitors. 60% of American Chamber of Commerce in Shanghai members report that local employees are leaving for Chinese competitors due to better career prospects, and 55% cite better compensation. Foreign firms will therefore need to carefully consider what else they can provide prospective talent beyond high salaries, such as company values, a sense of personal fulfillment and diversity in career growth paths.

Other thorny challenges arising from geopolitical tensions and an increasingly restrictive cybersecurity landscape will also persist into next year and beyond. Yet, despite these, approximately 60% of American and British companies continue to view China as a top-three priority market in their near-term investment plans. In the light of a relatively uncertain global economy, multinationals have little choice but to continue navigating China's increasingly complex business environment if they are to remain global players in their respective industries.