Perspectives

The Deloitte Research Monthly Outlook and Perspectives

Issue 72

4 March 2022

Economy

Managing the economic fallout from Ukraine

Having caught many of us off guard, the impact of Russia's invasion of Ukraine will ripple right across the global economy. Global financial markets sold off severely last Thursday but rallied sharply on Friday following somewhat limited sanctions against Russia from the West. This rally proved short-lived, and more worryingly, renewed upward pressure on prices of crude oil, natural gas and commodities have raised the risk of stagflation. More sanctions have since been unveiled, including the decision to cut off selected Russian banks from SWIFT. The Russian Ruble has tumbled by nearly 30% against the dollar so far and weaknesses have persisted while Kyiv remains under siege. However, these sanctions, while tough, have not been wholesale. For example, there has not yet been a complete ban on SWIFT and European governments have held off on an embargo of Russian energy. The degree of solidarity among Western governments has nonetheless been greater than anticipated.

For China, war between Russia and Ukraine has presented a number of considerations and unknowns, both economically and geopolitically. First and foremost, the outlook on inflation will worsen. Unlike spikes caused by higher demand, supply shocks will increase the risk of stagflation for major economies (particularly for energy importers). The Federal Reserve is still expected to raise the Fed Fund Rates in the next Federal Open Market Committee meeting (on March 15 and 16), but a previously anticipated 50bps will be off limits, and instead a 25bps is more likely. Heightened volatility of asset markets might be seen as a deterrent to a large dose of interest rate tightening by investors, but the US equity market was susceptible to profit-taking before Russia's invasion anyway. True, such heightened volatility is an effective form of tightening through wealth destruction, but on a two year view, the Fed's efforts in normalizing interest rates are set to continue. We are still of the view that there will be five hikes this year and two to three in 2023.

Second, how to quantify China's economic and financial connectivity with Russia? Russia's direct exposures to Hong Kong as a financial center is negligible (listing and insignificant participation through syndication of loans). The real question is to what extent Russia would have to switch to RMB settlements should its financing activities be crippled by an inability to access to SWIFT. Clearly, China could lend some indirect support through imports of Russia's agricultural goods and energy products, but even growing China-Russia trade is dwarfed by Russia's trade with the EU whose value was USD 280 billion in 2021 (China-Russia trade totalled USD 147 billion that same year).

Charts: Russia's dependence on trade and investment with Europe

Source: Wind

Third, unlike the US, almost all economies in Asia are net importers of crude oil and natural gas. If crude oil prices stay above USD 100 per barrel, most Asian economies will surely see higher inflation and some of them (e.g. Thailand and the Philippines) could experience fiscal difficulties as governments must step in by increasing fuel subsidies. For China, intense competition in down-stream industries will keep inflation at bay, but many firms will have to endure even greater profit-squeezes due to higher energy prices and more expensive commodities whose prices tend to move in tandem with energy products. Will all of this prompt China to quicken the pace of its energy transition away from oil and gas in response? A sharp departure from the government's current energy strategy is unlikely, but policymakers remain no less committed to reaching net-zero, despite the "tax on growth" and liberalization of energy prices that wholesale carbon reduction will entail. One of the key lessons from last year's power crunch was that policy coordination is important. We do not think there will be another campaign style of carbon reduction this year and reliance on price signals implies higher electricity tariffs for consumers. This is not easy against a backdrop of higher imported inflation.

Meanwhile, based on lackluster data in land sales and property transactions so far this year, the property sector is not expected to see a revival in terms of investment. The good news is that the residential market is getting extra support in addition to recent monetary easing, and eased restrictions (Heze in Shandong rolled out lower initial down payments on home purchases two weeks ago and we expect more cities to follow suit) ought to be viewed as a clear signal of encouraging consumers to increase their leverage amid an economic slowdown. In practice, the long-touted property tax will be put on the backburner. Our baseline scenario on the property market remains that property markets in first tier and most second tier cities will be well supported by pent-up demand, but less impressive land sales will weigh on local governments' fiscal revenues in 2022 and beyond.

On policy responses, monetary policy will be guided with focused easing as we have been advocating for all along. But in light of geopolitical risks in Europe and indirect exposure to Asia, investors could flock to safe haven currencies such as the dollar, Swiss franc and the Japanese yen, and as such, interest rate differentials between China and the US which are less than 100bps are unlikely to be sustained unless the appreciation of the RMB exchange rate is halted. Greater risk aversion will also naturally reduce portfolios around emerging Asian markets in the short run. Again, we would like to reiterate our view that a strong RMB may not undermine China's competiveness (it won't help for sure), but it will limit the effectiveness of intended monetary easing.

The crisis in Ukraine will reinforce the key role of fiscal policy because elevated commodity and energy prices will make fiscal relief or tax cuts to SMEs in more competitive downstream sectors more compelling. But will the conflict introduce yet another element of global distrust, and in turn, reinforce the notion of supply chain reconfiguration in the medium term? We believe that the current situation will exacerbate underlying geopolitical tensions, but this will have little tangible impact on decoupling. Finally, we expect the upcoming Two Sessions to stress stability, but policymakers will refrain from setting an explicit GDP growth target for this year.

Financial Services

Credit easing continues to drive steady growth

In December 2021, the Central Economic Work Conference (CEWC) set a new policy direction of prioritizing stability while pursuing growth. In accordance with this objective, the People's Bank of China lowered the reserve requirement ratio (RRR) and market interest rates in rapid succession. However, January 2022’s financial indicators significantly exceeded the expectations of the market. Credit conditions are expected to remain "stable and loose" for the rest of this year as the 20th CPC National Congress will be held in the second half of the year.

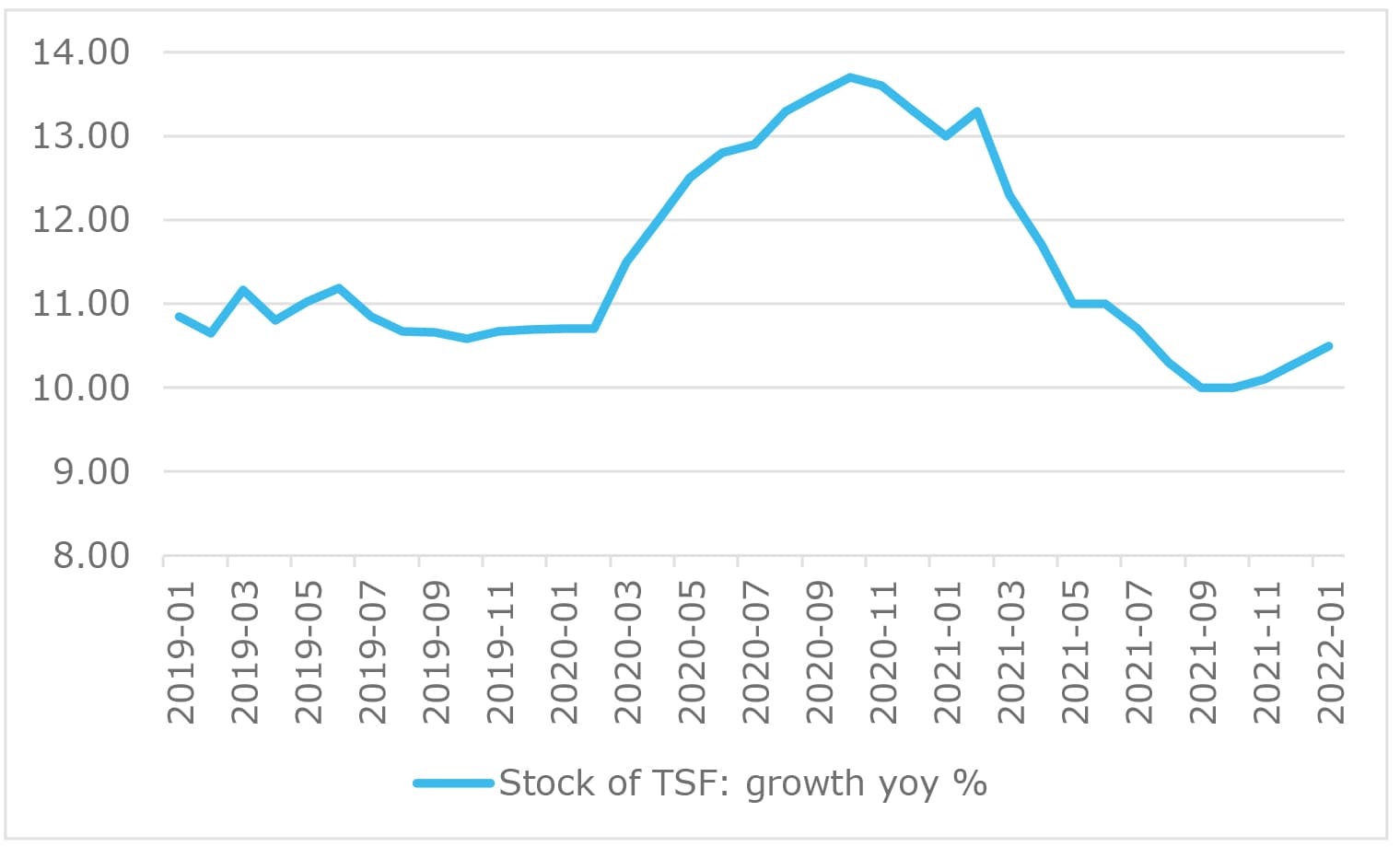

Total Social Financing (TSF) increased to a record high in January

Concerned that China's economy was under pressure from demand contraction, supply shocks and weakening expectations, the CEWC called on financial institutions to increase their support of the real economy, particularly small and micro businesses, scientific and technological innovations, and green development, ushering a certain degree of financial easing.

In January 2022, new TSF totalled RMB 6.17 trillion, hitting the highest monthly figure in history and significantly exceeding the RMB 5.45 trillion expected by the industry. The overall TSF outstanding increased by 10.5% YoY, rising for three consecutive months since the fourth quarter of 2021. RMB loans to the real economy rose by RMB 4.2 trillion in January, the highest monthly figure, and a YoY increase of RMB 380.6 billion. Credit data for January shows that the new policy initiative is off to a good start.

Chart: Overall TSF rebounds for three consecutive months

Source: Wind

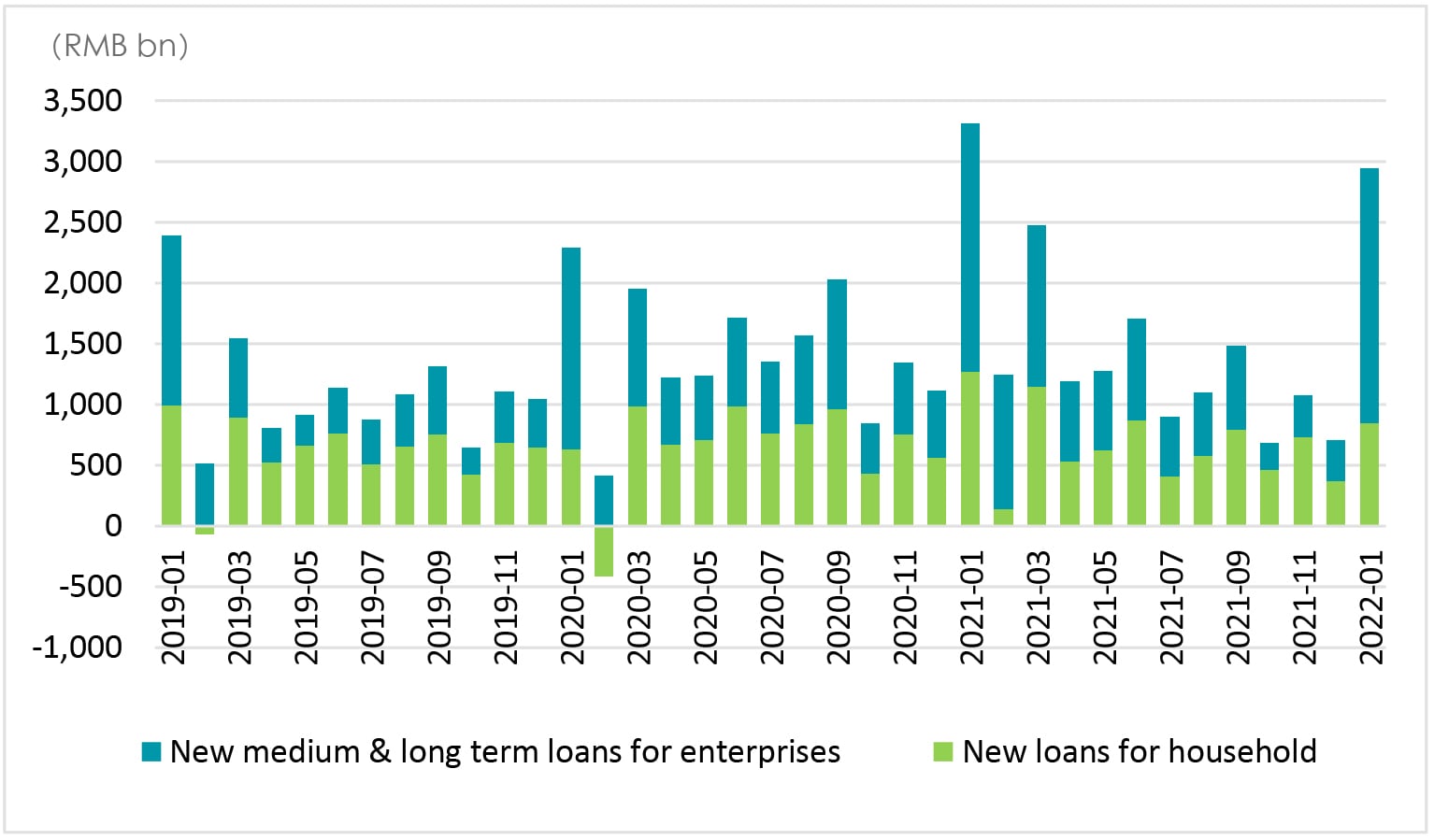

Credit structure needs to be continuously optimized

As far as the credit structure is concerned, the continuous recovery of consumer demand and medium and long-term loans are the key points for the steady growth of subsequent credit.

On the one hand, epidemic prevention and real estate control measures have continued to dampen people's willingness to consume. In January, short-term and medium & long-term household loans increased by RMB 100.6 billion and RMB 742.4 billion respectively, 227.2 billion and 202.4 billion less than the same period last year. As consumer demand has not yet fully recovered, the CEWC proposed to "implement a strategy of expanding domestic demand and enhancing the endogenous power of development". Thus, it is now possible to issue consumer vouchers and loosen housing interest rates. These have been put in place to stimulate domestic demand and boost consumer confidence.

On the other hand, medium & long-term loans to enterprises increased RMB 2.1 trillion in January, an increase of RMB 60 billion YoY, the first YoY increase since the second half of 2021. The Central Bank disclosed that the weighted average interest rate for corporate loans in 2021 was 4.61%, the lowest it has ever been in the four decades since China's reform and opening-up began. The RRR was cut twice last year, and financial institutions will provide greater support to the real economy this year. The LPR (money market interest rate) cut in January is expected to make sure that real lending rates continue to decline, so that total credit continues to grow in the coming months.

Chart: Medium & long-term corporate loans pick up, and consumer demand starts to recover

Source: Wind

However, if the real estate sector continues to be a drag on the economic recovery, which is our assumption, interest rates are inevitable but room for cuts is limited (please refer to macro commentary). In an environment of interest rate reduction, the loan yield of banks will decrease in the short term but credit easing will lead to an improvement in enterprise operations, and the resulting stabilization of the economy will contribute to the soundness of bank asset quality. Thus, banks' net interest margin is expected to remain stable in 2022.

Consumer

Chinese fast-food chains on the fast track

Though it is still early in the year, the Chinese fast-food industry has already witnessed a remarkable increase in initial public offerings (IPOs). This month alone a number of fast-food enterprises, including Country Style Chicken, Hefu Laomian and Yang Guofu, announced their listing plans.

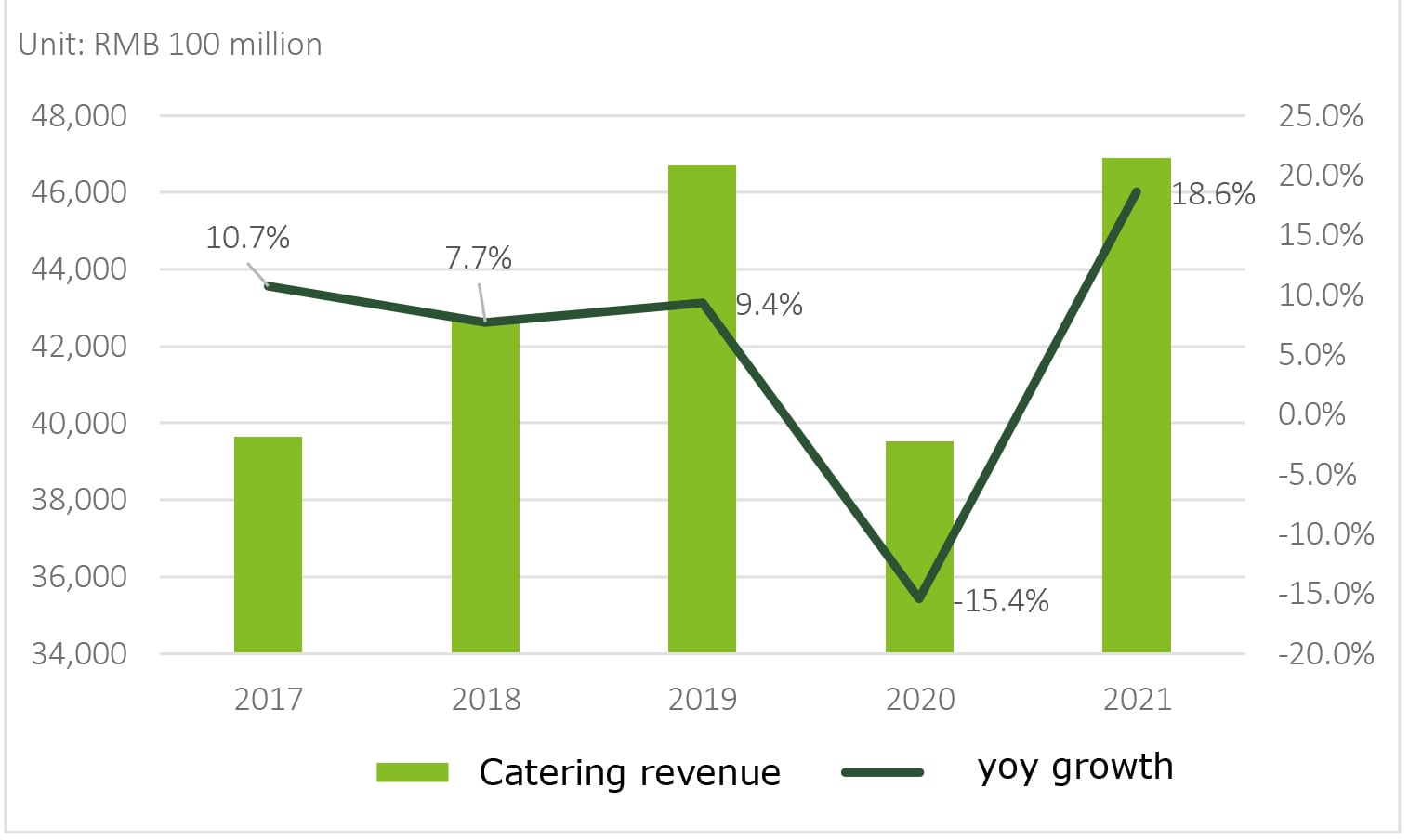

Data from the National Bureau of Statistics (NBS) reveals that the pandemic continues to impede the recovery of the catering industry. Catering revenue in 2021 totalled RMB 4,690 billion. Although it increased by 18.6% year-on-year in 2021 thanks to the prior year’s low-base comparison, the compound growth rate from 2019 to 2021 was only 0.19%. In contrast to the slow recovery of the catering industry as a whole, Chinese fast food chains demonstrated a rapid recovery in 2021. Country Style Chicken’s IPO prospectus states that although its revenue experienced a slight decline (-3%) due to the pandemic in 2020, its income in the first three quarters ending September 30, 2021 has exceeded the total annual income of 2019 by 5.4%.

Figure: Catering revenues in China, 2017-2021

Source: NBS

In the post pandemic period, growth in Chinese fast-food chains is clearly on the fast track. Euromonitor data shows that the fast-food chain store penetration rate in the United States is over 50%. While data collected by the catering school of Meituan University, the fast-food chain store penetration rate in China was only 16% in 2020, which means that there is enormous potential for growth.

Chinese fast food chain companies have accelerated the listing process after the pandemic for two reasons. First, companies are eager to secure financing via the IPO channel so that they can expand their businesses. Second, they are keen to take advantage of a more relaxed listing environment thanks to the implementation of the securities issuance registration system which removes the requirement for getting government approval of an IPO a year in advance. IPOs will only need a confirmation that the companies’ issuance breaches no regulations and does give a quick boost to cash liquidity in the market. The latter is especially important considering the corporate cash crunch created by the pandemic.

We see the main factors driving the rapid growth of Chinese fast-food chains as follows:

- The upgrading of consumer demand has promoted the rapid development of the Chinese fast-food sector. In recent years, both per capita disposable income and per capita food consumption expenditure of Chinese residents has increased, and the focus of fast-food consumption has gradually changed from ‘being full’ to dish taste, safety and health, dining environment and lifestyle. The increasing income and upgraded consumption habits of Chinese citizens has also made fast-food preferences in differently tiered cities across the country more diverse, and consumer’s price sensitivity has also decreased. Generally, Chinese consumers, especially the working class, are more loyal to Chinese fast food, which focuses on "porridge, noodles and rice", than to their higher calorie western equivalents. Demand for fast food has also grown because of lifestyle changes within the Chinese population. The increase in the pace of daily life has reduced the time citizens have to cook from scratch and increased the frequency of dining out or ordering take out. In addition, in recent years, Chinese fast-food chains have increased their investment in catering environment decoration, dish R&D, food safety, and meeting consumers’ increased demands for healthy food and personalization of service.

- Industry standardization and the rapid improvement of supply chains. In the past, there had been many issues hampering China's catering supply chain market, such as weak awareness of professional division of labor, lack of refined process management, imperfect infrastructure such as cold chain logistics and so on. In recent years, with the rapid increase of consumers' demand for dining out and the gradual expansion of the scale of Chinese fast-food chain stores, cross regional Chinese fast-food chain brands have begun to build centralized kitchens and carry out lean and standardized management of the supply chain in order to provide standardized products in each store. The emergence of some specialized catering supply chain service enterprises has helped fast-food chain enterprises make product customization viable to solve taste problems, process problems and product innovation problems.

- Digital technology has also helped to improve efficiency in the fast-food chain. Digital infrastructure such as O2O platforms and WeChat mini programs have helped to take catering digital, thereby increasing the scope of catering operations. For example, takeout order scheduling and online booking systems have improved the back-office operating efficiency of the Chinese fast-food chains. At the same time, to further ensure food hygiene and reduce the pressure on the kitchen labor force, some catering chains try to improve efficiency with artificial intelligence, such as food-serving robotic arms and meal delivery robots. While improving efficiency, these high-tech tools have increased the popularity of the brands on social media and improved the dining experience of customers.

Although the business models of Chinese fast-food chains have matured a lot in the last few years, the industry still faces many challenges. On the one hand, the cooking methods and flavor of many Chinese dishes are unique and resist excessive standardization. To ensure that the taste of the fast-food dishes meet consumer expectations, companies will have to come up with different configurations of on-site vs. off-site (centralized kitchen) preparation and standardization, based on the particular needs of each dish. On the other hand, the fast-food industry has low barriers to entry and is easily replicated. To combat this, companies need to increase consumer’s familiarity with their brand either by creating a unique taste, or by providing excellent service or through creating a special decor for their stores. Continuous links with consumers through social media and community sharing need to be established. Fast food chain enterprises also need to develop new innovative products on a regular basis and to continuously improve existing products and make full use of online channels to promote their products.

Government & Public Services

State-owned capital to lead urban renewal projects

Based on available public data, by the end of 2020, China's urbanization rate had reached 63.89%. In megacities such as Shanghai and Beijing, the urbanization rate hit more than 80%. Faced with such a rapid increase in the urban population, the government has decided to try to divert urban development work from developing new urban areas to upgrading current urban districts. Hence, today more and more first-tier and second-tier cities are choosing to carry out urban transformation via urban renewal programs rather than adding to the burden of existing infrastructure by increasing the size and the scope of their cities.

An urban renewal project differs from a typical commercial development project in many ways. For one, urban transformation is more complex and needs participants with higher operational capabilities. Thus urban renewal projects require a lot of supporting infrastructure and services. Moreover, unlike new developments, project investment is high and the investment period is long, with cash outflows barely covered by inflows. Therefore, project financing has always been the most difficult part of any urban renewal project.

Since new regulations to prevent large-scale demolition and construction were issued by the Ministry of Housing and Urban-Rural Development in August 2021, numerous cities have suspended urban renewal projects and begun to review the existing projects. As a result, the industry threshold has been raised and more and more local State-owned enterprises have become the main players in urban renewal. In addition, urban renewal funds led by the governments and State-owned enterprises have gradually become the main financing vehicles of urban renewal projects, such as the RMB 80 billion Shanghai Urban Renewal Guidance Fund launched by the Shanghai Real Estate Group and State-owned enterprises, the RMB 60 billion Tianjin Urban Renewal Fund jointly launched by Tianjin Urban Investment Group and State-owned enterprises, and the RMB 30 billion Wuxi Urban Renewal Fund jointly established by the Wuxi Urban Construction Development Group with 13 financial institutions and real estate enterprises.

Compared with other financing methods, an urban renewal fund has significant advantages:

First, urban renewal funds can work as equity to leverage bank loans for the project. According to the Circular of the State Council on Strengthening the Finance Management of Fixed Asset Investment Projects ([2019] No.26), infrastructure construction projects are encouraged to raise funds and other financial instruments to enhance equity in order to reduce reliance on bank loans.

Second, urban renewal funds face fewer restrictions and less regulation and they can be used for relocation compensation and land acquisition much more easily. In particular, if the ultimate investors are not financed via any asset management products, they will not be regulated at the private equity level. At present, the pre-financing of real estate projects is strictly regulated and the financing cost is high. Hence, more and more cities prefer to choose urban renewal funds to pay for relocation compensation and land acquisition.

With the registration of urban renewal funds this year, the expropriation and land acquisition of urban renewal projects led by governments and State-owned enterprises will proceed rapidly in 2022. This will attract the participation of various financial investors. During the annual Central Economic Work Conference held in Dec. 2021, it was proposed that infrastructure construction should be driven "moderately ahead" while the real estate industry should be turned into "a sustainable cycle". Urban renewal could play an important role in pushing infrastructure construction "moderately ahead" and "promoting a sustainable cycle" in the development of future real estate projects. Digital community, digital medical treatment, digital consumption, digital tourism and other greater interpenetration of digital technologies will become highlights of urban renewal projects, and will drive the demand for related hardware and software facilities. The government and State-owned enterprise-led urban renewal will focus on predictability and rationality in the early planning stages, as well as financing investment in the whole project cycle so as to realize the multiple goals of urban digital transformation and steady economic growth.