Perspectives

The Deloitte Research Monthly Outlook and Perspectives

Issue 77

21 September 2022

Economy

Fourth quarter comeback still to play for

The Chinese economy may have already emerged from its cyclical trough in Q2 of 2022, but the road to recovery has not been smooth. The summer heatwave led to electricity rationing in several major cities such as Chengdu and Chongqing, a booming economic area with a population of 50m. Meanwhile however, retail sales, a proxy for overall consumption, has maintained its steady pace of growth, while auto sales were a pleasant surprise in August (passenger car sales saw YoY growth of 28.9%). This has reinforced our long-held assertion that Chinese consumer resilience is often underestimated. As supply chain disruptions were eased on the back of Shanghai’s reopening following a lockdown that lasted for more than 60 days between March and June, China’s export boom was further bolstered by both price effects (global inflation) and improved logistics. Such price effects were particularly evident in China’s surging exports to certain economies (e.g., exports to India grew more than 50% YoY in both June and July).

Meanwhile, the recovery faces three noticeable headwinds – 1) a struggling property sector; 2) financial stress brought about by global tightening which has gathered momentum as of late; 3) the draconian zero-Covid policy.

Chart 1: Property investment has been shrinking since Sep 2021

Source: Wind, Deloitte Research

Chart 2: Pressure weighing on finishing property construction

Source: Wind, Deloitte Research

Property sector data for August effectively extended weak trends from previous months which began in September 2021. Sagging housing sales and investment levels have reinforced the bearish sentiment in offshore markets where bond yields of major developers such as Country Garden and Greentown are hovering at around 30% and 10% respectively. Taken together, data around investment, land auctions and home sales suggest that weaknesses in the property market are likely to persist beyond the short-term, meaning that the property sector will likely be a drag on overall growth for the next few years. In the immediate term, the policy objective is to get developers to finish their projects and to prevent the mortgage boycott from spreading further. A relief fund of RMB200bn was set up in late August with a stated mandate of finishing incomplete projects, but markets seem to have second-guessed its effectiveness. We are of the view that the government will not move away from its current stance that “homes are for living in, not for speculation”, but the reality is that local governments can only reduce their reliance on land sales in the medium-term. Therefore, even in the absence of a potent stimulus to support the property sector, the policy mix will ultimately have to be aimed at preventing consumers from increasing their savings rate. Ideally, mortgage rates could be guided lower while developers would be incentivized to complete their projects. For most Chinese consumers, they view property in terms of both consumption and investment. Banks will therefore have to sacrifice some profits through a narrowing of interest rates in order to provide future homeowners with more sweeteners. The question is to what extent commercial banks could lower the cost of capital against a backdrop of global monetary tightening. In our view, the PBOC could nudge banks to bring down mortgage rates more, say to 100bps, but ultimately, meaningful monetary easing could only be executed if the exchange rate is more flexible. On the latest development, major banks have slashed deposit rates on Sept 15 by 10 to 15 bps, a pre-emptive move of lowering lending rates. China’s favourable balance of payments and relatively benign inflation allow the PBOC to deviate from Fed’s tightening, but external environment does matter. The message from Jackson Hole where central bankers gather each year was unambitiously clear – major central banks such as the Fed and the ECB will have to continue their tightening crusade, even it means that the real economy may suffer. The latest move by the ECB of hiking interest rates by 75bps, announced on September 8, has confirmed such policy bias. The Euro has received a rare respite from the ECB’s hawkish signal and rallied above parity against the greenback, but an overwhelmingly bullish sentiment towards the USD remains intact, as evidenced by a further slide of the Yen (USD/JPY has risen above 142, another 25-year high). If the dollar stays strong due to the Fed’s tightening campaign and current woes in some emerging markets, more central banks will have to step up their monetary tightening efforts.

This is the case in Asia where most central banks will have to raise interest rates twice during the remainder of 2022. Again, the two largest economies in the region, China and Japan, have to reflate their economies for different reasons. For Japan, so long as domestic inflation is under control, a weaker Yen will have no downside. Unlike 25 years ago, China is the largest trading partner of most regional economies, and a rapidly depreciating Yen has had a relatively muted impact on regional currencies. The decision taken by the PBOC to guide USD/CNY close to 7.0, a psychological threshold, has surprised the market but not us. Our 2022 USD/CNY forecast of over 6.9 in the beginning of the year was based on China’s need to improve the effectiveness of monetary policy, not competitiveness. The question is whether China should adjust its exchange rate more meaningfully in sync with other central banks’ competitive depreciation policies (e.g., Korea). In our view, the PBOC is unlikely to replicate the BOJ’s reflation strategy on the grounds of stability. Meanwhile, rising interest rates globally may cause risky assets in most emerging economies to underperform until US interest rates peak. The next FOMC meeting will present a stern test as investors remain unconvinced that the Fed’s drastic rate hikes could easily arrest stubborn inflation.

The final challenge is Covid. Based on recent mobility data (passenger flows during Mid-Autumn Festival shrunk by 37.7% YoY), travel-related sectors have taken an additional hit as partial lockdowns have been implemented across many cities. The dynamic zero-Covid policy has made a recovery in Q3 more anaemic than previously expected, but it will always be possible to further optimize the current policy as we continue to learn how to better deal with the virus. Assuming lockdown measures would become more calibrated in Q4 and with the Fed entering its latter stages of tightening over the next couple of months, a recovery in Q4 remains on the cards. As such, we stand by our original 2022 GDP forecast of 3.5% with an asterisk.

Technology

Is the auto industry ready for the Metaverse?

From launching platforms that connect virtual and physical worlds, to rushing to register Metaverse-related trademarks, major auto makers have already entered the race to dominate the Metaverse market. In 2022, Metaverse related initiatives such as virtual reality communities and art collections have become among the latest fad in the automotive market.

Two important developments have helped the Metaverse find its footing in the automotive industry – improvements in technology and the need to provide a good customer experience. On the technology side, the development of autonomous driving and other A.I. related technologies can be used to integrate Metaverse applications, making an in-vehicle immersive experience possible. Smart cars today possess core capabilities such as cloud computing and blockchain systems which can easily become intelligent terminals of the Metaverse.

On the customer experience side, the Metaverse is transforming vehicles from transportation devices to mobile terminals that combine work, entertainment and other functions. Furthermore, automakers can use the Metaverse to attract and acquire new customers, thereby activating a new model of marketing and customer management. The induction of the metaverse into the automobile has begun a new chapter in the history of the auto industry: a vehicle, created to be a mode of rapid transportation from point A to point B, quickly became an asset that symbolized identity and value, and is now evolving into a tradeable digital asset that plays the role of a steward of intelligent life. Consequently, the upgrade of user experience evolves from the original “flat” experience of driving to a three-dimensional digital ecology of virtual socialization.

The enormous potential of the Metaverse will directly affect three major aspects of the automotive industry --sales, usage, and servicing a car to improve its intelligence and attractiveness:

- Sales – a new channel for digital marketing:

The extension of automotive marketing to the Metaverse will bring auto makers and consumers into greater proximity than ever before. For example, automakers and Tech companies in China have cooperated to create online new car launch events with virtual test-driving facilities, removing the barriers for actual car driving demonstrations that traditional telephone and online customer service channels faced. The new digital channels will also cater to young consumers' post-pandemic car-buying behavior, making it possible to reach new customer resources and thus enable more substantial sales. - Usage – a wealth of application scenarios:

The integration of the Metaverse into real-time car scenarios will turn the car into a mobile intelligent space. For example, some automakers are currently trying in-car VR games and multimedia meeting spaces, while also adding VR functions in the driver’s seat to replace the screen. These functions are expected to enhance the entertainment value of the car in the era of the Metaverse and the self-driving car, bringing new possibilities for the use of Metaverse technology. - Servicing – a new experience of digital service:

Traditional after-sales services require the physical presence of the car and driver at the maintenance center. This can be both time-consuming and laborious for car owners. The combination of after-sales service and the Metaverse, such as online virtual after-sales personnel, will significantly improve the efficiency of after-sales services, while keeping consumers abreast of the progress of the servicing in a timely manner, instilling trust and greatly enhancing the service experience.

For automakers to fully profit from the new business opportunities in the Metaverse and to prepare themselves for competition in the Metaverse, they need to enhance their core competitiveness in terms of digital capabilities across the organization, particularly in the following four areas

- Digital hardware capability: particularly with regard to the digitization of vehicle hardware. In the future, cars will become the biggest mobile Internet terminals, behind which the requirements for computing power, chips and hardware are precisely in line with the Metaverse. Hardware devices such as intelligent cockpits and screens need to be carefully designed as they will directly affect consumers' experience.

- Ecosystem partnering capabilities: including the creation of an ecosystem, through the introduction of ecosystem partners and the expansion of application scenarios. In future, as a mobile computing device, the car must also be compatible with other such devices within the consumer’s ecosystem. For example, an intelligent operating system developed by a communications company expressly for cars has been integrated from multi-partner devices with wide application scenarios.

- Digital content development capability: In addition to the hardware, content will also be critical to the success of the car Metaverse. User interaction content and in-car entertainment content will need to be developed to attract and hold users' attention. Creating personalized and diversified content in the digital world will become the differentiator in attracting users' attention.

- Digital operation capability: massive amounts of data will be generated in the Metaverse, and enterprises need to consider how to efficiently manage and utilize big data. In addition, with the continuous automotive application scenarios and diversification of user needs, enterprises also need to improve digital user operation capability.

Energy

Unleashing the profit potential of energy storage

In June, China’s National Energy Administration (NEA) and National Development and Reform Commission (NDRC) jointly issued the Notice on Promoting the Participation of New Energy Storage Technologies in the Electricity Market and Dispatch Operations (hereinafter refers as to “the Notice”). The new energy storage technologies refer to non-hydro energy storage resources, such as electrochemical energy storage, compressed air, and hydrogen.

The Notice affirmed that battery energy storage facilities can participate independently in China’s electricity spot market. Once this market gets established properly it will pave the way for other opportunities, along with varying energy storage uses, and these will create multiple revenue streams, and make the commercialization of energy storage easier. Here are our observations on The Notice and how it will affect those that are investing in energy storage facilities:

- The Notice is designed to remove market barriers for energy storage

Developing battery storage has long been on the agenda of energy policy makers. China has set goals to boost its non-hydro energy storage capacity to around 30GW by 2025 and 100 GW by 2030, a drastic increase from 5.7GW in 2021. However, constraints such as the high cost, unclear market role, and uncertain investment return, have long relegated energy storage resources to the role of supporting facilities. The Notice clarified the role of the market in energy storage, and set a clear direction for developing reasonable pricing mechanisms, trade mechanisms, and dispatch operation mechanisms. More specifically, it allows energy storage facilities to participate independently in both wholesale and spot markets, by selling utility services, including energy, various ancillary services, and capacity. The Notice is a commitment to remove market barriers and open the door for profitable energy storage investment. - Implementation details need to take into account the storage-specific characteristics of the sector

The Notice confirmed energy storage companies buying energy from the grid for charging need to pay only for the energy itself. They do not need to pay the transmission and distribution price, government levies, and surcharges on the corresponding amount of electricity used for charging. This will bring down the charging cost of storage facilities by about 30%-40%.

However, implementation details are not in the place yet. We expect future guidelines will take into account physical and operational characteristics of storage resources. For example, characteristics related to state of charge, charge time, charge/discharge limits, run time, and charge/discharge ramp rate will be carefully considered so that power grids can plan and optimize their dispatch around a more realistic picture of the operating capabilities of storage resources. This will help improve efficiency of both markets and physical operation of the grid. - A range of revenue streams are emerging to realize profits

With a clearer price mechanism, a range of revenue models are likely to become economically viable. As the amount of renewable energy generation and consumption increase, the power system requires greater system flexibility and grid stability. The inclusion of energy storage in the energy markets can reduce stress on the system by shifting the load away from peak conditions and reducing over-generation during low load conditions. It can also provide ancillary services to correct system frequency and help avoid contingency events. In country after country it has been seen that the spot market can provide marginal revenue to energy storage facilities and will be the major factor that enables these facilities to thrive.

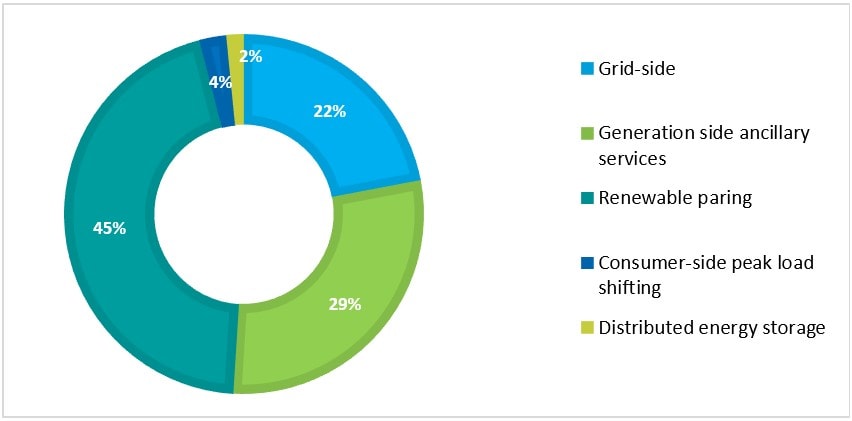

Chart 3: Various use of battery energy storage, 2021

Source: 2022 Energy Storage Application Research Report

Source: 2022 Energy Storage Application Research Report

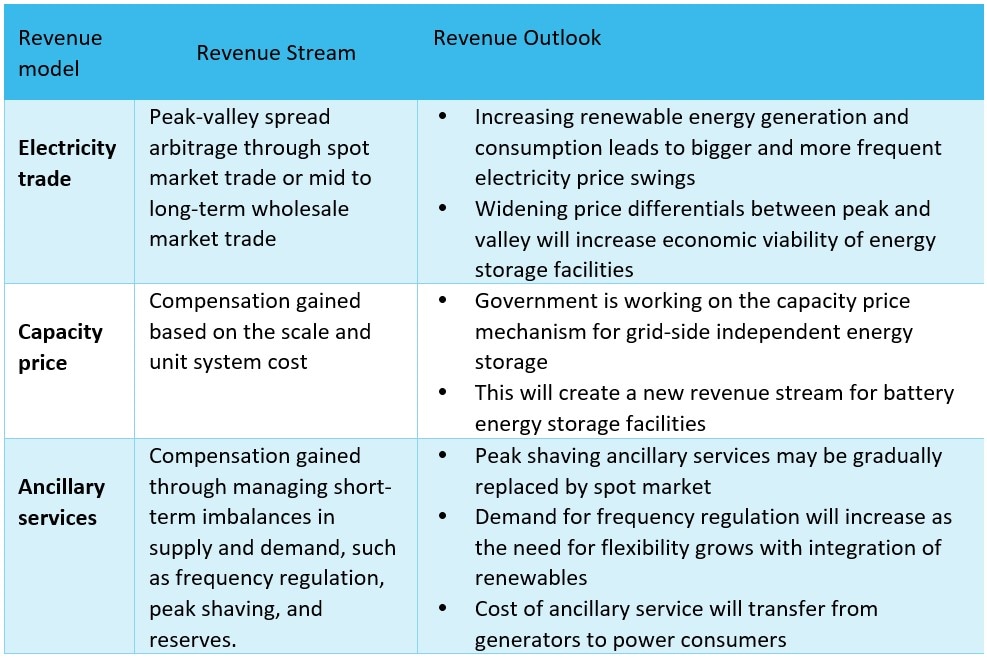

Chart 4: Revenue streams of energy storage business

Source: Deloitte Research

Source: Deloitte Research

Consumer

Outdoor ‘mini-vacations’ give a new direction to the tourism and leisure industry

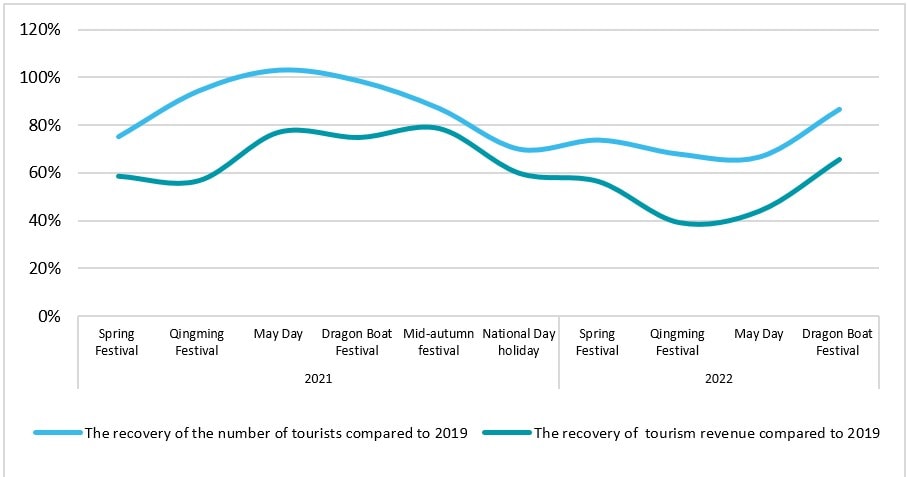

The tourism and leisure industry was severely disrupted by the Covid-19 pandemic that hit parts of China in the first half of 2022 but it has bounced back after hitting rock bottom in May. In the first half of this year, repeated outbreaks of COVID 19 in some parts of China made a dent in the recovery of the tourism market which has been slowly gaining strength since 2021. The number of tourists during the Qingming Festival and the May Day holidays dropped significantly this year. However, with the release of a series of policy initiatives such as the "COVID-19 Prevention and Control Plan (Ninth Edition)" at the end of June and the cancellation of the asterisk mark on travel codes, domestic tourism has begun to show signs of recovery. Since the 3-day Dragon Boat Festival in early June, the adjustment of the "circuit breaker" mechanism for inter-province tourism activities and summer holiday travel needs have driven up tourism demand, and the level of recovery even exceeded that of National Day holidays in 2021. Except for Beijing, Shanghai and areas severely hit by the pandemic, popular destinations such as Yunnan, Hainan and Sichuan saw tourism boom. Going forward, as the pandemic comes under control, with more targeted prevention and control measures, and the availability of COVID-19 medications, the tourism market may experience a retaliatory revival.

Chart 5: Degree of recovery in holiday tourist arrivals and income compared to 2019 (%)

Source: Ministry of Culture and Tourism, Deloitte Research

An influx of Gen Z consumers and increased numbers of tourists choosing domestic destinations rather than international ones has given a new direction to China's tourism market. Although the repeated outbreaks of COVID 19 negatively affected people’s confidence and willingness to travel, demand for high-quality tourism will remain unaffected in the long run. Furthermore, restrictions on outbound travel have forced people to search for other forms of travel and leisure and the two combined may actually serve to bring about a higher quality of service all around. The promulgation of the National Fitness Plans and Winter Sports Development Plan have helped build a loyal customer base for outdoor sports. Catalyzed by the epidemic, local outdoor tours that are close in distance but with high frequency and multimodality have replaced traditional long-distance travel, becoming the main way of leisure and relaxation for urban residents. The coming of age of Generation Z and people who would have chosen to travel internationally now vacationing at domestic destinations has given birth to new consumption models in the tourism industry. The new favorites are:

- Glamping: In the post-pandemic era, camping has become increasingly popular for its short travel time, proximity to nature, and flexibility. In contrast to traditional camping, which is simple and lightweight, glamping (which is a combination of the words 'glamorous' and 'camping') emphasizes ceremony over simplicity and requires a lot of luxury camping gear and beautifully designed accessories, a ‘must’ for trendy young travelers. According to the 2021 Generation Z Camping Activities White Paper, the current age group born after 1995 made up the highest proportion (32.8%) of all ‘glampers’. Another reason for the popularity of glamping is that it can be combined with a variety of other social occasions such as family gatherings, educational trips, and team building. As an industry, glamping creates many new opportunities for domestic tourism, from the camping industry ecosystem such as camp furniture and appliances, to clothing and food.

- Winter sports:With the help of science and technology, China's vision of "bringing 300 million people to participate in winter sports" has gradually become a reality. Winter sports have expanded beyond their normal physical and seasonal limits. For those who love winter sports there are many opportunities in China today, from the more traditional winter ski resorts in Heilongjiang and Xinjiang to indoor ski stations in Guangzhou and Chengdu that operate all year long and can even be used in summer. Ski simulators have further enhanced user stickiness and conversion rates as they are safer and have no venue restrictions. Meanwhile, as outbound tourists turn to domestic travel, ski enthusiasts who previously went abroad on ski trips are looking to ski domestically, thereby helping to expedite the improvement of service quality and domestic infrastructure.

- Water sports: Water sports have been moving inland from the sea and, from being a luxury experience, they are swiftly becoming more affordable. The growing popularity of water sports has made possible the development of more niche sports, for example, stand-up paddling, which has become this summer's new favorite on social media because it is easy to learn and has a high entertainment value. The popularity of wave pools has given rise to inland surfing and indoor surf simulators. Future development of water sports will attract and expand the consumer base with the help of brand aggregation in the upstream industry chain. A variety of marketing forms, and complimentary service offerings such as training, competitions and tourism packages are also expected to develop the industry.

With pandemic restrictions on overseas travel, changes in consumer preferences, and higher service requirements for domestic travel, outdoor leisure activities have given a new direction to the post-pandemic tourism market. This will affect the industry in a variety of new ways. Here are some of them:

- Greater generation of data: higher frequency of mini vacations will generate more data, creating more data operation value for organizing urban leisure activities and meeting household needs. In addition, increased frequency of consumption provides more operating space for reward and club membership programs.

- Tighter correlation between upstream and downstream: outdoor mini-vacationing is equipment heavy as most glampers like to equip themselves with premium, multi-category equipment and ancillary products, so the aggregation and development of the upstream equipment industry will provide crucial support to the glamping industry. Currently there are many participants in the domestic outdoor apparel and equipment market, and brands at home and abroad have been actively competing for customers.

- Immersive experience marketing: High-quality outdoor activities can be quickly turned into online marketing content, triggering further offline consumption. Using multiple marketing methods such as e-commerce live-streams, short-form videos, feature films and theme carnivals, merchants can create an immersive experience that targets fashion and trend-conscious young people and accelerates consumer outreach.

- More conducive to community-based marketing: Because outdoor mini-vacations are often done in groups, they offer outdoor sports brands opportunities to engage in community-based marketing. Brands can organize outdoor-themed local mini-vacation trips that create a new social space for Generation Z. The trips or events may also be equipped with photography services, catering to Generation Z's need for live sharing on social media.