Perspectives

Deloitte China Monthly Report Issue 96

Published date: 28 February 2025

Economy

Benign tariff hikes are no reason to cut back fiscal stimulus

Will China’s 2025 growth target be set at a similar level to 2024? The implicit goal seems to be "around 5%" GDP growth. But does such a lofty goal account for potential external shocks, particularly uncertainties surrounding tariffs and other policy measures aimed at curbing China's technological advances? If headline growth remains a key concern, where should policy efforts be directed? In our view, the answer largely depends on the magnitude of fiscal stimulus, which in turn is shaped by external conditions and the pace of consolidation in the property sector. At the annual Two Sessions in early March, we expect greater clarity on the required fiscal deficit to sustain a growth rate of "around 5%" and how those funds will be allocated.

The chief rationale for setting the growth target at "around 5%" is about instilling confidence and finding the right balance between providing support to traditional growth drivers (e.g., property related activities) and tilting to new productive forces (e.g., EV and advanced manufacturing). Nevertheless, the general direction is to prioritize quality over quantity.

As in 2024, China's economic challenges are multifaceted, including the vacuum left by once-mighty property sector, the broader impact of a slowing property market on the economy (clearly visible in the food-beverage sector) and the issue of tariffs. These challenges are both cyclical and structural.

The real estate sector’s problems are cyclical, yet many large property companies have built up complex financing structures during their go-go years. The property sector may not be a leading growth engine going forward, but it influences many sectors and might be considered akin to quasi-financial institutions. Therefore, if real interest rates need to be reduced, monetary easing must be significant.

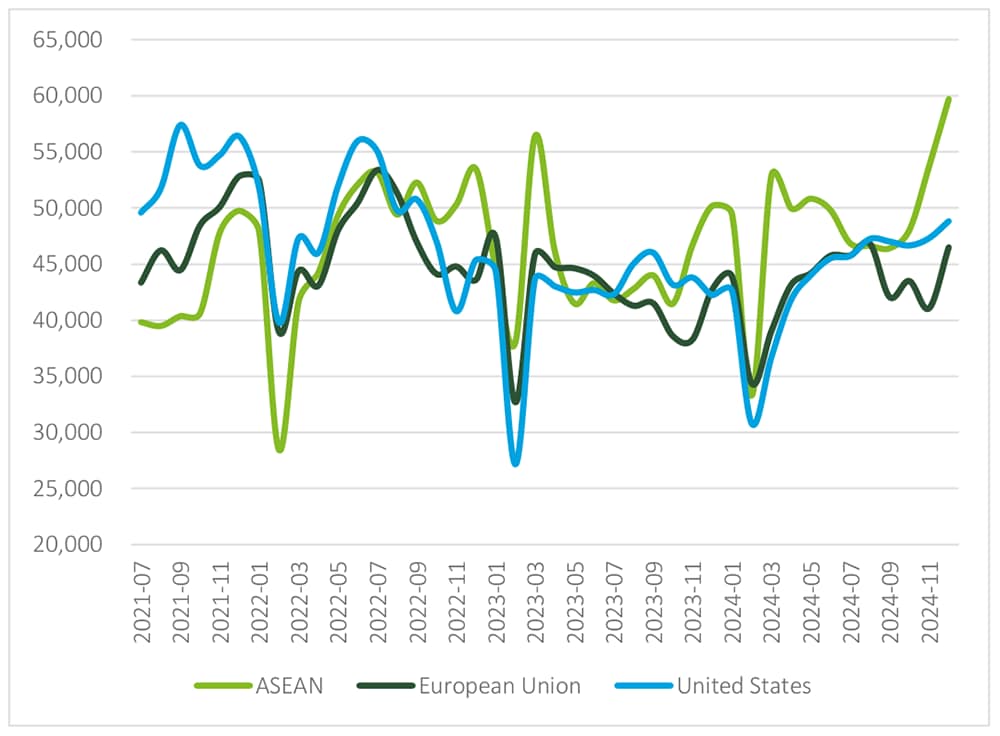

Regarding tariffs, we have consistently highlighted the disparity between rhetoric and genuine policy intensions from the US Administration, particularly since the presidential campaign of 2024. The imposition of highly punitive tariffs on Chinese EVs (i.e., 100% additional tariff) was a clear case of grandstanding, given the negligible volume of China's EV exports to the US (less than 1% of total Chinese EV exports). Similarly, President Trump's threat of 60% tariffs was largely rhetorical. With average tariffs on China’s exports to the US sitting at 20% and considering China’s efforts to diversify its export markets and use 3rd countries to reroute their exports, it would have been impractical for such threat of 60% tariff to materialize fully.

Chart: China’s exports have powered ahead despite tariffs (USD millions)

Source: Wind

For China, like countries with significant trade surpluses with the US, its economy must adapt to rising tariffs; unlike others, China has to live with export controls due to Washington's doctrine of "small yard and high fence". Additionally, due to geopolitical constraints, it does not have the luxury of over-adjusting its exchange rate as Japan has done in recent years. In many ways, the various headwinds have compelled Chinese companies to accelerate their overseas expansion, and the economy has become better equipped for a trade war under the second Trump administration. Precisely owing to its enhanced resilience, the announcement of a 10% tariff on China's exports, effective from February 1, 2025, was largely met with indifference in China.

In response, China swiftly retaliated with tariffs ranging from 10% to 15% on US exports of LNG, large-engine vehicles, and pick-up trucks. Nonetheless, these products represent only roughly 10% of China's total imports from the US. Clearly, China has adopted a strategy of avoiding trade tensions with the US, though it is less inclined to appease the US in the manner that Mexico and Canada have conciliated. The thinking is such: if tariffs are indeed viewed as a substitute for tax revenue by the US, China will not be the sole target. Yet, the treasury market has been selling off on concerns over unrealistic assumptions of budget balancing, prompting the Fed to suspend its easing campaign. So, if higher borrowing cost can indeed act as a constraint on imposing additional tariffs, there may be hope for another trade agreement. While it is challenging to envisage how such a deal would shape up, it could potentially involve a combination of purchasing commitment like the US-China phase one trade deal, along with expanded market access to US companies, such as agriculture and healthcare. However, for China, nothing can be taken for granted at this stage. The possibility of the US Congress revoking China's PNTR cannot be overlooked. Ultimately, fiscal leverage ought to take on a more prominent role in 2025, especially if such a trade deal might entail an implicit clause related to the RMB exchange rate.

What can we anticipate from the Two Sessions? First, the GDP growth target for 2025 is likely to be set at "around 5%". However, should the PNTR be revoked, or additional tariffs are to be imposed in the second half of 2025, fiscal policy may need to become more expansionary than initially planned. The most significant outcome from the slew of policy announcements since last September, in our view, is the implicit removal of the deficit ceiling, previously set at 3%. This gives the central government a lot of leeway in taking on local government debt. Naturally, the extent to which such financial support is implemented will depend on the financial health of local governments, which is closely tied to the state of the respective property market. Hence, stabilizing the property market remains a top priority.

In what ways could the unexpected success of DeepSeek influence policies? To state the obvious, the realization that AI can perform tasks at much lower cost has injected a massive boost to investment sentiment after the Chinese New Year holidays. Furthermore, DeepSeek’s achievements have also structurally boosted investor sentiment regarding Chinese companies, whose valuations have been dampened by geopolitical risks.

Chart: Equity market's ferocious rally propelled by DeepSeek

Source: Wind

Significantly improved investor sentiment may nudge policymakers to place greater focus on revitalizing consumption. Meaningful adjustment in boosting domestic consumption by China will be a boon to regional growth and to mitigate trade tensions. Consumption boosting measures ought to be tied to the real estate sector for a very simple reason – most consumers see properties as both consumption and investment, more for the latter. Notwithstanding seasonal effect of the Chinese New Year on data, January CPI (0.5% yoy) has again reinforced the need for policymakers to tackle deflation, which creates more pains for debtors. This is why the government's decision to lend more loans ($6.84bn) to Wanke to repay debt is a welcome development. Not only is Wanke the largest residential property developer, but it is also arguably the best-run private real estate company. And therefore, bailing out Wanke has signalled a profound policy shift. In short, benign tariffs are indeed a respite, but by no means can China count on exports as a potent driver in 2025 as it did in 2024.

Financial Services

Why the PBOC has suspended government bond purchases?

In January 2025, the PBOC announced a moratorium on purchasing government bonds (GBs), marking the first such suspension since August 2024, when it had actively bought and sold GBs in the secondary market for five consecutive months. That same month, the 10-year GB yield fell to a record low below 1.6%, while the RMB briefly weakened past the 7.30 mark against the U.S. dollar. As Chinese GB yields declined further, the interest rate spread between China and the US widened, intensifying depreciation pressure on the RMB.

Will this constrain the scope and effectiveness of China’s monetary policy? The countercyclical adjustment of monetary policy must strike a balance across multiple objectives—GB yields, the exchange rate, and interest rates—while also mitigating potential systemic financial risks.

PBOC buys GBs to stimulate the economy through monetary easing

Since August 2024, the PBOC has steadily increased its buying and selling of GBs in open market operations, positioning them as tools for base money delivery and liquidity management. These operations have been conducted in both directions. From August to December 2024, the PBOC made net GB purchases totaling RMB 1 trillion, coordinated with measures such as the reserve requirement ratio (RRR) cut and reverse repos to create a broadly accommodative monetary environment.

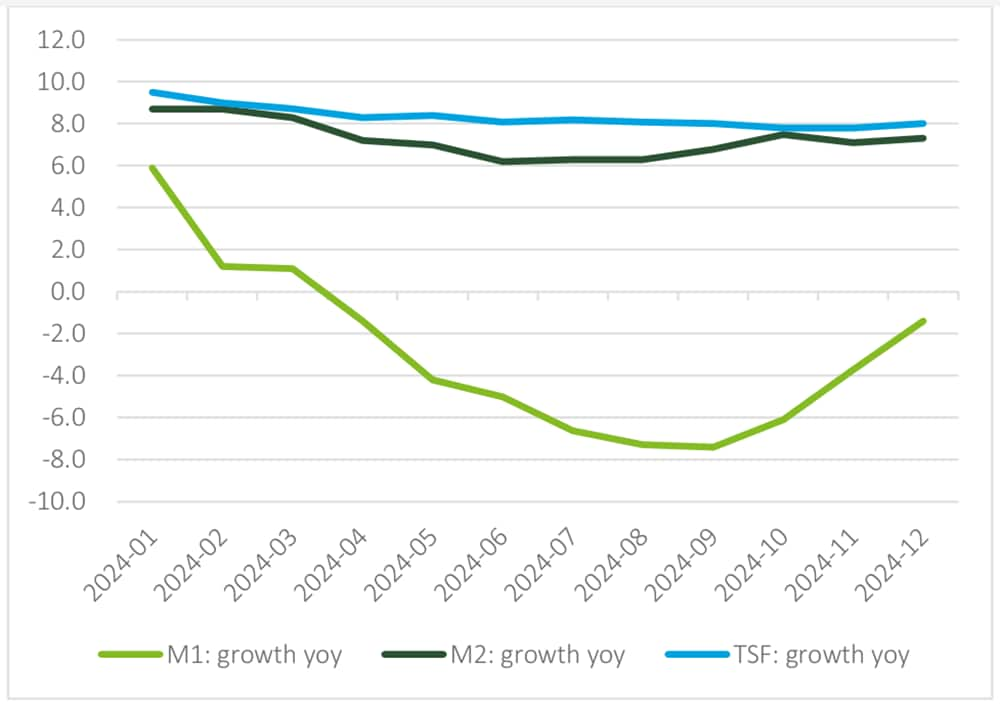

In Q4 2024, the large-scale implementation of a package of incremental policies led to stronger-than-expected financial data in December: the stock of total social financing (TSF) grew 8.0% year-on-year, the decline in M1 growth moderated from -3.7% to -1.4%, and M2 growth slightly increased from 7.1% to 7.3% year-on-year. This policy mix contributed to a notable recovery in economic activity, with GDP expected to grow by 5.0% in 2024, following a U-shaped trajectory throughout the year. The broad monetary policy played a key role in supporting economic stability and market confidence, with current money supply and liquidity remaining reasonably sufficient.

In the near term, the urgency for the PBOC to conduct further quantitative easing through GB purchases in the secondary market is significantly lower than it was in August 2024

Chart: The stock of social financing, M1, and M1 growth rates all improved (%)

Data source: PBOC, Wind

Stabilizing GB yields and controlling the downside risk of long-term yields

The level of GB yields is crucial to the stable development of the broader financial market. Long-term GB yields reflect market expectations for future economic growth and are also influenced by shifts in supply and demand, making them a key market focus. The PBOC’s involvement in GB trading directly impacts this supply-demand dynamic, allowing it to regulate bond yields and, importantly, mitigate the systemic risk of a prolonged downward trend in long-term GB yields.

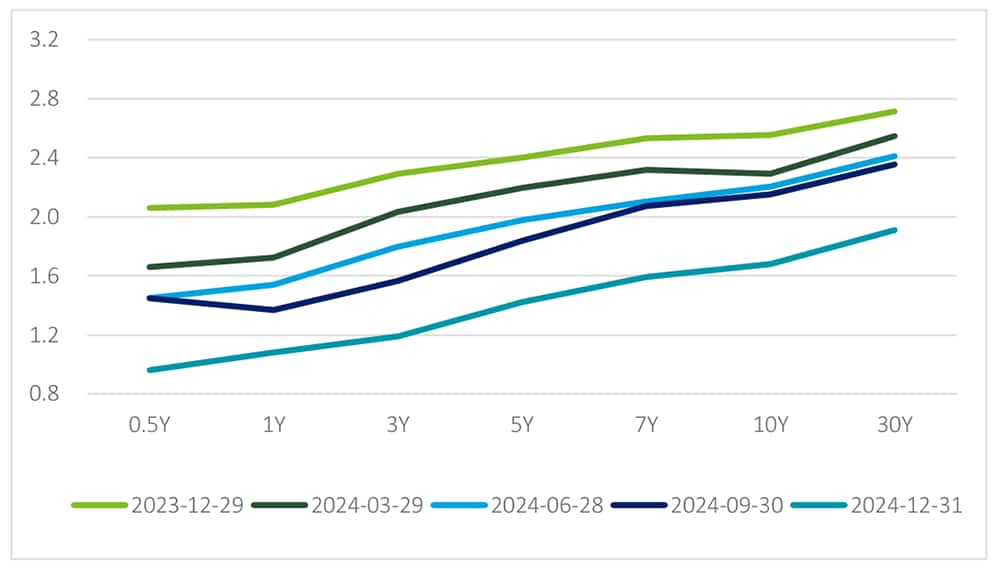

In 2025, with a "moderately loose" monetary policy and a stronger countercyclical adjustment, most market participants anticipate swift interest rate cuts and reserve requirement reductions, influencing asset allocation. The expectation of lower interest rates has already been reflected in bond yields. Since September 2024, GB yields have declined rapidly, leading to a significant downward shift in the yield curve and a narrowing of the term spread. In December 2024, the 10-year GB yield fell below 2.0%, and by the end of the month, the spread between 1-year and 10-year GBs had narrowed to 59 basis points, a 19bp contraction from the end of September.

Chart: Chinese GB yield curve moved significantly lower in 2024 (%)

Data source: ChinaBond, PBOC

The coupon rate of long-term GBs is fixed, meaning investors receive both the principal and agreed interest payments at maturity without credit risk. However, in the secondary market, interest rate fluctuations impact bond prices, creating opportunities for investors to profit from price differences. When price volatility is high, market risks increase, potentially leading to investor losses. A notable example is the Silicon Valley Bank crisis in 2023, where a low-interest rate environment compressed spreads, prompting some institutions to adopt excessive risk-taking strategies that ultimately weakened financial stability.

In response to persistent excess demand for GBs, the PBOC announced a suspension of bond purchases, aiming to rebalance supply and demand and prevent overheating in the bond market. By allowing bond prices to decline, GB yields—which move inversely to prices—are likely to rise, helping to stabilize market expectations and mitigate interest rate risk.

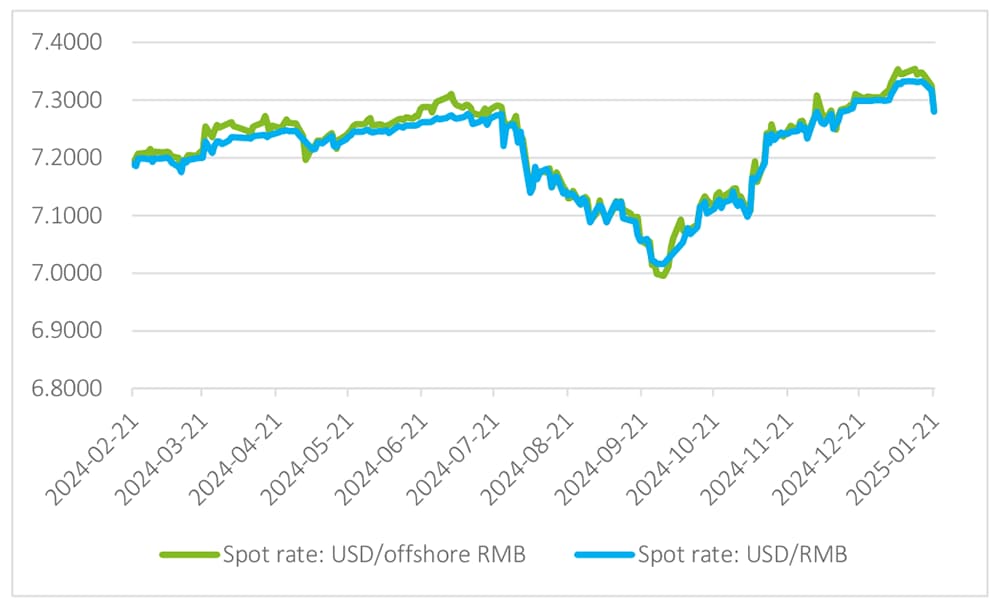

Stabilizing exchange rates and market expectations

In 2025, the Fed’s decision to delay rate cuts has strengthened the US dollar index and widened the interest rate gap between China and the US In January, both onshore and offshore RMB exchange rates briefly weakened past 7.30 against the US dollar, increasing depreciation pressure and placing constraints on the PBOC’s monetary policy. If monetary policy remains overly loose, it could further weaken the yuan and trigger capital outflows.

In response, the China Foreign Exchange Market Steering Committee swiftly introduced measures to stabilize expectations. The PBOC issued RMB 60 billion in offshore RMB central bank bills, raised macro-prudential adjustment parameters for cross-border financing, and sent a clear signal of exchange rate stability through a coordinated set of actions. Following the suspension of government bond purchases, short-term bond yields rose, limiting the downside for long-term yields. Stabilizing GB yields helps enhance the attractiveness of RMB assets, encouraging foreign capital inflows and ultimately supporting the stability of the RMB exchange rate.

Chart: rising exchange rate of the RMB against US dollar

Data source: ChinaMoney, Wind

Balancing multiple goals

The 7-day reverse repurchase rate (the policy interest rate) has remained unchanged since the end of September 2024, and the LPR quotation has stayed the same for four consecutive months. The market interest rate must balance the various objectives of stable growth, a stable exchange rate, and stable interest rate spreads. The current broad monetary environment aligns with market expectations, with the next step likely being a reduction in short-term interest rates, which would involve broad credit to lower financing costs and boost market demand. Rate cuts are still anticipated in the first half of the year. The decrease in short-term interest rates could ease the interest rate spread issue for financial institutions, stimulate the speed of money circulation, and boost economic activity.

Retail

Policy expansion and emotion-driven lifestyle to unlock consumption potential

In 2024, China grappled with weak demand and some deflationary pressures, with total retail sales of consumer goods increasing by just 3.5% year-on-year, a sharp decline from the 7.2% growth rate in 2023. The recovery of consumer demand in 2025 will continue to face challenges. The Spring Festival, a traditional peak season for consumption, serves as a critical point for observing shifts in consumer sentiment. During the Chinese New Year holiday, overall consumption experienced moderate growth. According to data from the Ministry of Commerce, sales at major retail and catering enterprises during the Spring Festival period rose by 4.1% year-on-year. High-growth categories and sectors mainly reflected new growth areas and highlights.

“Trade-in” policy expansion drives rapid growth in related products

At the end of 2024, the Central Economic Work Conference identified "boosting consumption" as the top priority for 2025. On January 5, the National Development and Reform Commission (NDRC) and the Ministry of Finance (MOF) issued the Notice on Further Expanding and Implementing the "Trade-in" Policy for Large-Scale Equipment Upgrades and Consumer Goods in 2025. The notice outlined the following:

- Continue to support "trade-in" promotions for home decoration and consumer goods, increasing subsidies for the renovation of old houses, kitchen and bathroom upgrades, and elderly-friendly home modifications, thereby encouraging smart home appliance consumption.

- Implement purchase subsidies for three categories of digital products: smartphones, tablets, and smartwatches/fitness bands.

Rapid growth of emotion-driven consumption

Unlike the moderate growth seen in the overall physical retail market, service-related consumption continues to thrive due to its ability to offer diverse consumption experiences and emotional connections. The share of service-oriented consumption among residents has steadily increased. During this year’s Spring Festival holiday, residents were particularly active in travel, and their willingness to engage in experiential service consumption remained strong.

- Record-breaking tourist numbers: According to statistics from the Ministry of Transport, cross-regional movement during the first 20 days of the Spring Festival transport season increased by 8% compared to 2024 and 20% compared to 2019. Domestic tourism spending during the 8-day Chinese New Year holiday reached 677 billion yuan, a 7.0% year-on-year increase, and a comparable growth rate of 15.2% compared to 2019.

- Box office performance: During the Chinese New Year holiday period, both daily average box office revenue and cinema attendance hit record highs, rising by 18.6% and 14.7% year-on-year, respectively. Notably, Ne Zha 2 grossed over 1 billion yuan at the box office, becoming the highest-grossing animated film globally. The popularity of the Ne Zha IP also sparked a wave of consumption for related trendy peripheral products. According to data from Taobao, by mid-February, sales of Ne Zha series licensed peripherals on the platform had exceeded 50 million yuan.

- Cultural and tourism consumption: In addition, cultural and tourism-related consumption continued to grow rapidly during Chinese New Year holiday. According to data from the State Taxation Administration, sales income from leisure sightseeing activities, cultural and artistic services, and park and scenic area services all increased by more than 50% year-on-year.

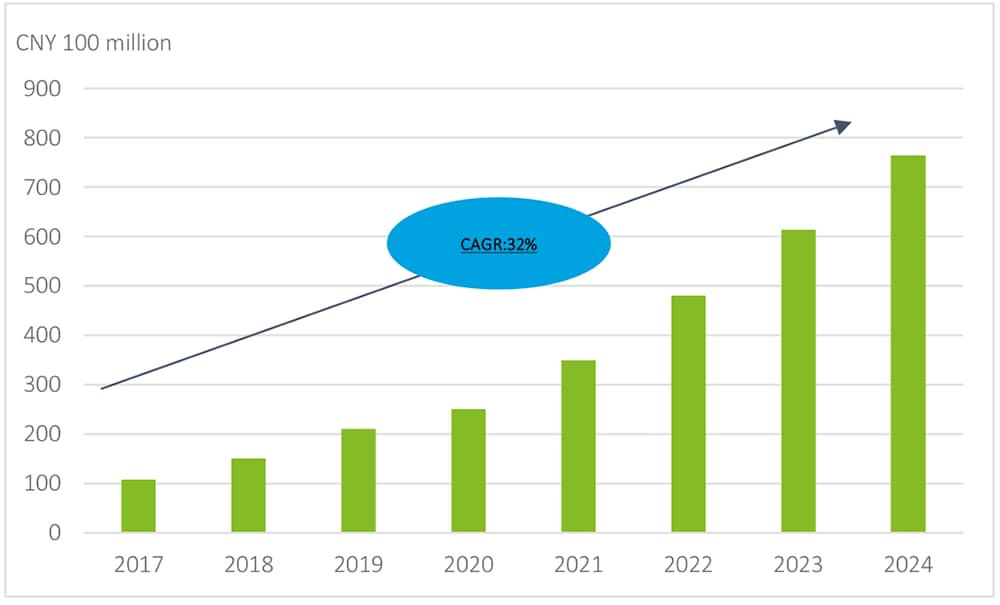

Chart: Size and growth rate of China’s toy market (2017-2024)

Source: Institute of Fiscal and Monetary Policy, Chinese Academy of Social Sciences; Frost & Sullivan

Based on the Chinese New Year consumption trends outlined above, businesses should focus on the following key areas in 2025:

Seizing the benefits of the “trade-in” policy to drive product upgrades and market expansion

Companies should adjust their product offerings and marketing strategies in line with policy guidance, gain a thorough understanding of the "trade-in" policy's implementation details, engage with government subsidy programs, reduce operating costs, and enhance market competitiveness. For example, in the home appliance sector, businesses can focus on creating high-performance, energy-efficient, and eco-friendly products targeted at scenarios such as old house renovations, kitchen and bathroom upgrades, and smart home solutions. These products can be paired with policy subsidies to attract consumers.

Deepening emotion-driven consumption scenarios to enhance service experiences and emotional connections

Companies dealing in physical goods can tap into experiential economics by expanding their IP industry chain, launching co-branded products, and introducing limited-edition trendy peripherals. By leveraging social media, they can generate buzz and create topical conversations. In the cultural tourism industry, businesses can develop themed travel routes based on popular IPs and offer personalized, immersive experiences that cater to consumers’ emotional needs. In retail, dining, scenic spots, and other service sectors, businesses should focus on the needs of the "pan-secondary dimension" group, driving the integration of national tide IPs and secondary dimension concepts into service experiences to enhance consumers’ enjoyment and sense of participation.

In 2025, companies must fully capitalize on the “trade-in” policy benefits while tapping into the potential of emotionally driven consumption. On one hand, they need to balance short-term growth with long-term strategy, avoiding price wars. On the other hand, they should prioritize technological innovation and brand-building to create differentiated competitive advantages. By closely aligning with consumer demands, policy guidance, and market trends, businesses can achieve sustainable growth.

Life Science & Healthcare

The advancement and challenges of low-cost generic drugs

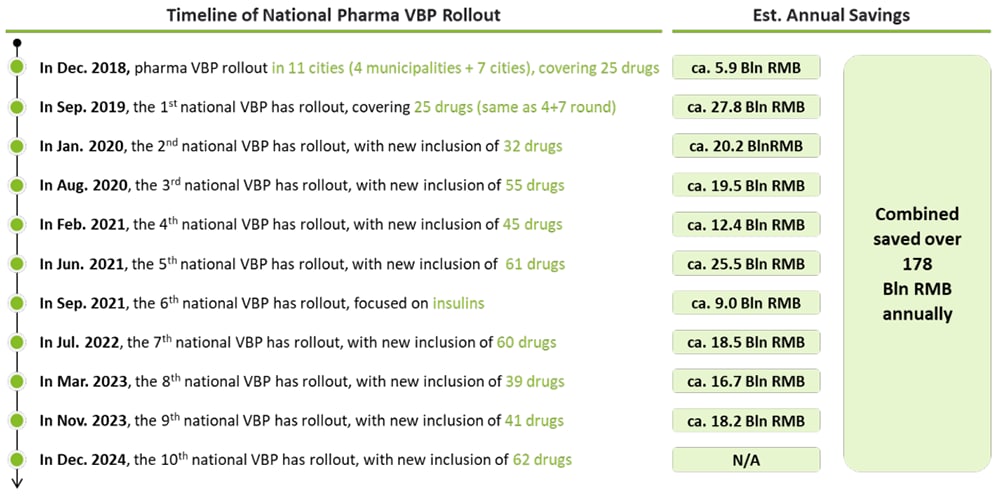

From 2018 to the end of 2024, China conducted ten rounds of national volume-based procurement (VBP) for western medicines, encompassing 426 off-patent drugs, many of which are commonly used. The substantial price reductions achieved through centralized procurement have eased the financial burden on both the public and the basic medical insurance fund. Estimates suggest that since the introduction of the national VBP, the program has generated annual savings of over 174 billion RMB, significantly contributing to the long-term sustainability of the BMI system.

Chart: Timeline of national pharma VBP

Source: NMPA, NHC, desktop research, Deloitte Research

The widespread replacement of originator drugs with generics has also raised new concerns. In January 2025, a group of medical experts jointly submitted a proposal titled "Ensuring Access to High-Quality Medications Under the VBP Framework" (hereinafter referred to as the "Proposal"). The efficacy and quality of drugs procured through centralized procurement are expected to become a key point of discussion during the 2025 Two Sessions in Beijing and Shanghai, bringing drug pricing and quality issues back into the public spotlight amid ongoing healthcare reforms.

Following the 2015 reform of China’s drug evaluation and approval system, the generic quality consistency evaluation (GQCE) was formally incorporated as a critical criterion in the drug registration review process. It requires generics to demonstrate bioequivalence to originator drugs. This reform has led to improvements in the quality of generics in China. However, because generic drug development primarily relies on pharmaceutical studies and bioequivalence trials, rather than comprehensive clinical trials, there remains a gap in clinical evidence compared to originator drugs, which have accumulated extensive clinical data over time. Therefore, the full clinical replacement of originator drugs by generics cannot be achieved immediately and requires further verification over time.

As of the end of 2024, a total of 11,443 drug specifications have passed the GQCE, reflecting the vast scale of the generic drug market. In advanced healthcare countries, the prescription share of generic drugs continues to rise, improving accessibility to medications. For instance, according to IQVIA, generic drugs account for over 90% of prescriptions in the U.S., yet they contribute to only 15% of total drug expenditure, highlighting the essential role of low-cost generics in pharmaceutical supply. In China, data from the National Healthcare Security Administration shows that following the implementation of VBP, the utilization rate of generic drugs increased from 70% to 88%. However, compared to the U.S., there is still room for further expansion and adoption of generics in China.

While China’s GQCE system aligns with international practices, there is still room for improvement in evaluation standards. Two key pharmacokinetic parameters used internationally to assess the equivalence of generics to originator drugs are maximum blood concentration (Cmax) percentage and area under the plasma concentration-time curve (AUC) percentage. According to the 2022 report "Comparative Analysis of Labeling Information for Chronic Disease Medications: Originator vs. Consistency-Evaluated Generics" (慢病用药中原研药与一致性药物评价药品说明书统计分析), the EU sets the threshold for these parameters at 90%-111%, while China’s pharmacokinetic parameters allow for a broader range, indicating relatively looser standards.

Recently, former NMPA Commissioner Bi Jingquan emphasized that GQCE evaluation should not become a one-time assessment and proposed several recommendations. He suggested strengthening regulatory oversight of manufacturing enterprises to ensure validation and stability for each production batch while enhancing quality assurance systems and enforcing GMP compliance. He also emphasized the need to ensure reasonable profit margins for companies winning bids in VBP, taking R&D and production cost recovery into account. Additionally, he proposed penalizing firms that submit unreasonably low bids to maintain market order. Furthermore, he advocated for enhancing public awareness of generic drugs by increasing transparency in pharmaceutical data and bioavailability information, thereby improving trust and acceptance among physicians, pharmacists, and patients.

China has only been conducting generic drug consistency evaluations for a decade, yet it has rapidly expanded the substitution of originator drugs with low-cost generics. This progress is thanks to advancements in domestic pharmaceutical R&D and manufacturing capabilities.

Looking ahead, as VBP becomes more institutionalized, China must continuously refine quality control mechanisms for generic drugs and enhance GMP compliance. The evaluation standards for generics need ongoing improvement, while dynamic GMP inspections should be strengthened and conducted more frequently. Stricter quality controls should be enforced throughout both the R&D and production phases. Simultaneously, future procurement policies must avoid an excessive focus on “lowest-price wins,” as ensuring reasonable profit margins for pharmaceutical companies is crucial for sustaining stable investment in generic drug research, development, and production quality.