Perspectives

The Deloitte Research Monthly Outlook and Perspectives

Issue 80

22 February 2023

Economy

Prolonging the recovery lies with property and consumption

China’s recovery continues to gather momentum. To begin with, Covid-19 has already become yesterday's news for most people in China, indicating that the scars from quarantines and strict lockdown measures over the past three years were temporary. If this really is the case, consumer caution towards future waves will subside. So far, anecdotal evidence (e.g., traffic jams and crowded restaurants) have supported the hypothesis of a meaningful recovery in consumption, if not, outright revenge consumption. Meanwhile, extensions to visa approval cycles have indeed underlined consumers' urge to travel overseas following three years of closed borders. But the key factor in bolstering consumer sentiment remains China’s housing market given that the lion’s share of consumer wealth is tied up with the property market.

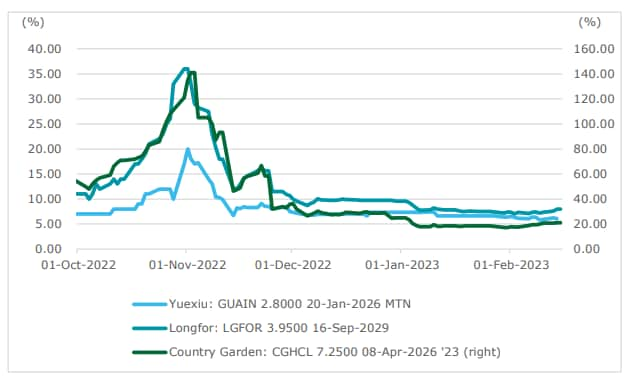

Figure: Offshore bond yield rate of developers

Source: Eikon, Deloitte Research

Supportive policy measures since last November (e.g., bank lending and government guarantees) have greatly eased the liquidity crisis facing most developers (as reflected by major developers' offshore dollar bond yields). Mortgage boycotts across the country have also been resolved, while the majority of unfinished projects are expected to be completed in due course. Banks are being guided to lower interest rates for both developers and homeowners on the back of the PBOC's accommodative monetary stance. The question is whether developers would ramp up investment in response to lower interest rates. This seems unlikely because even in the absence of downward price corrections of residential properties, the heyday for developers is highly unlikely to return. For consumers whose balance sheets remain strong, naturally there will be immense expectations on them to carry the load of growth in 2023 given challenges on the external front (risk of a recession of the US and sluggish outlook of Europe). Mortgage rates have come down to as low as 3.5% from about 5% in several cities. Some banks, such as those in Beijing, have unveiled mortgage schedules to the elderly population over 80 years old. All this underscores the fact that mortgages remain the best assets of banks who do not want to see consumers retire their borrowings early due to lower interest rates.

Precisely because consumers have overweighed real estate as an asset class, price appreciation rather than lower cost of capital is a far more potent inducement for their investment. Should supportive measures be better targeted at reflating the housing market? Just like any country, China does not have a national housing market with very different dynamics. Broadly speaking, the first tier cities of Beijing, Shanghai, Guangzhou and Shenzhen enjoy high property prices which are underpinned by favorable demographics. Second tier cities are a mixed bag but smaller cities most often suffer from population outflows which are defined as the differences between household registration and resident population. Even in many developed cities (e.g., across southern China), younger people may seek better economic opportunities in first and large second tier cities, and therefore housing prices, which have seen significant gains over the years, may not have much upside given oversupply overhang. From this perspective, if the housing market can be truly revitalized, restrictions on demand ought to be eased or removed. This should start with first tier cities where scarce resources such as healthcare and education are concentrated. Lower tier cities could benefit from spill-over wealth effects if first tier cities see price gains in the housing market. Such calibrated housing supportive measures reflect an ongoing debate around reflating the economy and pursuing either an investment-driven recovery or consumption-led growth.

In this column, we have been consistently advocating for the latter because it is all about final demand. To focus on final demand is critically important against a backdrop of a challenging environment which could be characterized as a simultaneous slowdown of major economies (the US most notably) and stubbornly high inflation. China's export growth in 2023 is unlikely to repeat the levels of growth seen in 2020-2022, and unless the Fed is unwinding its tightening on a major slowdown which we view as unlikely, many emerging economies, except for Asia), could still be mired by a debt crisis. China must therefore make greater efforts to unleash domestic demand. In the most recent issue of ‘Seeking Truth’, the Party’s key theoretical publication, President Xi Jinping gave a speech titled ‘a few key issues on the economy’. According to President Xi, the most acute economic challenge is inadequate aggregate demand, and therefore consumption plays the fundamental role while investment is the key. However, policies must be more optimal in view of lessons from the Asian Financial Crisis (1998), the Global Financial Crisis (2008) and shocks from pandemic since 2020. On consumption, President Xi has pointed out that room for greater consumption lies in a number of areas such as improved housing, the needs of senior citizens, education, recreation and sports. On investment, the focus will be manufacturing upgrading and strengthening supply chains. Also on investment, President Xi has emphasized the ‘two unshakables’ – to deepen SOE reform and to the improve business environment for private enterprises. Based on this important speech, even if economic reflation is a top priority, the quality of growth should not be compromised.

In short, as the reopening has so far turned out to be much smoother than expected, China's recovery in 2023 is likely to surprise on the upside. But our recent upward revision of 2023 GDP growth from the range of 4.5%-4.8% to 5.0% also reflects our caution on the impact of investment.

Consumer

Spring Festival signals consumption recovery

Consumption recovered steadily during the 2023 Spring Festival holiday season as adjustments in the pandemic prevention and optimization measures along with a decline of peak infections, supplemented by the implementation of numerous local consumption promotion policies, restored consumer confidence. According to VAT invoice data from China’s State Taxation Administration, during the 2023 Spring Festival holiday, sales revenue of consumption-related industries nationwide increased by 12.2% year-on-year (YOY) and 12.4% over the same period in 2019, maintaining a steady growth trend overall. Among them, consumption of goods increased by 10% year-on-year and 13.1% over the same period in 2019, while consumption of services increased by 13.5% year-on-year and 8.1% over the same period in 2019. A further analysis of VAT invoice data from the State Taxation Administration reveals the following consumption characteristics during the Spring Festival holiday:

- In terms of goods, sales of consumer non-durable and household-related goods grew rapidly. During the holiday, sales revenue of basic living commodities such as grain, oil and food increased by 31.5% year-on-year while fruits and vegetables increased by 39% year-on-year, and alcoholic and non-alcoholic beverages also increased by 18.7% year-on-year. For household-related goods, sales revenue of stationery and sports supplies increased by 20.9% year-on-year while sales revenue of furniture and hardware increased by 15.2% and 8.6%, respectively.

- In terms of service consumption, the recovery of tourism and accommodation services has accelerated. During the Spring Festival holiday, sales revenue of travel agencies and related service industries increased by 1.3 times YOY, which has recovered to 80.7% of the revenue for the 2019 Spring Festival holiday. Sales revenue of tourist hotels and economy chain hotels increased by 16.4% and 30.6% year-on-year, respectively, reaching 73.4% and 79.9% of the 2019 Spring Festival holiday level. The personalized services provided by homestay services are very popular, and sales revenue increased by 74.2% year-on-year, an average annual increase of 13.3% over the Spring Festival holiday in 2019.

It is worth noting that consumption in the lower-tier urban markets showed remarkable growth during the Spring Festival holiday. This was because e-commerce channels had gone downstream, and infrastructure had been strengthened in these areas during the pandemic. Thus, a far greater number of township users all over China used e-commerce services during the Spring Festival holiday. According to a JD.com report entitled “The 2023 Spring Festival Holiday Consumption Trend”, the proportion of turnover coming in from lower-tier markets has climbed steadily over the last three years, and the per customer transaction record of consumers in the lower-tier consumer markets also shows significant increases during the 2023 Spring Festival holiday. Moreover, Alipay's data shows that the revenue coming from third-tier cities and below increased by nearly 20% compared with the same period last year, exceeded consumption in first- and second-tier cities. Part of this success is due to new consumer brands tailoring their sales strategies to meet the needs of lower tier cities’ consumers. Luckin Coffee, for example, with its delicious and cheap characteristics, met the consumption habits of users in the lower-tier markets, triggering a consumption boom. Short video platforms are gradually penetrating lower tier markets, and the rise of WeChat's Channels provides a new choice for middle-aged and elderly users in lower-tier cities. Businesses such as Local life and Community group-buying have also established a foothold in lower-tier cities.

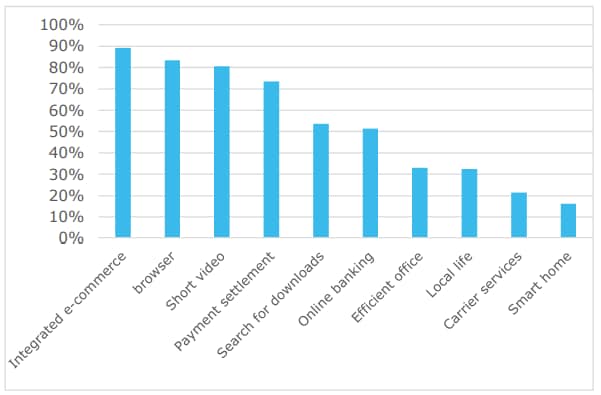

Figure:The active penetration rate of lower-tier market users in the secondary industry of mobile Internet

Note: Active penetration rate: the number of monthly active users of a target group who started an app category divided by the number of monthly active users of that target group

Source: QuestMobile, Deloitte Research

Online and offline demand continues grow, and the trend is for the consumption recovery to continue throughout 2023. According to the National Bureau of Statistics, in 2022, total retail sales of consumer goods in China were RMB 43.97 trillion, down 0.2% year-on-year. Online consumption has been an apparent driving force bolstering overall consumption. In 2022, China's online retail sales of physical goods reached RMB 11.96 trillion, accounting for 27.2% of the total retail sales of consumer goods, an increase of 2.7 percentage points over last year. Offline consumption has also improved. In 2022, amongst retailers with sales revenue above the minimum amount stipulation, retail sales of supermarkets, convenience stores and specialty stores increased by 3.0%, 3.7% and 3.5% year-on-year, respectively. With the continuous expansion of online consumption in the lower-tier market and the acceleration of the recovery of offline consumption, the momentum of consumer recovery is bound to increase. Based on what we have seen in the Spring Festival holiday, the main characteristics of consumer recovery in 2023 are as follows:

- Food and Beverage: Due to the recovery of catering and the massive number of hometown visits, sales of consumer non-durables such as food and beverages during the Spring Festival exceeded expectations. On the supply side, replenishments at points of sales are greater than in previous years; on the demand side, the return of mass catering and banqueting during the year is expected to accelerate the recovery. With the increase in active socialization, tourism and consumption, the performance of food and beverage enterprises will improve significantly.

- Local life: The recovery of food delivery platforms exceeded expectations, and there is sufficient room for long-term growth in the industry; Online travel platforms have also entered the fast lane of growth, and industry leaders have accelerated their expansion. In the future, tapping into both local and non-local customer groups, the life service industry will continue to strengthen local supply of quality goods and services. This will become an important beachhead to enhance domestic demand and boost consumption.

- Duty-free industry: The rapid increase of tourist inflows into the island of Hainan has led to the recovery of offshore duty-free spending. During the first five days of the Spring Festival holiday, total sales of offshore duty-free shops in Hainan were RMB 1.685 billion, a year-on-year increase of 20.03%, and an increase of 325% over the same period in 2019. The increase in size of offshore duty-free facilities, the steady development of online shopping channels, the liberalization of duty-free channels in the city and international expansion is likely to provide multiple long-term growth channels for duty-free operators in China.

- Instant retailing: Instant retailing has become a new channel for purchasing lunar new year-themed goods during the Spring Festival holiday. According to JD.com data, hourly sales of such goods increased by 90% compared to the same period in 2022. Instant retail is a retail model that deeply integrates online and offline, and its main feature is "online order, offline delivery within 30 minutes". As consumers are warming up to such consumption modes, instant retailing is expected to bring new incremental growth to many industries and merchants.

Automotive

Getting around EV’s thorny profitability problem

In 2023, China's new energy vehicle industry will usher in a “post-subsidy" era where there will be less incentives available for buyers to opt for EVs. The onus of stimulating consumer demand for EVs over gasoline-powered cars will fall on car makers themselves. However, few of the NEV makers have managed to become profitable. The combination of surging material costs and intensified competition over the past two years have taken a severe toll on NEV maker’s profit margins. Hence, how to realize profitability has become a burning issue for NEV makers at this stage.

The new energy vehicle industry is a highly capital-intensive business. From R&D activities, construction of manufacturing production and parts sourcing, to the establishment of self-operated sales and service networks, all require a substantial commitment of long-term investment funds. This makes NEV makers something of a cash flow risk.

The reality is that only a small number of companies have turned a profit from the sales of electric vehicles. Most NEV companies are still in the stage of losing money and without subsidies the scale of losses will continue to grow. The production cost of new energy vehicles is about 20-30% higher than that of gasoline-powered cars of the same level. With government subsidies ending, OEMs will not be able to recover these costs through vehicle pricing alone. Almost all current EVs are sold at a loss. Obviously, this model cannot last.

But, there are exceptions. Two NEV makers, Tesla and BYD, have achieved profitability. Tesla has realized an operating profit of USD 13.7 billion in 2022, with an operating profit margin of 16.8%. Domestic NEV producer BYD is reported to have recorded a net profit of RMB 16-17 billion with a net profit margin of about 4%. We’ve identified some common factors that contribute to their profitability.

First, cutting down BOMs (bill of materials) and production costs through technological innovation. Tesla is leading in overall investment in technology innovation with R&D cost per car at about three times the industry average. This hefty investment seems to have paid off, bringing a visible reduction in production and operating costs. For example, the revolutionary 4680 battery (named as such because its cells measure 46mm by 80mm) can reduce the production cost of batteries by 54% through improvements in material and process redesign. The CTC (cell to chassis) technology – a process of integrating the battery cell directly into the vehicle chassis – can further drive down cost by simplifying the structure and improving the reuse of parts.

Second, achieving shorter product-to-market cycles and higher efficiency through vertically integrated supply chains also helps to reduce costs. With the help of deep integration of many outsourced parts into their own production process, NEV makers can gain greater control over core technology and hence obtain more leeway for potential disruptions. For example, BYD has reduced dependence on suppliers by manufacturing almost all critical parts in-house, including battery, electric engine, and semiconductor chips, which allows the EV maker to withstand supply chain disruptions and keep a larger share of profit in-house, at the same time having more control over technology stack and innovation.

Third, exploring new business models. Compared with traditional car companies, the business model around NEVs is changing. For example, Tesla uses OTA (over the air) to make cars no longer a one-off sale by turning software and data services into a new stream of profit. For example, in the full year of 2021, Tesla's operating income from services including autopilot software and other businesses was US$3.802 billion, an increase of 65%, accounting for 7% of its total revenue. In addition, software enabled functions has opened up new streams of revenues for OEMs. For instance, subscription of autonomous driving, on-demand purchase of digital content or entertainment features, predictive maintenance and personalized insurance can later on become important sources of revenues for OEMs.

Fourth, implementing other cost innovation measures. They include deployment of pre-emptive maintenance to reduce cost of vehicle recalls, modular design of software platforms to dilute software development costs, implementation of direct sales channels to reduce sales and marketing expenditures.

Both Tesla and BYD’s road to profitability could offer valuable lessons for EV start-ups as most of them haven’t achieved economies of scale whilst their R&D expenditures are still increasing and their control over suppliers is weak.

In the long run, as the market evolves from being policy-oriented to being market-driven, NEV makers need to invest in greater technology innovation, supply chain management and exploration of new source of revenues in order for them to stay in the running.

Life Science & Healthcare

The “10 New Measures” for coping with Covid-19 outbreaks

Since the release of the paper entitled 10 New Measures to Optimize COVID-19 Response ("10 New Measures") on 7th Dec. 2022, the number of newly confirmed Covid-19 cases has surged rapidly, reaching a peak of single-day infections of 6.94 million people on 22nd Dec. 2022. The upsurge caused a shortage of medical supplies and dealt a severe blow to the established medical system, resulting in patients being unable to receive much needed medical treatment. On 30th Jan. 2023, the number of newly confirmed infection cases decreased to 24,000 a day, easing the strain on medical resources and the medical system. With more COVID-19 therapeutic medicines receiving emergency approval from early 2023 onwards and the improvement of the medical system, China can now cope more effectively and efficiently with future outbreaks of COVID-19 and its variants.

Major challenges are as follows:

- Medical supply shortages

The abrupt change of Covid policy caused a shortage of supplies that failed to meet the dramatically surging demand. As a result, some symptomatic patients who were unable to do self-testing and self-treatment at home flocked to hospitals, increasing the risk of cross-infections. According to the National Administration of Disease Prevention and Control (China’s CDC), as of 28th Nov. 2022, the Covid-19 full vaccination rate among all age groups in China reached 90%. But the full vaccination rate of the elderly aged 60 plus and over 80 were only 86% and 66%, respectively. The health care system was further burdened by the weak Covid-19 vaccine shield caused by the low vaccination rate of the most vulnerable parts of the population.

- Medical staff in short supply

On 1st Feb. 2023, China’s CDC released the cumulative data on number of confirmed COVID-19 cases in hospitals. The number jumped from 164,000 on 9th Dec. 2022 to 1.6 million on 5th Jan.2023, a near tenfold increase in only one month. In addition, the daily hospitalizations of severe cases reached nearly 10,000 people per day from 27th Dec. 2022 to 3rd Jan. 2023, peaking at 128,000 new cases on 5th Jan. 2023. But by 30th Jan. 2023, however, daily new cases of hospitalization plummeted by 89.3% from its peak. Medical personnel were at highest risk of being infected due to their frequent and direct contact with patients. As a result, many medical workers were infected and unable to work, making it harder to cope with the soaring medical demand.

In response to the above-mentioned situations, local governments have taken various actions. Their experience and methods have provided significant and valuable insights on how to deal with future Covid-19 outbreaks.

- Expediting approvals and expanding capacity to tackle the medical supply shortage issue

To meet clinical needs, the National Medical Products Administration initiated emergency approval procedures for new drugs, greatly expediting the approval process. By the end of Jan. 2023, two more COVID-19 drugs had been approved under the emergency approval process, which took only two weeks from application to approval. By 6th Feb. 2022, a total of five COVID-19 drugs had received emergency approvals. In addition, the Zhejiang Provincial Department of Economy and Information Technology dispatched officers to factories to help companies expedite emergency approval and improve production capacity. By the end of 2022, output of cold antipyretics had reached 4.4 million tablets a day. Expedited approval and government-enterprise cooperation have effectively alleviated the shortage of medical supplies.

- Optimizing the stratification system of patients to reduce the work pressure on medical staff

A more refined hierarchical medical treatment system can effectively mitigate the impact of short-term outbreaks of Covid-19. In Suzhou city for example, the Suzhou government turned some nucleic acid test stations to "fever stations" to filter out patients who need medical care at the hospital. All in all, a total of 1,035 fever stations were set up in Suzhou in order to stratify patients. Apart from Suzhou, the Shanghai government also promoted the stratification of patients. In Jan. 2023, 2,594 fever clinics located in community-level medical facilities went into operation. Meanwhile, all community healthcare centres have set up 24-hour hotline services to provide medical information and consultation for Covid-19 symptoms. With these implementations, both cities successfully improved their hierarchical medical treatment systems, and easing the strain on medical resources.

Going forward, with the lessons learned from this outbreak of COVID-19, China's medical system will be better prepared to deal with future COVID-19 outbreaks.

On 30th Jan. 2023, the National Health Commission announced that the present COVID-19 outbreak had bottomed out in China. However, as the COVID-19 pandemic is still ongoing around the world, China remains at risk for COVID-19 outbreaks. According to the chief physician of the infectious diseases department of Tongji Medical College, antibody levels will remain high for 3 to 6 months in a recovered patient. Once a new Covid-19 variant emerges however, the possibility of reinfection remains high due to the gradual decline in antibody levels over time. Hence, another outbreak could occur in March to May 2023. Before the next outbreak, however, it is important to ensure adequate medical supplies. Also, efforts should be redoubled to increase the vaccination rate amongst the elderly and most vulnerable groups. The re-enforced hierarchical medical treatment system should be improved.

Government and Public Services

Infrastructure investment's key role remains critical but consumers must step up

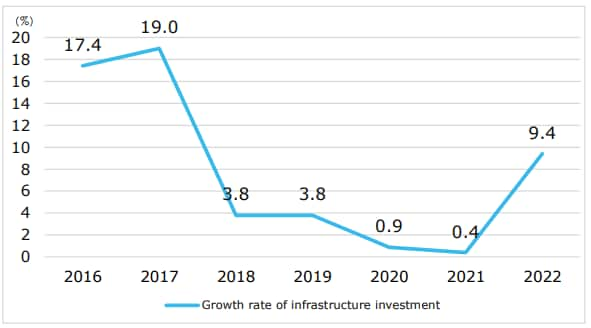

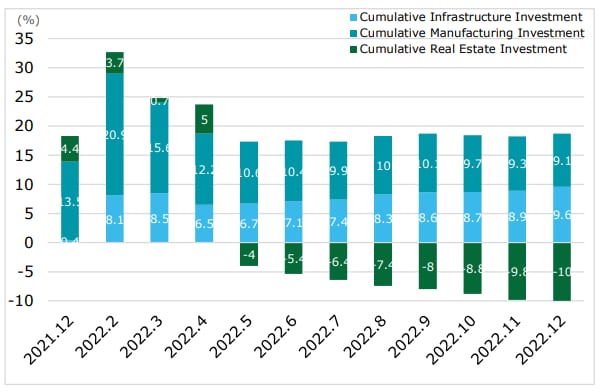

Infrastructure investment and manufacturing investment continue to underpin economic growth. Driven by infrastructure investment, gross capital formation accounted for 1.5 percentage points of GDP growth in 2022 and contributing 50.1% to GDP growth. Infrastructure investment grew at a rate of 9.4% in 2022, marking the first rebound since 2017. Manufacturing investment grew at a rate of 9.1%, which, together with infrastructure investment, drove the growth of fixed asset investment. As the key driver of the economy, growth in infrastructure investment effectively backstop China's economy against downturn in consumption, the fall in foreign demand and the rapid decline in real estate investment. At present, as pressure from contracting domestic demand, supply shocks and weakening expectations remains great, the foundation for a robust economic recovery is far from solid. In 2023, infrastructure investment is expected to be maintained at the same pace as in 2022 to sustain economic recovery.

Figure: Growth Rates of Infrastructure Investment from 2016 to 2022

Data source: National Bureau of Statistics of China

Figure: Cumulative Investment Growth in Fixed Assets by Sector in 2022

Data source: National Bureau of Statistics of China

Water conservation and transportation projects remain the traditional infrastructure investment priorities. In 2022, investment in water conservation and public facilities projects increased by 13.6% and 10.1% respectively. In addition, several major infrastructure projects were successfully completed. The report to the 20th National Party Congress on food security and energy security stated that, at the end of 2022, 38,000 projects, including energy, water, and transportation infrastructure, were newly added to the infrastructure project pool, which induce capital in the following 3 to 5 years . In terms of funding support, the Ministry of Finance(MoF) allocated a fund of 7 billion RMB in November 2022 to support 2023 national water conservancy project construction. In January 2023, the National Development and Reform Commission (NDRC) announced that investment from the central government budget will be issued in January and February to support the construction of new infrastructure projects, especially electronics and communication devices in remote locales in China’s central and western regions. The coverage of new infrastructure will be expanded further to provide digital infrastructure for rural revitalization and county-level urbanization strategies.

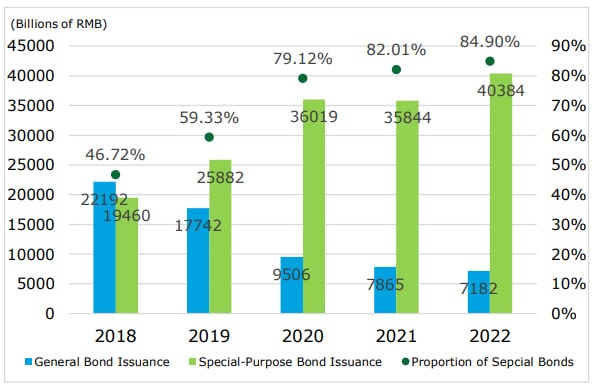

The pace of issue of local government special-purpose bonds remains accelerated and the scope of investment continues to expand. In 2022, local governments issued 4.04 trillion RMB special-purpose bonds, accounting for 84.9% of total government bond issuance. The pace of government special-purpose bond supply remains front-loaded in 2023. At the end of 2022, the MoF issued 2023 special-purpose bond quotas to local governments ahead of schedule. According to East Money Information Co., new local government special-purpose bonds issued in January 2023 reached 491.2 billion RMB. A November 2022 NDRC Notice expanded the investment areas in which local government special-purpose bonds can be used as project capital from 10 to 13. The three new areas are new energy projects, coal reserve facilities and infrastructure in national industrial parks. Hence we expect that more projects in the three new areas will begin in 2023.

Figure: Chinese Local Government Bond Issuance from 2018 to 2022

Data source: National Bureau of Statistics of China

The scale and variety of offshore RMB local government bonds will expand.

To broaden the issuing channels of local government bonds and reduce the crowding-out effect on domestic corporate bonds, after Shenzhen and Guangdong issued offshore RMB bonds totaling RMB 7.2 billion for the first time in October 2021, Hainan, Guangdong and Shenzhen issued offshore RMB bonds totaling RMB 12 billion again in November 2022, RMB 4.8 billion more than in 2021. Hainan Province issued 5 billion RMB, including a 2-year blue bond of 1.2 billion RMB, a 2-year sustainable development bond of 12 billion RMB and a 3-year sustainable development bond of 2.6 billion RMB, primarily for investment in water system restoration, marine ecosystem restoration, urban and rural sewage treatment, and other projects. This marks the first time that a Chinese local government issued both blue bonds and sustainable development bonds in the offshore market. To reach carbon peaking goals, more Chinese local governments are expected to issue green bonds and sustainability bonds offshore in 2023.