News

Hong Kong Tax Newsflash

Draft legislation on patent box tax concession

Published date: 10 April 2024

The draft legislation1 on patent box tax concession is introduced into the Legislative Council today. The Bill seeks to provide a concessionary tax rate of 5% for qualifying profits sourced in Hong Kong2 from eligible intellectual property (IP) created through research and development (R&D) activities. It aims to encourage enterprises to forge ahead with more R&D activities and create more IPs for promoting IP trading with a view to strengthening Hong Kong's competitiveness as a regional IP trading centre. Upon enactment, the patent box tax concession will apply retrospectively from the year of assessment beginning on or after 1 April 2023.

Eligible IP

Only income derived from an eligible IP could benefit from the preferential tax treatment under the proposed patent box regime. Eligible IP means the following IP that is generated from R&D activities:

- Patent;

- Plant variety rights3; and

- Copyrighted software.

Eligible patents and plant variety rights include not only those granted or registered, but also those under applications, in or outside Hong Kong4.

Eligible IP income

Eligible IP income includes:

- income derived from an eligible IP in respect of the exhibition or use of, or a right to exhibit or use (whether in or outside Hong Kong) the IP;

- income derived from the sale of an eligible IP;

- price of a product or service that includes an amount attributable to an eligible IP5 (embedded IP income); and

- insurance, damages or compensation derived in relation to an eligible IP.

The assessable profits from an eligible IP income would be ascertained by deducting the relevant outgoings and expenses incurred during the basis period, depreciation allowances, commercial building allowance and industrial building allowances, and adding balancing charge on assets used to produce the eligible IP income.

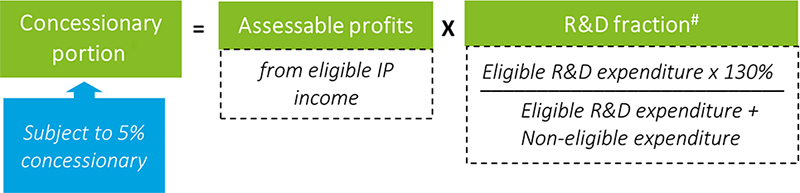

R&D fraction for concessionary portion of assessable profits

Hong Kong generally follows the nexus approach adopted by the Organisation for Economic Co-operation and Development (OECD) in designing the proposed patent box regime. Specifically, R&D fraction is a ratio which determines the portion of assessable profits that could benefit from the preferential tax treatment.

# Cumulative ratio; limited to 100%

Eligible and non-eligible R&D expenditures

Eligible R&D expenditure means expenditure incurred for an R&D activity that is directly connected to the eligible IP to which the eligible IP income relates.

When calculating the R&D fraction, a jurisdictional approach will be adopted to determine the scope of eligible R&D expenditures, which cover the expenditures on R&D activities that are:

- undertaken by the taxpayer in or outside Hong Kong;

- outsourced to non-associated person and undertaken in or outside Hong Kong; and

- outsourced to associated person6 that is a Hong Kong resident person7 and undertaken in Hong Kong.

Acquisition costs of IP are not regarded as eligible expenditures, but non-eligible expenditures. Interest payments and payments for any land or building are neither eligible expenditures nor non-eligible expenditures.

Please note that the purpose of classifying the R&D expenditures as eligible and non-eligible is for calculating the R&D fraction. Whether the expense is deductible should be governed by other provisions under the Inland Revenue Ordinance (IRO), e.g. Section 16B for expenditures on R&D activities, Section 16E for purchase of patent rights, Section 16EA for purchase of specified IP rights, subject to certain clarifications as discussed below.

Concessionary tax rate

The concessionary tax rate for the proposed patent box regime is 5%. In other words, the 5% tax rate will apply to the concessionary portion of the assessable profits from the eligible IP income.

Treatment of losses

A loss incurred in relation to income benefiting from the proposed patent box regime can be allowed to set off against assessable profits subject to a tax rate other than that provided under the regime so long as the amount of loss allowed is adjusted with reference to the tax rate difference. For example, tax loss from patent box regime (subject to 5% concessionary tax rate) can be used to set off against other assessable profits (subject to standard tax rate of 16.5%) of the taxpayer by adjusting the difference between the tax rates.

Record keeping requirements

Taxpayers are required to adopt a detailed mechanism of record keeping to track and trace the R&D expenditures and income derived from the eligible IP. As a transitional measure, taxpayers will be allowed to apply a ratio where the eligible R&D expenditures and overall expenditures are calculated on a three-year average rolling basis. After the transitional period8, taxpayers will need to change from the three-year average to a cumulative ratio.

Election

A written election for the tax concession is required. Once the election is made, it is irrevocable.

Our observation

Although the concessionary tax rate of 5% is not lower than those in neighbouring jurisdictions (e.g. Singapore also has a 5% concessionary tax rate), it is substantially lower than Hong Kong’s prevailing standard profits tax rate of 16.5%. We hope it will encourage enterprises to engage in more R&D activities and commercialise the R&D results and in turn increase Hong Kong’s competitiveness as an international innovation and technology centre and a regional IP trading centre.

Meanwhile, we observe several uncertain areas of the Bill which require further guidance from the Inland Revenue Department (IRD):

- Interaction with the enhanced R&D expense deduction: The Bill sets out the formula of calculating assessable profits from eligible IP income where outgoings and expenses incurred in the production of eligible IP income are deductible. Under Section 16B of the IRO, certain R&D expenditures e.g. R&D staff cost are eligible for enhanced deduction at 200% or 300%. It is unclear how the enhanced deduction of R&D expense will be taken into account in calculating the assessable profits from eligible IP income according to the Bill. (Update: It is clarified with the IRD that the enhanced deduction will be taken into account in calculating the assessable profits from eligible IP income in accordance with the formula under the patent box regime.)

- Interaction with capital expenditure for purchase of specified IP rights: According to the Bill, outgoing and expenses incurred during the basis period are deductible in calculating the assessable profits from eligible IP income. Under Section 16EA of the IRO, capital expenditure on purchase of specified IP rights, e.g. plant variety right, is deductible over 5 years. For instance, a taxpayer acquires a plant variety right in Year 1 before the enactment of patent box regime and is entitled to deduction of the acquisition cost over 5 years. The patent box regime becomes in force in Year 2. Strictly speaking, the capital expenditure was not incurred in Year 2 to Year 5. It is unclear how the deduction by instalment will be taken into account in calculating the assessable profits from eligible IP income according to the Bill. (Update: It is clarified with the IRD that the deduction by instalment will be taken into account in calculating the assessable profits from eligible IP income in accordance with the formula under the patent box regime.)

- Share of R&D expenditure under a Cost Sharing Arrangement9: The Bill does not explicitly mention whether the R&D expenditures (contributions) borne by a taxpayer under a Cost Sharing Arrangement would be considered as an eligible R&D expenditure for ascertaining the R&D fraction. It is uncertain whether reference could be made to the Departmental Interpretation and Practice Notes No.55 for enhanced R&D deduction where the R&D expenditures under a Cost Sharing Arrangement could be regarded as expenditures incurred by the taxpayer even if the R&D activities are undertaken by other entities outside Hong Kong. It would be helpful if the IRD can issue guidance in this area.

The proposed patent box regime, once enacted, will apply to the year of assessment 2023/24 while the earliest 2023/24 profits tax return filing due date is early May. With less than 1 month, taxpayers who would like to elect for the patent box regime in the upcoming profits tax return should get prepared of the relevant information although the form for patent box will not be released in the IRD's website until the enactment of the legislation. Taxpayers should also seek professional advice in evaluating any potential opportunities in IP development and trading in Hong Kong under the proposed tax concession.

1 Inland Revenue (Amendment) (Tax Concessions for Intellectual Property Income) Bill 2024

2 Foreign-sourced IP income is subject to the Foreign-Sourced Income Exemption regime (FSIE).

3 Plant variety rights are rights granted to the owners of plant varieties over cultivated plant varieties they have bred or discovered or developed.

4 There are additional requirements for patents and plant variety rights filed or granted outside Hong Kong if the applications for registration are filed outside the 24-month grace period after the commencement date of the Bill.

5 The income attributed to the eligible IP should be calculated in accordance with the commentary on the business profits article of the OECD Model Tax Convention and OECD Transfer Pricing Guidelines.

6 The persons are associated if one person was participating in the management, control or capital (generally means at least 50% beneficial interest or voting rights) of the other person or the same person or persons was or were participating in the management, control or capital or each of the affected persons.

7 A company incorporated in Hong Kong or, if incorporated outside Hong Kong, normally managed or controlled in Hong Kong.

8 The transitional period refers to the period beginning from 1 April 2023 to the last day of the taxpayer’s basis period for the year of assessment beginning on 1 April 2025.

9 A Cost Sharing Arrangement is a contractual arrangement among business enterprises to share the contributions and risks involved in the joint development, production or the obtaining of intangibles, tangible assets or services with the understanding that such intangibles, tangible assets or services are expected to create benefits for the individual businesses of each of the participants.

Tax Newsflash is published for the clients and professionals of Deloitte Touche Tohmatsu. The contents are of a general nature only. Readers are advised to consult their tax advisors before acting on any information contained in this newsletter.

If you have any questions, please contact our professionals:

Authors

Doris Chik

Tax Partner

+852 2852 6608

dchik@deloitte.com.hk

Carmen Cheung

Senior Tax Manager

+852 2740 8660

carmcheung@deloitte.com.hk

Kiwi Fung

Tax Manager

+852 2258 6162

kifung@deloitte.com.hk

Global Business Tax Services

National Leader

Andrew Zhu

Tax Partner

+86 10 8520 7508

andzhu@deloitte.com.cn

Hong Kong

Raymond Tang

Tax Partner

+852 2852 6661

raytang@deloitte.com.hk

Recommendations

Hong Kong Tax Newsflash

Newly published advance ruling and updated guidance on single family office tax concession

Hong Kong Tax Newsflash

Passage of stamp duty adjustments for residential properties