{kind=link}

{kind=link}

{kind=link}

{kind=link}

India economic outlook, October 2022 has been saved

Cover image by: Jaime Austin

The seemingly unending saga of global economic uncertainties (which we discussed at length in our previous outlook) has begun to negatively impact India’s main drivers of growth. And recent events—such as the US Fed’s 75-basis-point (bp) hike with assurances of more to come, a slowdown in China with growth falling below the rest of Asia for the first time since 1990, and the United Kingdom’s steepest tax cuts since 1972 (but reversed recently)—have provided little solace either, with likely implications on INR and the country’s current account deficit. These events prompted the Reserve Bank of India (RBI) to implement another aggressive rate hike of 50 bps in September, taking the policy rate up from 4% to 5.9% in a span of six months.

So volatile is the current economic environment that if one is looking for certainties from the recent data releases, it is unlikely that a consistent outlook will emerge. In this outlook, we try to decipher the current data with a broader focus on drivers of growth, inflation, currency, and the current account. Although we remain optimistic about India’s economy in the foreseeable future, this forecast comes amid a lot of debate.

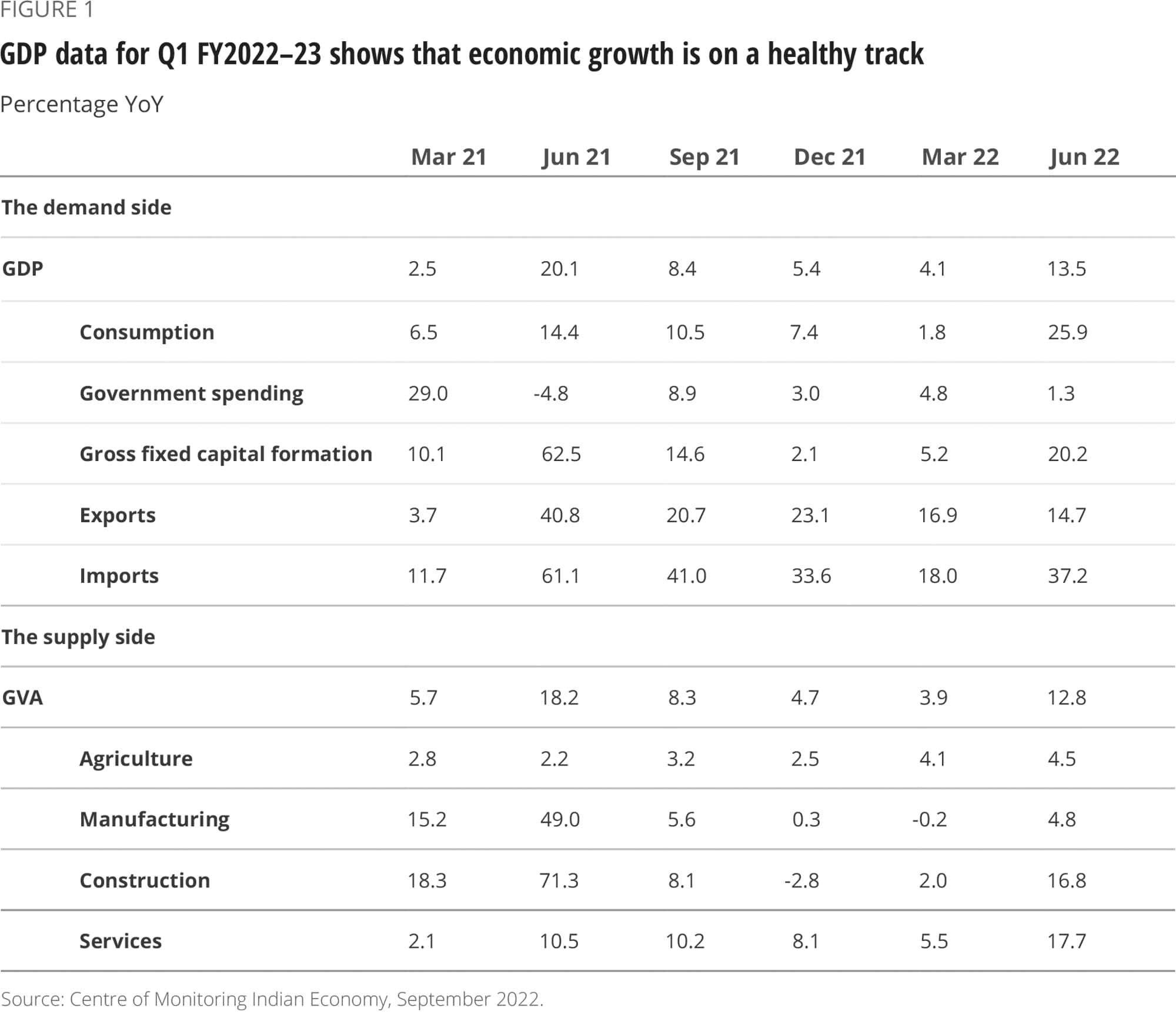

The latest GDP numbers for Q1 FY2022–23 suggest that economic growth is on a healthy track (figure 1). Consumers, after a long lull, have started to step out confidently and spend—private consumption spending went up 25.9% in Q1. Investment also kept pace with demand, although uncertainties around supply and prices are preventing firms from committing to large capex spending. Nevertheless, aided by a strong rebound in demand drivers, the Indian economy grew by 13.5% in Q1 FY2022–23.1

On the production side, the contact-intensive services sector also witnessed a strong rebound of 17.7%, thanks to improving consumer confidence. Agriculture, the only sector that consistently performed well throughout the pandemic, remained buoyant. Industrial growth boosted from accelerating growth in “construction” and “electricity, gas, water supply and other utility services” sectors.

A sector that has not yet taken off sustainably is manufacturing, which witnessed modest growth of 4.5% in Q1 (see “Are we underestimating the contributions of manufacturing?” for more on this). Higher input costs, supply disruptions, and labor shortages due to reverse migration have weighed on the sector’s growth. According to the Reserve Bank of India’s (RBI’s) data on nonfinancial firms, surging raw material costs have stressed the profitability and margins of companies.2

It is possible that the current estimation of the manufacturing sector growth may not be capturing the true activity. The sector’s contribution is estimated using the index of industrial production data, which is still indexed at the 2012 base. Since then, government schemes and policies to boost the manufacturing sector may have structurally changed the sector’s contribution. For instance, considering the exports basket, one may notice a significant jump in manufacturing exports from India as well as changes in the export composition since 2012. Additionally, India is moving up the value chain in its export basket as it is now exporting more engineering goods, chemicals, and pharma products. A study by the State Bank of India (SBI) has also highlighted the need for serious introspection regarding a fair representation of the manufacturing sector in India’s GDP.3

High-frequency data provide a mixed signal about the growth drivers in the near future.4 Exports—the first growth driver—are slowing down and are likely to moderate along with the probable global economic slowdown. Government spending—the second driver—is already at an elevated level, thanks to the pandemic, and the government will likely focus on its prudence in utilizing limited resources. The good news is the share of capital expenses is going up even as the government is reducing revenue expenses. Multiplier effects of this spending will aid in growth in income, assets, and employment for years to come. Strong tax revenues may support further capital spending in the future.

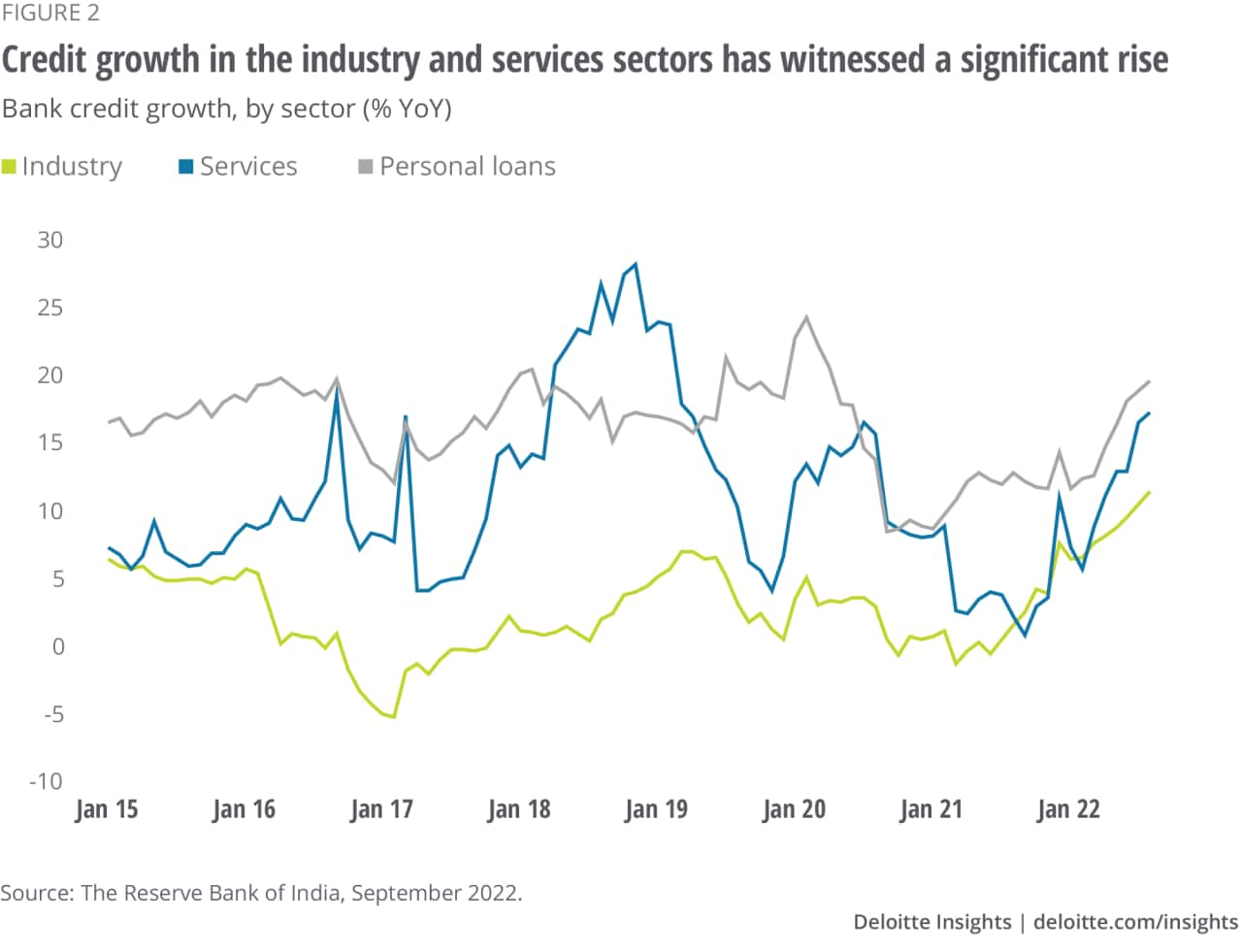

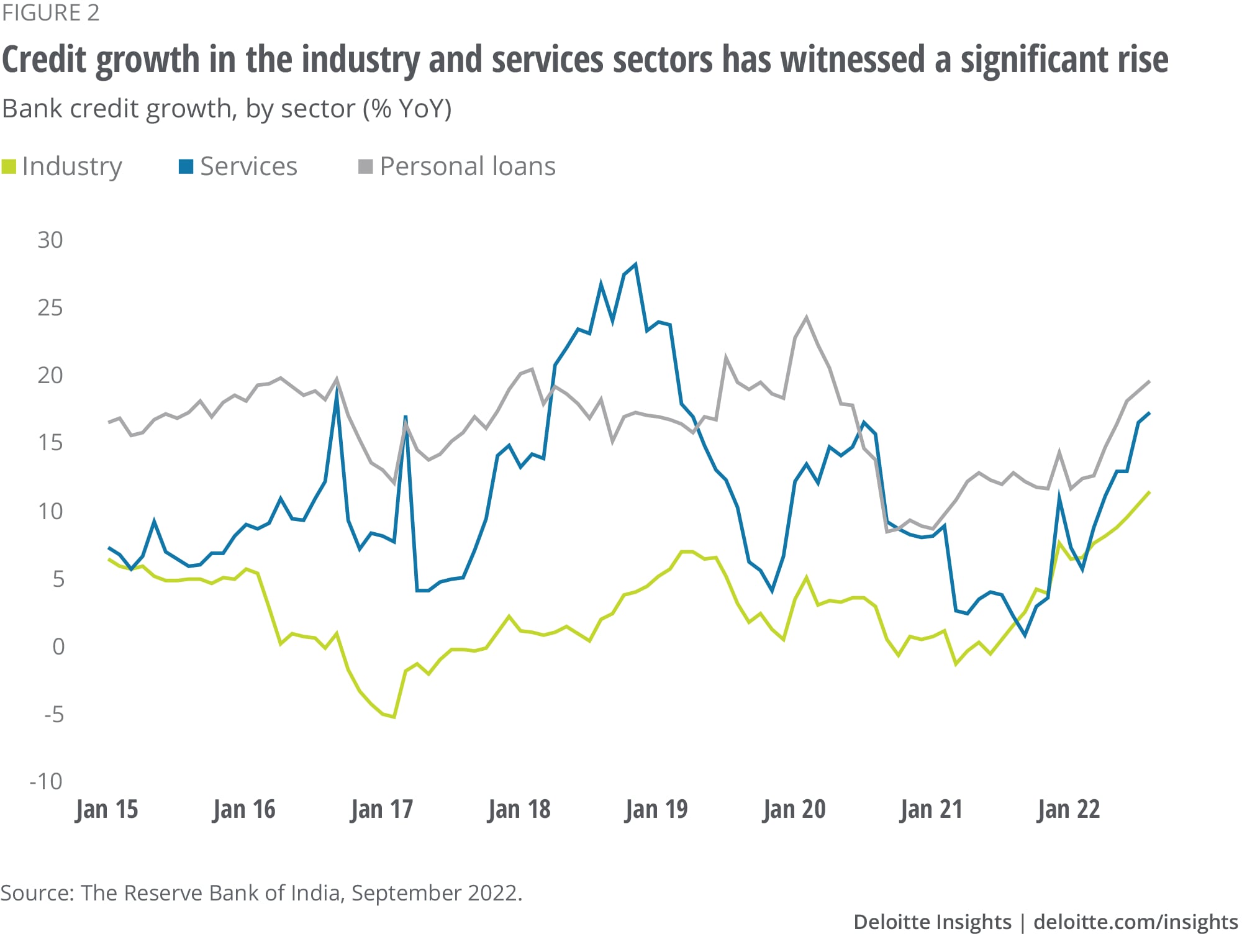

The purchasing managers’ index (PMI) suggests that economic activity stayed strong in July and August. Input cost inflation also fell to the lowest in 2022 due to falling commodity prices, including the lower prices of aluminum and steel.5 This bodes well for company margins. Capacity utilization in the manufacturing sector is now above its long-run average (although it varies quite a lot across sectors) and bodes well for fresh investment activity in creating additional capacity.6 Credit growth in the industry and services sector has also risen remarkably (figure 2), suggesting that prospects for capex investments—the third growth driver—by companies are brighter. Sustained demand growth may be the most-awaited cue for a sustained push for investment.

Consumer demand—the fourth, and perhaps the most important, growth driver—has improved significantly in recent quarters. However, spending has not grown sustainable despite improving consumer confidence. For instance, retail sales are growing but the pace is patchy, and auto registrations have remained muted. We expect that receding pandemic fears and the upcoming festive season could give a much-needed boost to the consumer sector.

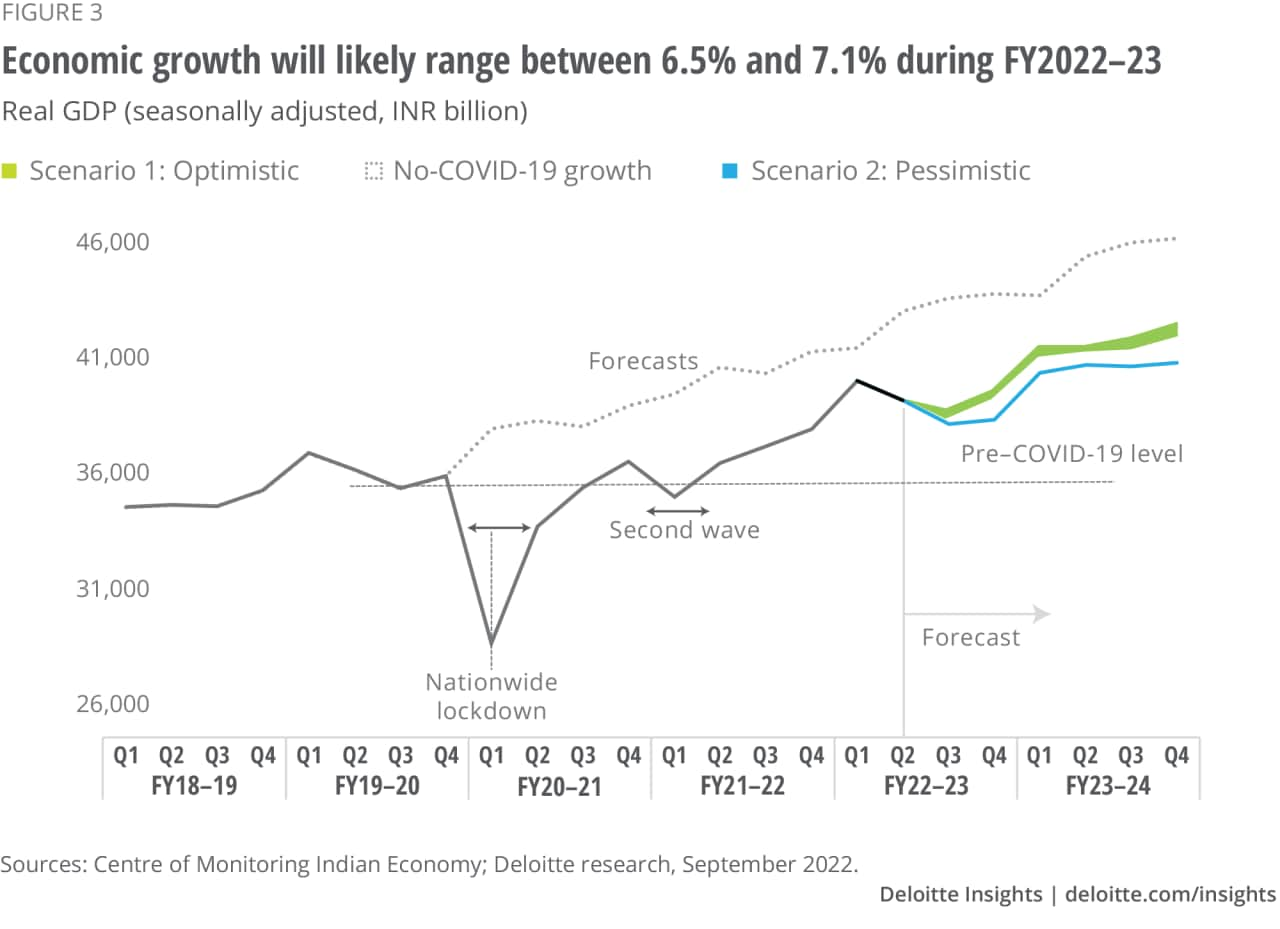

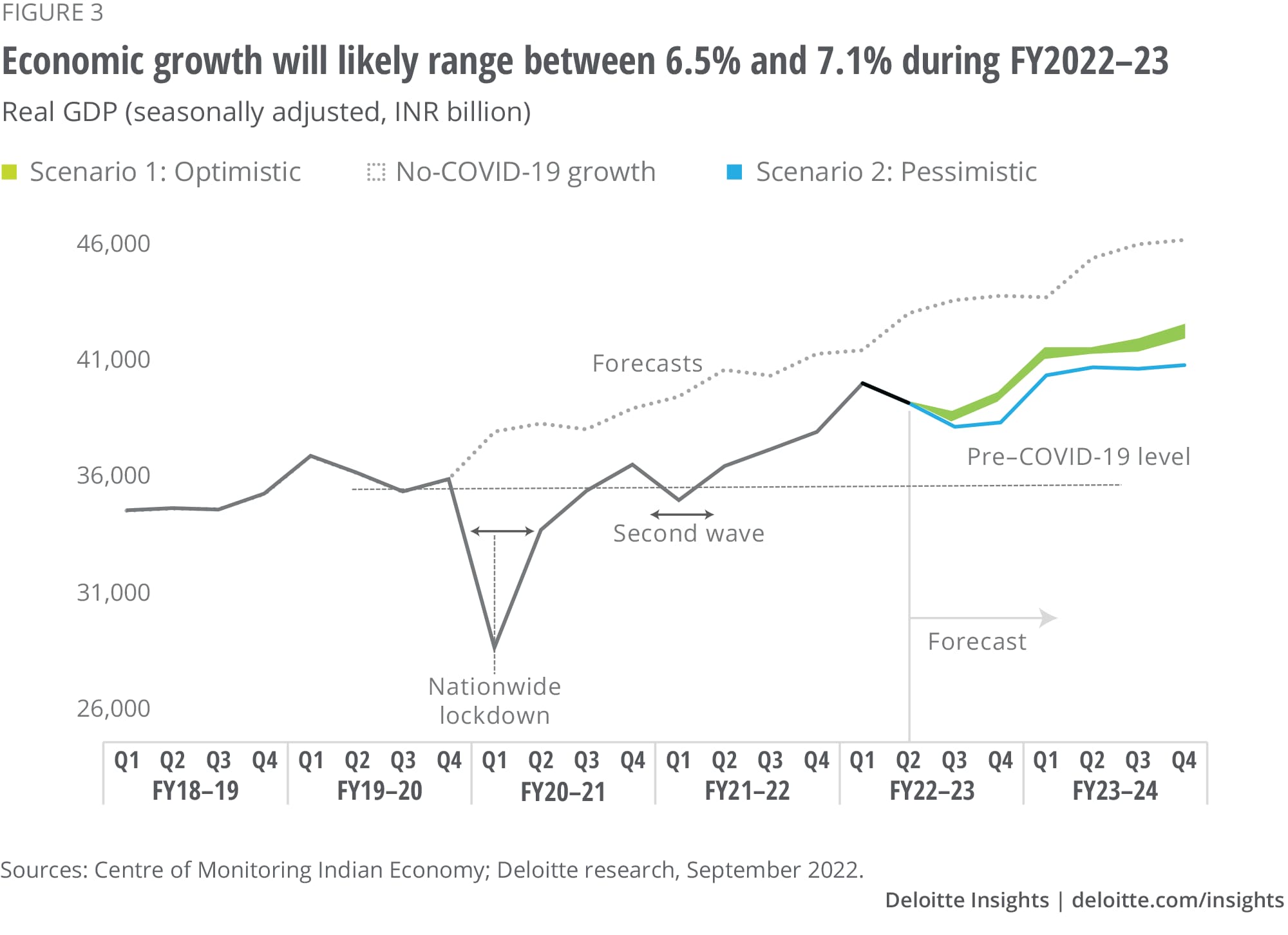

Expectations: There are several moving parts to the story, lending low visibility to how growth drivers would shape up in the coming quarters. Assuming that the dust of uncertainties settles down over the next few quarters (the optimistic scenario), we expect GDP to maintain reasonable growth momentum, although not as much as we had expected at the beginning of the year. Cognizant of the global economic uncertainties and a possible slowdown, we remain cautiously optimistic about growth, which may range between 6.5% and 7.1% during FY 2022–23 and between 5.5% and 6.1% the following year (figure 3). Economic activity will likely pick up rapidly early next year, contingent on the revival of the global economy and improving economic fundamentals.

On the other hand, downside risks are significant and if they weigh on the economic fundamentals and outlook, we may see a substantial slowdown (the pessimistic scenario). We highlight the challenges in the following section.

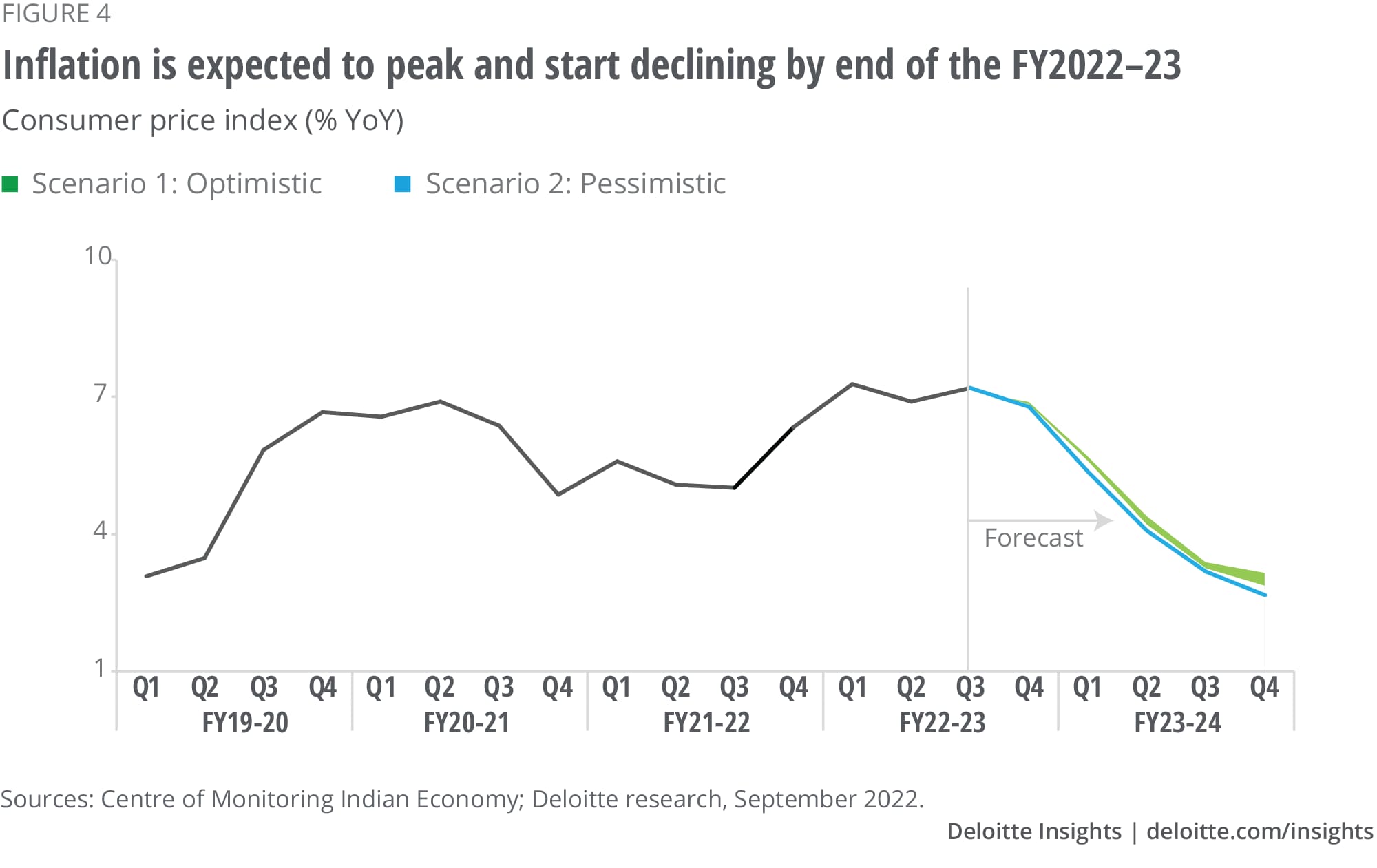

The biggest worry is that of high inflation (which has persisted for way too long) and all the challenges that come along with it. Inflationary environments increase the costs of doing business, impact profitability and margins, and reduce purchasing power. In short, inflation thwarts both supply and demand. Central banks’ monetary policy actions, in response to rising inflation, can impede credit growth and economic activity, thereby intensifying the probability of a recession in a few advanced nations.

The overall consumer price index (CPI) inflation has remained above the upper range of the RBI’s target rate for most of the year. Earlier this year, inflation was largely driven by higher commodity prices and supply disruptions. While upstream energy companies benefitted due to higher realizations, profitability in most other sectors remained stressed due to rising production and transportation costs.7 This prompted manufacturers, from consumer goods to automobiles to steel, to pass on the higher costs to consumers by calibrating price increases.

The runaway inflation prompted the government to reduce excise duty to bring down prices of petrol and diesel, as well as for essential items such as edible oil and other imported raw materials for industries. It also imposed bans on exports of certain commodities to address domestic supply issues. The RBI, meanwhile, promptly hiked its repo rates by 1.9 bps in a span of five months and introduced the standing deposit facility to absorb the excess liquidity (see sidebar, “Why RBI’s tighter monetary policy makes sense?” for more on this).

It was only in the second half of Q1 that commodity prices witnessed some corrections. Lately, inflation has been driven primarily by consumer food prices, suggesting a seasonal impact of variations in rains across the country on agricultural output. Rising food prices hurt rural demand the most, and in August, rural inflation witnessed a greater increase compared with urban inflation. This is not good news for rural demand, which has been struggling to revive.

A large part of the inflation is driven by supply-side factors, while demand-pull inflation drivers remain range bound. According to a study by the SBI, 65% of CPI inflation in May was due to supply-side disruptions and had marginally dropped to 58% in July.8 However, it increased again to 61% in August, suggesting supply disruptions in the food products owing to unseasonal rains causing their prices to rise.

Can a tighter monetary policy help contain inflation caused due to supply-side challenges and not derail the nascent recovery instead? The reason why the RBI’s move is justified is that tighter policy helps in anchoring inflation expectations when inflation has remained persistently high for a very long time (over two years now). Prolonged inflation feeds into expectations, which means people expect the inflation trend to continue and expect prices to remain high in the future as well and change their behavior accordingly. Higher inflation expectations result in consumers postponing purchases, and therefore, delaying the demand pickup. Producers raise the prices of goods assuming that the higher production costs will persist. That results in a rise in core prices. In fact, core prices are on a steady rise, which is a cause for concern because they often tend to be sticky-down. The RBI’s move is thus prudent to contain inflation expectations and prevent adaptive expectations from impacting demand and preventing the spiraling of prices.

The other challenge is the rising current-account deficit and currency depreciation against the dollar. While a rebounding domestic economy is resulting in higher imports, moderating global demand is causing exports to slow. The US dollar’s unrelenting rise and global inflation are further causing India’s import bills to rise.

INR’s depreciation against the US dollar is more due to the appreciation of the latter owing to the flight to safety among global investors amid global uncertainties. It is appreciating against the euro, pound, and yen, suggesting that the macroeconomic fundamentals of the Indian economy remain strong.

Yet, the RBI had to intervene to contain volatility and ensure an orderly movement of the rupee. The RBI’s intervention is leading to a drawdown in foreign exchange reserves. Consequently, the import cover from reserves has reduced to nine months from a high of 19 months at the start of 2021 (although, it remains above the benchmark of three months).

Expectations: With global economic growth likely to moderate, global prices may ease. A possible moderation in crude oil and industrial raw material prices may reduce inflation by mid of 2023. The falling prices of oil and gas, copper, zinc, and other commodities are likely to help sectors such as consumers, metals, cement, and automobiles in the coming quarters. Falling cost of production will be of great help to local small-scale manufacturers that have struggled to survive during the pandemic and maintain their market share because of rising prices.

The fall in prices may be short-lived if a sustained demand improvement exceeds supply, leading to overheating of the economy. Similarly, despite easing commodity prices, the current account may remain a concern as India’s growth path will likely defy the global slowdown, resulting in higher imports than exports.

Optimistic scenario: The Russia-Ukraine crisis does not escalate but prolongs for a long period. Growth in the United States and EU slows down over a tighter monetary policy.

Pessimistic scenario: The crisis continues for a prolonged period. Globally, nations impose sanctions on Russia. However, tensions become far and wide with several nations getting directly involved in the war. The United States and Europe enter a recession and the pandemic results in lockdowns in several economies.

The path to recovery has been lengthier than we’d expected at the start of the year. There are too many variables that blur the outlook, and we will likely have some clarity over the next few months as we assess the energy crisis in Europe and the slowdown in China. The strength of all four economic drivers will be key for sustainable growth, and there are possibilities that not all four may reach full steam.

Press Information Bureau, India.

View in ArticleRBI data.

View in ArticleSBI Research Ecowrap, Headline GDP hides more things than it reveals: Time to seriously introspect on the measurement of IIP and CPI basket, last revised in 2012: FY23 GDP growth now at 6.8%, September 1, 2022.

View in ArticleData on high-frequency numbers mentioned in the next couple of paragraphs has been obtained from the CMIE and Haver analytics.

View in ArticleEconomic Times, “India's manufacturing growth trends higher as input cost inflation eases,” September 1, 2022.

View in ArticleAanchal Magazine and Sandeep Singh, “Higher capacity utilisation signals investment revival,” August 6, 2022.

View in ArticleNIFTY earnings data for Q1 FY2022–21.

View in ArticleSBI Research Ecowrap, CPI inflation eases on the back of easing of supply side constraints: Demand pull inflation contribution has risen, August 12, 2022.

View in ArticleCover image by: Jaime Austin