China economic outlook, December 2022 has been saved

Cover image by: Jaime Austin

The Q3 GDP data1 clearly shows that the Chinese economy is recovering. And the growth in Q4 will likely see marginal improvement, assuming the policy focus pivots toward economic reflation and decisive action is taken to stabilize the property market, which holds the key to consumer confidence. In light of this, a GDP growth of 3.2%–3.5% remains a realistic goal for 2022.

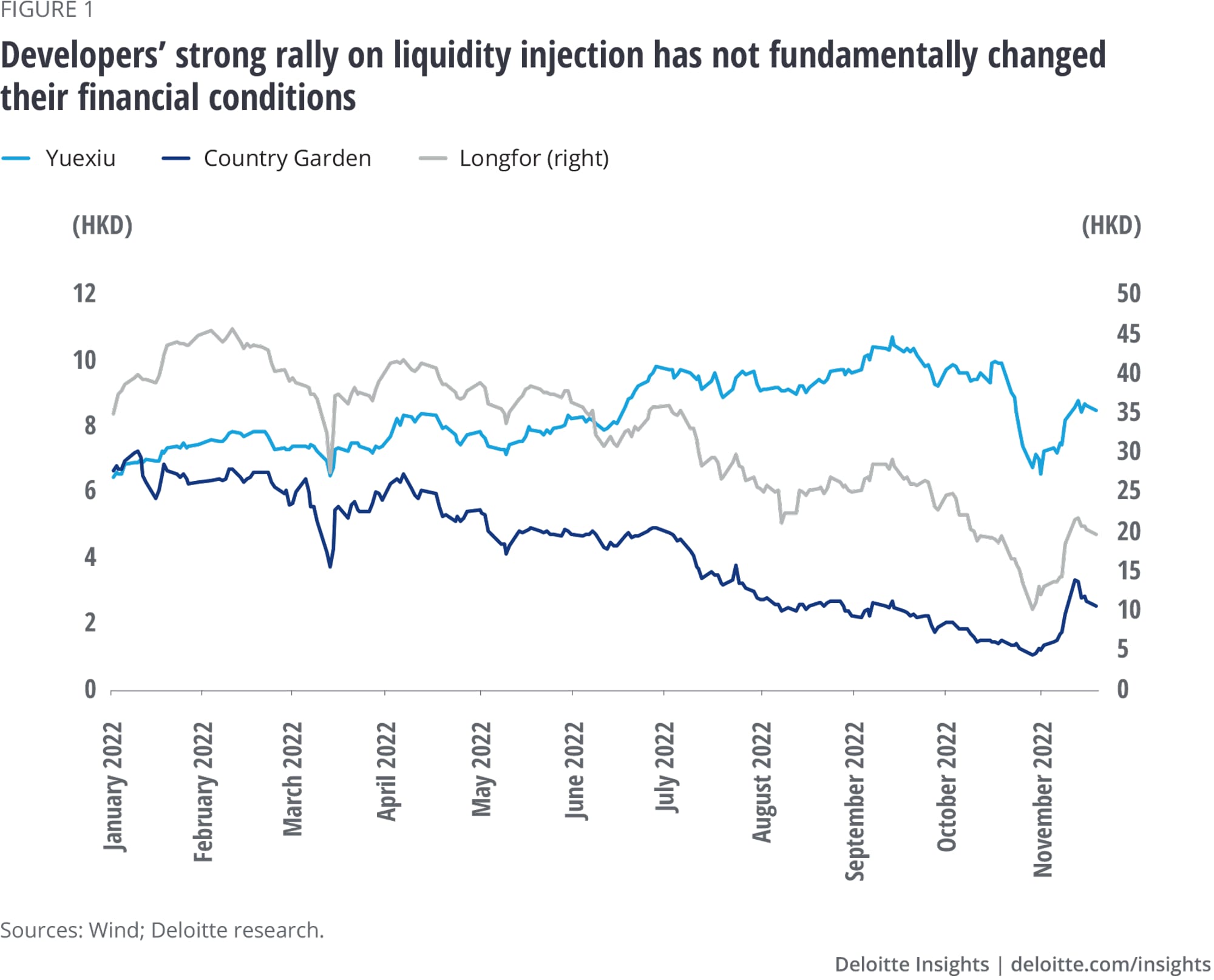

However, financial markets have been experiencing jitters since mid-October because investors are unsure about the government’s policy response. The dramatic sell-off of property developers in both the equities and off-shore bond markets in October suggests that the financial distress plaguing the real estate sector may present a bigger risk to consumption than expected a few months ago. The ferocious rally of equities, in both the mainland and Hong Kong, and a sharp rebound of the RMB after the German Chancellor Scholz’s visit to Beijing have suggested that investors are banking on an easing of the government’s zero-tolerance COVID-19 policy (According to the Wall Street Journal,2 China has agreed to approve BioNTech’s vaccines for foreigners in China, which appears to be a step toward expanding it later down the road). Despite the latest reimposition of lockdowns in several cities such as Shijiazhuang in Hebei Province, the board is moving toward a gradual easing of COVID-19 restrictions.

The release of the Q3 GDP data was delayed by the 20th Party Congress, but at 3.9% year over year (YoY), growth was much stronger than the earlier consensus of approximately 3%—our forecast had ranged between 2.5% and 3.2%. Growth was led by consumption (e.g., auto) and net exports, contributing 2.1 and 1.1 percentage points, respectively. Export growth, although losing some momentum in September, remained steady at 5.7%.3

However, the property sector, once a key driver of growth, continued to remain a drag on the economy in Q3. In fact, declining investment in the property sector, which began a year ago, has become even more pronounced, declining by more than 12% in Q3 and 16% in October 2022.4 This has raised questions over the need for further measures to boost the real estate sector, as previous moves such as lowering mortgage rates and tax rebates have clearly been viewed as inadequate by the market.5

While its role as a growth driver remains important in the short term from reflation and fiscal revenue standpoint, the property market is likely to become a drag on the Chinese economy in the medium term. That is why the government is keen to boost confidence in the property sector by implementing new support measures. Most recently, the Ministry of Finance, People’s Bank of China (PBOC), and China Banking and Insurance Regulatory Commission (CBIRC) announced a slew of support measures before the National Day celebrations got underway. The PBOC lowered the lending rate for housing provident fund loans by 0.15 percentage points to 2.6% and 3.1% for tenures less than five years and longer than five years, respectively.6 The CBIRC reduced mortgage rates for first-time home buyers in some cities,7 while the Ministry of Finance announced it will offer tax rebates to those purchasing new homes after selling their previous properties within a year.8

Taken together, these measures serve to underscore the government’s policy goal of reflating the economy through the property market. Why? Given the size of the real estate sector (it accounts for roughly one-quarter of the economy), it will be impossible to rely on other emerging sectors such as electric vehicles or advanced manufacturing to fill the gap left by the property market this year or even the next. More importantly, however, Chinese consumers can still reduce their savings at a time when local governments and many firms must do the exact opposite. If all actors tighten their belts at the same time, an economic downturn will be unavoidable.

In the long run, fiscal revenue of local governments must be broadened out, but in the immediate future, other sources of revenue can’t move the needle given the sheer size of the contribution from land auctions. Notwithstanding the extraordinary level of consumer resilience, there is a risk of consumers becoming more cautious should the current bearish sentiment become more pervasive against a backdrop of several major global property markets such as the United States, the United Kingdom, and Canada showing cracks.

We have held the view that China’s property sector does not present a systemic risk on the basis of 1) high consumer savings rate; 2) low consumer leverage; and 3) most banks’ creditworthiness being perceived as sovereign risk by the general public. Indeed, the mortgage boycott is being forcefully addressed by the government.9 A relief fund was set up to ensure that developers can finish their projects, and there have been subsequent assurances from policymakers on implementing further relief funds (e.g., PBOC Governor Yi Gang’s pledge at the Finance Ministers and Central Bank Governors of the G20 meeting). However, financial distress among many large private developers owing to slumping home sales has been exacerbated by a strong US dollar and rising global interest rates.

All these support measures will likely improve sentiment on the margins, but their impact should not be overestimated. For example, tax rebates are only available to those who have sold their apartments within a year, and such rebates will be calculated on an incremental basis. Net savings from tax rebates and reduced mortgage payments are therefore unlikely to be substantial. At the end of the day, the underlying motivation for most Chinese consumers to move up the property ladder is the expected appreciation of house prices (so far, housing has been the principal form of investment), not lower interest rates. Major developers have incurred staggering corrections in term of both stock prices and offshore bond yields; such financial distress suffered by developers could result in further difficulties of property investment, putting additional strain on local tax revenues.

Finally, with the conclusion of the Party Congress, core economic issues are expected to rise again to the fore, but whether to relax the zero-tolerance COVID-19 policy has been perceived by investors as an acid test of striking a balance between economic development and safeguarding public health.

First, will the policy be adjusted? China’s decision of shortening quarantine from 7 plus 3 days to 5 plus 3 days for inbound travelers and scrapping penalties on airlines to bring infected passengers on November 11, 2022 is a clear signal that the COVID-19 policy will be adjusted, albeit gradually. The reality is that any drastic adjustment is unlikely, but incremental changes might well be possible as more international flights will be made available soon, such as direct flights between Beijing and Singapore.

Second, the PBOC is expected to further reduce interest rates as the Fed’s tightening campaign appears to end earlier than previously expected. At least with the most recent rate hike (75 basis points on November 2, 2022), the Fed might be getting closer to the end of its tightening cycle. However, as China continues to run a comfortable current account surplus, a weaker RMB should not be a constraint on policymakers’ continued monetary easing.

In conclusion, a continued cyclical recovery should not obscure the need for reviving the economy. October export data (–0.3%), a rare decline in US dollar terms in years, has highlighted potential risks on external demand caused by weakening economies in both the United States and Europe, adding a sense of urgency on reflation.

What China needs is not a 2008-type fiscal stimulus, which has been repeatedly denied by policymakers, but a more focused reflation of the property sector and continued fine-tuning of the COVID-19 policy. In our view, the “comprehensive” package of injecting liquidity into property sector announced on November 14, 2022, has signaled a clear pro-growth policy stance; and investors have cheered this package. Going forward, the focus will be on balancing long-term goal of unleashing demand from new growth drivers and temporally relying on the property sector for growth stabilization.

{kind=link}

{kind=link}