Eurozone has been saved

Cover image by: Jaime Austin

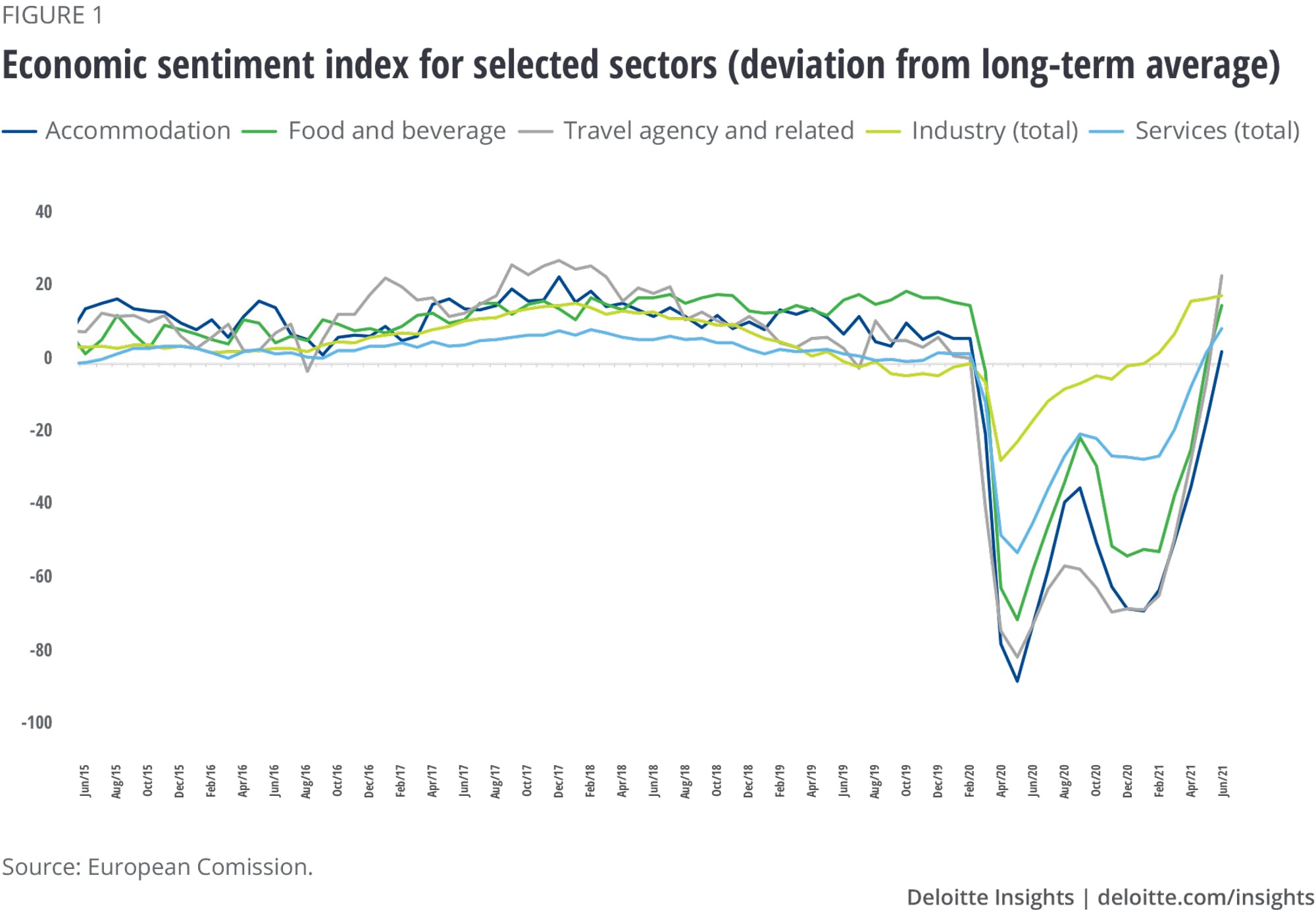

The major early economic indicators for the Eurozone have reported values unseen in years, if not decades (figure 1). The Purchasing Managers’ Index for June indicated that the Eurozone grew at the fastest rate in the last 15 years.1 This is due to two developments. First, the export-oriented manufacturing sector benefitted from booming world trade. Second, the Eurozone’s services sectors have recovered strongly—the tourism and travel sectors have especially seen a sharp increase in sentiment since May, with travel restrictions easing in Europe. This is welcome news for the southern European countries, which rely heavily on tourism. In Spain, for example, tourism contributes almost 12% to Spanish GDP.2

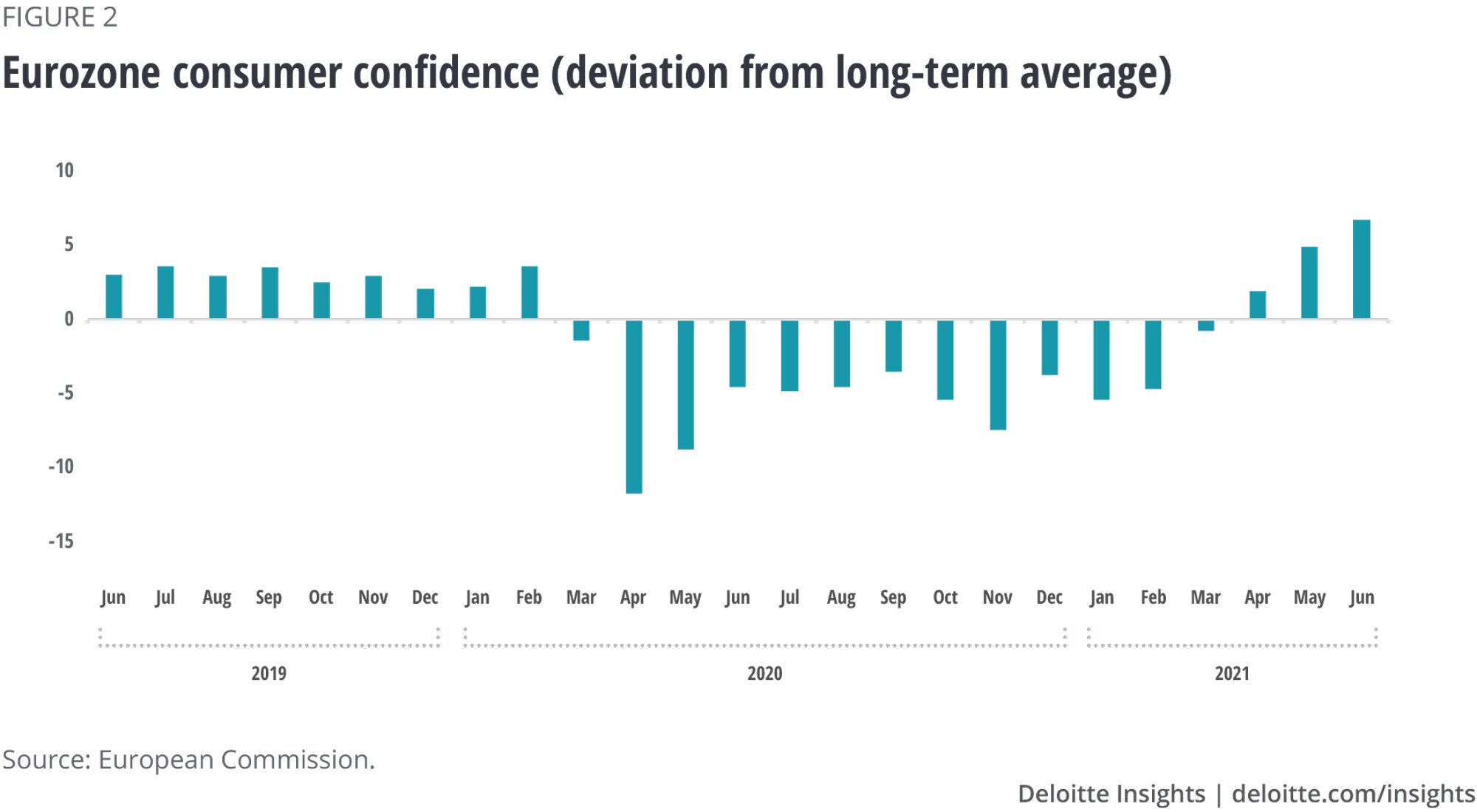

For the first time since March 2020, consumer sentiment exceeded its long-term average in April 2021 and continued to increase strongly in May and June, buoyed by the general easing of containment measures that began in May. This indicates that the fear that the crisis would have long-lasting negative effects and result in consumer hesitancy seems to have not materialized (figure 2). At a country level, however, declining consumer confidence in Spain and Portugal underlines that newly rising infection rates caused by the spread of the Delta variant might put a break on the recovery of consumer spending in the upcoming months.

The overall outlook for the European economy is therefore positive, barring a drop of bitterness. The manufacturing industry is struggling with scarce input factors, especially semiconductors, which is holding back production.3 The production of the German car industry, for example, fell by 13% in June from May, after a steep 20% fall in May. Compared to last autumn, German car production has halved.4 Also, other industrial raw materials experienced strong price increases in recent months—the price of tin, for example, exceeded its 10-year high in May, driven by an increased demand for electronics during the pandemic.5 While most of these changes are assumed to be temporary, continued bottlenecks could become a drag on the recovery.

Further economic stimulus will come from the European recovery fund, which is about to release its first tranche of money. The €750 billion fund, based on joint debt, was established a year ago to help EU member states recover from the COVID-19 recession and make European economies greener and more digital.6

Member states submitted plans to the European Commission outlining how they would use their shares of the fund and which economic reforms they commit to implement. By mid-July, 12 countries—including the biggest Eurozone countries of Germany, France, Italy, and Spain—received the green light for their plans, and the fund money is likely to flow from summer onward.7 The remaining EU countries are likely to receive approval for their plans over summer, although there are disagreements over Hungary’s recovery plan.

The fund consists in equal parts of grants and loans; 70% is to be spent in 2021 and 2022, the rest in 2023. Southern European countries, which were severely hit by the COVID-19 crisis, will receive more fund money than their less affected counterparts. For instance, Italy and Spain will receive close to €70 billion of grant money each.8 The European Union expects that the program will lift European GDP by 1.2% in 2021 and 2022.9 Taking a longer perspective, Standard & Poor’s estimates that the effects will be somewhere between 1.5% and 4.1% of GDP until 2026. At a country level, the fund is likely to have the biggest impact on Greece and Bulgaria—in a positive scenario, their GDP could increase by up to 18% until 2026. The growth for Spain is likely to lie somewhere between 3% and 10%, and for Italy, between 1.9% and 6.5%.10

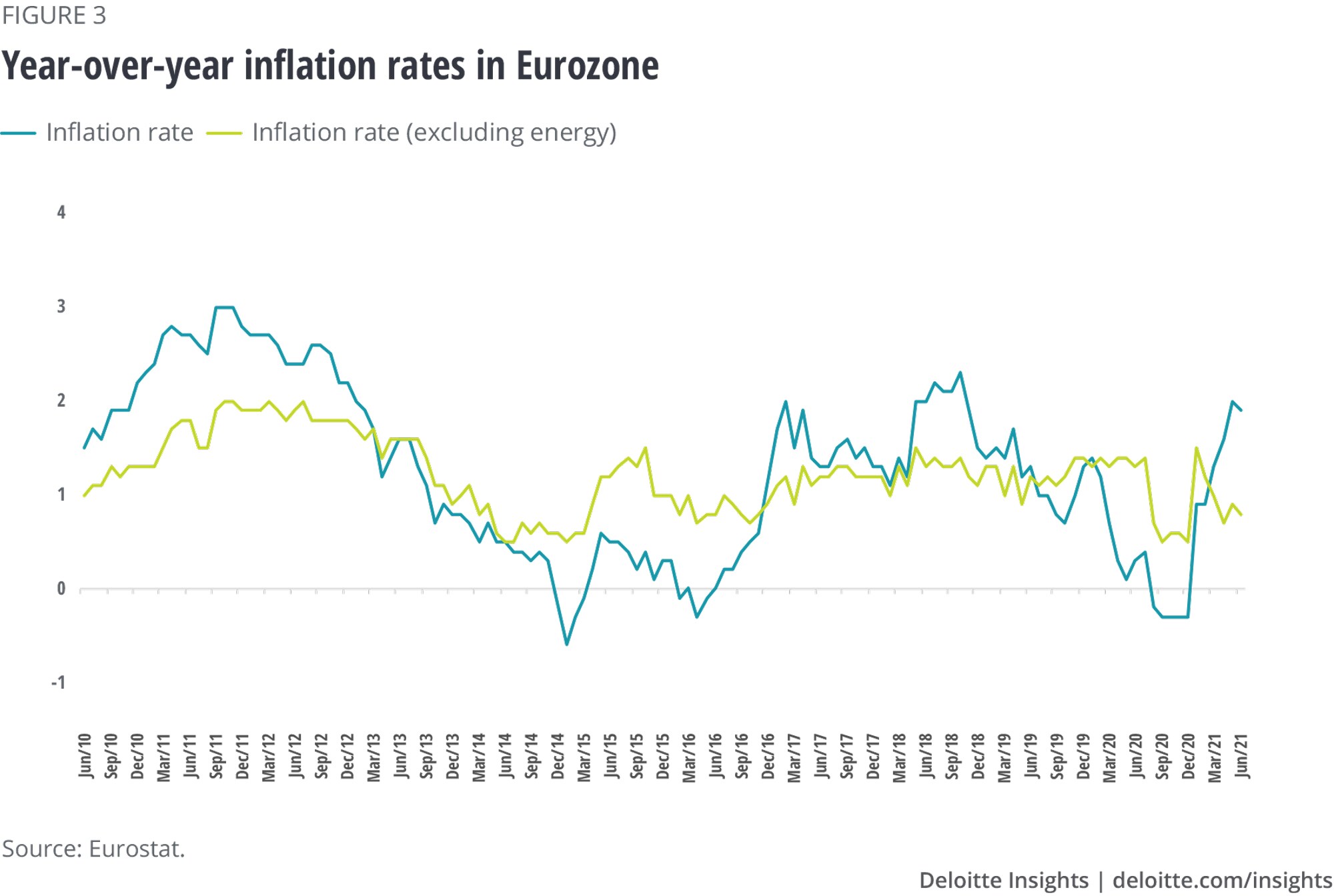

A side effect of the recovery underway is a rise in inflation. In the Eurozone, the inflation rate in June stood at 1.9% (figure 3); in Germany it was higher, at 2.3%.11 This is hardly runaway inflation, but is a significant change nevertheless. The last time the Eurozone’s inflation rate was above the European Central Bank’s (ECB’s) 2% threshold was in 2012; deflation has been the biggest worry for monetary policymakers for the most part of the last decade.

However, this does not necessarily signal a shift to a permanently higher level of inflation. First, current developments appear to be mostly driven by temporary factors. Energy prices especially have increased substantially in recent months and a sudden yet temporary release of pent-up demand from consumers in the upcoming months could further push prices higher due to capacity constraints.

Second, market and company expectations suggest that inflation will remain within the boundaries set by the ECB. The ECB survey of professional forecasters shows that they expect inflation in 2021 to be slightly lower than 2%, and expect similar levels to hold for the next two to five years.12 Also the corporate sector does not seem to be overly worried about inflation. The latest Deloitte European CFO Survey showed that only 16% CFOs expected inflation to exceed 2% in the next 12 months.13 So, while higher inflation for the rest of the year is likely, especially given strong consumer demand and rising prices of raw materials, the recovery alone will be unlikely to shift inflation upward permanently.

Nevertheless, structural factors might increase inflation pressures in the long run. Demographic changes will result in a substantial shrinking of the Eurozone’s workforce in the 2020s: The European Commission expects the workforce to shrink by 10 million people by the end of the decade and by almost 40 million by the end of 2050.14 Shortages in the labor market could result in a higher bargaining power of employees, higher wages, and, finally, a higher level of inflation.15 In that sense, inflation might become a risk in the long run, but for reasons unrelated to the current recovery and the COVID-19 crisis.

After a disappointing first quarter and a difficult second one, the Eurozone is moving toward a robust bounce-back. We expect a growth rate of 4% in 2021 in its baseline scenario, which would be the highest since the Eurozone’s inception. However, while an even stronger consumer boom, driven by accumulated savings, is a clear upside scenario, risk factors persist. The Delta variant of the coronavirus has spread in Europe, especially in the Netherlands and Spain, where some restrictions had to be reintroduced.16 If rising infection rates lead to a new round of lockdowns and new travel restrictions, the Eurozone’s growth prospects would fade substantially. Also, continued shortages of semiconductors and other inputs pose a risk. Despite these factors, the economic situation and the outlook for the Eurozone look better than at any time during the COVID-19 crisis.

{kind=link}

{kind=link}

{kind=link}