{kind=link}

{kind=link}

Facing the heat has been saved

The authors would like to thank Alexander Boersch, Kate McCarthy, and Derek Pankratz for their valuable comments on previous versions of the article.

Cover art: Tushar Barman

Germany

United States

United Kingdom

United States

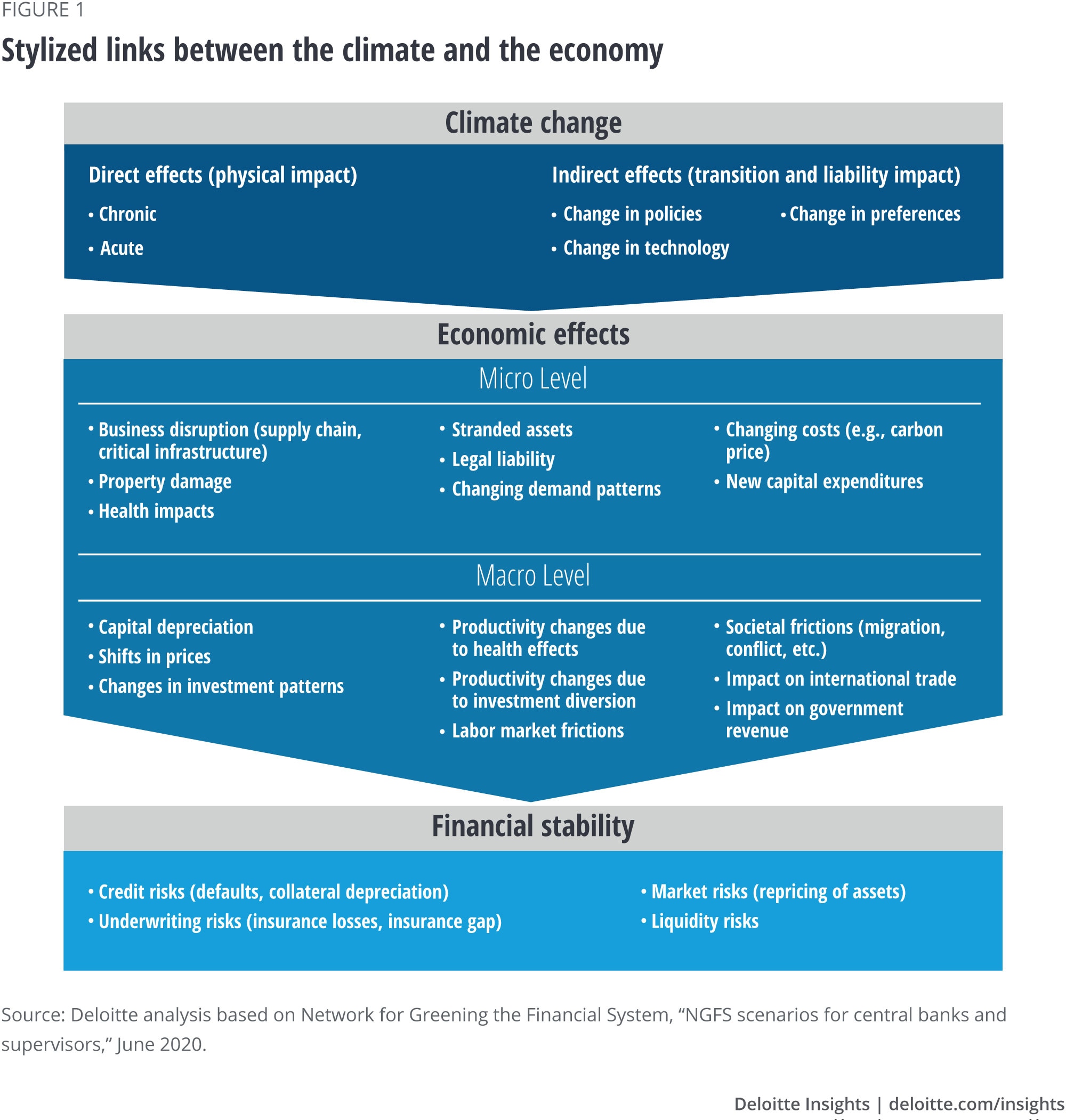

It’s no secret that forces of nature can have a strong impact on economies, COVID-19 being a case in point. The issue of climate change has risen in significance over the last few years and is likely to have far-reaching economic consequences in the years to come. Climate change affects the economy in more ways than one (figure 1), making it that much more important to approach this issue from different perspectives.

Understandably, there is a huge push from different quarters to move toward a low-carbon future. But what economic implications does this transition bring as part of the package? Read on.

That climate change wreaks havoc on the economy with physical damage is a given—in terms of both chronic (such as the gradual rise in temperature and sea levels or the shift in precipitations) and acute impacts (related to the frequency and severity of extreme weather events). For example, 2020 saw many natural hazards, from historic wildfires to a hyperactive hurricane season in the North Atlantic, producing losses of US$210 billion worldwide.1 This is part of a broader trend. Over recent decades, losses due to severe weather have risen significantly. This can be attributed to the increase in the number of natural disasters and growing concentration of human and physical assets in vulnerable areas.2

In addition to causing economic losses by damaging assets (e.g., destroying houses, businesses, and infrastructure), natural disasters can weaken the rate of economic growth. In particular, hydrometeoerological disasters reduce growth in both the short and long run.3 Furthermore, they can have broader consequences for international trade as damaged port and trade-related infrastructure may not be easily or quickly replaced, forcing exporters and importers to find alternative routes to move goods across borders.4

And, of course, changing weather patterns and weather extremes affect human health and lower productivity. Climate change is expected to cause approximately 250,000 additional deaths per year between 2030 and 2050, leading to estimated health costs worth US$2–4 billion per year by 2030.5 Studies have tied higher death rates to lower rates of economic growth across low-, medium-, and high-income countries.6 Apart from injuries and premature deaths, climate change also causes or exacerbates a host of diseases and illnesses,7 prompting authorities to divert additional money and resources toward health care. It also reduces people’s ability to work, thereby decreasing economic output. In particular, higher temperatures have been shown to reduce labor productivity (output per hour). In one US study, researchers estimated the effect of daily temperature on annual income over a 40-year period and found that productivity of individual days declined as temperatures rose.8 The impact of climate change and the related direct costs are unequally spread, with some places and communities being more exposed than others. Disadvantaged people and communities are often the worst hit, in developing as well as in developed countries. Nonetheless, the evidence so far indicates that the net damage costs are likely to be significant and may increase over time.9

With increasing carbon awareness, efforts to mitigate climate change have also intensified, staging a large-scale transition toward a low-carbon economy. The 2015 Paris Agreement to limit temperature increase has been ratified by 189 countries to date.10 Many of them—including China, Japan, and South Korea—are pledging carbon neutrality by 2050.11 Reaching these targets requires substantial changes in the economic structure. Although consumers and employees are pressurizing businesses to act on climate change,12 market forces alone cannot achieve the kind of transition necessary to limit global warming.

The reason? Economic actors, whether individuals or businesses, bear no direct costs from generating greenhouse gases (GHGs) and the social costs that impact other people. GHGs emissions are, therefore, “negative externalities” that businesses do not take into account when making decisions, thereby overemitting GHGs and underinvesting in the research and development (R&D) necessary for new low-carbon solutions.

Policy interventions of different kinds are necessary to address this issue. A wide range of policy tools is available. Among them, carbon pricing—that is, charging GHGs emitters a price equal to the value of the social costs incurred—is an important policy tool to channel market forces to tackle climate change. There are two main pricing mechanisms: a carbon tax on each ton of gases emitted, and an emissions trading system (ETS). The latter comprises setting a limit to the aggregate quantity of emissions allowed and distributing permits to companies based on this emission limit criterion, allowing companies to trade the permits on the secondary market if they are particularly efficient.

The number of carbon pricing schemes tripled over the past decade. To date, there are 64 carbon pricing schemes (taxes or ETS) at varying stages of implementation, covering almost a quarter of global GHGs emissions up from about 5% in 2010 (figure 2).13 After three years of preparation, China’s national ETS system will take effect this year, bringing the largest carbon market online. More initiatives are expected. Japan, for example, is working on a plan to create a national scheme.14 In the United States, the Biden administration is likely to consider carbon pricing to reduce GHGs.15 Prices are also likely to increase. In Canada, the federal government announced in December 2020 that the carbon tax will increase from CAD30 to CAD170 per metric ton by 2030—more than a fivefold increase over 10 years.16 In Europe, after languishing for a decade, ETS prices have surged recently, hitting all-time highs. Investors expect them to increase even more.17

These policies will likely increase production costs and could have significant negative effects on emission-intensive, trade-exposed producers. They are also likely to affect the profitability of these companies and employment. However, higher prices induce firms not only to become more energy-efficient, but also to be more innovative, as a recent study that analyzed the causal effect of carbon pricing on patent data application reveals.18 Furthermore, carbon pricing schemes can generate significant fiscal revenues that can be used not only to offset the negative effects of the transition (for example, in terms of reduced employment in carbon-intensive sectors), but also to actively foster innovation.

Apart from carbon pricing, R&D subsidies and public investments in green infrastructure (such as in public transportation networks or in infrastructure for carbon capture and storage) are also part of the policy tool that governments are increasingly willing to deploy. Green projects, for example, are at the heart of the European Commission’s proposed €1.85tn recovery plan. The returns to these investments appear to be attractive. An Oxford University study found that fiscal recovery packages that seek synergies between climate and economic goals are more likely to increase national wealth and enhance productive capital.19

All in all, the innovation required to decarbonize the economy and to increase resource efficiency can spark a new industrial revolution, fueling growth. A recent analysis of 14 countries (primarily in Europe and North America) reveals that environmental policies have a productivity-enhancing effect and foster capital accumulation, particularly in countries with a high level of information and communication technology (ICT) capital.20 The development of new clean technologies seems to have significant effects in terms of knowledge spillovers to the rest of the economy. In this respect, the “cleantech” sector could provide substantial scope for innovation-driven economic growth.21 Also, in terms of employment, the net effect of a large-scale transition is expected to be positive. The International Renewable Energy Agency (IRENA) expects job growth in the renewable energy sector to offset any decline in fossil fuel employment globally.22 However, the shift in employment could affect individual countries and regions unevenly, with mismatches in the location of job opportunities and available skills likely resulting in misalignments that would require a policy response to support those affected.

Both direct and indirect effects of climate change on the real economy influence the financial sector. Insurance companies are among the first ones to feel the direct impact of climate change. However, due to reduced labor productivity and lower stock and quality of capital, the direct consequences of climate change have implications also for equity markets, private equity, pension funds, and banks’ balance sheets. According to a recent study, climate change will increase the frequency of banking crises (from +26% up to 248%), while rescuing insolvent banks will cause an additional fiscal burden of approximately 5% to 15% of GDP per year and an increase of public debt to GDP by a factor of two by the end of the century.23

Also, the transition toward a low-carbon economy has financial implications—more so if a delay in action leads to a stronger and more sudden action to meet the climate goals (disorderly transition). As a result of the changes associated with the economic transition (such as lower demand than anticipated, higher prices, and regulatory prohibitions) existing assets might stop earning a return earlier than expected at the time of initial investment. They might even turn into liabilities. This is known as the risk of “stranded assets.”24 Financial assets worth US$2.5 trillion are estimated to be at risk of stranding25—enough to represent a systemic shock on stock markets. The financial repercussions can also have a cascading effect on the economy.

That’s why central banks around the world are increasingly thinking about the potential financial systemic risks from climate change. This is leading to more climate stress testing. It represents efforts to evaluate the risks involved that have not been understood well enough yet. It is essential to understand not just the direct financial implications, but also the interconnected nature of the financial risks.

For a successful low-carbon economy transition, financial markets and financial institutions have an important role to play, especially in mobilizing and channeling private investments. Capital appears to be shifting significantly toward green assets, a glimpse of which was seen during the pandemic. The largest renewable energy stocks rose in value in 2020 by 145% while the largest oil, gas, and coal equities fell by 30%.26 The cost of renewable energy technologies has fallen dramatically over the past decade, often making them cheaper than fossil fuels, making a strong investment case for renewables. The supply of capital for more environmentally friendly projects is also increasing. Environmental, social, and governance (ESG) strategies are popular with investors, and, within them, climate change is the dominant theme.27

Climate change is often dubbed as the defining issue of our time. This is not hyperbole. Amid climate change, the global economy is expected to change profoundly, and no country or industry is completely immune to the forces of change. For example, an analysis of the Australian economy by Deloitte’s Access Economics found that the industries hit hardest by COVID-19 “are also the most vulnerable to the effects of a warming world and climate change” and that “over 30% of employed Australians are exposed to economic disruption and risk from COVID-19, climate change, and unplanned economic transition as the world responds.”28

Only by understanding the far-reaching economic consequences of climate change for their specific industries and local economic conditions can companies prepare for possible future scenarios and build strategies to thrive.