Headaches from headwinds?

Cheerful as the forecasts seem, especially relative to 2020, consumer spending faces key headwinds. First, the labor market is not yet out of the woods with employment far short of prepandemic levels. There were 7.1 million fewer people working in the economy in May this year compared to February 2020. And labor force participation at 61.6% is close to two percentage points lower than prepandemic levels. Without these people coming back to the labor market and finding jobs, consumer spending growth may suffer over the medium to long term.

Second, low-income households will face challenges in ramping up spending given the pandemic’s disproportionate impact on them.11 As of May 2021, employment in low-wage occupations12 was still 5.4% lower than that in February 2020, worse than the declines in medium-wage occupations (4.2%) and high-wage (2%) ones.13 Low-income households are also less likely to have health insurance—especially after layoffs—and more likely to have health conditions that complicate recovery from infection.

Third, spending by retirees will come under pressure as retirement income falls due to low interest rates. Retirement savings, an indicator of future spending by retirees, has been hit due to the impact of the pandemic on labor markets and is unlikely to recover fast if the participation rate does not return to prepandemic levels soon. Even before the pandemic, fewer than four in 10 nonretired adults thought their retirement was on track, with one-quarter of nonretired adults saying they have no retirement savings.14 And the great majority of Americans’ balance sheets have not benefitted from the recent stock market boom.15

That the impact of the pandemic on people’s incomes and finances is deep and continuing is evident from latest trends in Deloitte’s consumer survey, which shows that the share of respondents attributing their anxiety to financial stress has been edging up since January. In fact, in the latest survey, 48% of respondents cited financial stress as the reason for greater anxiety in the survey week, higher than even the share of those who blamed COVID-19 (41%).

Some shifts in spending may stay for long

The post–COVID-19 world will have a lot in common with the one we lived in before the pandemic, but some things may change permanently.16 This will likely impact consumer spending patterns over the medium to long term.

- The future of work may well turn out to be a mix of in-person, remote, and hybrid work. Such a change will likely nudge consumers to head more to single-family homes in the suburbs than multi-family units within the city. A shift to larger homes with adequate space for home offices will translate to higher spending on home office furnishings and home utility services compared to prepandemic levels.

- Life in the suburbs may also lead to a rise in car ownership due to mobility requirements. Also, people—even those living within a city—may prefer to have their own set of wheels as they may feel safer traveling alone rather than share space with people outside their households. Most consumers are therefore unlikely to engage as much in ride-sharing and mass transit than they did in 2019.

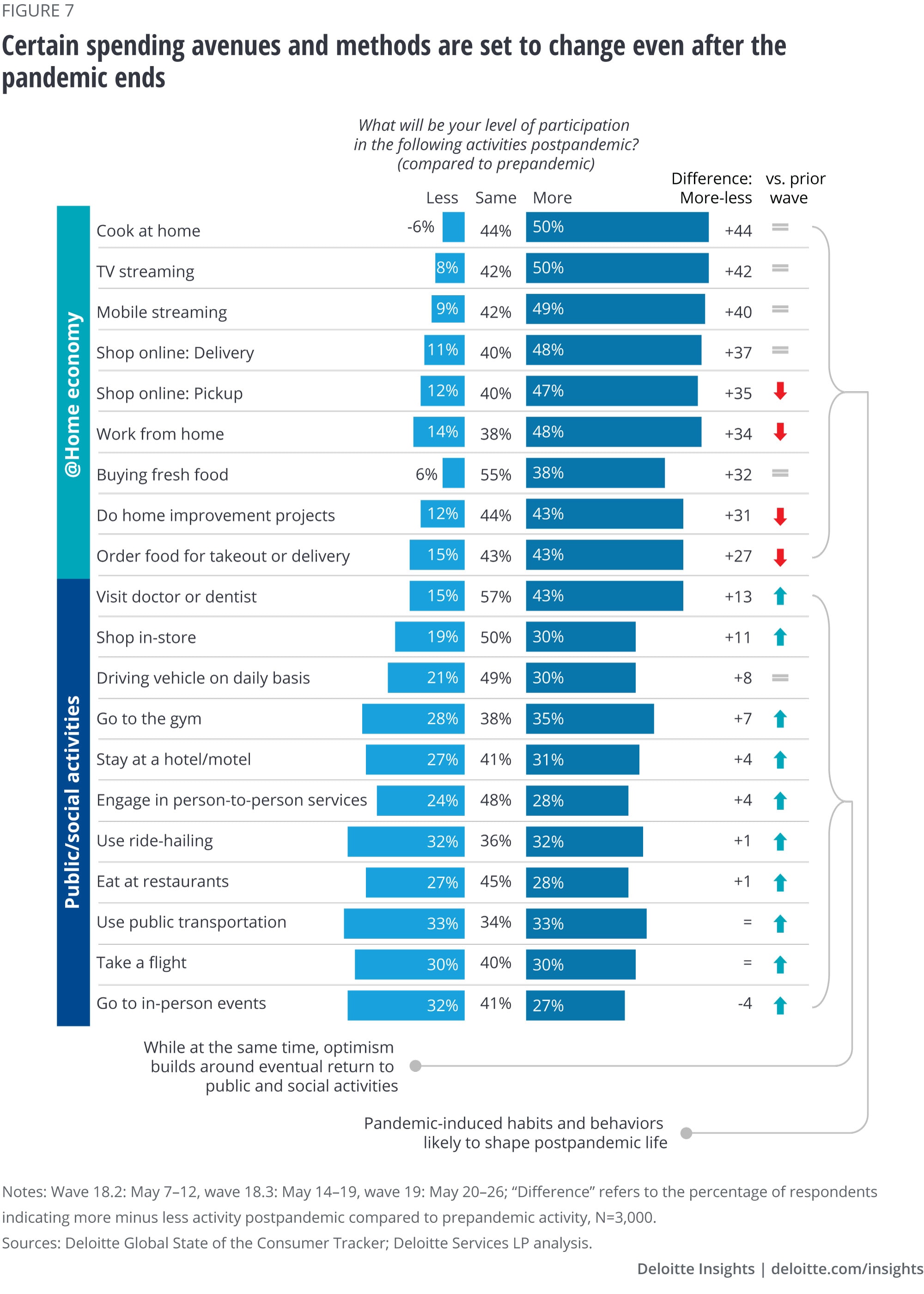

- A study of responses from Deloitte’s consumer surveys over May 7–26 reveals that even as the health-related uncertainty over the pandemic eased, respondents who are more likely to engage in remote work in future appear more intent to cook at home, engage in online shopping, and enjoy streaming services compared to prepandemic levels (figure 7). Figure 7 also reveals that people are keen to travel more and eat out as the health scenario improves further.

- If financial inequality—exacerbated by the pandemic—doesn’t go down over the next few years, the divergence in spending baskets between those at the top of the income and wealth ladders, and the ones at the bottom will only widen. Those at the bottom may find it even more difficult to spend on health care, insurance, retirement, and transport.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}