Eliminating bias, however, requires more than just equitable data. FSIs should focus on organizational diversity and understanding local context to reduce the risk of bias. They should proactively engage in bias detection to explain the causes and sources of biases. HSBC, for instance, has developed a governance framework that includes principles for the ethical use of AI.19 Other steps FSIs can use to deter bias include having senior management’s end-to-end involvement, regular audits, and, when needed, retraining algorithms.

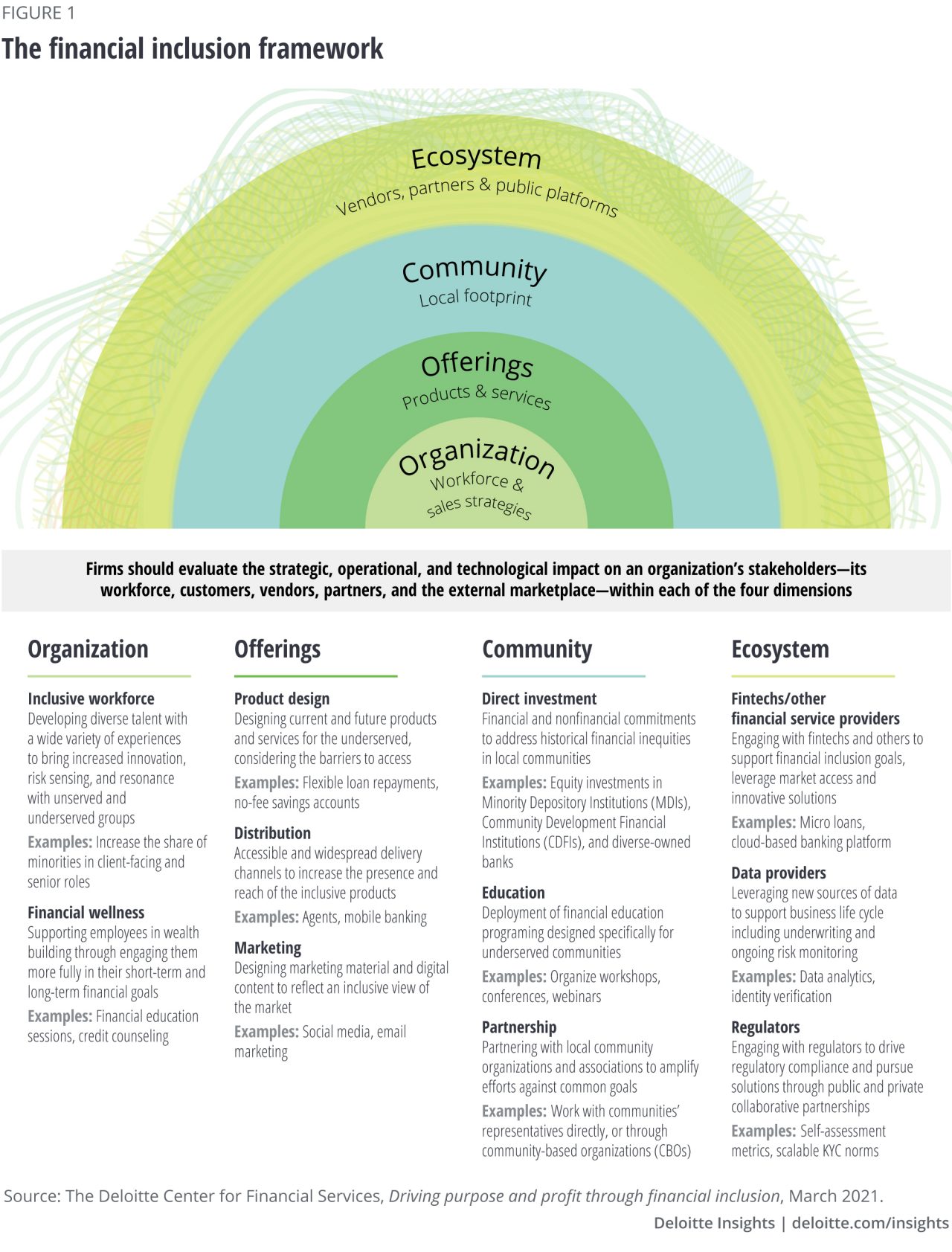

Community

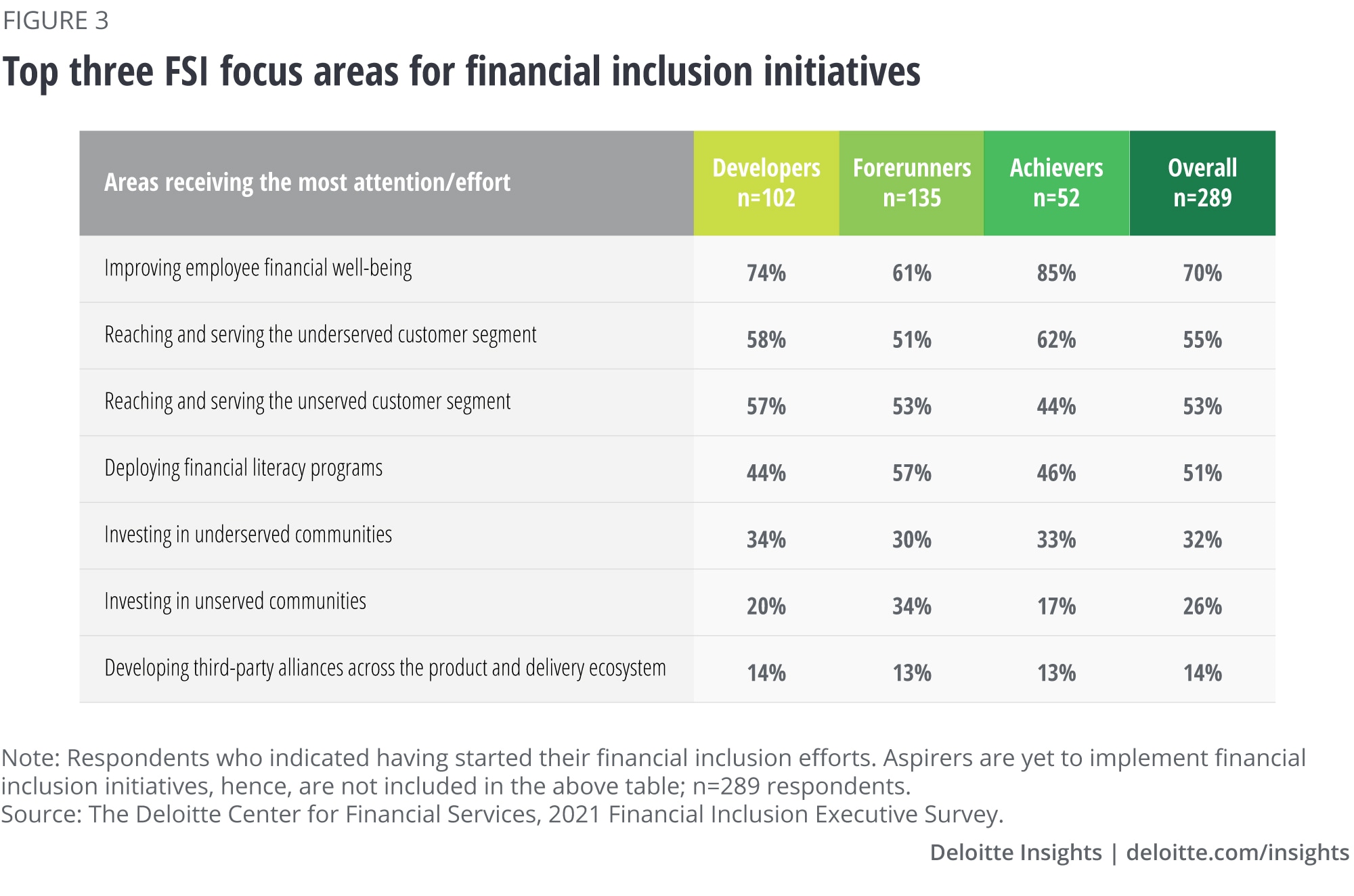

Most FSIs continue to partner with local organizations and offer financial literacy programs

When pursuing financial inclusion strategies, FSIs should demonstrate a commitment to the communities in which they operate, recruit, and invest. By having a visible and tangible brand presence, firms can enhance their relationship with local communities, build trust, and provide opportunities to work in concert with local businesses.

Almost 60% of survey respondents are partnering with local community organizations and associations to amplify their financial inclusion impact. FSIs, for instance, have invested billions of dollars20 in minority depository institutions (MDIs) or community development financial institutions (CDFIs) for the communities they serve. By supporting individuals and small businesses through lending, housing, neighborhood revitalization, supporting employee volunteerism, and financial education, FSIs continue to demonstrate a corporate purpose beyond profits.

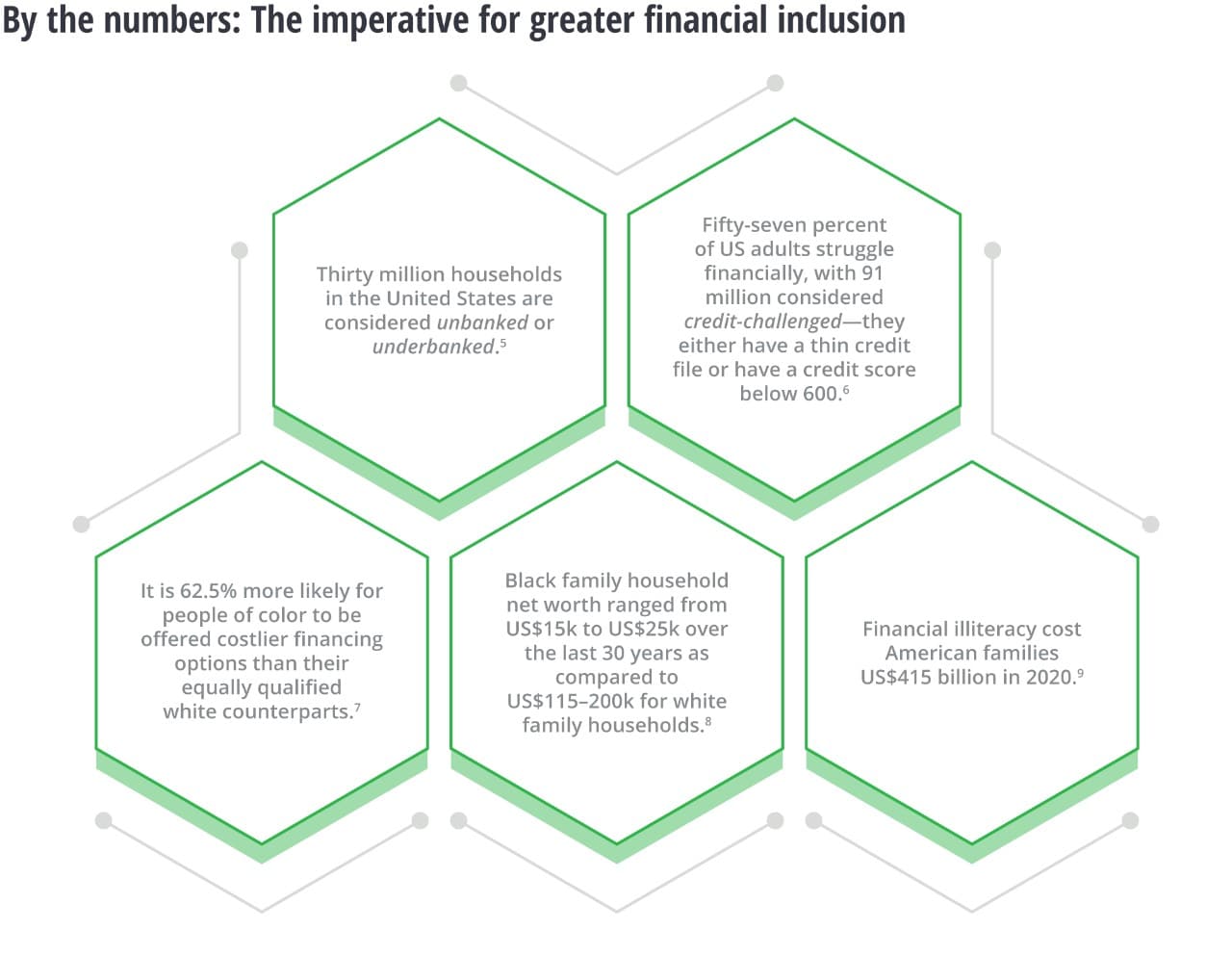

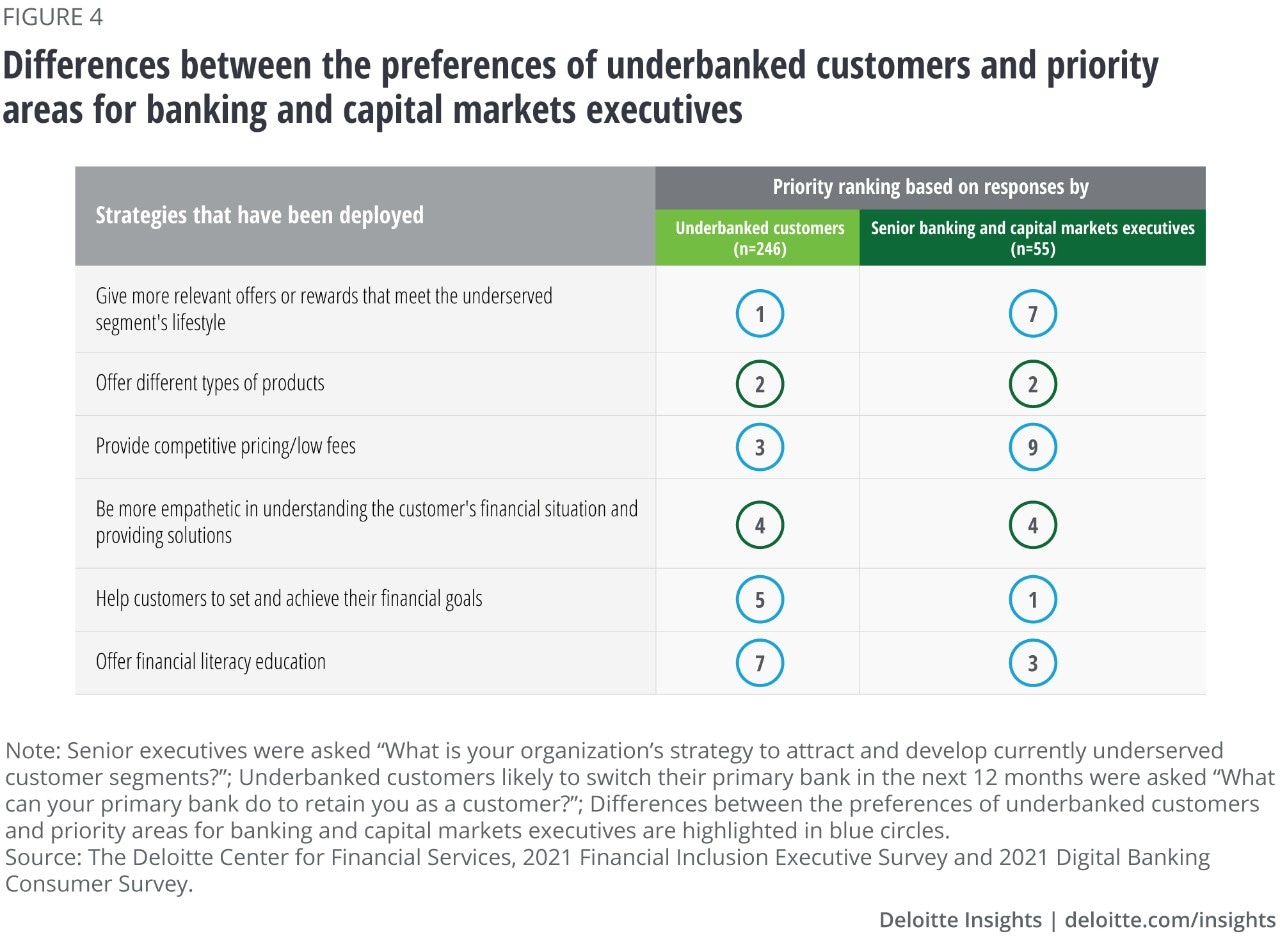

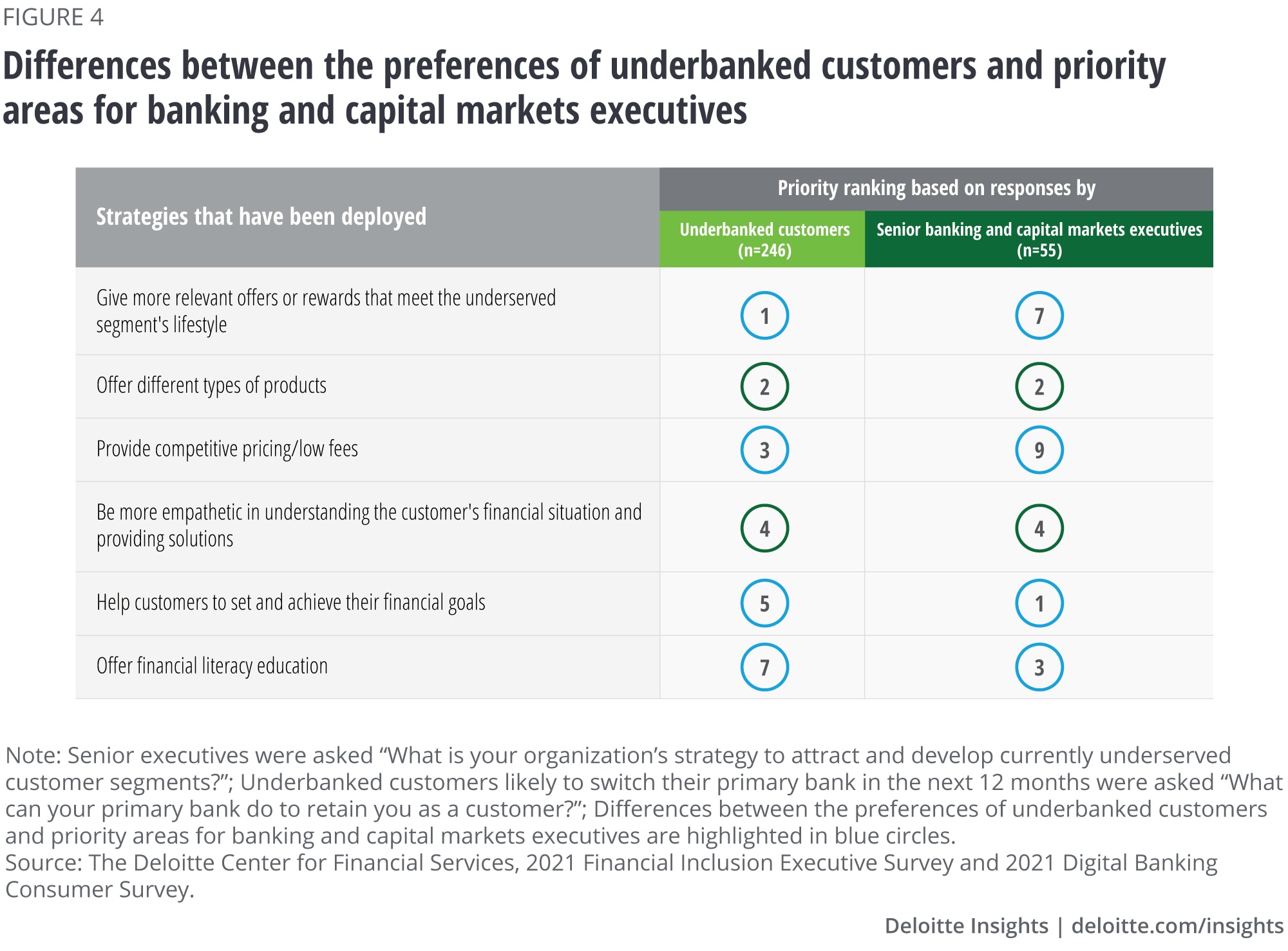

Investing in communities can also include promoting financial literacy among community members. The National Financial Educators Council estimates that financial illiteracy—lacking the skills and knowledge to make informed financial decisions—cost American families US$415 billion in 2020.21 FSIs can join forces across communities and industries to reach the unserved with much-needed financial education on topics such as effective money management, financial planning and protection, and savings and investment strategies. Fifty-seven percent of respondent FSIs already have established these programs. That said, as mentioned earlier and highlighted in figure 4, a recent Deloitte survey shows financial literacy programs ranked low among the preferences of underbanked customers. Therefore, FSIs may want to target more of their financial literacy efforts at unbanked customers specifically.

Leveraging established distribution channels to serve communities a likely priority over the next 6–12 months

To offer broader access to financial services, FSIs can invest in distribution channels where the unserved and underserved live and work. Forty-six percent of our survey respondents, half of whom are Forerunners, said they plan to enhance access to financial products and services by utilizing established, traditional, community-based distribution channels. Examples included using retail outlets or post office locations for banking customers and workplaces or auto dealers for insurance customers.22

These initiatives clearly indicate that FSIs do not have to tackle financial inclusion alone. By engaging with the communities they serve, FSIs can bridge the gap to unserved and underserved customers and promote financial inclusion programs.

Ecosystem

During the coming year, FSIs are mulling multiple ecosystem-related initiatives

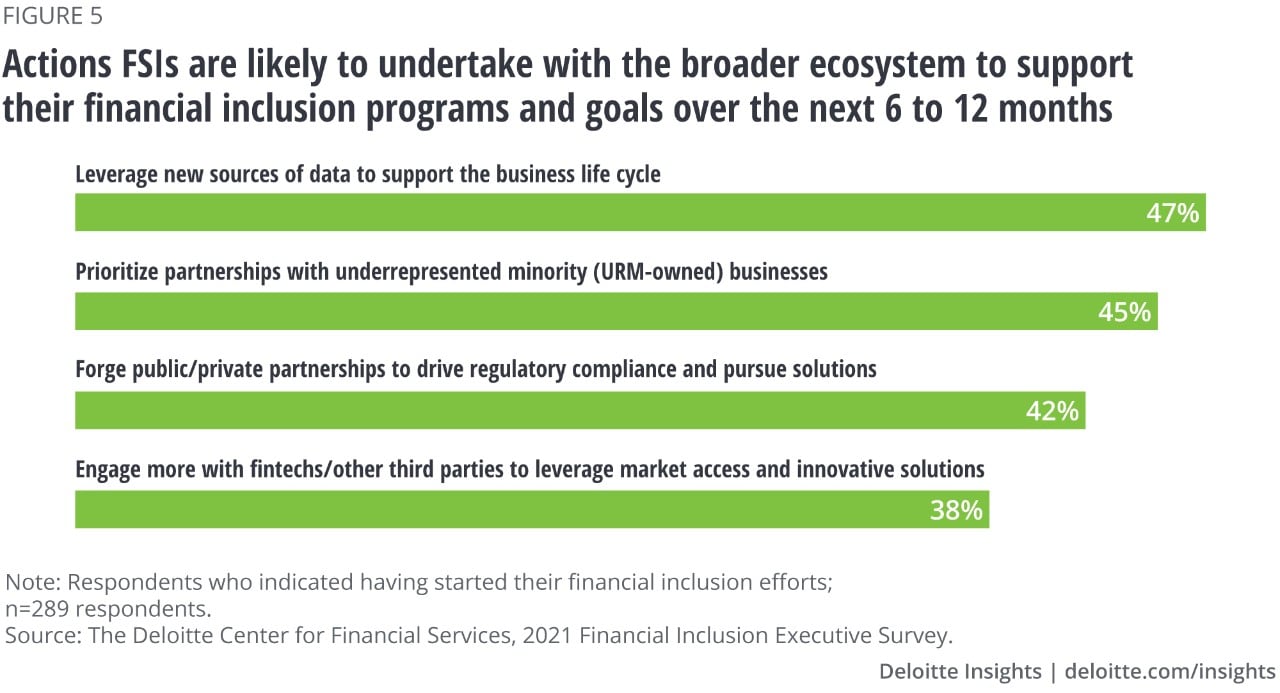

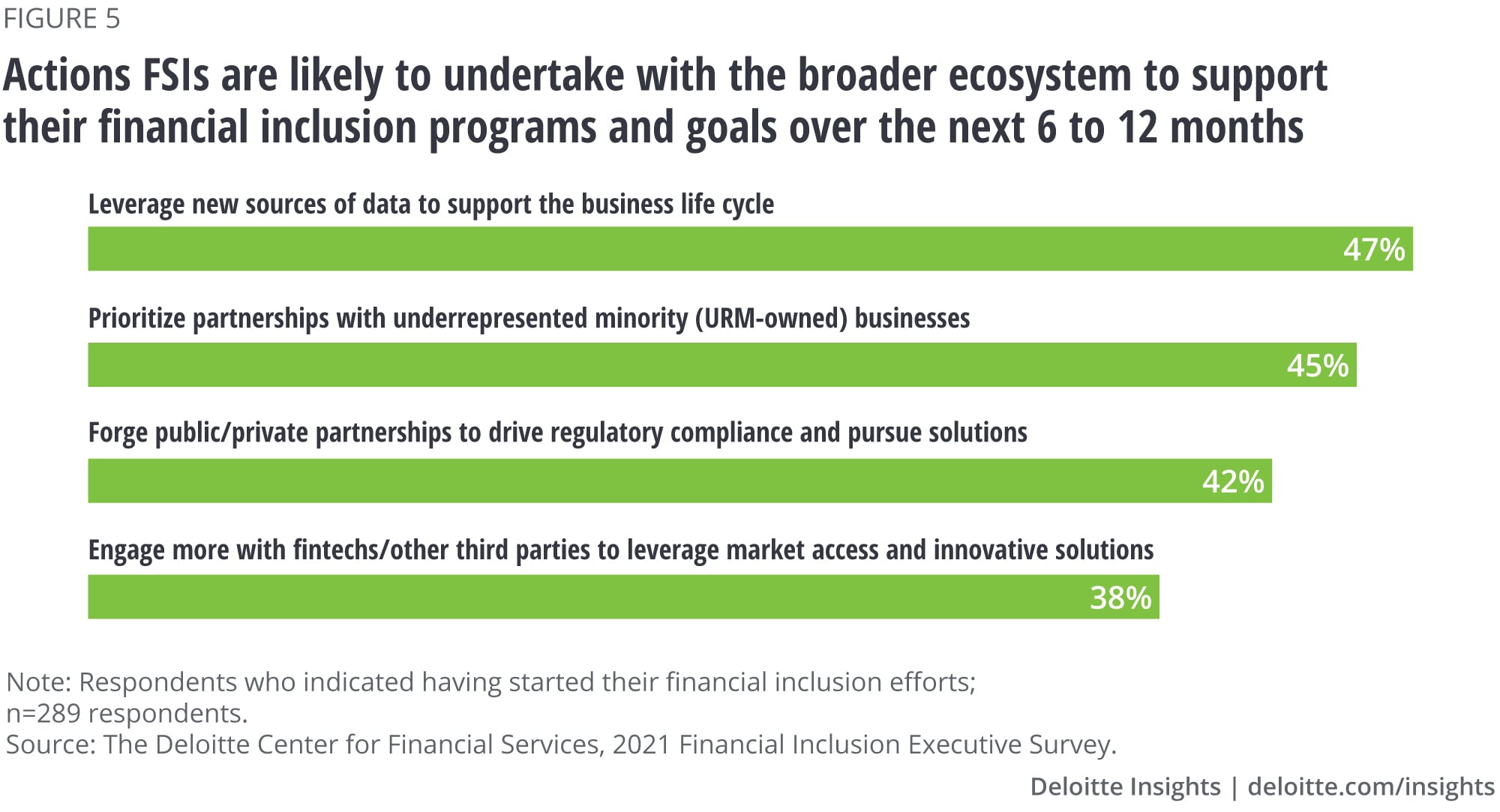

FSIs can establish partnerships within the broader ecosystem to bolster their financial inclusion agenda in many ways. A sizeable proportion of respondents, across all maturity levels, say that their institutions will likely explore multiple financial inclusion initiatives with fintechs, other financial services providers, data providers, and regulators (figure 5).

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}