2025 commercial real estate outlook

Turning the corner to capitalize on a generational opportunity

Jeffrey J. Smith

Kathy Feucht

Renea Burns

Tim Coy

Jim Eckenrode

Turning the corner

A message from our real estate sector leaders

Dear colleagues,

The commercial real estate (CRE) industry has faced a myriad of uncertainties in recent years, primarily brought on by elevated interest rates and high inflation, shifts in how—and where—tenants occupy commercial space, the impacts of climate change on buildings, and the emergence of technologies like generative AI. Organizations have likely been taking more defensive postures—fortifying their balance sheets, shoring up core capabilities, and focusing inward—rather than being on the offensive.

The good news is that there may be more clarity in the next 12 to 18 months, which should create an opportunity for a shift in that posture. This year’s commercial real estate outlook aims to help leaders turn the corner on the recent challenging years to better position their organizations for the road ahead.

In this year’s report, we explore what economic scenarios might need to play out for a CRE recovery; what investment opportunities might arise amid current bottom-cycle pricing dislocations; the growing financial imperative of investing in sustainable real estate strategies; what may be important to the next generation of real estate talent, and how their skills can adapt to changing business expectations; and if the industry is ready to implement artificial intelligence solutions for transformative change.

Our annual global real estate outlook survey again helps us gather what is top of mind for real estate owners and investors across North America, Europe, and Asia Pacific for the remainder of 2024 and into 2025. The survey findings are supported by insights gathered from Deloitte’s own subject matter specialists as well as research leaders at the Center for Financial Services.

We hope you find our insights and guidance useful and thought-provoking as you begin your strategic planning for 2025. We welcome any opportunity to discuss our findings with you and your organizations.

Sincerely,

Jeff Smith

US Real Estate leader

Partner, Deloitte & Touche LLP

Kathy Feucht

Global Real Estate leader

Partner, Deloitte & Touche LLP

Table of contents

- A message from our real estate sector leaders

- Can global economic growth and falling inflation bring stability to CRE?

- Where are CRE companies looking to deploy capital in 2025?

- Can property climate resilience coexist with financial viability?

- How can CRE be an attractive career destination for next-generation talent?

- Is the CRE industry ready for the AI revolution?

- Turning the corner on an uncertain past

Can global economic growth and falling inflation bring stability to CRE?

A rebound for commercial real estate could depend on where global interest rates go

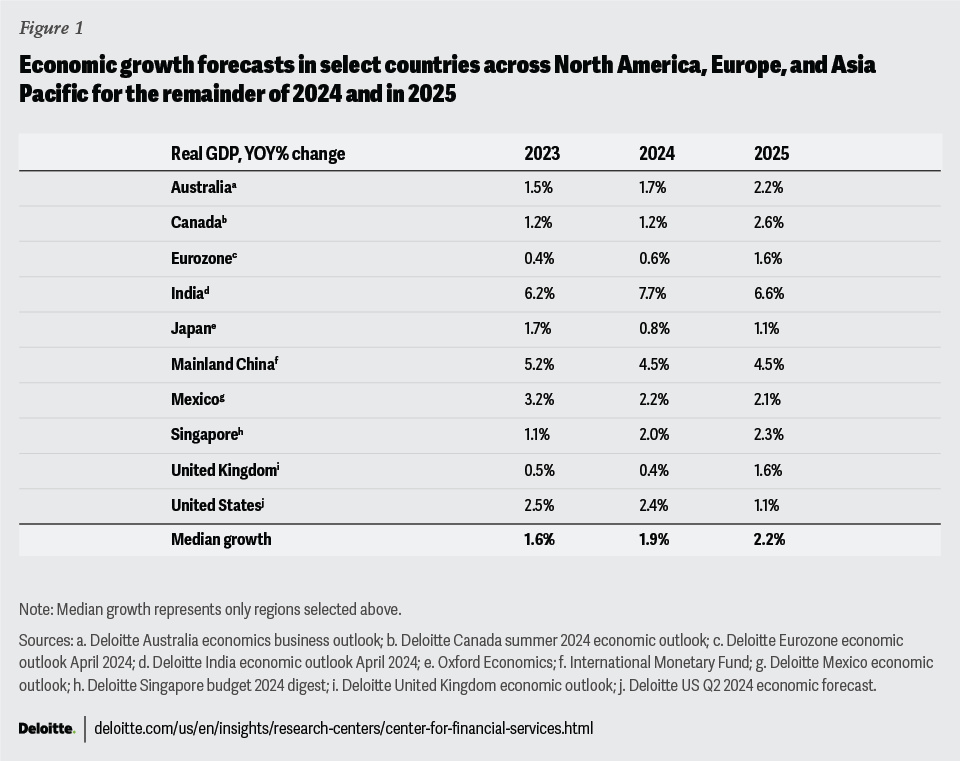

The global economic recovery has been uneven across geographies, and this will likely continue going forward. Deloitte’s economics team projects that gross domestic product (GDP) growth for the remainder of this year will be faster than 2023 in India and Singapore, but slower in Mexico and Japan (figure 1). Looking forward to 2025, the United States is expected to see GDP growth slow by 1.3 percentage points year over year,1 while the United Kingdom and the eurozone are expected to outperform, increasing by 1.2 and 1.0 percentage points, respectively (figure 1).2 India will see healthy growth, though at a slower pace than in 2024.3

While growth for 2025 will likely be slower than historical levels, attributed to high borrowing costs and geopolitical conflicts in Ukraine and the Middle East, the outlook comes with some optimism. Recession has been mostly avoided and the pace of inflation has decreased substantially across most major economies from 2023 highs.4 Central banks appear to be on the precipice of more significant loosening of monetary policy. The European Central Bank and the Bank of Canada cut rates in early June,5 followed by the Bank of England in early August,6 ahead of any such action by the US Federal Reserve, which left rates unchanged through their July meeting.7

For some in the commercial real estate industry, the shift to prospective rate cuts has boosted sentiment for the remainder of 2024 and 2025.8 That said, a single rate cut alone is not expected to immediately alleviate lingering concerns around refinancing risk for maturing loans or make capital and debt for acquisitions suddenly cheaper or easier to attain.

Real estate owners and investors hint at renewed optimism for 2025

Results from Deloitte’s 2025 commercial real estate outlook survey give some indication that commercial real estate owners and investors are hopeful that 2025 will emerge as a year of potential recovery over two years of muted revenues and pullbacks in spending. The survey collected input from more than 880 global chief executives and their direct reports at major real estate owner and investor organizations across 13 countries (see "Methodology").

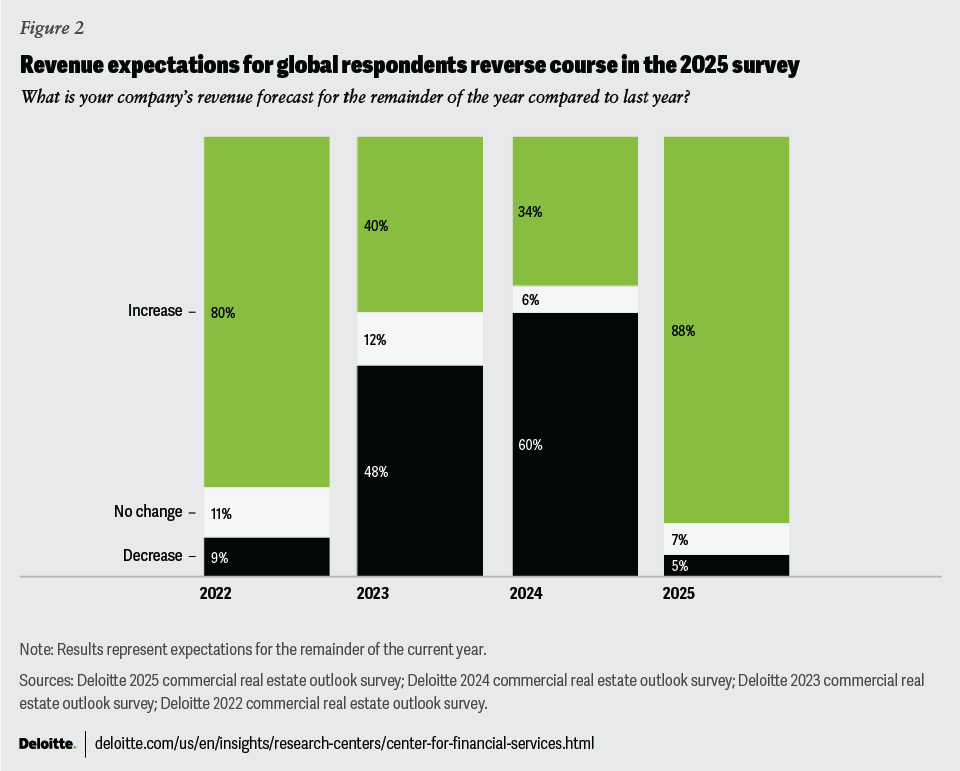

After two consecutive years where most survey respondents expected revenue declines, 88% of global respondents now report they expect their company’s revenues to increase going forward (figure 2), a substantial shift from the 60% who expected further declines last year. Moreover, 60% of respondents expect growth to be in excess of 5% year over year. While their companies may be coming off muted baseline financial performances across the real estate industry last year, the turn in revenue sentiment could indicate that global real estate executives expect better prospects ahead.

With renewed optimism come expectations for increased budgets. Nearly 40% of respondents in last year’s survey expected to reduce spending, but this year, only 7% reported further expense mitigation efforts, in line with levels from survey responses in the 2023 (6%) and 2022 (4%) commercial real estate outlooks. In a sign that the industry recognizes its limited technology capabilities, and perhaps encouraged by the emergence of generative artificial intelligence (gen AI), most respondents (81%) identified data and technology as the area where they are most likely to focus spending for the coming year.

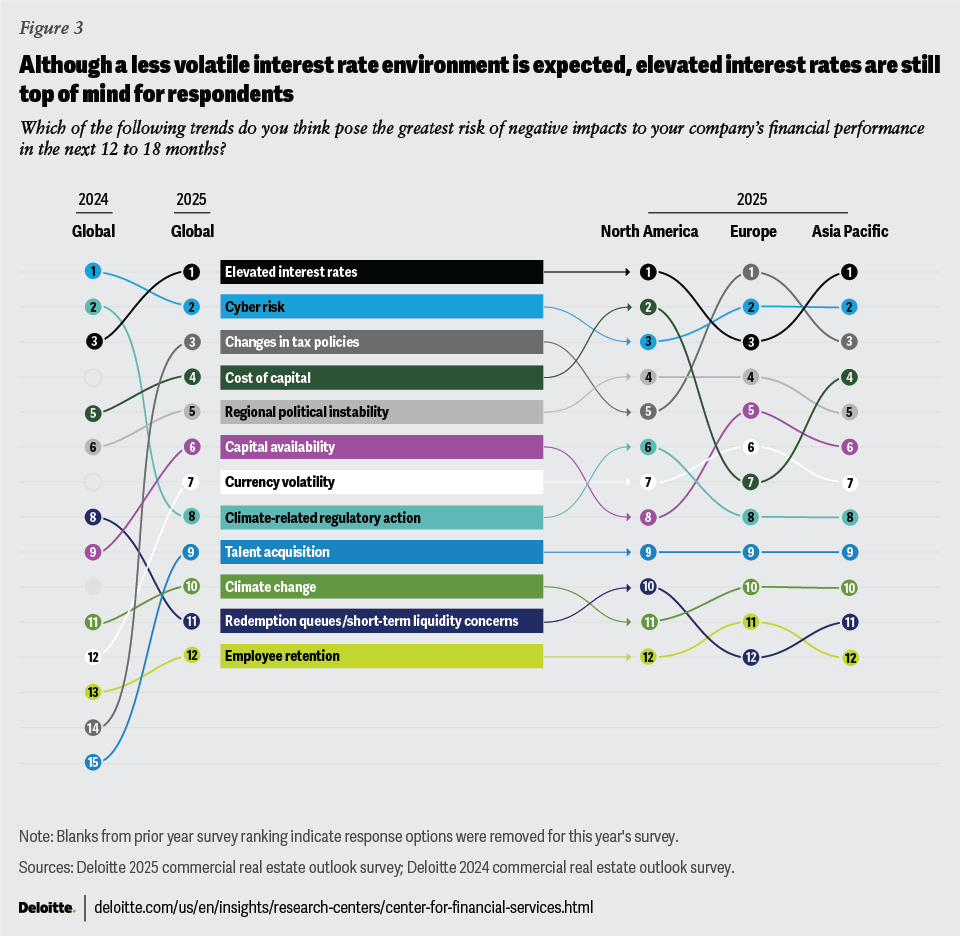

Renewed optimism is not without further caution, though. When asked about the macroeconomic trends that could most impact their financial performance for the next 12 to 18 months, respondents identified elevated interest rates, cyber risk, changes in tax policies, and cost of capital as the biggest factors (figure 3).

While elevated interest rates may be less about further rate increases this year compared to prior years, real estate organizations will likely face a rate environment that is higher for longer, particularly when compared to the record low-rate levels from the prior decade. Deloitte economists expect two rate cuts by the US Federal Reserve by the end of 2024, then another four cuts in 2025 with the federal funds rate settling at 4.5%,9 well above prior levels of sub-1.0% rates from before the pandemic. However, this would be far from record highs and more in line with conditions from the 1990s.10

Changes in tax policies surged to the third position, likely due to a combination of factors. The first being the enforcement of Pillar Two, the 15% global minimum tax, beginning around many global jurisdictions in 2024 and 2025.11 Another factor could be about 80 countries globally holding elections by the end of this year, the results of which may hold long-ranging implications for social and fiscal policy.12

With the expectation that rates will be higher for longer, respondents expressed concerns around elevated cost of capital, rising to fourth place this year. Of particular concern are the upcoming maturities for commercial mortgages—originally underwritten at lower interest rates—that will need to be refinanced. This impending wall of loan maturities has increased from earlier marketplace estimates as lenders offered extensions to troubled borrowers in hopes of a lower rate environment upon the new due date.13 Global regions are seeing this wall of maturities play out at different scales:

- Based on first quarter estimates, US$600 billion in loans in the United States will be maturing in 2024, with another US$214 billion from extensions that were originally slated for maturity in 2023.14 In addition, nearly US$500 billion is set to mature in 2025.15

- In Asia Pacific, there is about US$257 billion in outstanding senior debt set to mature, coupled with the emergence of a US$8.4 billion funding gap—the shortfall between the original secured debt amount originated and the amount available for refinance at loan maturity—between 2024 and 2026.16

- European markets are not expecting as high a concentration of loans maturing at once compared to other regions, with about US$165 billion due by the end of 2026.17

Actionable guidance to consider

- The impending wall of loan maturities is not insurmountable. For owners and investors facing a near-term loan maturity, alternative capital sources, like private credit, are available to fill the financing void left by traditional lenders. Bank lending will likely still be more subdued compared to prior levels as they manage exposure to the sector amid regulatory scrutiny.18 For organizations not as dependent on debt capital, or those with low leverage, there may be an extended window for acquisitions while others look to navigate funding accessibility challenges. That window may be closing as prospective rate decreases enable previously encumbered players to reenter the buyer pool.

- As CRE organizations become more open to technology spending again in 2025, investment should be methodical and incremental. Leaders should be intentional about digital transformation. Companies should avoid the allure of quick fix technology solutions placed on top of legacy systems and manual processes, as these could fail to deliver the expected return on investment. Poorly executed technology projects may not only result in immediate technology cost write-off, but could also limit future technology investment allocations and could create organizational ill will toward future efforts.

- Concern about elevated cyberthreats and real estate organizations’ abilities to respond to those threats suggest that technology investment should focus on enhancing core operations and processes, as well as on properties, to ensure organizationwide cybersecurity. The industry’s move toward smarter buildings—those with greater interconnectivity for monitoring and optimizing performance—also exposes asset-level vulnerabilities that should be monitored.

Where are CRE companies looking to deploy capital in 2025?

Capitalizing on a window of dislocation

Is 2024 the bottom of the current commercial real estate market cycle? If recent activity is anything to go by, that could be the case. Global property valuation declines continued through the second quarter of 2024, down 6.3% year over year, but the pace of decline is slowing from 7.7% two quarters prior.19 Global property transaction activity is still muted, down 31% year over year20 through June,21 though there is evidence that buyers and sellers are becoming more aligned on pricing estimates after two years of discontinuity.22 Moreover, the aforementioned expectations for inflation mitigation and interest rate reduction efforts around the globe could lend credence to the opinion that the next 12 to 18 months could be less tumultuous for real estate activity than the recent past.

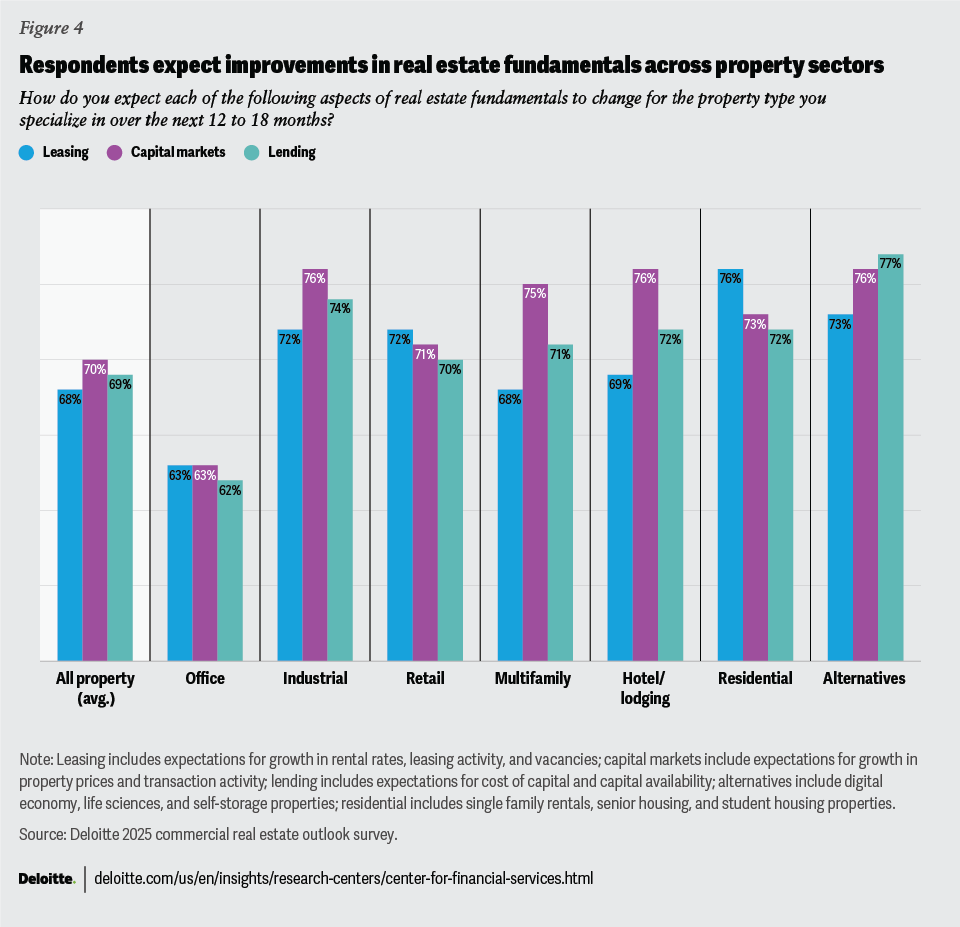

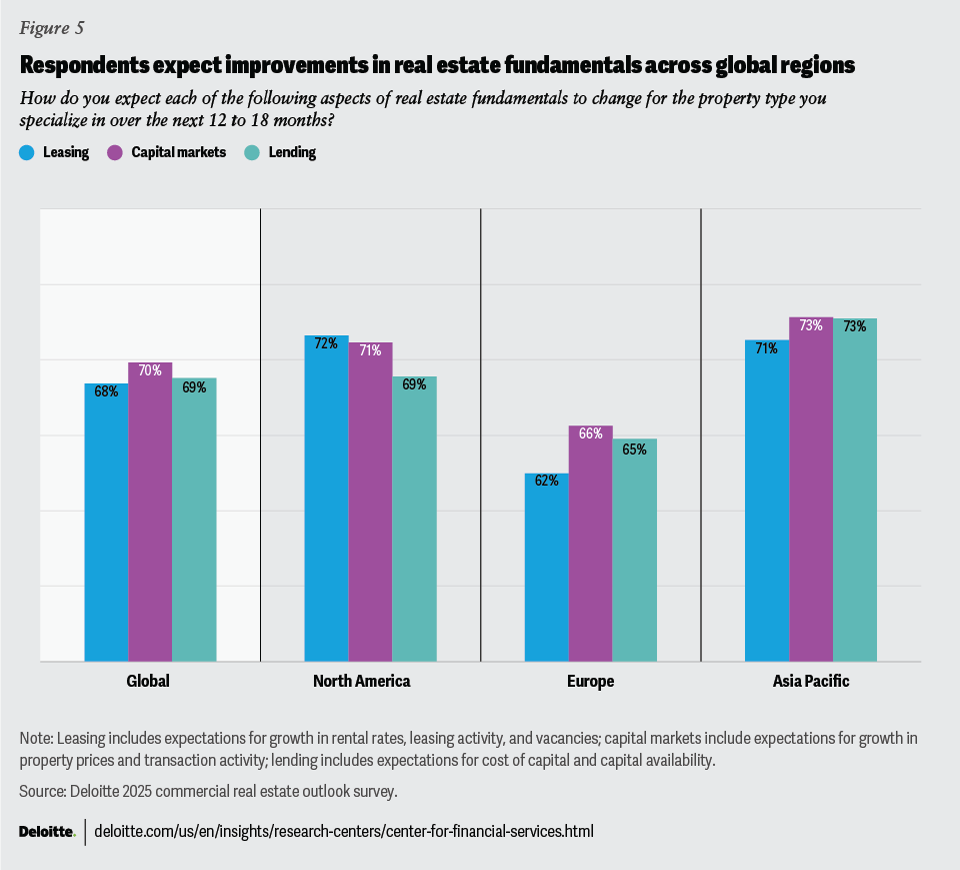

Responses to this year’s survey reflect a near-term shift in sentiment for commercial real estate in 2025 as well. Over 68% of respondents expect conditions for CRE fundamentals to improve in 2025 across areas such as cost of capital, capital availability, property prices, transaction activity, leasing activity, rental growth, and vacancies. This is a major boost in optimistic sentiment as only 27% of respondents in last year’s survey anticipated improved conditions. Conversely, only 13% expect fundamental conditions to worsen, down significantly from 44% last year.

The largest reversals came from expectations for cost of capital and capital availability. Nearly half of respondents in last year’s survey expected financing would be more expensive and 49% of respondents said that it would be more difficult to obtain for the remainder of 2023 and in 2024. That increased substantially this year—68% of respondents said financing will be less expensive and 69% said financing will be easier to obtain. Although these fundamental expectations vary widely by property type and regional focus, there appears to be some heterogeneity in how the broader CRE sector might recover. Global respondents appear most optimistic about leasing conditions for residential properties (including build-to-rent single-family, student housing, and senior housing); industrial, hotel/lodging, and alternative sectors capital markets (including digital economy, life sciences, and self-storage); as well as lending for alternative property types (figure 4). Respondents were the least optimistic about prospects for the office sector, tied to lower-than-average expectations for improving transaction activity, elevated vacancies, and more expensive borrowing costs.

Regionally, respondents from North America and Asia Pacific expressed greater optimism for improved leasing conditions compared to those in Europe. Asia-Pacific respondents are also optimistic about improved lending conditions (figure 5). Sentiment in Europe was more reserved than in other regions, though more expect improvements in capital markets conditions there compared to leasing or lending.

Rebalancing portfolios

High-growth property sectors

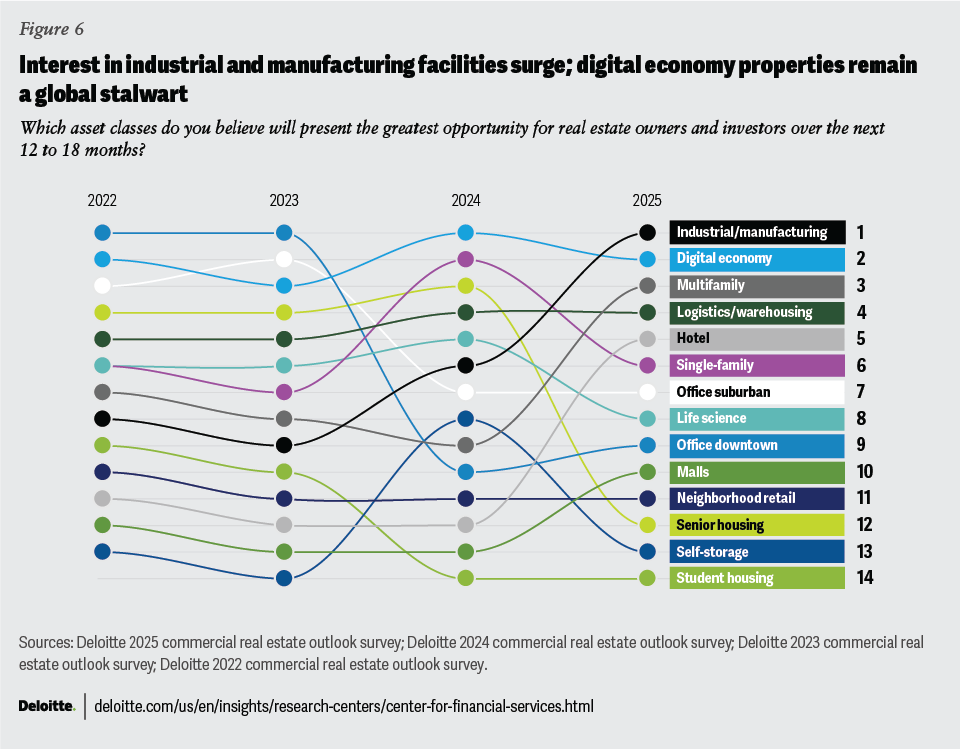

When asked about which asset classes might present the greatest opportunity for real estate owners and investors over the next 12 to 18 months, familiar responses resurfaced this year (figure 6). Last year’s top response–digital economy properties that include data centers and cell towers—ranked second this year. Logistics and warehousing facilities remained in the top five as well. Three sectors—industrial and manufacturing, multifamily, and hotel and lodging assets—came in at first, third, and fifth respectively, up from sixth, ninth, and twelfth last year (see “Select sector spotlight” for details).

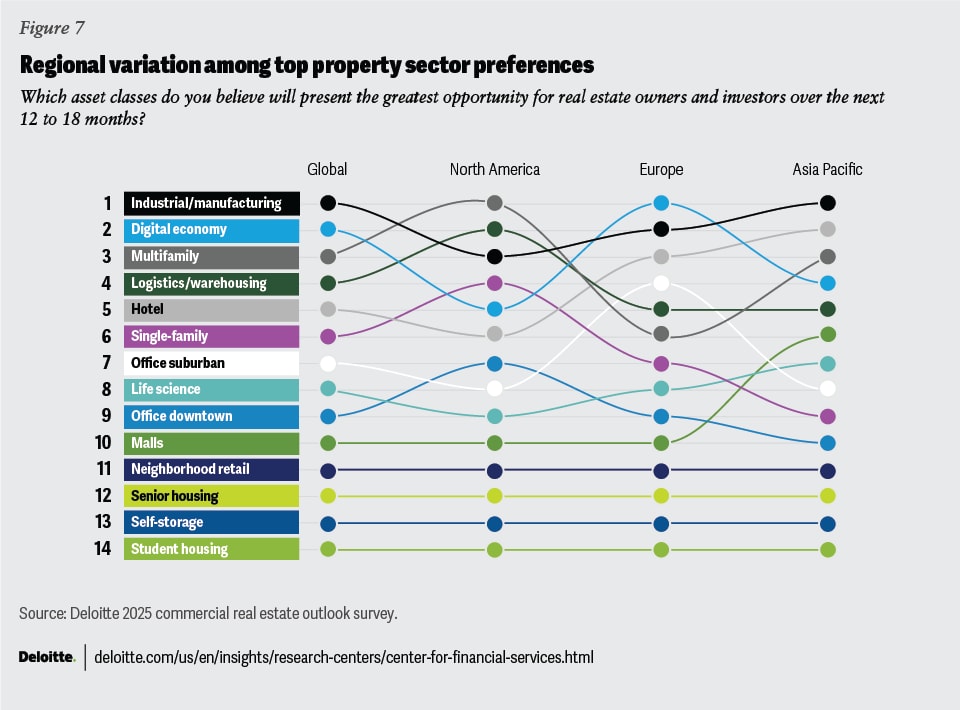

Regionally, respondents in Asia Pacific identified industrial and manufacturing properties as a top priority (figure 7). In North America, multifamily secured the top spot while interest in digital economy properties was driven primarily by respondents in Europe.

Select sector spotlight

Respondents’ emphasis on industrial properties was likely driven by continued global demand for manufacturing space, where two factors are likely at play. First, following several years of COVID-19–related disruptions, companies are pushing for greater supply chain resilience by bringing their manufacturing facilities closer to home for shorter, more flexible shipping. Since the passage of the United States-Mexico-Canada Agreement in 2020, reshoring in North America increased,23 with the low cost and high availability of labor drawing many companies to Mexico in particular.24 Companies that have made recent announcements for investment into the region include Walmart and Volkswagen.25 Mexico surpassed China as the largest exporter to the United States in 2023.26

Second is the outperformance of semiconductor manufacturers. While many factors come into play for decisions around leasing, semiconductor tenants have increased their leasing activity by 33% since August 2022 when the CHIPS and Science Act was passed in the United States, a policy that aims to spur domestic semiconductor production.27 Other properties surrounding these manufacturing facilities have similarly benefitted, increasing rents by 48% in some markets.28 Globally, available land for new development is constrained, which could lead to retrofitting opportunities for older existing buildings rather than through new development alone.

Demand for digital economy properties, in particular data centers, has proliferated globally with the growth in adoption of artificial intelligence (AI).29 But with increased storage demand also comes a concern—the environmental impact of energy-intensive facilities. Estimates suggest that electricity used by data centers, brought on by requirements for AI, will more than double by 2026,30 and could consume over 250 billion gallons of water per year by 2030.31 As the demand for AI solutions fuels interest in specialized data centers, owners and investors in this sector should consider the sustainability impact along with prospective regulatory intervention to curb excessive energy usage. Some are already tackling data center energy efficiency head-on:

- Real estate investment trust (REIT) Equinix, which operates over 250 data centers globally, installed fuel cells for cleaner electricity consumption, and has committed to renewable energy production through power purchase agreements.32

- Spanish real estate company Merlin Properties recently began operations at three completely waterless, carbon-neutral data centers located in the Port of Barcelona, Bilbao-Arasur, and Madrid Getafe. An additional data center is under construction in Lisbon.33

Offices have garnered many of the industry’s headlines over the past year for some of the most drastic asset valuation declines, waning vacancies amid adjustments to pandemic-era hybrid work arrangements, and loan distress. Findings from the Deloitte’s April Economics Insider indicate that the office sector is still rebalancing in the wake of the pandemic, and there will likely be more consolidation to come for lower-quality products should valuation declines continue in the near term.34 There is still a high degree of heterogeneity in how individual office properties perform across geographies.35 Our survey respondents only narrowly changed their opinion of the sector for 2025. Suburban offices came in at seventh place, no change from last year, and downtown offices followed in at ninth, down one place year over year. Both segments saw more dramatic de-prioritization in the 2024 commercial real estate outlook survey, falling from third and first positions, respectively, in the 2023 survey.

Into new locations

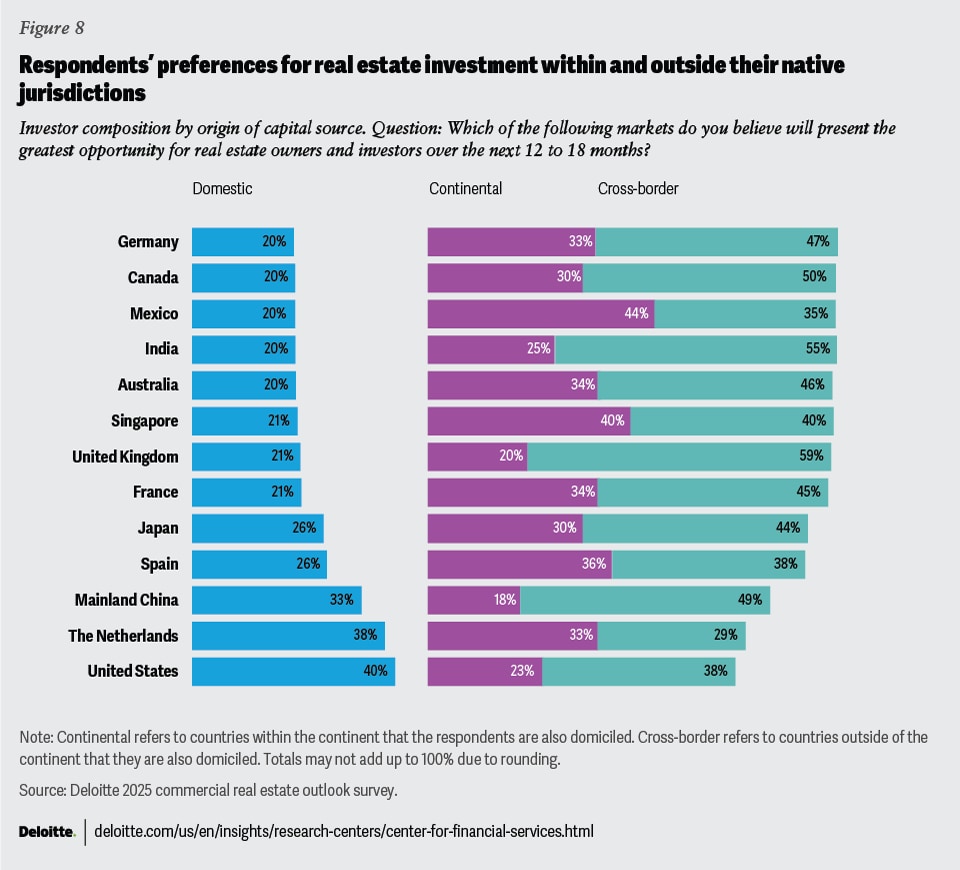

Investors in global real estate seemingly hit a pause last year. Dollar volumes fell by 36% year over year to US$1.2 trillion, making it the weakest year for global investment since 2012.36 Pullbacks were led by slowing deal flow in the Americas (–52%) and Europe (–45%).37 Despite also posting nearly 20% annual dollar volume declines, Asia Pacific had the largest concentration of global investment at 57% of all volumes, the largest share of global activity for the region in over a decade.38

CRE investors have been more focused on domestic assets rather than international opportunities since the pandemic. In 2019, an all-time high of 32% of all global investment was made outside company home countries.39 That share has progressively dipped since 2020 and settled at 23% in 2023.40 And while survey respondents still overwhelmingly chose home jurisdictions as top regions of focus through 2025, there are some indications that prospects for international investment could again be emerging. When asked about the top geographies for investment outside their native jurisdictions, Germany, Canada, Mexico, India, and Australia emerged as top choices (figure 8). Should transaction activity return in 2025, these areas may be where international investors look first.

Mergers and acquisitions

Deloitte’s latest commercial real estate M&A outlook predicted that 2024 could be the turning point for global mergers and acquisition activity. According to Deloitte mergers and acquisitions research services data, dollar volumes globally declined 62% to only US$158 billion in 2023.41 But M&A activity through May 2024 has rebounded from the same period last year, led by Europe (+56%) and closely followed by North America (+50%) and Asia Pacific (+46%).42

Survey respondents seem hopeful that this trajectory could continue. Most of them (68%) indicated that they are likely to increase their M&A activity in the next 12 to 18 months, up from 53% who expected the same for 2024 and only 40% for 2023. Primary goals for M&A activity appear to be largely targeted toward improving existing organizational capabilities rather than expanding the scope of their property portfolios. When asked what the top M&A ambitions were for those expecting to increase their activity for the coming 12 to 18 months, most chose adding new technology capabilities, increasing scale, and acquiring new talent.

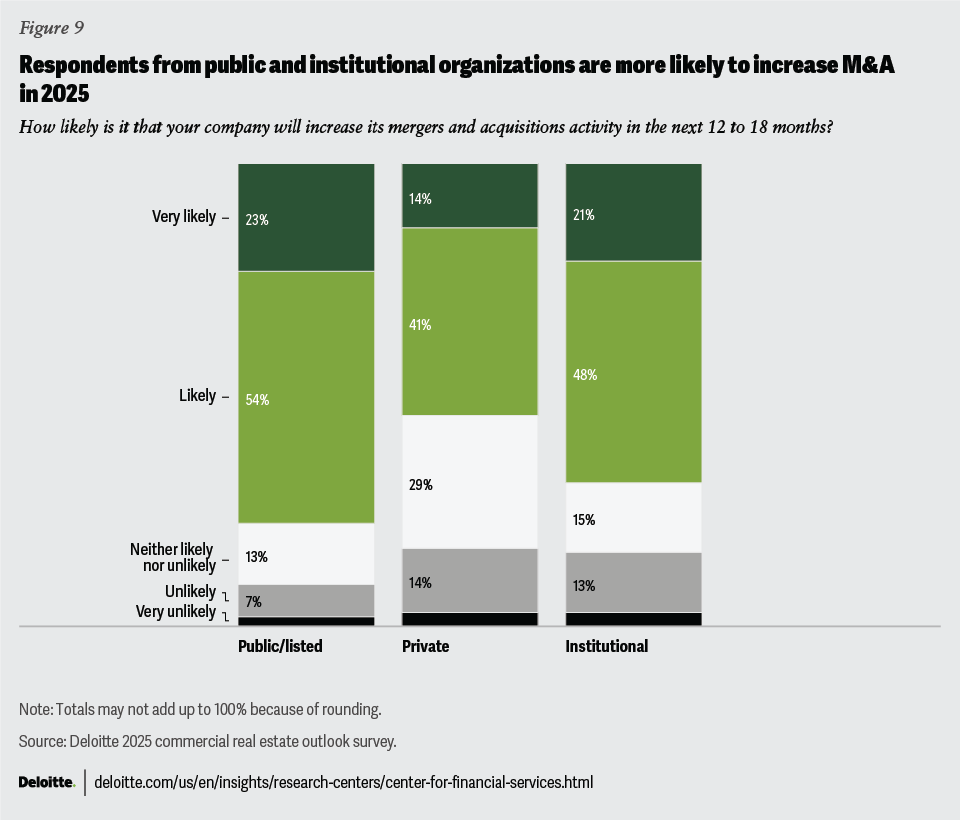

Of the types of owners and investors surveyed, respondents at public43 and institutional44 organizations indicated that they are likely to conduct more M&A in the coming year, while respondents at private45 owners and investors were more noncommittal (figure 9). Among respondents at REITs, 80% indicated that their organizations are likely to increase activity. Conversely, 23% of bank respondents were the most likely to decrease activity, closely followed by 21% of leaders at non-REIT private owners.

Actionable guidance to consider

- Do not just “buy the dip.” Aim for next-generation facilities that can be smarter and greener or for businesses in high-growth sectors.

- Have a long-term growth horizon. Even for property sectors that have become more embattled of late, owners and investors who have held those assets for longer time frames have likely accumulated enough valuation growth to have been insulated from the latest declines. For instance, on average across the 20 largest metropolitan areas in the United States, an office property purchased five years ago (the first quarter of 2019) is still valued 15% higher today than it was at the time of acquisition.46

- Consider markets with a healthy balance of supply and demand that can offer fewer volatile swings in fundamentals. In geographies where there is limited new development opportunity due to restricted land access or high costs for ground-up construction, consider value-add or opportunistic properties in well-located areas and redevelop them into more modern facilities. Don’t rely on assets, property sectors, or locations that might require a V-shaped recovery.

- Prepare for active asset management. Commercial real estate may have pockets of financial engineering opportunities, but those who are able to actively add value to a commercial asset during the hold period could position themselves for outsized returns over those who simply buy, hold, and sell.

Can property climate resilience coexist with financial viability?

As the planet heats up, extreme weather conditions such as devastating storms, prolonged heatwaves, and rolling wildfires have affected buildings across the globe.47 These escalating conditions turn the spotlight on a vital question: How can real estate companies best position their properties to mitigate the impacts of climate change and reduce the negative impact of their operations on the environment while meeting financial imperatives?

Prioritize deep energy retrofits

Retrofitting an existing building produces less than half of the carbon emissions of redeveloping it outright.48 Building Performance Standards (BPS), which prioritize retrofits and performance thresholds on specific schedules for existing buildings, are gaining broader acceptance in certain geographies like the European Union49 and the United States.50

Deep energy retrofits, which aim to enhance a building’s energy efficiency by at least 50%,51 are currently implemented in less than 1% of buildings worldwide each year, primarily due to steep initial expenses and operational interruptions.52 Increasing the current renovation rate of the global stock from the current 1% to 3% and scaling the depth of renovation may bring net-zero goals into the realm of possibility by 2050, the target year set by many geographies.53 Seventy-six percent of our global survey respondents plan to undertake deep energy retrofits over the next 12 to 18 months.

Both BPS and building energy codes are increasing in stringency across countries.54 Six states and 41 cities in the United States have committed to implement BPS by the end of 2024 with 13 already passing legislation.55 In the United Kingdom, all commercial real estate assets will need Minimum Energy Efficiency Standards of at least Grade B from 2030 onward. Otherwise, owners could face restrictions in offering new leases to prospective tenants.56 It is estimated that nearly two-thirds of office buildings in the United Kingdom are rated lower than the required B grade, presenting an opportunity for deep energy retrofits to help mitigate the risk of stranded assets.57 Investor and regional regulatory pressure may be driving action across regions, as 80% of survey respondents in Asia Pacific expect to take up deep energy retrofits in the next 12 to 18 months, closely followed by respondents in Europe (78%) and North America (70%).

Sustainability evolves from being a compliance-driven, reputational imperative to having a financial impact

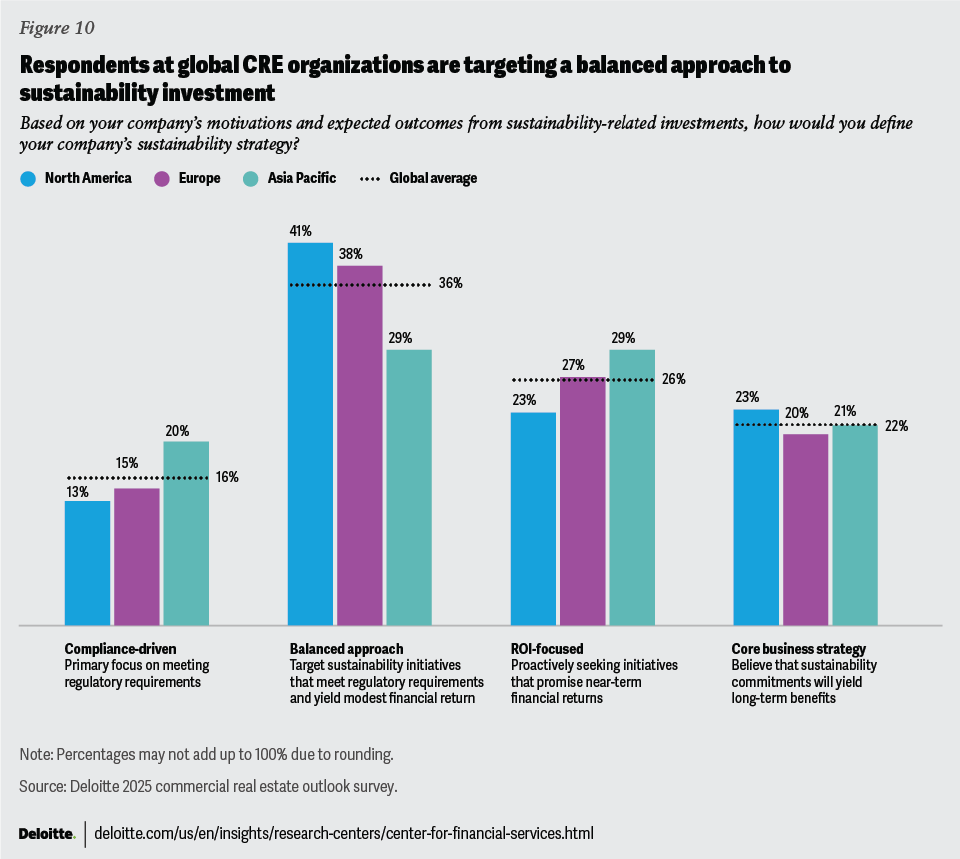

Even though the business case for sustainability strategies is gaining ground, there remains a balancing act as firms try to evaluate short-term financial returns and long-term benefits. Thirty-six percent of our survey respondents mentioned that they currently have a more balanced approach to sustainability investment, targeting initiatives that yield modest financial returns while also meeting regulatory requirements (figure 10). Only 16% are doing so for compliance alone. Leading from the front, another 22% of our global respondents believe that sustainability is embedded in their organizational DNA and core business strategies and believe it will provide long-term benefits.

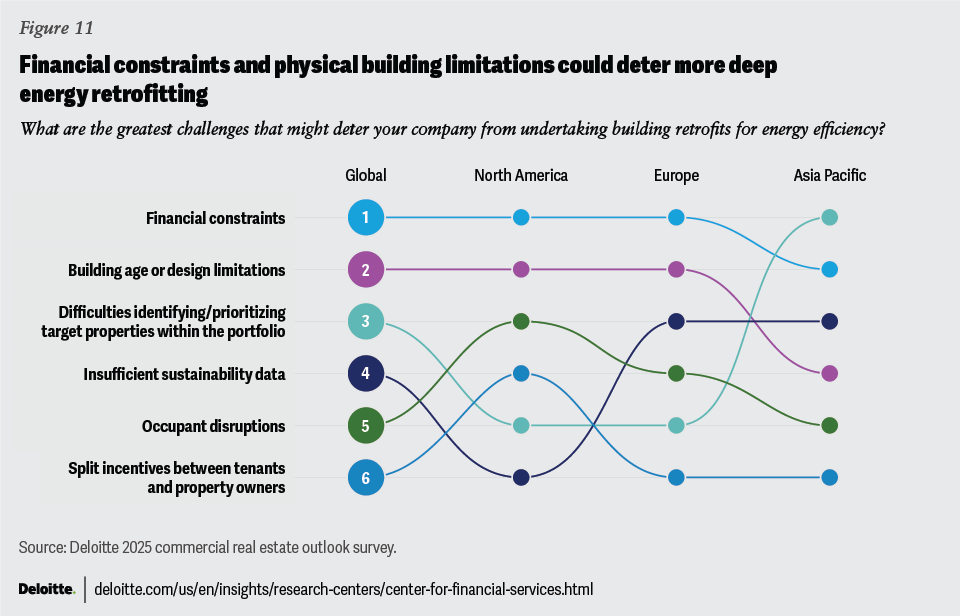

Retrofitting existing buildings may require investments of US$3 trillion globally,58 even though costs to do so may become prohibitive without access to innovative financing. Green bond issuance by US REITs dipped in 2023 with gross proceeds totaling US$1.6 billion—a six-year low—challenged by a higher interest rate environment.59 Survey respondents identified financial constraints, building age, and design limitations as the greatest challenges to conducting more deep energy retrofits (figure 11), but regional variations exist: European and North American respondents identified financial constraints and building age as key concerns whereas respondents from Asia Pacific highlighted asset prioritization difficulties.

Understanding the greening opportunity for value creation

The success of these initiatives may hinge on how capital investments are prioritized for maximum impact and how quickly firms can transition from “brown to green.” Some investors may be wary of carbon-intensive brown assets, those that are decades old and are heavily reliant on gas boilers or fossil fuels. However, greening such assets could hold immense potential to meet both investment returns and climate objectives. Some real estate investors may be in a rush to off-load carbon-intensive assets to avoid significant price drops. However, adding value to an asset and then drawing attractive exit valuations may be worth pursuing. Sixty-one percent of global respondents expect hurdle rates to further improve over the next 12 to 18 months. Almost half of those also identified investing in climate-related risk management measurement capabilities and digital twin technologies to model and simulate resource usage as their top actions to ensure climate resilience over the next 12 to 18 months. If property managers can mitigate asset obsolescence through strategic sustainability road maps while demonstrating incremental cost reduction and resource management, then a positive environmental impact without compromising long-term financial returns may be achievable.

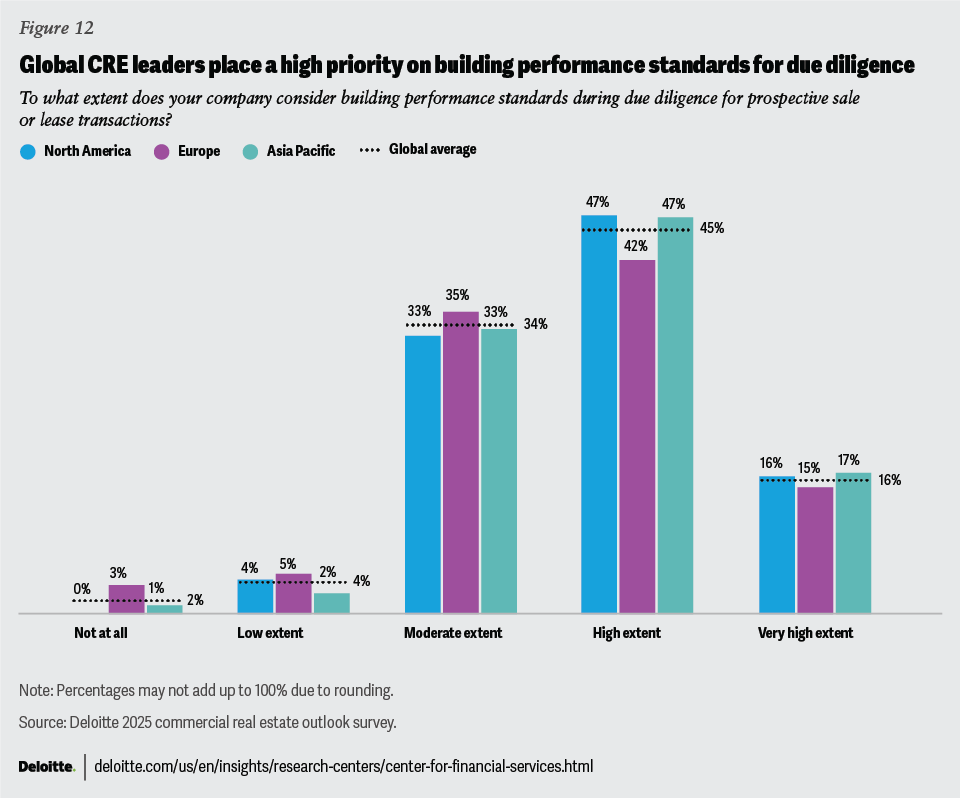

Metrics, approaches, and other due diligence criteria are still evolving, and some investors are still struggling to add sustainability to their due diligence “lexicon” amid a fractured regulatory landscape and inconsistent reporting.60 Over 61% of our global respondents mentioned that they place high to extremely high priority on BPS during the due diligence stage of sale and lease transactions, with another 34% mentioning it as a moderate priority (figure 12). Environmental and social impact investment considerations are growing in prominence.61 That said, existing key performance indicators and return metrics in cash flow modeling may still fall short of fully capturing future climate risks including carbon pricing, soaring insurance costs, penalties, elevated vacancies, risk of stranded assets, and the increased cost of capital. If transition risks are not properly accounted for, a potential carbon bubble could emerge, risking a flood of stranded assets.

Navigating the path to achieving net zero demands not only enhanced technology and data collection tools but also an understanding of the associated risks and opportunities. When asked about priorities for the next 12 to 18 months to bolster climate resilience in their portfolios, 45% of respondents emphasized the need to enhance their risk management capabilities. Data collection may be one of the biggest challenges confronting real estate stakeholders with looming penalties for inconsistent carbon measurements.62 Our survey results show a shift underway, with another 41% of respondents mentioning that they plan to invest in digital twin technologies to model the effects of energy efficiency retrofits, optimize energy efficiency,63 and gauge how these initiatives could advance their net-zero objectives more realistically.

Actionable guidance to consider

- Some organizations may choose to focus sustainability investment only on a few properties or technologies However, taking a more integrated approach by including core accounting reporting, tax and regulatory, operations, or strategy functions while seeking synergies between multiple properties and across the business can be critical to managing climate risks and achieving targets.

- Green bonds, loans, or government-backed programs can help finance sustainability initiatives.64 Sustainability-linked bonds consider building performance metrics and coupon adjustments based on targets achieved. The issuance of sustainability-linked bonds for 2023 continued to exceed pre-pandemic levels at US$66 billion, well above the US$9 billion from 2020, even though they were down 14% year over year, likely due to the elevated interest rate environment.65 CRE owners may have to carefully assess the incentives and financing options available and seek independent verification on asset performance and reporting to comply with funding terms.

- When considering deep energy retrofits, there may need to be an adjustment in mindset from typical investment hurdles (that is, those in new acquisition, development, expansion, or renovation). This could include more regular exercises in benchmarking, scenario analysis and target setting, building construction of calibrated dynamic energy models, navigating the tenant/landlord split incentives barrier, and accessing and coordinating the use of multiple funding mechanisms.

- Accessing carbon markets through the purchase of carbon credits. Carbon markets can help in achieving net- zero goals while staying within the limits of the global carbon budget.66 It’s important to conduct due diligence before funding any project in the voluntary markets as they often lack uniform accreditation standards and supporting market infrastructure required for efficient trading.67

- Linking building performance with underwriting can potentially help secure better financing terms for retrofit opportunities. Digital twins and digital renovation passports, which are whole-life cycle repositories of building information on renovation and performance data, can both help plan and finance future retrofits. These tools not only facilitate enhanced data-sharing among stakeholders but also bolster the overall strategy by providing a clear, actionable view of performance metrics and improvement opportunities, which can increase exit values.

How can CRE be an attractive career destination for next-generation talent?

The commercial real estate industry is facing a retirement cliff. In the next decade, 40% of the US industry workforce will reach the age of retirement.68 Meanwhile companies are struggling to attract and retain the next generation of talent.69 As detailed in Deloitte’s 2024 real estate workforce prediction, in order to help bridge this gap, real estate companies should align with the expectations of the next generation and take steps now to fortify their talent pipelines.70 These steps can include a combination of integrating the values and priorities of Gen Zers and millennials into the company culture and modernizing technological capabilities to help drive efficiency and upskill current team members.

Aim to meet the expectations of the next generation of talent

As real estate organizations look to reinvigorate their workforce for this shift, they should consider the alignment between the values of the next generation of real estate professionals and the needs of the organization. According to Deloitte Global’s 2024 Gen Z and Millennial Survey,71 they value climate action, mental health, and work/life balance. Seventy-six percent of respondents surveyed by the Commercial Real Estate Women Network noted that their organizations have policies or benefits that support mental health and well-being, such as employee assistance programs, but that the majority of their respondents still wished their company would offer more mental health benefits.72

But there’s more: Gen Zers and millennials are even willing to reject a potential employer based on personal and ethical beliefs, and this number continues to increase. Forty-four percent of Gen Z respondents and 40% of millennials would reject an employer for a disconnect in values, up from 39% and 34%, respectively, in 2023.73

They’ve also expressed optimism—albeit with some concern—around the use of generative AI in the workplace, with 80% of Gen Z gen AI users believing that gen AI will free up their time and improve work/life balance. Nearly 60% of Gen Zers and millennials are expecting that gen AI will impact their career trajectories and require them to learn new skills. However, that same survey revealed that only 51% believe their employers are training them on the capabilities and benefits of gen AI, resulting in a need for companies to lead the charge and differentiate on upskilling and reskilling to ensure that employees are set up for success in this new technological landscape.

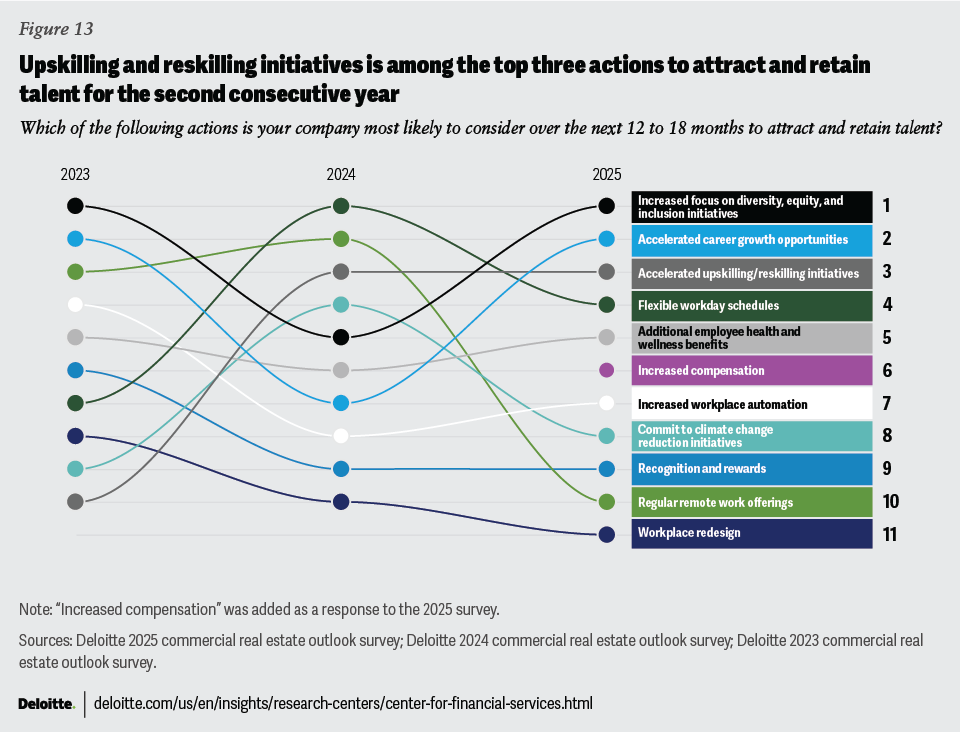

Upskilling for a digital real estate future

There has been a growing discrepancy between the skills that employers seek and the skills that job seekers bring to the table, a mismatch coined the “skills gap.”74 And more recent advances in digital technologies and automation, such as gen AI, have led businesses, including those in commercial real estate, to require new and evolving skills from their workforce. When it comes to top actions leaders at real estate organizations are planning to take to attract and retain talent over the past several years, “accelerated upskilling and reskilling initiatives” has remained a top three response for the past two years (figure 13). But when asked to rank what challenges their companies are facing most in building better technical workforce readiness, most respondents identified limitations from compensation practices, apprehensions around adopting new ways of working, and dependence on legacy technologies. The solution, however, could be more homegrown: reskill and upskill existing team members to help ensure that there is a strong, adaptable pipeline of talent for decades to come.

We are beginning to see signs of this shift, with real estate companies leaning more heavily on “property skills”—skills that are often essential to understanding marketplace dynamics and improving properties and their cash flows—than they may have in the past. When looking to upskill and reskill employees on new technologies, change management across the organization will likely be key. Senior leadership teams should set the tone by using the technology themselves, spending time on team well-being, creating a safe and innovative environment to experiment and learn, and believing in and explaining “why” the adoption will propel the team forward. As technology continues to evolve, so should the team members that use it.

Actionable guidance to consider

- There is a shift in the composition of the real estate talent pool, driven by the impending retirement cliff and demands from the next generation of talent. Leadership succession planning should be proactive, rather than reactive, and should be a board-level priority. Nearly 50% of succession plans for CEOs in real estate start from scratch, with a risk of notable business discontinuity if the timing of leadership transitions is misaligned.75 To further meet these demands, real estate organizations will need to provide a working environment that reflects the values of their people and look to harness technology at their fingertips.

- Make sure expertise does not walk out of the door before employees can reach their full potential as leaders at the organization. Promote knowledge-sharing and mentorship opportunities across all levels within the organization. Prioritizing the sharing of hard property skills such as knowledge of local market dynamics, understanding of supply and demand patterns, or property valuation methods will be imperative should more proactive capital allocation decisions come into play in the coming year.

- Shift toward a skills-based organization and away from a role-defined organization. Instead of having traditional job descriptions with defined tasks, consider identifying projects to be executed and problems to be solved, and seek out team members with skill sets that meet those discrete needs. Doing so may be a bridge across the skills gap, breaking down functional silos that may exist under traditional job descriptions, and allowing workers to operate with autonomy and agility.76

Is the CRE industry ready for the AI revolution?

A new era of artificial intelligence in real estate

Our 2025 survey revealed that the level of AI adoption in commercial real estate is still in its infancy, with 76% of respondents claiming their organizations are either researching, piloting, or in early-stage implementation of AI processes and solutions. Companies in early stages of AI adoption, particularly those in the pilot and research phase, are primarily focusing on leveraging AI for accounting and reporting (37%) closely followed by financial planning and analysis (36%) and risk management and internal audit (34%). Conversely, real estate companies that are more advanced in their AI journey—either in early-stage implementation or fully in production—are prioritizing financial planning and analysis (43%), risk management and internal audit (37%), and property operations (35%), over other areas such as accounting and reporting.

The benefits of AI adoption in commercial real estate are wide-ranging, and automation can make real estate decision-making processes more efficient and streamlined.77 Predictive forecasting for rent growth and the ability to analyze large volumes of data quickly are just some of the ways AI can contribute. Here are a couple of examples:

- Alpaca RE, a New York-based venture capital firm, launched an investing platform that allows it to capitalize on repricing opportunities in real estate by using AI to scrape unique data points from transaction records.78 This automation allows staff to focus on specific deals rather than spending time manually sifting through data.

- Brokerage firm JLL recently announced their own in-house large language model, JLL GPT. It has been leveraged for space utilization dashboards and to help generate insights. JLL predicts that it could eventually provide price modeling and predictions for investors, or matchmaking for leasing transactions.79

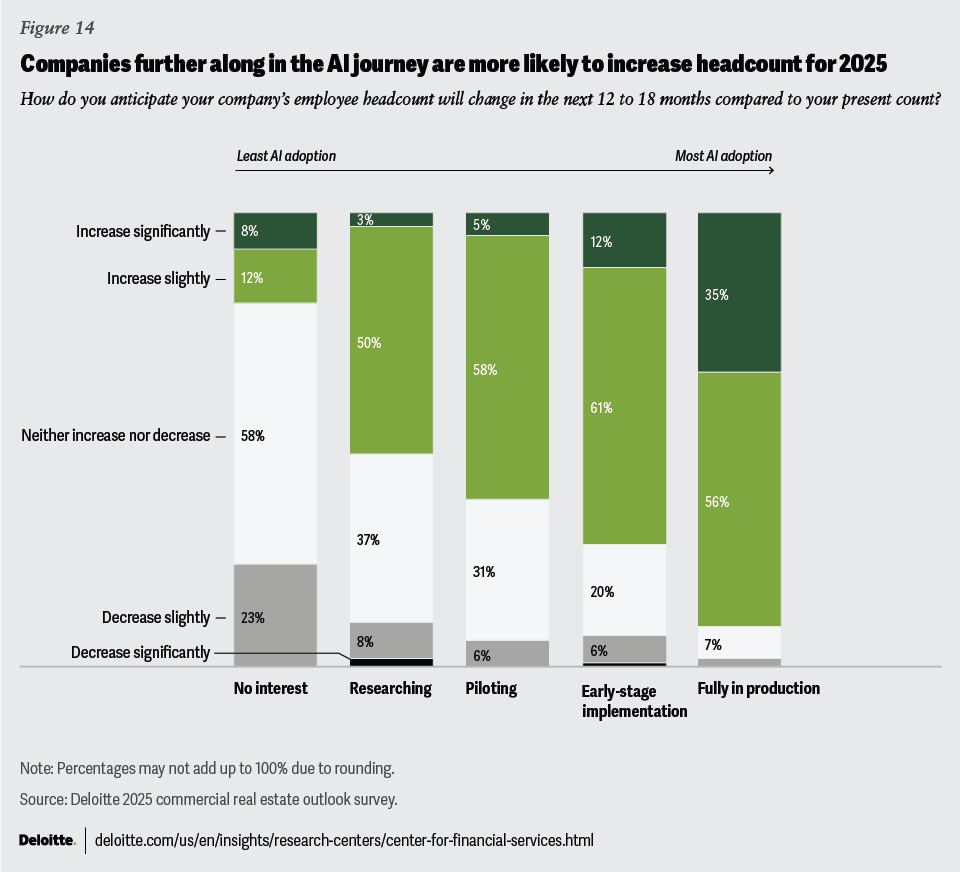

The use of AI could become an accelerator for real estate companies, freeing up employees’ time to work on value-add projects rather than onerous tasks. Survey respondents at companies further along in their AI journeys actually expect their headcounts to increase more drastically in the next 12 to 18 months than for those companies in the early stages (Figure 14).

Data is still the backbone

The enthusiasm around AI adoption is obvious—97% of the respondents are committed to AI-enabled solutions with a notable year-over-year increase in those who state that their companies are already in early-stage implementation (40%), up 12 percentage points from last year (28%). However, there are still obstacles, particularly with data quality and reliability. Real estate data has historically not been standardized and data fragmentation is a common issue.80 AI results rely on the data underpinning the results being accurate and complete, and bad data could be detrimental to both AI-generated content and the business decisions that are based on it. Real estate companies seem to be recognizing the need to improve data quality first, with respondents identifying data readiness and security/confidentiality as the top two challenges in scaling AI adoption.

Our survey revealed that many real estate companies acknowledge that there is work to be done before their data is “AI-ready”—with only 14% of respondents believing that their companies have well-structured data collection and management processes in place and robust privacy policies. However, there may be optimism that change could be coming as 88% of respondents are planning to use digital technologies to radically improve performance or reach of a company’s business over the next 12 to 18 months. Of those respondents, 51% say their main objective of increased investment is to use AI to automate processes, second only to improving the speed of dataflow for fast decision-making.

Progress toward gen AI readiness

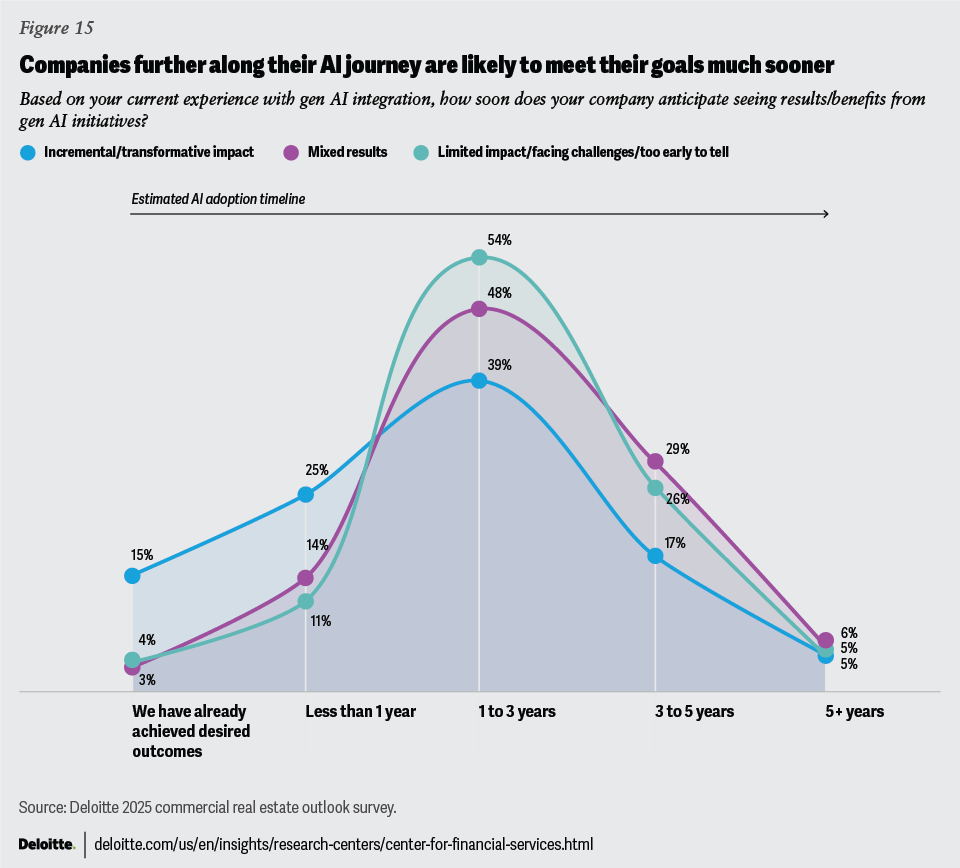

Despite these challenges, the real estate industry is starting to increase its AI adoption. And for those who believe that they are further along in their AI-adoption journey, 47% note that their benefits so far have been transformative. However, these cases are not in the majority, as real estate organizations are likely still ironing out the wrinkles in the AI-adoption process. A little more than half of our respondents (53%) cited challenges with implementation, less than expected impacts, or mixed results that still need to be overcome before realizing AI’s full potential.

Fifty percent of respondents estimate their companies are still one to three years away from fully realizing benefits from gen AI in particular, with another 25% stating that it will be another three to five years or beyond. Among those who have said they are already realizing some incremental or transformative impacts from gen AI, 40% have already met or expect to meet their end goals within the next year with another 39% saying that they are likely to get there within the next one to three years (figure 15).

While there may be challenges to immediate adoption, most notably with data readiness, there are seemingly no limits to exploring AI benefits. The industry is committed to the financial investment to make realizing AI’s full potential a reality. The widespread adoption of AI could be just the catalyst the industry needs to revolutionize the real estate technology landscape.

Actionable guidance to consider

- Determine if data is trustworthy, secure, accessible, and organized.81 Companies should standardize data and work to ensure its accuracy and reliability by critically evaluating where data is sourced and what data alliance partnerships can be made, if large scale data cleanup will be required to standardize and store data in one place, and what legal or ethical barriers may exist to using data in an AI model. These changes may be key to effectively scaling AI ambition.

- Tackle security and confidentiality head-on. These two concerns emerged as the greatest challenges in scaling gen AI implementation in our survey, and should include a thoughtful, proactive approach to ensure data remains secure.

- Think about change management—those actions companies take when making substantial adjustments within an organization82—early on and across the enterprise when considering investment in new technologies. With AI, work may be fundamentally changing, so it cannot be an afterthought. Here’s a framework that CRE companies can use to bring about change:83

- Define the outcome: Identify clear priorities and leaders to champion the change.

- Plan: Leverage leading industry practices to develop a data-driven strategy.

- Execute: Communicate and train the change program.

- Measure performance and reassess: Monitor progress, identify successes and challenges, and modify the program in real time.

Turning the corner on an uncertain past

Following several years of muted revenue growth, cutbacks in spending, and weakening fundamentals, there are indications that 2025 could be a year of revival for the global commercial real estate industry. Leaders should consider shifting from recent defensive approaches to more proactive strategies.

While full recovery of the industry is expected to be influenced by global geopolitical stability and interest rates over the coming 12 to 18 months, our survey respondents have indicated that there has been a positive change in sentiment on the prospects of real estate broadly. An increase in revenue growth and transaction activity could soon be at play. The link between sustainable investment and financial returns is becoming clearer. The next generation of real estate talent will likely have the tools at their disposal to change how this industry has always functioned. And artificial intelligence is changing how real estate organizations think about leveraging technology. Commercial real estate leaders who plan for the changes could be the ones best positioned to capitalize.

Methodology

The Deloitte Center for Financial Services conducted a survey of more than 880 C-level executives (CEOs, chief financial officers, and chief operating officers) and their direct reports at major commercial real estate owners and investment companies.

Respondents were asked to share their opinions on their organizations’ growth prospects and workforce, operations, and technology plans for the coming 12 to 18 months. We also asked about their investment priorities and anticipated changes for commercial real estate fundamentals.

Respondents were broadly based out of three regions: North America (Canada, Mexico, and the United States); Europe (France, Germany, the Netherlands, Spain, and the United Kingdom); and Asia Pacific (Australia, India, Japan, Mainland China, and Singapore).

The survey included real estate companies with assets under management of at least US$75 million and was fielded in June and July of 2024.

This article contains general information only and Deloitte is not, by means of this article, rendering accounting, business, financial, investment, legal, tax, or other professional advice or services. This article is not a substitute for such professional advice or services, nor should it be used as a basis for any decision or action that may affect your business. Before making any decision or taking any action that may affect your business, you should consult a qualified professional advisor.

Deloitte shall not be responsible for any loss sustained by any person who relies on this article.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}